Architectural Coatings Market Size and Growth Driven by Urbanization, Renovation Trends, and Sustainable Construction

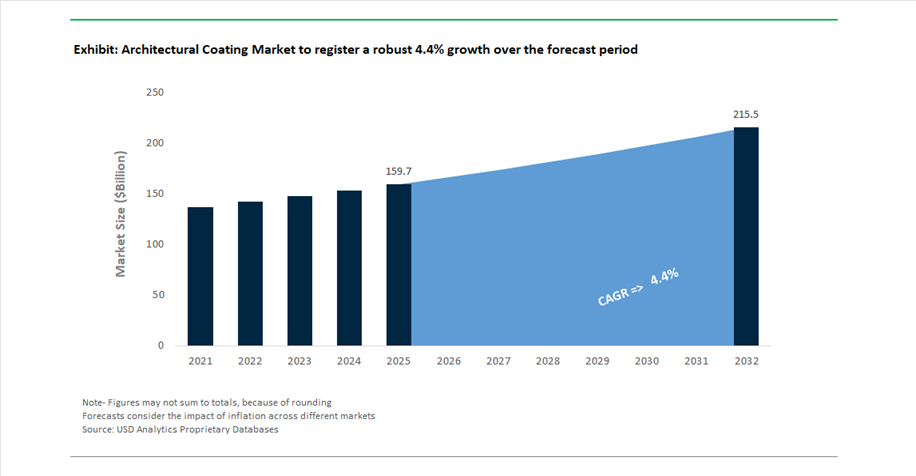

The Architectural Coatings Market is a large and mature segment, valued at USD 159.7 billion in 2025 and projected to reach USD 215.88 billion by 2032, expanding at a CAGR of 4.4%. Market growth is primarily underpinned by rapid urbanization, residential construction expansion, and increasing renovation and remodeling activities across both developed and emerging economies. As populations shift toward urban centers, demand for high-performance decorative and protective coatings in residential, commercial, and institutional buildings continues to rise.

Architectural coatings encompass a wide range of products including interior and exterior paints, primers, sealers, varnishes, and specialty coatings, all designed to provide aesthetic enhancement, weather protection, and surface durability. A major transformation within the market is the increasing preference for low-VOC, water-based, and environmentally compliant coatings, driven by stringent environmental regulations and growing consumer awareness around indoor air quality. Additionally, the integration of multi-functional properties—such as antimicrobial protection, heat reflectivity, moisture resistance, and self-cleaning surfaces—is redefining product innovation and value propositions.

The market is also witnessing strong demand for premium and customized finishes, supported by rising disposable incomes and changing consumer preferences toward design-led interiors and sustainable building materials. In parallel, the adoption of energy-efficient coatings, including solar-reflective and thermal-insulating paints, is gaining traction as governments and developers prioritize green building certifications and Net Zero construction goals.

Sustainability Innovation, Strategic M&A, and Premiumization Trends Reshaping Architectural Coatings Market

The architectural coatings market is undergoing a structural transformation driven by sustainability initiatives, strategic consolidation, and premium product innovation. Sustainability is emerging as a central competitive differentiator. In September 2025, AkzoNobel, Arkema, and BASF partnered to develop low-carbon powder coatings using bio-based resins and mass-balance certified raw materials. This initiative aligns with increasing demand for environmentally responsible construction materials and supports compliance with global ESG and green building standards. Complementing this, Hempel’s achievement of a 70% reduction in operational emissions enhances its positioning as a sustainability-focused supplier in the architectural coatings space.

Product innovation is increasingly focused on functional and design-oriented coatings. Asian Paints’ launch of “Moonlit Silk” (April 2026) reflects growing demand for aesthetic-driven interior solutions, while its Damp Proof range expansion introduces coatings that combine waterproofing with thermal reflectivity, capable of reducing surface temperatures by up to 10°C. Similarly, Hempel’s Farrow & Ball Flat Eggshell finish (March 2026) offers a durable low-sheen interior coating, addressing consumer demand for both aesthetics and performance.

Technological advancements are also enabling circular economy integration and energy-efficient applications. PPG’s ENVIROLUXE™ Plus coating (May 2025) incorporates recycled plastic content, demonstrating the industry’s move toward resource-efficient materials. Additionally, AkzoNobel’s October 2025 agreement to supply coatings for solar-absorbing wall technology highlights the convergence of coatings with energy generation systems, transforming building surfaces into active contributors to energy efficiency.

California’s 50 g/L VOC Cap Forcing Industry-Wide Transition to Waterborne Technologies

The architectural coatings industry is undergoing a decisive transformation as California’s South Coast Air Quality Management District enforces the 50 g/L VOC limit under updated Rule 1113. This regulatory benchmark is rapidly becoming the de facto standard across multiple U.S. regions, with over 22 of California’s 35 air districts adopting revised Suggested Control Measures that impose strict emission caps on flat, non-flat, and specialty coatings. These limits are effectively eliminating remaining solvent-borne formulations in architectural applications, accelerating the transition toward waterborne acrylic and high-solids polyurethane systems.

The formulation impact is significant. Manufacturers are increasing R&D investment by 15% to 20% to develop low-VOC and near-zero VOC resins that maintain key performance characteristics such as open time, flow, and leveling without relying on traditional coalescing solvents. This shift is particularly challenging in high-performance applications such as floor coatings and primers, where durability and application properties must be preserved under tighter chemical constraints.

Regulatory enforcement is backed by financial penalties. California imposes fees on manufacturers exceeding 250 tons of VOC emissions annually, creating strong economic incentives for rapid product reformulation and portfolio realignment. As a result, leading coating manufacturers have accelerated the commercialization of advanced water-reducible coatings, particularly in early 2026, to stay ahead of the elimination of small-container exemptions.

This regulatory environment is not only reshaping product chemistry but also redefining competitive positioning. Manufacturers capable of delivering high-performance, compliant coatings are gaining preferential access to regulated markets, making low-VOC innovation a central driver of growth in the architectural coatings industry.

Hollow Sphere Pigments Reducing TiO₂ Dependency and Enhancing Cost Efficiency

The architectural coatings market is witnessing a strategic material shift as manufacturers reduce reliance on titanium dioxide and adopt hollow sphere polymer pigments as cost-effective opacity extenders. Titanium dioxide, while highly effective for opacity and whiteness, is associated with price volatility and a high carbon footprint due to energy-intensive production processes. Hollow sphere pigments offer a viable alternative by leveraging air-filled void structures to enhance light scattering efficiency.

Advanced hollow sphere formulations with solids content exceeding 32% can replace up to 20% of titanium dioxide in a coating formulation without compromising hiding power or visual performance. This substitution delivers meaningful cost advantages, enabling manufacturers to reduce raw material costs by approximately $0.05 to $0.12 per gallon, a critical margin improvement in high-volume architectural coatings markets.

In addition to cost benefits, hollow sphere technology contributes to lightweighting. Coatings formulated with these pigments are 10% to 15% lighter than traditional high pigment volume concentration systems, reducing transportation costs and easing application for contractors. This is particularly relevant in large-scale construction projects where logistics and labor efficiency are key considerations.

Sustainability is another major driver. Reducing titanium dioxide content lowers Scope 3 emissions associated with raw material sourcing, supporting corporate decarbonization goals. As environmental, cost, and performance factors converge, hollow sphere pigments are emerging as a key innovation in architectural coatings, enabling manufacturers to optimize formulations while aligning with evolving sustainability standards.

Cool Roof Coatings Gaining Momentum with LEED v5 Climate Resilience Requirements

The introduction of LEED v5 is creating a strong growth opportunity for cool roof coatings, which are increasingly specified as part of climate-resilient building design strategies. Effective from July 1, 2026, LEED v5 mandates enhanced sustainability and resilience criteria, placing significant emphasis on reducing urban heat island effects and improving building energy efficiency.

Cool roof coatings with high Solar Reflectance Index values are playing a central role in achieving these objectives. These coatings can reduce roof surface temperatures by up to 30°C, resulting in a 10% to 15% reduction in building cooling energy demand during peak summer conditions. This performance not only contributes to energy savings but also enhances occupant comfort and reduces strain on HVAC systems.

LEED v5 also introduces new resilience-focused credits, such as Enhanced Resilient Site Design, which favor coatings that maintain long-term performance. As a result, formulations incorporating algae resistance and self-cleaning properties are gaining traction, as they ensure sustained reflectivity over service lifespans of up to 20 years. Market adoption trends indicate that approximately 40% of commercial specifiers now prioritize cool roof coatings supported by Environmental Product Declarations, reflecting a growing demand for transparent and quantifiable sustainability metrics.

Formaldehyde-Eliminating Coatings Driving Indoor Air Quality Innovation in Buildings

Indoor air quality is emerging as a critical differentiator in building design, driving demand for architectural coatings that actively remove pollutants rather than simply minimizing emissions. Formaldehyde-eliminating coatings represent a new generation of “active” surface technologies capable of chemically neutralizing airborne contaminants, particularly in residential, healthcare, and commercial environments.

These coatings utilize advanced scavenging mechanisms to convert formaldehyde into inert byproducts such as water vapor, achieving reductions of up to 70% in ambient concentrations within the first 24 hours of application. This capability is particularly relevant in modern buildings where off-gassing from furniture, adhesives, and engineered wood products contributes significantly to indoor pollution levels.

Regulatory developments are reinforcing this trend. The implementation of REACH Annex XVII Entry 77 in August 2026 introduces strict limits on formaldehyde emissions from indoor materials, creating a complementary role for air-purifying coatings in maintaining compliance. In parallel, the growing adoption of wellness-focused building standards, such as the WELL Building Standard, is driving demand for coatings that enhance occupant health and comfort.

From a commercial perspective, real estate developers are increasingly leveraging these technologies to differentiate properties. Buildings incorporating air-purifying coatings are achieving rental premiums of 3% to 5% in the “healthy building” segment. Additionally, these coatings offer long-term performance, remaining effective for six to ten years, providing sustained benefits without frequent reapplication.

Water-Borne Architectural Coatings Dominate with 64% Share Driven by Global VOC Regulations and Acrylic Innovation

Technology Analysis: Water-Based Acrylic Coatings Lead with Compliance and Performance Advantages

Water-borne coatings account for a dominant 64.0% share of the global architectural coatings market in 2025, primarily due to strict VOC (volatile organic compound) regulations across major regions including North America (OTC Phase II, SCAQMD), Europe (Deco Paint Directive), and China (GB 18582-2020 standards). These low-VOC, eco-friendly coatings are now the default choice for interior wall paints, exterior coatings, and decorative finishes, replacing traditional solvent-borne systems. Beyond compliance, water-based coatings offer significant advantages such as low odor, fast drying times, and easy soap-and-water cleanup, making them ideal for both DIY homeowners and professional contractors. Technological advancements in 100% acrylic emulsions and alkyd-modified acrylic hybrids have achieved full performance parity with solvent-based paints, delivering superior block resistance, flow and leveling, and long-term exterior durability (15–25 years). This convergence of regulatory compliance and high-performance coatings cements water-borne systems as the backbone of the architectural coatings industry.

Residential Sector Leads Architectural Coatings Market with 58% Share Driven by Repaint Cycles and Housing Growth

End-Use Sector Analysis: Residential Demand Fueled by Repainting Trends and Premium Coating Adoption

The residential segment dominates the architectural coatings market with a 58.0% share in 2025, driven by the vast global housing stock exceeding 2 billion residential units and consistent repaint cycles of 4–7 years for interiors and 8–12 years for exteriors. This segment includes interior wall paints, exterior house coatings, wood stains, deck coatings, and floor paints, making it the largest volume consumer of architectural coatings worldwide. Growth is further supported by new housing construction, adding approximately 60–70 million newly painted rooms annually, particularly in India, Southeast Asia, and North America. A key trend shaping 2025 is the “home improvement and hybrid work effect,” where increased time spent indoors is driving demand for premium, durable, and aesthetic coatings, including scrubbable matte finishes and antimicrobial interior paints. The segment is bifurcated into DIY high-volume paints and professional contractor-grade coatings, with “paint + primer in one” formulations emerging as a high-value solution, boosting efficiency and profitability in the residential architectural coatings market.

Architectural Coating Market Competitive Landscape Driven by Retail Expansion and Sustainable Formulations

The architectural coating market is driven by waterborne coatings, high-solids formulations, and digital color technologies. Leading companies are focusing on retail network expansion, contractor ecosystems, and sustainable coatings to address demand across residential, commercial construction, and infrastructure renovation segments.

Sherwin-Williams dominates architectural coatings with Sun Belt expansion and contractor ecosystem leadership

Sherwin-Williams holds a leading share in the architectural coatings market, supported by its expansive retail and contractor-focused ecosystem. The company is executing an aggressive strategy of 80–100 new store openings annually, concentrating on the U.S. Sun Belt and select Latin American markets to strengthen urban coverage. With over 5,000 company-operated stores, it delivers strong supply chain efficiency and rapid jobsite services. Financial performance remains stable with projected mid-single-digit growth and EBITDA margins in the low-to-mid 20% range for 2025–2026. Product innovation focuses on PFAS-free coatings and high-solids formulations to meet evolving EPA and EU regulations. The company continues to strengthen its leadership in residential repaint and renovation markets.

PPG Industries expands architectural coatings with digital color systems and global manufacturing investments

PPG Industries commands a share in the architectural coatings market, leveraging cross-segment integration and advanced coating technologies. The company achieved four consecutive quarters of organic growth leading into 2026, including a 3% increase in Q4 2025. Its MOONWALK® automated paint mixing system has reached over 3,000 installations globally, enhancing precision in custom architectural coatings. Strategic investments include a $380 million advanced coatings facility and a waterborne coatings plant in Thailand to capture Southeast Asian demand. The ENVIROLUXE™ Plus powder coatings incorporate recycled materials, aligning with LEED-certified construction requirements. Product development focuses on sustainable coatings and digital color innovation.

AkzoNobel strengthens architectural coatings with color leadership and energy-efficient technologies

AkzoNobel holds a leading share in the architectural coatings market, driven by its focus on aesthetic sustainability and operational efficiency. The company improved its adjusted EBITDA margin to 14.2% in 2025 through cost optimization and manufacturing modernization. Its “Rhythm of Blues™” 2026 color collection aligns with modern interior design trends, emphasizing coordinated wood finishes. A partnership with IPG Photonics introduces laser curing technology that reduces energy consumption in powder coatings by up to 30%. The company also supplies Calosol heat-absorbing coatings that convert building façades into energy-generating surfaces. Product development focuses on sustainable coatings and advanced architectural technologies.

Nippon Paint accelerates APAC architectural coatings growth through AI innovation and regional customization

Nippon Paint Holdings is a key growth driver in the architectural coatings market, particularly in APAC regions such as China and India. The company launched Phase II of its AI-driven collaboration with the University of Tokyo to develop low-VOC and CO2-reducing coatings. Its acquisition of AOC in 2025 expanded its presence in Europe and North America. Regional strategies include customized shade cards in multiple Indian languages with climate-specific coatings for diverse environmental conditions. The company is targeting a revenue growth, driven by infrastructure and non-residential construction projects. Product development emphasizes localized solutions and sustainable coating technologies.

Asian Paints leads regional architectural coatings with supply chain digitization and home solutions integration

Asian Paints Limited dominates the Indian architectural coatings market and is expanding across the Middle East and Africa. The company leads the waterborne coatings segment, driven by cost efficiency and environmental compliance in emerging markets. Its strong presence in the residential segment, with 63% market share, is supported by a highly localized distribution network reaching Tier-3 and Tier-4 cities. Business expansion includes integration of home décor, kitchen, bath, and lighting solutions to capture end-to-end home renovation demand. Investments in nanotechnology and UV-resistant coatings address performance requirements in tropical climates. Product development focuses on durability, affordability, and integrated home solutions.

United States Architectural Coatings Market: Ultra-Low VOC Regulations and Smart Coating Technologies Transforming Demand

The United States architectural coatings market is undergoing a structural transformation, driven by stringent environmental regulations and advanced material innovation. Tightening EPA and CARB mandates have established ultra-low VOC architectural coatings (≤80 g/L) as the industry benchmark, forcing the phase-out of high-solvent formulations and accelerating the shift toward sustainable coating chemistries. This regulatory landscape is positioning the U.S. as a global leader in low-VOC and PFAS-free architectural coatings, particularly in residential and commercial construction.

Innovation is further reshaping the market, with the introduction of carbon-negative bio-based paints that reduce the environmental footprint of building envelopes. The growing demand for cool roof coatings with high Solar Reflectance Index (SRI >110) is addressing urban heat island challenges across major metropolitan regions. Additionally, the integration of self-healing polyurethane coatings and antimicrobial architectural finishes is enhancing durability and indoor air quality in modern housing projects. Investments in automated tinting technologies are also improving supply chain efficiency, ensuring faster delivery of customized coatings for large-scale construction projects.

China Architectural Coatings Market: Green Building Mandates and Urban Renewal Driving High-Volume Demand

China continues to dominate the global architectural coatings market in terms of volume, supported by aggressive green building policies and large-scale urban renewal initiatives. The implementation of the GB 30981.1-2025 standard has significantly reduced allowable VOC levels, accelerating the transition toward waterborne and environmentally compliant coatings.

Government-backed urban renewal programs are creating strong demand for green-certified architectural coatings, with financial incentives encouraging adoption in residential renovation projects. Technological advancements such as aerogel-based thermal barrier coatings are improving building energy efficiency by reducing surface temperatures. Additionally, innovations in façade coatings, including sintered-stone and liquid-granite textures, are offering lightweight and low-carbon alternatives to traditional materials. The integration of AI-driven formulation platforms and mandatory use of anti-formaldehyde coatings in schools and hospitals further highlights China’s leadership in sustainable and high-performance architectural coatings.

India Architectural Coatings Market: Infrastructure Boom and Domestic Manufacturing Expansion Fueling Growth

India is emerging as one of the fastest-growing markets for architectural coatings, driven by large-scale infrastructure investments and rapid urbanization. The expansion of manufacturing capacity, particularly through projects like Birla Opus, has significantly increased domestic supply, reshaping competitive dynamics in the market.

Government initiatives such as the Pradhan Mantri Awas Yojana are creating sustained demand for both interior and exterior coatings across millions of housing units. The market is witnessing a shift toward climate-adaptive coatings, including high-performance acrylic resins designed to withstand extreme heat and monsoon conditions. Technological advancements in digital tinting and omnichannel distribution are improving accessibility in Tier-2 and Tier-3 cities. Additionally, the rise of professional painting services and vertical integration in raw material supply chains is enhancing efficiency and positioning India as a key growth hub in the global architectural coatings market.

Germany Architectural Coatings Market: Green Chemistry Leadership and Advanced Insulation Coating Systems

Germany remains the global benchmark for sustainable architectural coatings, driven by stringent environmental standards and advanced material innovation. National decarbonization targets are encouraging the adoption of carbon-sequestering lime-based coatings, which actively absorb CO₂ during curing, supporting the country’s climate goals.

The market is also characterized by high adoption of photocatalytic coatings that neutralize pollutants such as NOx and SOx, improving urban air quality. Innovations in mineral-silicate coatings are supporting heritage building restoration while maintaining breathability and durability. Additionally, the expansion of recycled-content paints and circular economy initiatives is reducing waste and improving sustainability. Government subsidies for energy-efficient retrofits are driving demand for advanced insulation coatings, reinforcing Germany’s leadership in eco-friendly architectural coating technologies.

Saudi Arabia Architectural Coatings Market: Mega-Projects and Extreme Climate Coatings Driving Demand

Saudi Arabia’s architectural coatings market is experiencing rapid growth, driven by large-scale infrastructure projects under Vision 2030. Mega-developments such as NEOM and Red Sea Global are creating significant demand for high-reflectivity solar-shielding coatings, designed to manage extreme desert temperatures and improve building energy efficiency.

Regulatory mandates are also shaping the market, with new requirements for intumescent fire-retardant coatings in high-rise buildings and public infrastructure. Investments in domestic manufacturing are strengthening supply chains, while the integration of smart coatings with embedded sensors is enabling real-time monitoring of structural performance. Additionally, the use of anti-carbonation coatings in transportation infrastructure is improving durability and longevity, positioning Saudi Arabia as a key market for advanced architectural coatings in extreme environments.

Japan Architectural Coatings Market: Nanotechnology-Driven Surfaces and Aging Population Solutions

Japan’s architectural coatings market is defined by its focus on advanced nanotechnology and solutions tailored to an aging population. The widespread adoption of self-cleaning photocatalytic coatings is enhancing building maintenance efficiency, particularly in high-rise urban environments.

Innovations in antimicrobial coatings are improving hygiene standards in residential and healthcare facilities, while ultra-matte finishes are catering to traditional design aesthetics. The development of flexible, crack-bridging coatings is enhancing seismic resilience, ensuring structural integrity during earthquakes. Additionally, near-zero odor coatings are enabling renovations in occupied spaces without disruption. Strong investments in bio-inspired surface technologies, including lotus-effect coatings, are further advancing performance and sustainability in Japan’s architectural coatings market.

Brazil Architectural Coatings Market: Mineral Resource Advantage and Infrastructure Expansion Driving Growth

Brazil’s architectural coatings market is leveraging its strong raw material base and expanding infrastructure investments to drive growth. The country’s abundant supply of titanium dioxide and minerals is enabling cost-effective production of high-performance coatings, giving domestic manufacturers a competitive advantage.

Infrastructure development programs, including public-private partnerships in sanitation and transportation, are boosting demand for durable architectural and protective coatings. Innovations such as anti-graffiti coatings are supporting urban maintenance, while antimicrobial coatings are gaining traction in agricultural storage facilities. Additionally, eco-certification programs promoting reduced solvent content are encouraging the adoption of sustainable coating solutions. These factors position Brazil as a key player in the global architectural coatings market.

United Kingdom Architectural Coatings Market: Graphene Innovation and Net-Zero Construction Driving Market Evolution

The United Kingdom architectural coatings market is evolving through strong innovation in graphene-based materials and stringent regulatory frameworks. The adoption of graphene-infused coatings is enhancing water resistance and thermal insulation, particularly in coastal and residential construction projects.

Government initiatives such as the Social Housing Decarbonization Fund are accelerating the use of anti-condensation and mold-resistant coatings in aging housing stock. Regulatory developments under the Building Safety Act and UK REACH framework are enforcing stricter safety and environmental standards. The growing shift toward e-commerce distribution channels is also transforming the market, improving accessibility for consumers. Additionally, the requirement for Environmental Product Declarations (EPDs) in public projects is driving transparency and sustainability, positioning the UK as a leader in next-generation architectural coatings.

Architectural Coating Market Report Scope

Architectural Coating Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$159.7 Billion

|

|

Market Size (2032)

|

$215.9 Billion

|

|

Market Growth Rate

|

4.4%

|

|

Segments

|

By Resin (Acrylic, Alkyd, Epoxy, Polyurethane, Polyester and Urethane Hybrids, Specialty Resins), By Technology (Water-borne, Solvent-borne, Powder Coatings, Radiation Curable Systems), By Functional Category (Paints, Primers and Sealers, Stains and Varnishes, Ceramic and Glass Coatings, Functional Coatings), By End-Use Sector (Residential, Non-Residential, Infrastructure and Public Works)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, PPG Industries, Inc., Akzo Nobel N.V., Nippon Paint Holdings Co., Ltd., Asian Paints Limited, RPM International Inc., Masco Corporation, Kansai Paint Co., Ltd., Jotun A/S, Hempel A/S, Axalta Coating Systems Ltd., BASF SE, Benjamin Moore & Co., DAW SE, Berger Paints India Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Architectural Coating Market Segmentation

By Resin

- Acrylic

- Alkyd

- Epoxy

- Polyurethane

- Polyester and Urethane Hybrids

- Specialty Resins

By Technology

- Water-borne

- Solvent-borne

- Powder Coatings

- Radiation Curable Systems

By Functional Category

- Paints

- Primers and Sealers

- Stains and Varnishes

- Ceramic and Glass Coatings

- Functional Coatings

By End-Use Sector

- Residential

- Non-Residential

- Infrastructure and Public Works

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Architectural Coating Market

- The Sherwin-Williams Company

- PPG Industries, Inc.

- Akzo Nobel N.V.

- Nippon Paint Holdings Co., Ltd.

- Asian Paints Limited

- RPM International Inc

- Masco Corporation

- Kansai Paint Co., Ltd.

- Jotun A/S

- Hempel A/S

- Axalta Coating Systems Ltd.

- BASF SE

- Benjamin Moore & Co

- DAW SE

- Berger Paints India Limited

*- List not Exhaustive

Table of Contents: Architectural Coatings Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Architectural Coatings Market Landscape & Outlook (2025–2032)

2.1. Introduction to Architectural Coatings Market

2.2. Market Valuation and Growth Projections (2025–2032)

2.3. Urbanization, Renovation Trends, and Housing Demand Dynamics

2.4. Regulatory Landscape: VOC Restrictions and Environmental Compliance

2.5. Sustainability Trends and Green Building Integration

3. Innovations Reshaping the Architectural Coatings Market

3.1. Trend: Low-VOC, Waterborne, and Sustainable Coating Technologies

3.2. Trend: Functional Coatings Including Antimicrobial, Self-Cleaning, and Heat-Reflective Systems

3.3. Opportunity: Cool Roof Coatings and Energy-Efficient Building Solutions

3.4. Opportunity: Formaldehyde-Eliminating and Indoor Air Quality Enhancing Coatings

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. R&D and Material Innovation

4.3. Sustainability and ESG Strategies

4.4. Market Expansion and Regional Focus

5. Market Share and Segmentation Insights: Architectural Coatings Market

5.1. By Resin

5.1.1. Acrylic

5.1.2. Alkyd

5.1.3. Epoxy

5.1.4. Polyurethane

5.1.5. Polyester and Urethane Hybrids

5.1.6. Specialty Resins

5.2. By Technology

5.2.1. Water-borne

5.2.2. Solvent-borne

5.2.3. Powder Coatings

5.2.4. Radiation Curable Systems

5.3. By Functional Category

5.3.1. Paints

5.3.2. Primers and Sealers

5.3.3. Stains and Varnishes

5.3.4. Ceramic and Glass Coatings

5.3.5. Functional Coatings

5.4. By End-Use Sector

5.4.1. Residential

5.4.2. Non-Residential

5.4.3. Infrastructure and Public Works

6. Country Analysis and Outlook of Architectural Coatings Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. UK

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Architectural Coatings Market Size Outlook by Region (2025–2032)

7.1. North America Architectural Coatings Market Size Outlook to 2032

7.1.1. By Resin

7.1.2. By Technology

7.1.3. By Functional Category

7.1.4. By End-Use Sector

7.2. Europe Architectural Coatings Market Size Outlook to 2032

7.2.1. By Resin

7.2.2. By Technology

7.2.3. By Functional Category

7.2.4. By End-Use Sector

7.3. Asia Pacific Architectural Coatings Market Size Outlook to 2032

7.3.1. By Resin

7.3.2. By Technology

7.3.3. By Functional Category

7.3.4. By End-Use Sector

7.4. South America Architectural Coatings Market Size Outlook to 2032

7.4.1. By Resin

7.4.2. By Technology

7.4.3. By Functional Category

7.4.4. By End-Use Sector

7.5. Middle East and Africa Architectural Coatings Market Size Outlook to 2032

7.5.1. By Resin

7.5.2. By Technology

7.5.3. By Functional Category

7.5.4. By End-Use Sector

8. Company Profiles: Leading Players in the Architectural Coatings Market

8.1. The Sherwin-Williams Company

8.2. PPG Industries, Inc.

8.3. Akzo Nobel N.V.

8.4. Nippon Paint Holdings Co., Ltd.

8.5. Asian Paints Limited

8.6. RPM International Inc

8.7. Masco Corporation

8.8. Kansai Paint Co., Ltd.

8.9. Jotun A/S

8.10. Hempel A/S

8.11. Axalta Coating Systems Ltd.

8.12. BASF SE

8.13. Benjamin Moore & Co

8.14. DAW SE

8.15. Berger Paints India Limited

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures