Asia-Pacific Water Treatment Chemicals Market: Value Analysis, Growth Trends, and Forecast to 2034

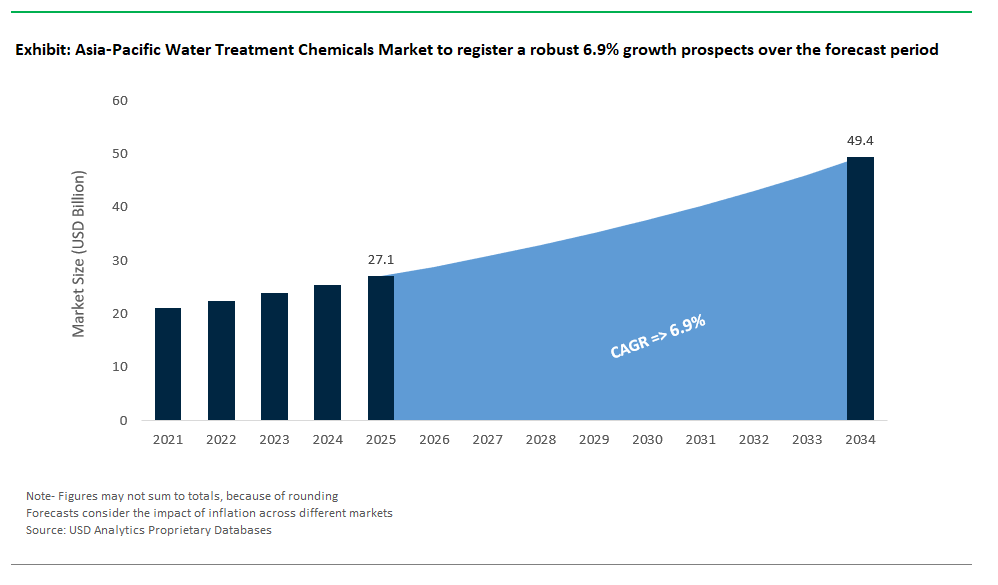

Asia-Pacific Water Treatment Chemicals Market Size is estimated at $27.1 Billion in 2025 and is forecast to register an annual growth rate (CAGR) of 6.9% to reach $49.4 Billion by 2034.

The Asia-Pacific water treatment chemicals market is undergoing a significant transformation, driven by a confluence of industrial expansion, regulatory tightening, and an accelerating shift toward sustainable treatment practices. Countries across the region are grappling with diverse water quality challenges ranging from high total dissolved solids (TDS) and microbial contamination to complex industrial effluents necessitating tailored chemical formulations for both municipal and industrial use. Core chemical categories such as scale and corrosion inhibitors, coagulants and flocculants, disinfectants, and sludge treatment additives remain central to treatment regimes, but regional disparities in feedwater composition, infrastructure maturity, and policy enforcement have led to distinct national strategies.

Corrosion and Scale Inhibitors- In countries like India and China, phosphonate-based formulations often blended with acrylic polymers remain widely used in industrial cooling systems and reverse osmosis pretreatment, where they are typically dosed at 5–10 ppm to control calcium scaling and maintain Langelier Saturation Index (LSI) within acceptable limits. However, growing concerns over phosphorous discharge are prompting a gradual shift toward biodegradable or phosphorous-free inhibitors, especially in water-stressed industrial zones. In Japan and South Korea, regulatory restrictions on zinc and phosphate discharges are more stringent, encouraging adoption of zinc-free, all-organic formulations and dispersants. These are especially relevant in electronics manufacturing regions where ultra-pure water standards are enforced.

Coagulants and Flocculants- Municipal treatment facilities across Southeast Asia and Australia continue to rely heavily on aluminum-based coagulants, such as polyaluminum chloride (PACl), to achieve compliance with drinking water turbidity limits (typically <0.5 NTU in line with WHO and local standards). In the industrial sector, particularly in sectors like pulp and paper and electronics, polyacrylamide-based flocculants and cationic polymers are commonly used for dewatering and sludge conditioning. Many facilities aim for 20–30% solids in dewatered sludge to comply with national waste disposal regulations, such as India’s Central Pollution Control Board (CPCB) standards.

Disinfectants and Biocides- Chlorine-based disinfectants dominate municipal water treatment across the region, but chloramines and alternative oxidants (e.g., chlorine dioxide) are increasingly used to address long-distance distribution and biofilm formation. In industrial applications, non-oxidizing biocides such as isothiazolinones and glutaraldehyde are employed in closed-loop cooling systems to prevent microbial fouling. In tropical regions, especially in urban centers like Singapore and Jakarta, Legionella control is mandated in high-risk cooling towers, encouraging routine biocide rotation and monitoring under health authority guidelines.

Sustainability and Green Chemistry- Growing awareness of environmental impact is driving interest in greener alternatives across the region. In India and parts of Southeast Asia, natural coagulants derived from plant sources (e.g., chitosan, tannin-based polymers) are being trialed at small-scale and rural treatment plants, though commercial-scale adoption remains limited due to higher costs and inconsistent performance. In Japan and South Korea, industrial wastewater treatment plants are integrating alkaline materials (such as calcium-rich industrial byproducts) to assist in heavy metal removal, a practice aligned with national circular economy frameworks. Regulatory push from agencies like Japan’s Ministry of the Environment and South Korea’s Ministry of Environment is fostering collaboration between academia and industry for low-toxicity, biodegradable treatment agents.

Digitalization and Material Innovation- Digital transformation is influencing chemical dosing and process optimization. China’s urban utilities are integrating online sensors (e.g., UV254, TOC analyzers) into smart water management systems, enabling more precise control of coagulant and disinfectant dosages. In South Korea and Australia, early-stage commercial trials of advanced adsorbents such as functionalized activated carbon and hybrid ion exchange resins are being conducted for contaminants like PFAS, arsenic, and heavy metals. These developments reflect the region’s interest in combining traditional chemistry with emerging materials science to address emerging contaminants and resource constraints.

Market Trend: Green Chemistry Gains Ground as Asia-Pacific Pursues Carbon-Neutral Water Treatment

The Asia-Pacific water treatment chemicals market is witnessing a decisive shift toward green chemistry as national decarbonization strategies and ESG mandates reshape procurement and formulation standards. Government-backed policies including China’s “Blue Sky Protection Campaign” and India’s growing emphasis on cleaner industrial production under its National Action Plan for Climate Change are accelerating the phaseout of traditional phosphate- and halogen-based chemistries in favor of biodegradable, low-toxicity alternatives. Key growth areas include polyaspartate- and glutamic acid–based scale inhibitors, next-generation biodegradable chelants, and plant-derived coagulants that align with local effluent discharge regulations and carbon-reduction goals. For example, readily biodegradable aminopolycarboxylates used as substitutes for EDTA and NTA are being deployed in high-precision sectors like semiconductor manufacturing in Japan and Taiwan. Meanwhile, regulatory revisions such as China’s surface water standard (GB 3838) and South Korea’s TMS-linked wastewater mandates are raising enforcement pressure on phosphorus-laden corrosion control products.

Southeast Asian economies including Vietnam and Indonesia are tightening industrial effluent norms. Vietnam’s Circular 08/2022, for instance, has introduced tougher permit renewal criteria tied to water reuse and toxicity metrics. These shifts have elevated environmental compliance from a peripheral concern to a board-level risk, especially in export-facing industries. At the corporate level, growing investor scrutiny reflected in increased disclosure under frameworks like MSCI ESG Ratings and CDP Water Security has catalyzed demand for water treatment products certified under ISCC PLUS, EcoLabel, or equivalent green certifications. As a result, green chemistry is increasingly viewed not merely as a regulatory safeguard but as a competitive differentiator within broader sustainability portfolios. This trend is set to accelerate, especially as regional markets align with global carbon-neutrality targets and Scope 3 emissions reporting becomes more mainstream.

Market Opportunity: Hydrogen Economy Triggers Surging Demand for Ultra-Pure Water Treatment Chemicals

Asia-Pacific’s rapid expansion of its green hydrogen sector is creating a new and highly specialized market for ultra-pure water (UPW) treatment chemicals, estimated to exceed $1.5–$1.8 billion over the next decade. As electrolyzer deployment scales up from alkaline to proton exchange membrane (PEM) and solid oxide (SOEC) technologies the requirement for ultrapure feedwater has intensified, with specifications typically demanding resistivity above 18 MΩ·cm, silica levels below 10 ppb, and near-zero boron and total organic carbon (TOC). These exacting standards are beyond the capability of conventional demineralization, driving adoption of tailored ion exchange resins, PFAS-free membrane conditioners, and low-fouling antiscalants designed specifically for electrolyzer systems.

Companies such as Lanxess, DuPont Water Solutions (AMBERLITE™), and Purolite are expanding their portfolios with nuclear-grade resins that meet semiconductor-level water standards, now repurposed for hydrogen production. For example, South Korea’s Doosan Fuel Cell mandates PFAS-free additives in its SOEC hydrogen plants, aligning with both domestic chemical safety regulations and export compliance needs. In Australia, hydrogen pilot projects under the HySupply framework are incorporating multi-stage polishing units with proprietary ion exchange systems capable of achieving sub-ppb boron levels, crucial for protecting sensitive electrodes.

This segment also intersects directly with carbon accounting. Several governments including Japan and China are incentivizing low-carbon hydrogen through subsidy mechanisms that include water treatment systems in the eligible scope. Japan’s “Green Innovation Fund” under NEDO, for instance, offers preferential support for projects using ISCC PLUS-certified inputs. Modular UPW systems from companies like Veolia and Suez are gaining traction for their ability to reduce chemical consumption via real-time conductivity and TOC feedback, improving electrolyzer performance by up to 0.3% efficiency per 1% gain in water purity (as estimated by the IEA). With electrolyzer OEMs increasingly embedding water treatment compatibility into performance guarantees, the UPW chemical segment is emerging as a strategic bottleneck and profit center within Asia-Pacific’s green hydrogen value chain.

Asia-Pacific Water Treatment Chemicals Market Competitive Landscape

The Asia-Pacific water treatment chemicals market features intense competition among global multinationals and locally established specialists. Differentiation relies on digital capabilities, water reuse integration, and adapting to regulations. Traditional value propositions like scale control, corrosion prevention, and managing microbes remain important. However, leading suppliers now compete on their ability to provide performance-focused, site-specific programs that meet stricter discharge standards and sustainability requirements in key markets such as China, India, and Southeast Asia.

Digital water management platforms have become a key area for differentiation. Technologies like real-time sensing, automated dosage control, and predictive analytics are transforming service delivery models. They also help providers build long-term relationships with customers. Companies with established offerings in this area backed by locally staffed service teams and solid remote monitoring systems have a competitive advantage, especially in industries with complicated system dynamics like power generation, petrochemicals, and steel. In these sectors, performance guarantees tied to key performance indicators such as water recovery, system uptime, and treatment efficiency are becoming standard in commercial contracts.

Localization of manufacturing and formulation capabilities is another important competitive factor. While global suppliers offer standardized chemicals with broad certifications, regional companies thrive with quicker responses, flexible batching, and the ability to customize solutions for different feedwater types, like high-silica or biologically active sources common in Southeast Asia and coastal India. Additionally, regional firms often align better with new national mandates on zero liquid discharge, sludge reduction, and low-phosphorus content. This alignment allows them access to public sector and mid-cap industrial contracts that prioritize local compliance over global branding.

Strategic partnerships and licensing agreements are also crucial in shaping competitive outcomes. Several international companies have teamed up with local water engineering firms, utilities, and EPC contractors to integrate their chemicals into wider turnkey water management systems. This ecosystem-based approach has helped them grow quickly in fragmented markets where direct sales can be limited by procurement rules or service delivery challenges. Meanwhile, some Asian companies are using innovative technologies like recyclable dispersants, biodegradable biocides, and hybrid corrosion inhibitors to expand beyond their home markets, often targeting areas with similar regulatory and operational issues.

Lastly, sustainability credentials are increasingly affecting competitive positions. Certifications aligned with ISO 14046 (water footprinting), UL ECOLOGO®, and local environmental labeling schemes have become crucial differentiators in large industrial bids. Companies that can connect their chemical programs with circular water strategies including reuse, sludge reduction, and brine concentration are more likely to succeed in obtaining contracts in export-oriented manufacturing hubs, where environmental audits and ESG metrics play a significant role in buyer agreements.

Asia-Pacific Water Treatment Chemicals Market – Segmentation Insights (2025–2034)

By Application: Industrial Water Treatment Drives Market Leadership

In 2025, industrial water treatment is projected to account for approximately 49.2% of the Asia-Pacific water treatment chemicals market. This dominance is driven by heavy chemical usage across power plants, chemical refineries, and high-tech manufacturing sectors especially in China and India. Cooling water and boiler water systems require continuous dosing of corrosion inhibitors, biocides, and scale control agents to meet both operational and regulatory standards. Municipal water treatment holds a significant share of around 38.4%, supported by investments in disinfection infrastructure, sludge dewatering, and the push for centralized sanitation. However, the water reuse and recycling segment is poised to be the fastest-growing, expanding at a CAGR of 8.1% between 2025 and 2034. Initiatives like China’s Sponge Cities and India’s Jal Jeevan Mission are fostering chemical demand for advanced tertiary treatment, nutrient stripping, and membrane protection. Desalination is also rising, with a CAGR of 13%, fueled by RO plant deployments in coastal and arid regions. The commercial segment sees steady demand for compact water systems in hotels, hospitals, and office complexes, especially for cooling tower and potable water maintenance.

.png)

By Form of Chemical: Liquid Formulations Lead the Asia-Pacific Market

Liquid formulations represent the dominant format in the Asia-Pacific market, accounting for approximately 67.8% of total chemical consumption in 2025. These formulations are preferred for their ease of integration into automated dosing systems, superior dissolution properties, and suitability for real-time control in smart water systems. They are especially favored in both municipal and industrial applications where dosing accuracy and fast reactivity are essential. As utilities and manufacturing plants adopt digital water platforms, liquid chemicals align well with trends in IoT-enabled treatment optimization. Powder and solid formulations make up the remaining 32%, used in bulk applications or remote areas where logistics and shelf stability are key. Solid coagulants, flocculants, and descalers are common in mining and decentralized municipal systems. Despite their operational limitations, they offer lower transportation costs and are often chosen in areas lacking dosing infrastructure. The market is expected to continue shifting toward liquid blends, especially as formulation science advances and hybrid chemicals with multifunctional properties become more prevalent.

Asia-Pacific Water Treatment Chemicals Report Scope

Asia-Pacific Water Treatment Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$27.1 Billion

|

|

Market Size (2034)

|

$49.4 Billion

|

|

Market Growth Rate

|

6.9%

|

|

Segments

|

By Type of Chemical (Coagulants and Flocculants, Corrosion and Scale Inhibitors, Biocides and Disinfectants, pH Adjusters and Softeners, Oxygen Scavengers, Defoamers and Antifoaming Agents, Membrane Cleaning Chemicals, Others), By Application (Municipal Water Treatment, Industrial Water Treatment, Commercial Water Treatment, Water Desalination, Water Reuse and Recycling), By Form of Chemical (Liquid, Powder/Solid), By Distribution Channel (Direct Sales, Distributors/Channel Partners, Online Sales

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ecolab Inc. (U.S.), Kurita Water Industries Ltd. (Japan), Kemira Oyj (Finland), Solenis LLC (U.S.), BASF SE (Germany), Ion Exchange (India) Ltd. (India), Veolia Water Technologies (France), Thermax Limited (India), SNF Floerger (France), The Dow Chemical Company (U.S.), Nouryon (The Netherlands),

|

|

Countries

|

China, India, Japan, South Korea, Australia, South East Asia

|

Asia-Pacific Water Treatment Chemicals Market Segmentation

By Type of Chemical

- Coagulants and Flocculants

- Corrosion and Scale Inhibitors

- Biocides and Disinfectants

- pH Adjusters and Softeners

- Oxygen Scavengers

- Defoamers and Antifoaming Agents

- Membrane Cleaning Chemicals

- Others

By Application

- Municipal Water Treatment

- Drinking Water Treatment

- Municipal Wastewater Treatment

- Industrial Water Treatment

- Power Generation

- Mining and Metallurgy

- Oil and Gas

- Food and Beverage

- Chemical and Petrochemical

- Pulp and Paper

- Pharmaceutical

- Electronics and Semiconductors

- Other Manufacturing Industries

- Commercial Water Treatment

- Water Desalination

- Water Reuse and Recycling

By Form of Chemical

By Distribution Channel

- Direct Sales

- Distributors/Channel Partners

- Online Sales

By Country

- China

- India

- Japan

- South Korea

- Australia

- South East Asia

- Rest of Asia

Top Companies in Asia-Pacific Water Treatment Chemicals Market

- Ecolab Inc. (U.S.)

- Kurita Water Industries Ltd. (Japan)

- Kemira Oyj (Finland)

- Solenis LLC (U.S.)

- BASF SE (Germany)

- Ion Exchange (India) Ltd. (India)

- Veolia Water Technologies (France)

- Thermax Limited (India)

- SNF Floerger (France)

- The Dow Chemical Company (U.S.)

- Nouryon (The Netherlands)

* List Not Exhaustive

Research Coverage

The Asia-Pacific Water Treatment Chemicals Market report provides a comprehensive analysis of the trends, opportunities, and challenges shaping water treatment in industrial, municipal, and commercial sectors. It examines market drivers such as industrial growth, stricter discharge regulations, and the transition toward green chemistry under regional sustainability frameworks. The research highlights technological shifts like digital dosing platforms, smart sensors, and hybrid chemical formulations, along with macro drivers including ESG mandates and decarbonization policies.

Scope Includes:

- Segmentation By Type of Chemical: Coagulants & Flocculants, Corrosion & Scale Inhibitors, Biocides & Disinfectants, pH Adjusters & Softeners, Oxygen Scavengers, Defoamers, Membrane Cleaners, Others.

- Segmentation By Application: Municipal Water (Drinking Water, Wastewater), Industrial Water (Power, Mining, Oil & Gas, Chemicals, Electronics, Pulp & Paper, Food & Beverage), Commercial Water, Desalination, Water Reuse & Recycling.

- Segmentation By Form: Liquid, Powder/Solid.

- Segmentation By Distribution Channel: Direct Sales, Distributors/Channel Partners, Online.

- Geographic Scope: Analysis of China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia

- Companies Covered: Ecolab, Kurita, Kemira, Solenis, BASF, SNF Floerger, Veolia, Thermax, Ion Exchange, The Dow Chemical Company, Nouryon.

- Study Period: Historic: 2021–2024; Forecast: 2025–2034

Methodology

The market analysis applies a bottom-up approach, aggregating chemical consumption by application sector and correlating it with plant capacities, chemical dosing norms, and treatment technologies across the region. Primary data sources include interviews with water treatment specialists, industrial engineers, and municipal utility managers, while secondary sources span regulatory documents, trade flows, and technical literature. Market projections consider variables such as urbanization trends, industrial water demand, adoption rates of advanced formulations, and regulatory timelines for ZLD and phosphorus restrictions. Data triangulation combines chemical import/export statistics, capacity expansions in power, oil & gas, and high-tech industries, and chemical pricing models to validate revenue estimates. Forecast scenarios account for technological shifts like PFAS-free chemicals, circular water systems, and green hydrogen-linked UPW demand, providing a robust and future-ready outlook.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements