Automotive Paints and Coatings Market Size and Growth Driven by Customization Trends and EV Design Evolution

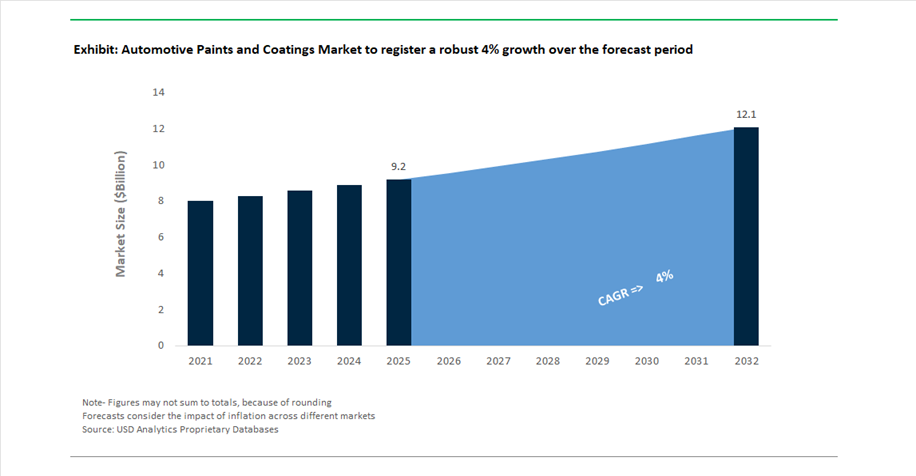

The Automotive Paints and Coatings Market is projected to grow from USD 9.2 billion in 2025 to USD 12.1 billion by 2032, registering a CAGR of 4%. This segment, covering primers, basecoats, and clearcoats, plays a critical role in delivering both aesthetic differentiation and long-term surface protection across passenger and commercial vehicles.

Market growth is increasingly influenced by the rising demand for vehicle customization, premium finishes, and differentiated color palettes, particularly in the passenger car and electric vehicle (EV) segments. Consumers are shifting toward matte finishes, metallic and pearlescent effects, and high-pigment coatings, pushing manufacturers to develop formulations with enhanced UV resistance, color stability, and scratch durability. At the same time, coatings must maintain performance under harsh environmental exposure, including temperature fluctuations, UV radiation, and chemical contaminants.

The transition toward EVs is further reshaping coating requirements. Modern EV designs emphasize aerodynamic surfaces, lightweight materials, and integrated sensor technologies, requiring coatings that support functional properties such as radar transparency, thermal management, and adhesion to advanced substrates. Additionally, sustainability is becoming a core focus, with increasing adoption of waterborne coatings, low-VOC formulations, and energy-efficient curing technologies to align with environmental regulations and OEM decarbonization goals.

The refinish segment also contributes significantly to demand, driven by vehicle parc expansion and repair cycles, where fast-curing, high-performance coatings improve body shop productivity and turnaround times. Competitive dynamics are defined by color innovation, material science advancements, and strategic collaborations with OEMs and EV manufacturers, positioning automotive paints and coatings as a key differentiator in modern vehicle design.

Color Innovation, Strategic Consolidation, and OEM Partnerships Transforming Market Dynamics

The automotive paints and coatings market is undergoing structural evolution driven by advanced pigment technologies, strategic mergers, and expanding OEM collaborations. A major industry development occurred in November 2025, when AkzoNobel and Axalta finalized a merger agreement, forming a global coatings leader with $17 billion in combined annual sales. This consolidation is expected to accelerate innovation in EV-focused coatings, high-durability finishes, and next-generation mobility solutions.

Another significant transformation is underway with BASF’s agreement with Carlyle Group and QIA (October 2025) to establish a standalone automotive coatings company, valued at €4.5 billion. This move is designed to create a focused global player dedicated to OEM and refinish coatings, enhancing specialization and innovation capabilities across the value chain.

Color innovation remains a central competitive lever. In February 2026, PPG introduced its “Secret Safari” color, a dynamic shade with light-responsive, chameleon-like properties, targeting luxury EV and off-road vehicle segments. Similarly, Axalta’s “Solar Boost” (2026 Color of the Year) reflects growing demand for bold, expressive finishes, particularly among younger consumers and EV buyers. BASF’s “Driving the Proxy” collection (October 2025) further demonstrates advancements in liquid-metal effects and radar-transparent coatings, supporting both aesthetics and functional integration for autonomous vehicles.

Strategic partnerships and regional expansion are strengthening market reach. PPG’s collaboration with Xiaomi (February 2026) to develop 100 new automotive colors highlights the increasing importance of localized design and rapid innovation cycles in the EV ecosystem. Meanwhile, Nippon Paint’s revenue growth (April 2026), driven by recovery in China’s automotive production, underscores the significance of Asia-Pacific as a core demand hub.

Corporate consolidation is also enhancing operational capabilities. Sherwin-Williams’ integration of Suvinil (January 2026) expands its footprint in Latin American automotive coatings, while Kansai Nerolac’s amalgamation with Nerofix (February 2026) strengthens its position in India’s automotive manufacturing ecosystem under the “One-Kansai” strategy.

Long-term OEM relationships continue to shape market dynamics. Axalta’s multi-year agreement with BMW Group ensures consistent deployment of premium refinish systems globally, reinforcing the importance of OEM-aligned coating technologies in maintaining brand consistency and quality standards.

China’s GB 30981.2-2025 Standard Driving Rapid Reformulation Toward Low-VOC Systems

The automotive paints and coatings industry is undergoing a significant regulatory shift in China with the enforcement of GB 30981.2-2025, effective June 1, 2026. This updated standard replaces GB 24409-2020 and establishes stricter limits on harmful substances in industrial coatings, including automotive refinish paints. The regulation introduces tighter thresholds on VOC content, formaldehyde, and heavy metals, aligning China’s coating standards more closely with global environmental benchmarks.

The reformulation impact is substantial. Industry assessments indicate that approximately 30% of existing solvent-borne refinish systems currently in use will require complete chemical redesign to meet the new compliance limits. This is accelerating the transition toward waterborne and high-solids coatings, particularly among leading manufacturers seeking to clear non-compliant inventory ahead of enforcement deadlines. The regulatory framework also mandates comprehensive hazard classification labeling, requiring manufacturers to provide verifiable documentation of chemical composition and safety compliance.

This shift is not purely regulatory—it is also strategic. Manufacturers that successfully transition to compliant formulations gain a competitive advantage in both domestic and export markets, where environmental compliance is increasingly a prerequisite. The enforcement of GB 30981.2-2025 is therefore acting as a catalyst for innovation, driving the adoption of safer, lower-emission coating technologies across China’s automotive sector.

Waterborne Migration in Mexico Accelerating Green Automotive Manufacturing

Mexico’s role as a global automotive production hub is driving a parallel transformation toward sustainable coating technologies, particularly through the adoption of waterborne basecoat systems. This transition is closely tied to the “Green Supply Chain” requirements imposed by export markets such as the United States, Canada, and the European Union, which collectively account for approximately 80% of Mexico’s automotive exports.

The shift to waterborne coatings is delivering measurable operational and environmental benefits. Automotive assembly plants that have fully transitioned to aqueous-based coating systems are reporting reductions of up to 70% in solvent emissions, significantly lowering their environmental footprint. Additionally, waterborne systems enable a reduction in paint shop energy consumption by approximately 20%, primarily through the elimination of high-temperature flash-off stages required for solvent evaporation.

This transformation extends beyond OEM manufacturing into the refinish segment. Approximately 15% of high-volume body shops in key industrial regions such as Monterrey and Puebla have upgraded to waterborne mixing systems, ensuring compatibility with modern factory-applied coatings and meeting evolving regulatory standards.

The alignment of Mexican manufacturing practices with global environmental requirements is reinforcing its position as a preferred production base for automotive OEMs, while simultaneously accelerating the adoption of low-emission coating technologies across the region.

Self-Healing Clearcoats Introducing Smart Surface Technologies in Premium Vehicles

The emergence of self-healing clearcoats represents a major innovation in automotive surface engineering, particularly within the premium and electric vehicle segments. These coatings utilize dynamic covalent bonding mechanisms, enabling reversible chemical interactions that allow the coating to repair surface damage such as micro-scratches and swirl marks when exposed to heat or sunlight.

Performance improvements are significant. Self-healing clearcoats can achieve up to 95% gloss recovery without the need for mechanical polishing, maintaining a high-quality finish throughout the vehicle’s lifecycle. In long-term durability testing, these coatings demonstrate up to 70% greater surface integrity over a 10-year period compared to conventional high-solids clearcoats, making them highly attractive for luxury automotive applications.

Sustainability benefits further strengthen their value proposition. By reducing the need for repainting and abrasive maintenance processes, self-healing coatings can lower a vehicle’s lifecycle maintenance carbon footprint by up to 12%. This aligns with broader industry efforts to reduce environmental impact across the entire vehicle lifecycle.

Market adoption is accelerating rapidly. By 2026, approximately 20% of premium vehicles incorporate some form of self-repairing coating technology, signaling a transition from experimental innovation to mainstream application. This trend reflects growing consumer demand for durable, low-maintenance finishes and positions self-healing coatings as a key differentiator in high-end automotive design.

Low-Temperature Cure Clearcoats Enabling Lightweight Composite Integration

The increasing use of lightweight materials such as carbon fiber reinforced polymers in automotive design is creating strong demand for low-temperature cure clearcoats. Traditional curing processes, which typically operate at around 140°C, can cause thermal degradation or outgassing in composite materials, compromising structural integrity and surface quality.

Low-temperature clearcoat systems, capable of curing at approximately 90°C, address these challenges by providing a safer thermal profile for heat-sensitive substrates. This enables the seamless integration of composite components into automotive manufacturing processes without requiring separate curing lines, improving production efficiency and flexibility.

The operational benefits are notable. By reducing curing temperatures, manufacturers can achieve energy savings of approximately 35% in the clearcoat application stage, contributing significantly to zero-carbon paint shop initiatives. Additionally, the ability to process both metal and composite components on the same line can increase overall plant throughput by around 15%, reducing production complexity and costs.

Importantly, performance parity has been achieved. Advanced two-component low-cure clearcoats now match the scratch resistance, chemical durability, and weathering performance of traditional high-temperature systems, meeting stringent OEM validation standards.

Basecoat Segment Leads Automotive Paints Market with 33.5% Share Driven by High-Value Pigments and Multi-Layer Color Systems

Coating Layer Analysis: Premium Pigment Technologies and Waterborne Systems Drive Basecoat Dominance

The basecoat segment commands a leading 33.5% share of the automotive paints and coatings market in 2025, driven by its central role in delivering vehicle aesthetics, color differentiation, and premium visual effects. This layer contains high concentrations of expensive pigments such as aluminum flakes, mica, Xirallic pigments, and high-performance organic and inorganic colorants, making it 3x–6x more costly per liter than primer or electrocoat layers. In 2025, over 80% of OEM basecoat applications are waterborne, ensuring compliance with stringent VOC regulations while introducing greater application complexity, including humidity-controlled environments and precision robotic spraying. A major value driver is the rise of tri-coat and quad-coat systems, which significantly increase material usage and enable premium finishes commanding $500–$1,500 per vehicle. Additionally, compact 3-wet paint processes integrate primer functionality into basecoat layers, further consolidating value and reinforcing basecoat leadership in the global automotive coatings market.

Self-Healing Coatings Lead Smart Performance Segment with 41% Share Driven by Premium Automotive Finish Demand

Smart Performance Analysis: Advanced Clearcoat Technologies Enhance Durability and Consumer Appeal

Self-healing coatings dominate the smart performance segment with a 41.0% share in 2025, driven by increasing consumer demand for scratch-resistant and long-lasting automotive finishes. These coatings, typically based on elastomeric polyurethane or siloxane-polyurethane hybrid clearcoats, possess the ability to repair micro-scratches and swirl marks through heat activation, restoring surface smoothness when exposed to sunlight or warm temperatures. This technology is widely adopted as standard in luxury vehicles and offered as premium options in mass-market models, enhancing vehicle resale value and reducing maintenance costs. The growing prevalence of automated car wash systems, which can cause extensive micro-abrasions, has further accelerated demand for self-healing coatings, reducing visible damage by 70%–80%. Additionally, emerging innovations in thermal management coatings, particularly for electric vehicles, are expanding the smart coatings segment, reinforcing its importance in the automotive paints and coatings market.

Automotive Paints and Coatings Market Competitive Landscape Driven by EV Innovation, Digital Color Systems, and Sustainable Coating Technologies

The automotive paints and coatings market is advancing through OEM coatings, refinish coatings, electrocoat systems, and EV-specific solutions. Industry leaders are investing in radar-compatible coatings, low-bake technologies, AI-driven color matching, and sustainable formulations to enhance durability, energy efficiency, and next-generation vehicle aesthetics.

PPG leads automotive paints and coatings with radar-compatible technology and digital color ecosystems

PPG Industries dominates the automotive paints and coatings market with $15.9 billion in 2025 net sales and strong OEM growth in Asia. Its “Parallels” 2026 color strategy, featuring Secret Safari, reflects evolving EV color trends and biophilic design integration. Strategic partnerships with Chery and Xiaomi to co-develop 100 new colors strengthen its position in the Chinese EV ecosystem. The MOONWALK automated mixing system, with 3,500 installations, delivers a 15% reduction in material waste in refinish operations. PPG’s radar-compatible coatings enable seamless ADAS functionality without signal interference. Product innovation focuses on digital color development, autonomous compatibility, and high-performance coatings.

BASF strengthens automotive coatings leadership with electrocoat dominance and low-bake sustainability

BASF Coatings is advancing automotive paints and coatings through its standalone operational model and sustainability-driven innovation. The “Driving the Proxy” collection showcases advanced interference pigments that create liquid-metal visual effects for modern vehicles. BASF leads the cathodic electrocoat segment with CathoGuard 800, used on over 100 million vehicles globally for corrosion protection. Its biomass balance approach supports OEM Scope 3 emission reduction goals by replacing fossil feedstocks. Increased R&D investment targets low-bake technologies that reduce curing temperatures to 100°C, cutting energy consumption by up to 30%. Product strategy focuses on efficiency, sustainability, and advanced coating performance.

AkzoNobel accelerates automotive coatings growth with merger strategy and bio-based innovations

AkzoNobel is strengthening its automotive paints and coatings portfolio through operational efficiency and strategic consolidation. The proposed merger with Axalta, expected to close in late 2026, aims to create a $25 billion global coatings leader. The company reported €10.16 billion in revenue and a 14.2% EBITDA margin, supported by strong cost optimization. Its “Rhythm of Blues” color series integrates bio-based resins to improve in-cabin air quality. AkzoNobel’s partnership with BYD enhances its position in the fast-growing Chinese EV export market. Product development focuses on sustainable coatings, color innovation, and OEM integration.

Axalta drives automotive coatings innovation with EV safety solutions and AI-based color precision

Axalta Coating Systems continues to lead innovation in automotive paints and coatings, supported by a record 22% EBITDA margin in 2025. Its 2026 Color of the Year, Solar Boost, highlights the shift toward expressive finishes in EV and lifestyle vehicles. The Alesta e-PRO range provides fire-resistant protection for EV batteries, addressing thermal runaway risks. Axalta’s TintMaster AI platform improves color accuracy by 29%, enabling efficient large-scale production. The company’s focus on UV-curable clearcoats enhances processing speed and scratch resistance. Product innovation centers on EV safety, digital color systems, and advanced coating technologies.

Kansai Paint expands APAC leadership with ultra-thin coating technologies and EV material integration

Kansai Paint maintains a strong position in automotive paints and coatings across Asia-Pacific, particularly in India and Japan. The company is shifting its portfolio toward OEM and industrial coatings, targeting a 50% business mix by 2026. Its “I-system” viscosity control technology enables metallic finishes at ultra-thin 1 μm thickness, significantly reducing material usage. Kansai has entered the lithium-ion battery materials segment with advanced dispersion technologies that improve performance. The RUBIGOL series strengthens its refinish coatings presence by enabling direct application over rust. Product development focuses on ultra-thin coatings, EV materials, and integrated automotive solutions.

China Automotive Paints & Coatings Market: Waterborne Shift and Smart Mobility Customization Driving Global Leadership

China dominates the automotive paints and coatings market, combining high-volume production with rapid technological advancement. The enforcement of GB 30981-2026 standards has triggered a 45% shift toward waterborne basecoats and low-VOC powder coatings, significantly improving environmental compliance across OEM plants. This transition aligns with China’s strategy to lead in sustainable EV manufacturing.

Innovation is increasingly focused on customization and smart mobility. Strategic collaborations—such as BASF with Xiaomi—are enabling mass customization of automotive colors, targeting next-generation consumers. Additionally, Chinese OEMs are pioneering radar-transparent pigments, allowing ADAS sensors to function without signal interference. The deployment of photocatalytic self-cleaning coatings across public fleets is reducing maintenance costs, while AI-enabled “digital twin” paint plants are optimizing pigment dispersion and reducing energy usage. These advancements position China as a leader in both scale and innovation.

United States Automotive Paints & Coatings Market: PFAS-Free Transition and Thermal Management Coatings Enhancing EV Efficiency

The United States automotive paints and coatings market is undergoing a strong regulatory-driven transformation. Following EPA directives, approximately 85% of fluoropolymer coatings have transitioned to PFAS-free alternatives, reshaping formulation strategies and accelerating sustainable coating adoption.

Technological innovation is centered on EV performance and manufacturing efficiency. The integration of infrared-reflective pigments is reducing cabin temperatures by up to 5°C, improving battery efficiency in hot climates. Advanced overspray-free coating technologies (e.g., ABB PixelPaint) are enabling precise application with near-zero waste. Additionally, the development of high-dielectric e-coats for EV battery enclosures is improving safety in high-voltage systems. The refinish segment is also evolving rapidly, with UV-cured coatings reducing repair times significantly, enhancing productivity in collision centers.

Germany Automotive Paints & Coatings Market: Biomass-Based Resins and Zero-Carbon Paint Shops Driving Sustainability

Germany remains the global benchmark for premium and sustainable automotive coatings, driven by advanced resin technologies and strict environmental standards. The widespread adoption of biomass-balanced clearcoats is reducing reliance on fossil fuels, aligning with Europe’s decarbonization goals.

The market is also characterized by high efficiency and innovation. The implementation of low-temperature curing (≈80°C) enables coating of multi-material vehicle bodies on a single production line, improving operational efficiency. Industry consolidation, including major mergers, is strengthening global competitiveness. Additionally, the use of anti-graffiti polyurethane coatings in public transportation and the alignment of paint shop efficiency with energy certification standards are reinforcing Germany’s leadership in sustainable automotive coating systems.

India Automotive Paints & Coatings Market: Capacity Expansion and EV Localization Driving Rapid Growth

India is emerging as one of the fastest-growing markets for automotive paints and coatings, driven by large-scale manufacturing expansion and government initiatives. The launch of Birla Opus’ 1,300+ million liter capacity has significantly disrupted pricing dynamics, especially in primer and basecoat segments.

Growth is being fueled by multiple factors. The expansion of refinish studios and paint protection services is catering to the rising luxury used-car market. Government-backed localization under the PLI scheme is driving demand for fire-retardant coatings for EV battery packs, while the two-wheeler segment is adopting UV-resistant coatings to withstand extreme climatic conditions. Additionally, the shift toward concentrated paint formulations is improving logistics efficiency and reducing carbon emissions, positioning India as a major growth engine in the global market.

Japan Automotive Paints & Coatings Market: Sensor-Compatible Pigments and Smart Surface Technologies Driving Precision

Japan leads in high-precision automotive coating technologies, particularly in sensor-compatible and multifunctional coatings. The development of radar-transparent pigments ensures seamless integration with autonomous driving systems, maintaining signal clarity without compromising aesthetics.

Innovation is also focused on advanced functionalities. The adoption of hydrophilic self-cleaning coatings is improving performance of cameras and LiDAR sensors in wet conditions. Japan is also advancing electrophoretic color-changing coatings, enabling vehicles to alter appearance dynamically. Additionally, the introduction of soft-touch antimicrobial interior coatings is enhancing hygiene in shared mobility applications. These advancements reinforce Japan’s leadership in precision and high-performance automotive coatings.

South Korea Automotive Paints & Coatings Market: Dielectric Coatings and OLED Integration Driving EV Innovation

South Korea is a global hub for advanced automotive paints and coatings, particularly in EV-focused technologies and display integration. The development of hybrid epoxy-silicone dielectric coatings is enabling reliable insulation for silicon carbide (SiC) power modules operating at high temperatures.

The market is also driven by strong synergy between coating and battery industries. Innovations such as fire-resistant coatings for battery systems are improving EV safety, while optically clear coatings for OLED dashboards are protecting next-generation display systems. Advanced application technologies like PECVD for 3D sensors are enhancing precision in autonomous vehicle components. Additionally, government incentives under the “Green New Deal” are accelerating the adoption of low-temperature curing coatings, reinforcing South Korea’s position as a leader in next-generation automotive coating technologies.

Automotive Paints and Coatings Market Report Scope

Automotive Paints and Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$9.2 Billion

|

|

Market Size (2032)

|

$12.1 Billion

|

|

Market Growth Rate

|

4%

|

|

Segments

|

By Coating Layer (Electrocoat (E-Coat), Primer Surfacer, Basecoat, Clearcoat), By Resin Chemistry (Acrylic, Polyurethane (PU), Epoxy, Alkyd and Polyester, Specialty Resins), By Technology Type (Water-borne, Solvent-borne, Powder Coatings, UV-Cured and Radiation Curable), By Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCV), Heavy Commercial Vehicles (HCV), Two-Wheelers and Three-Wheelers), By Sales Channel (OEM (Original Equipment Manufacturer), Automotive Refinish), By Smart Performance (Self-Healing Coatings, Thermal Management, Sensor-Compatible Coatings, Antimicrobial and Soft-Touch)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

PPG Industries, Inc., Akzo Nobel N.V., BASF SE, Axalta Coating Systems Ltd., The Sherwin-Williams Company, Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd., KCC Corporation, Jotun A/S, RPM International Inc., Asian Paints Limited, Berger Paints India Limited, Hempel A/S, Mankiewicz Gebr. & Co., Sika AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Automotive Paints and Coatings Market Segmentation

By Coating Layer

- Electrocoat (E-Coat)

- Primer Surfacer

- Basecoat

- Clearcoat

By Resin Chemistry

- Acrylic

- Polyurethane (PU)

- Epoxy

- Alkyd and Polyester

- Specialty Resins

By Technology Type

- Water-borne

- Solvent-borne

- Powder Coatings

- UV-Cured and Radiation Curable

By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles (LCV)

- Heavy Commercial Vehicles (HCV)

- Two-Wheelers and Three-Wheelers

By Sales Channel

- OEM (Original Equipment Manufacturer)

- Automotive Refinish

By Smart Performance

- Self-Healing Coatings

- Thermal Management

- Sensor-Compatible Coatings

- Antimicrobial and Soft-Touch

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Automotive Paints and Coatings Market

- PPG Industries, Inc.

- Akzo Nobel N.V.

- BASF SE

- Axalta Coating Systems Ltd.

- The Sherwin-Williams Company

- Nippon Paint Holdings Co., Ltd.

- Kansai Paint Co., Ltd.

- KCC Corporation

- Jotun A/S

- RPM International Inc.

- Asian Paints Limited

- Berger Paints India Limited

- Hempel A/S

- Mankiewicz Gebr. & Co.

- Sika AG

*- List not Exhaustive

Table of Contents: Automotive Paints and Coatings Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Automotive Paints and Coatings Market Landscape & Outlook (2025–2032)

2.1. Introduction to Automotive Paints and Coatings Market

2.2. Market Valuation and Growth Projections (2025–2032)

2.3. Market Drivers: Customization Trends, Premium Finishes, and EV Design Evolution

2.4. Regulatory Transformation: Low-VOC Transition and Environmental Compliance Standards

2.5. Technology Advancements: Radar-Transparent, Low-Temperature Cure, and Sustainable Coatings

3. Innovations Reshaping the Automotive Paints and Coatings Market

3.1. Trend: Color Innovation and Smart Coatings for Premium and EV Segments

3.2. Trend: Waterborne and Low-VOC Coating Technologies Driven by Global Regulations

3.3. Opportunity: Self-Healing Clearcoats and Smart Surface Technologies

3.4. Opportunity: Low-Temperature Cure Systems for Lightweight and Composite Materials

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. R&D and Material Innovation

4.3. Sustainability and ESG Strategies

4.4. Market Expansion and Regional Focus

5. Market Share and Segmentation Insights: Automotive Paints and Coatings Market

5.1. By Coating Layer

5.1.1. Electrocoat (E-Coat)

5.1.2. Primer Surfacer

5.1.3. Basecoat

5.1.4. Clearcoat

5.2. By Resin Chemistry

5.2.1. Acrylic

5.2.2. Polyurethane (PU)

5.2.3. Epoxy

5.2.4. Alkyd and Polyester

5.2.5. Specialty Resins

5.3. By Technology Type

5.3.1. Water-borne

5.3.2. Solvent-borne

5.3.3. Powder Coatings

5.3.4. UV-Cured and Radiation Curable

5.4. By Vehicle Type

5.4.1. Passenger Cars

5.4.2. Light Commercial Vehicles (LCV)

5.4.3. Heavy Commercial Vehicles (HCV)

5.4.4. Two-Wheelers and Three-Wheelers

5.5. By Sales Channel

5.5.1. OEM (Original Equipment Manufacturer)

5.5.2. Automotive Refinish

5.6. By Smart Performance

5.6.1. Self-Healing Coatings

5.6.2. Thermal Management

5.6.3. Sensor-Compatible Coatings

5.6.4. Antimicrobial and Soft-Touch

6. Country Analysis and Outlook of Automotive Paints and Coatings Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. UK

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Automotive Paints and Coatings Market Size Outlook by Region (2025–2032)

7.1. North America Automotive Paints and Coatings Market Size Outlook to 2032

7.1.1. By Coating Layer

7.1.2. By Resin Chemistry

7.1.3. By Technology Type

7.1.4. By Vehicle Type

7.1.5. By Sales Channel

7.1.6. By Smart Performance

7.2. Europe Automotive Paints and Coatings Market Size Outlook to 2032

7.2.1. By Coating Layer

7.2.2. By Resin Chemistry

7.2.3. By Technology Type

7.2.4. By Vehicle Type

7.2.5. By Sales Channel

7.2.6. By Smart Performance

7.3. Asia Pacific Automotive Paints and Coatings Market Size Outlook to 2032

7.3.1. By Coating Layer

7.3.2. By Resin Chemistry

7.3.3. By Technology Type

7.3.4. By Vehicle Type

7.3.5. By Sales Channel

7.3.6. By Smart Performance

7.4. South America Automotive Paints and Coatings Market Size Outlook to 2032

7.4.1. By Coating Layer

7.4.2. By Resin Chemistry

7.4.3. By Technology Type

7.4.4. By Vehicle Type

7.4.5. By Sales Channel

7.4.6. By Smart Performance

7.5. Middle East and Africa Automotive Paints and Coatings Market Size Outlook to 2032

7.5.1. By Coating Layer

7.5.2. By Resin Chemistry

7.5.3. By Technology Type

7.5.4. By Vehicle Type

7.5.5. By Sales Channel

7.5.6. By Smart Performance

8. Company Profiles: Leading Players in the Automotive Paints and Coatings Market

8.1. PPG Industries, Inc.

8.2. Akzo Nobel N.V.

8.3. BASF SE

8.4. Axalta Coating Systems Ltd.

8.5. The Sherwin-Williams Company

8.6. Nippon Paint Holdings Co., Ltd.

8.7. Kansai Paint Co., Ltd.

8.8. KCC Corporation

8.9. Jotun A/S

8.10. RPM International Inc.

8.11. Asian Paints Limited

8.12. Berger Paints India Limited

8.13. Hempel A/S

8.14. Mankiewicz Gebr. & Co.

8.15. Sika AG

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures