Automotive Specialty Coatings Market Size and Growth Driven by Functional Performance and Interior Comfort Trends

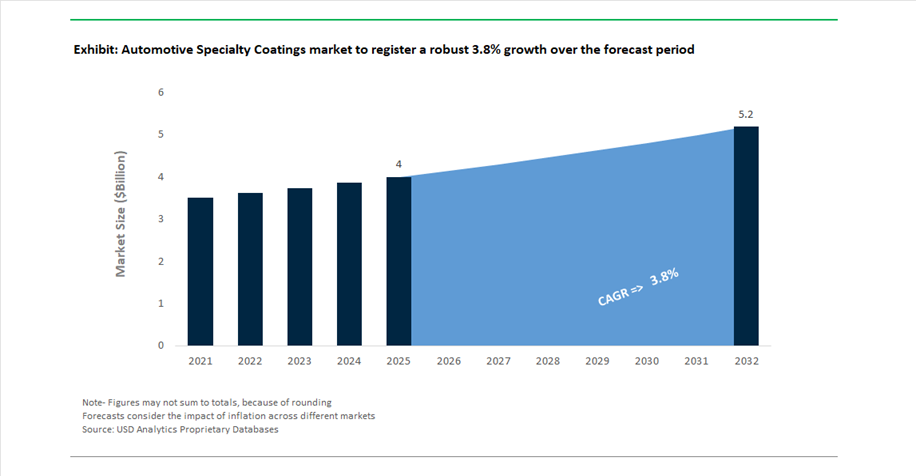

The Automotive Specialty Coatings Market is projected to grow from USD 4 billion in 2025 to USD 5.2 billion by 2032, registering a CAGR of 3.8%. This segment focuses on high-value, application-specific coatings that deliver targeted functional benefits beyond conventional decorative and protective layers, making it a critical enabler of next-generation vehicle design and user experience.

Specialty coatings are increasingly used to enhance vehicle safety, durability, and comfort, with applications including anti-fog coatings for headlights and sensors, anti-smudge and easy-to-clean interior surfaces, UV-resistant trims, and noise-damping underbody coatings. As automotive design evolves toward premium interiors and user-centric experiences, demand is rising for coatings that improve tactile feel, visual depth, and long-term surface performance. This is particularly evident in electric vehicles (EVs), where the absence of engine noise places greater emphasis on acoustic insulation and interior refinement, driving adoption of specialized damping coatings.

Technological advancements are enabling the development of multi-functional coatings that combine properties such as scratch resistance, anti-microbial protection, thermal management, and sensor compatibility. Additionally, sustainability is becoming a core focus, with manufacturers introducing bio-based resins, low-temperature curing systems, and high-solids formulations to reduce environmental impact while maintaining high performance. The integration of coatings with autonomous driving systems and advanced sensors is also driving demand for radar-transparent and optically optimized surfaces.

The market is further supported by increasing vehicle customization, rising EV penetration, and growing demand for differentiated finishes, particularly in premium and luxury segments. Competitive dynamics are shaped by innovation in material science, OEM collaborations, and expansion of specialty coating portfolios, positioning this segment as a key contributor to automotive value addition

Bio-Based Innovation, Functional Coating Technologies, and Strategic Collaborations Transforming Market Dynamics

The automotive specialty coatings market is undergoing transformation driven by sustainability innovation, advanced functional technologies, and strategic industry consolidation. A major development occurred in November 2025, when AkzoNobel and Axalta announced a merger of equals, creating a global coatings leader with enhanced capabilities in specialty and performance coatings. This consolidation is expected to accelerate innovation in high-value automotive coatings, particularly those designed for EVs and autonomous vehicles.

Sustainability is emerging as a key innovation driver. AkzoNobel’s commercialization of a bio-based interior coating for KIA (November 2024, expanded in 2026) represents a significant shift toward renewable raw materials, utilizing resins derived from rapeseed and pine rosin. Similarly, PPG’s “AAA” ESG rating (October 2024) highlights its leadership in developing low-energy curing and high-solids specialty coatings, enabling OEMs to reduce CO₂ emissions during production.

Functional innovation is central to market differentiation. BASF’s “Driving the Proxy” collection (October 2025) showcases coatings with liquid-metal effects and radar-transparent properties, enabling seamless integration of sensors in autonomous vehicles. In parallel, PPG’s “Secret Safari” color (February 2026) demonstrates advancements in chameleon-like coatings, offering dynamic visual effects that change under varying lighting conditions, particularly for high-end EVs and SUVs.

Strategic partnerships and motorsport collaborations are also influencing technology transfer. Sherwin-Williams’ extended partnership with the Mercedes-AMG PETRONAS Formula One Team (October 2025) focuses on ultra-lightweight specialty coatings, with innovations such as the Ultra 9K® system being adapted for commercial automotive applications. These coatings are engineered to withstand extreme thermal and aerodynamic conditions, providing insights for high-performance vehicle segments.

Regional growth and OEM demand are reinforcing market expansion. Nippon Paint’s revenue growth in China (April 2026) highlights strong demand for high-value specialty coatings driven by EV production and local automaker expansion. Additionally, Kansai Paint’s “GOING THROUGH” concept (April 2026) introduces advanced texture-driven coatings, emphasizing translucency, gloss depth, and human-centric haptics, aligning with future mobility design trends.

Investment in manufacturing and supply chain capabilities is also strengthening market positioning. PPG’s $380 million investment in a new coating facility (May 2025) supports increased production of specialized automotive finishes, particularly for EV battery and sensor-related applications. Meanwhile, Axalta’s Global Color Popularity Report (December 2025) highlights growing demand for functional individuality, with increased adoption of specialty chromatic finishes across key regions.

NMP Phase-Out Under EU REACH and TSCA Driving Transition to Safer Specialty Coatings

The automotive specialty coatings industry is undergoing a decisive chemical transition as N-Methyl-2-pyrrolidone (NMP) faces near-complete phase-out under EU REACH Restriction 71 and the U.S. EPA’s TSCA regulations. Historically used in high-performance wire coatings and anti-stick applications, NMP is now heavily restricted due to its reproductive toxicity profile, forcing a rapid shift toward safer solvent systems and alternative chemistries.

Regulatory thresholds are stringent. The EU has established Derived No Effect Levels at 14.4 mg/m³ for inhalation exposure and 4.8 mg/kg/day for dermal exposure, effectively limiting NMP concentrations to below 0.3% unless strict containment measures are implemented. In the U.S., TSCA regulations impose a de minimis threshold of 0.1%, requiring manufacturers to certify NMP-free formulations for new automotive OEM programs.

This regulatory pressure has triggered widespread reformulation. By early 2026, approximately 85% of major coating manufacturers have commercialized NMP-free systems, including waterborne and high-solids specialty resins that achieve comparable chemical resistance for under-the-hood applications. However, this transition has increased formulation complexity, particularly in applications requiring high thermal stability and solvent resistance.

The implications extend beyond compliance into procurement strategy. OEMs and Tier 1 suppliers are increasingly mandating NMP-free certification as a prerequisite for supplier qualification, making chemical compliance a core competitive differentiator. This shift is accelerating innovation in alternative solvent systems and reinforcing the industry’s move toward safer, environmentally compliant specialty coatings.

Zinc-Flake Coatings Replacing Chromate Systems in High-Performance Chassis Applications

The automotive specialty coatings market is also being reshaped by the global elimination of hexavalent chromium in pretreatment processes, driving the adoption of zinc-flake coating systems for chassis and fastener protection. These non-electrolytic coatings provide a high-performance, environmentally compliant alternative to traditional electroplating methods.

Performance improvements are substantial. Zinc-flake coatings now deliver neutral salt spray resistance exceeding 1,000 to 2,000 hours, significantly outperforming conventional electroplated coatings, which typically fail within 200 hours. This enhanced corrosion resistance is achieved at lower dry film thicknesses of 5 to 15 micrometers, enabling weight and material savings while maintaining durability.

Thermal stability is another key advantage. Advanced zinc-flake systems can withstand temperatures up to 300°C, making them suitable for components located near high-heat zones such as EV battery enclosures. Additionally, these coatings incorporate self-lubricating properties, achieving stable friction coefficients between 0.12 and 0.18. This eliminates the need for secondary lubrication or topcoats on critical fasteners, simplifying assembly processes.

Adoption rates reflect strong market momentum. As of 2026, the automotive sector accounts for approximately 45% of global zinc-flake demand, with a clear preference for water-based, chromium-free formulations that comply with RoHS and End-of-Life Vehicle directives. This transition is not only improving performance but also aligning coating technologies with global sustainability and regulatory requirements.

Laser-Activatable Coatings Enabling In-Mold Electronics and Smart Interior Surfaces

The rise of software-defined vehicles and seamless Human-Machine Interface design is creating a new class of functional coatings tailored for In-Mold Electronics (IME). Laser-activatable coatings and conductive inks are enabling the integration of electronic functionality directly into molded interior components, eliminating the need for traditional mechanical interfaces.

These coatings support Laser Direct Structuring processes, allowing conductive traces to be formed with precision levels as fine as 0.1 mm on complex three-dimensional surfaces. This enables the integration of capacitive touch controls, lighting elements, and sensor systems directly beneath decorative panels, supporting the trend toward “hidden-until-lit” interfaces in modern vehicle interiors.

Weight reduction is a key benefit. Replacing mechanical buttons and wiring harnesses with IME-integrated coatings can reduce the weight of center console assemblies by up to 70%, contributing to improved energy efficiency and extended driving range in electric vehicles. Additionally, these coatings are engineered for high formability, capable of withstanding elongation rates of up to 300% during thermoforming without cracking or loss of functionality.

The ability to integrate electronics into recyclable plastic substrates further enhances sustainability, aligning with circular economy objectives while enabling advanced interior design. As automotive interiors become increasingly digital and interactive, laser-activatable coatings are emerging as a critical enabling technology.

Anti-Scratch and Anti-Fingerprint Coatings Enhancing Durability of High-Gloss Interior Surfaces

The widespread adoption of high-gloss “piano black” finishes across automotive interiors has created a significant demand for advanced protective coatings that address durability and usability challenges. These surfaces, while visually appealing, are highly susceptible to micro-scratches, smudging, and wear, necessitating the development of specialized anti-scratch and anti-fingerprint coatings.

Next-generation UV-curable topcoats are delivering substantial performance improvements. With pencil hardness levels ranging from 2H to 4H, these coatings provide up to 40% greater scratch resistance compared to conventional clearcoats, ensuring long-term surface integrity in high-contact areas such as center consoles and infotainment panels. At the same time, oleophobic surface treatments are increasing the contact angle of skin oils to above 110 degrees, enabling easy-clean functionality and reducing visible fingerprint residue.

Operational benefits are also significant. OEMs integrating these coatings into production processes have reported a 15% reduction in scrap rates associated with surface damage during assembly and protective film removal. Additionally, self-healing variants of these coatings can repair micro-scratches at temperatures as low as 40°C, maintaining a high-gloss appearance over the vehicle’s lifecycle.

This combination of durability, aesthetics, and functional performance is positioning anti-scratch and anti-fingerprint coatings as essential components in modern automotive interior design, supporting both consumer expectations and manufacturing efficiency.

Protective Specialty Coatings Lead Automotive Specialty Market with 31.5% Share Driven by Corrosion Resistance and EV Battery Protection

Functional Category Analysis: Underbody Protection and Battery Coatings Drive Market Leadership

Protective specialty coatings account for a leading 31.5% share of the automotive specialty coatings market in 2025, driven by their essential role in corrosion prevention, impact resistance, and long-term vehicle durability. These coatings, including underbody PVC and polyurethane layers (500–1,500 microns), protect critical components such as wheel wells, rocker panels, and floor pans from stone chipping, road salt, and moisture intrusion. As OEMs increasingly adopt lightweight high-strength steel and aluminum, the need for advanced protective coatings has intensified due to higher susceptibility to corrosion. Additionally, cavity waxes and seam sealers prevent internal corrosion in structural components, ensuring long-term reliability. A major growth driver in 2025 is EV battery enclosure protection, where coatings provide dielectric insulation, abrasion resistance, and corrosion protection, preventing costly failures and safety risks. Backed by 10–12 year corrosion warranty mandates, these coatings remain indispensable in the global automotive coatings market.

Exterior Body and Trim Segment Leads with 29% Share Driven by Premium Finishes and Sensor-Compatible Coatings

Application Area Analysis: Aesthetic Innovation and ADAS Integration Fuel Demand

The exterior body and trim segment holds a 29.0% share of the automotive specialty coatings market in 2025, driven by consumer demand for premium aesthetics, customization, and advanced functional coatings. High-value applications include matte finish clearcoats, piano black coatings, and textured finishes used on SUVs, EVs, and luxury vehicles, with matte coatings commanding $500–$2,500 per vehicle. A key trend is the rise of sensor-compatible coatings, designed to support ADAS technologies such as radar, LiDAR, and cameras. These coatings ensure signal transparency by minimizing interference from metallic pigments, making them critical for autonomous and connected vehicles. Additionally, the global shift away from hexavalent chrome plating due to environmental regulations has accelerated adoption of coating-based alternatives, including PVD coatings with UV topcoats and high-gloss paint systems, enabling “dark chrome” and “black optic” finishes. This convergence of aesthetic innovation and functional performance drives strong growth in the automotive specialty coatings market.

Automotive Specialty Coatings Market Competitive Landscape Driven by EV Functional Coatings, Self-Healing Technologies, and Digital Color Innovation

The automotive specialty coatings market is advancing through radar-transparent coatings, self-healing coatings, low-bake primers, and EV battery protection systems. Leading players are focusing on functional coatings, antimicrobial and UV-resistant layers, and digital color technologies to enhance vehicle durability, safety, and next-generation automotive design.

PPG leads specialty coatings innovation with self-healing technologies and radar-transparent clearcoats

PPG Industries dominates the automotive specialty coatings market with $15.9 billion in 2025 net sales and strong focus on technology-advantaged coatings. The company is advancing radar-transparent clearcoats that ensure zero signal attenuation for Level 3 autonomous systems. A $300 million manufacturing expansion supports production of self-healing coatings using micro-encapsulation technology to repair surface damage. Strategic capital reallocation toward aerospace-grade specialty coatings enables cross-application into high-end automotive segments. PPG’s digital color ecosystem enhances styling precision while delivering 99% UV resistance. Product development focuses on functional coatings, autonomous compatibility, and durability.

BASF strengthens specialty coatings leadership with electrocoat systems and low-bake sustainable technologies

BASF Coatings is advancing automotive specialty coatings through its standalone operational model and sustainability-driven innovation. The company leads the electrocoat segment with CathoGuard systems designed for corrosion protection in multi-material EV architectures. Increased R&D investment supports low-bake specialty primers that reduce curing temperatures and energy consumption by up to 30%. BASF’s Verbund expansion in China strengthens supply of specialty plastic coatings for lightweight automotive interiors. Its strategic focus on green transformation aligns with OEM sustainability targets. Product development emphasizes efficiency, corrosion protection, and advanced material integration.

AkzoNobel drives specialty coatings growth with bio-based innovations and circular coating technologies

AkzoNobel is strengthening its specialty coatings portfolio through sustainability leadership and strategic consolidation with Axalta. The company raised €1.1 billion in 2026 to fund innovation and integration of specialty mobility assets. Its “Rhythm of Blues” collection incorporates bio-based resins that reduce VOC emissions by 40%, addressing the growing demand for healthy vehicle interiors. The Removing Coatings on Command technology enables easier recycling of advanced materials such as carbon fiber. Portfolio optimization includes divestment of non-core operations to focus on high-margin specialty coatings. Product development focuses on circularity, sustainability, and advanced functional coatings.

Axalta advances specialty coatings with EV safety solutions and AI-driven color precision

Axalta Coating Systems is a key innovator in automotive specialty coatings, supported by a record 22% EBITDA margin in 2025. Its Alesta e-PRO range provides dielectric insulation and fire resistance for EV battery enclosures, protecting against thermal runaway above 1200°C. The TintMaster AI platform improves specialty color matching accuracy by 29%, enabling consistent production for custom automotive applications. Axalta’s strong position in polyurethane coatings supports its leadership in heavy-duty and emergency vehicle segments. The company’s strategy focuses on expanding mobility coatings and EV-specific solutions. Product innovation centers on safety, performance, and digital integration.

Kansai Paint expands specialty coatings leadership with ultra-thin technologies and EV thermal solutions

Kansai Paint maintains strong growth in automotive specialty coatings across Asia-Pacific, supported by rising production and OEM demand. The company achieved a 10% increase in output in early 2026, targeting ¥605 billion in annual revenue. Its ultra-thin 1-micrometer coating technology delivers high-gloss metallic finishes with 50% lower material usage, improving cost efficiency. Kansai is advancing heat-reflective coatings that reduce cabin temperatures by up to 5°C, enhancing EV battery performance and range. Expansion in Southeast Asia strengthens its refinish coatings presence in high-growth markets. Product development focuses on lightweight coatings, thermal management, and sustainable solutions.

China Automotive Specialty Coatings Market: 800V EV Standardization and Smart Coating Ecosystems Driving Scale Leadership

China remains the global powerhouse in the automotive specialty coatings market, driven by its massive New Energy Vehicle (NEV) ecosystem and aggressive regulatory enforcement. The standardization of high-dielectric silicone-epoxy coatings for 800V battery systems (2026) is a major milestone, ensuring protection against electrical arcing in ultra-fast charging architectures. This is fundamentally reshaping coating requirements for EV electronics and battery safety.

Regulatory and technological shifts are accelerating innovation. Enforcement of GB 30981-2025 has triggered a 45% transition toward UV-curable and waterborne specialty coatings, particularly in major manufacturing hubs like the Pearl River Delta. Additionally, the commercialization of radar-transparent pigments that allow 77 GHz signals with minimal attenuation is supporting Level 3 autonomous driving. China is also advancing photocatalytic TiO₂ coatings for public EV fleets to reduce NOx emissions, while investments in nano-titania production are enabling air-purifying and antiviral coating solutions. These factors position China as the leader in high-volume, multifunctional specialty coatings.

United States Automotive Specialty Coatings Market: PFAS-Free Transition and EV Efficiency Coatings Driving Innovation

The United States automotive specialty coatings market is defined by sustainability mandates and performance-driven innovation. Following EPA directives, approximately 85% of specialty coatings have transitioned to PFAS-free formulations, reshaping material selection and accelerating environmentally compliant technologies.

Innovation is strongly tied to EV efficiency and advanced mobility systems. The adoption of infrared-reflective pigments is reducing cabin temperatures by up to 5°C, improving battery efficiency. Additionally, hydrophilic self-cleaning coatings for LiDAR and camera modules are enhancing ADAS reliability by preventing water streaks. Product innovation is also evident in coatings with microbicidal oxide additives for high-touch interior surfaces. The refinish segment is evolving rapidly with UV-cured coatings that reduce repair times from 40 minutes to under 5 minutes, improving productivity. Strategic investments in low-cure coatings for multi-material substrates further reinforce the U.S. as a leader in sustainable and high-performance specialty coatings.

Germany Automotive Specialty Coatings Market: Biomass-Balanced Resins and Zero-Carbon Paint Shops Leading Sustainability

Germany continues to set the global benchmark for automotive specialty coatings, particularly in sustainability and manufacturing efficiency. Leading OEMs have standardized biomass-balanced (BMB) clearcoats, replacing fossil-based inputs with renewable feedstocks derived from organic waste, aligning with net-zero goals.

Technological innovation is centered on efficiency and premium performance. The deployment of low-temperature curing (≈80°C) allows simultaneous coating of multi-material vehicle components, reducing production complexity. Additionally, advancements in ceramic-hybrid ultra-matte coatings are enhancing durability while maintaining premium aesthetics. Regulatory updates such as VDI 6022 (2026) are driving the adoption of biocide-free antimicrobial coatings in HVAC electronics. Consolidation among major chemical players is further scaling production of advanced specialty coatings, reinforcing Germany’s leadership in sustainable automotive coating technologies.

India Automotive Specialty Coatings Market: PLI-Driven Localization and Thermal Management Needs Driving Rapid Growth

India is emerging as the fastest-growing market in the automotive specialty coatings segment, supported by strong government incentives and expanding manufacturing capabilities. The $3.5 billion PLI scheme has significantly boosted domestic production of resins and pigments, reducing dependency on imports and narrowing the titanium dioxide supply gap.

Market growth is driven by infrastructure and EV adoption. The standardization of anti-corrosive polyurethane coatings for railway expansion and electric buses is creating strong demand. Additionally, the mandatory use of heat-reflective coatings for electric two-wheelers is addressing thermal challenges in extreme tropical climates. Regulatory updates are also increasing demand for low-migration specialty pigments in cold-chain transport applications. Digital transformation through tinting kiosks and experience centers is expanding access to customized specialty coatings, positioning India as a key growth hub.

Japan Automotive Specialty Coatings Market: Nanoscale Precision and Smart Surface Integration Driving Advanced Applications

Japan’s automotive specialty coatings market is defined by its leadership in nanoscale materials and precision engineering. Innovations such as Shin-Etsu’s MR-COAT series combine high hardness with exceptional elongation, reducing mechanical stress on miniaturized PCB components in advanced automotive electronics.

The market is also advancing in smart and multifunctional coatings. The development of optically clear conformal coatings for OLED dashboards is protecting next-generation displays, while antiviral smart glass coatings are enhancing passenger safety and comfort. Japan is also focusing on flexible, crack-bridging coatings for seismic resilience and waterborne polyisocyanate systems for zero-solvent high-performance coatings. Strategic stockpiling of critical materials is ensuring supply chain stability, reinforcing Japan’s position as a leader in high-precision specialty coatings.

South Korea Automotive Specialty Coatings Market: Self-Healing Polymers and Battery-Centric Coatings Driving EV Innovation

South Korea is a dominant force in the automotive specialty coatings market, particularly in functional polymer engineering and EV-focused innovations. The commercialization of self-healing elastomeric clearcoats that repair micro-scratches at room temperature is redefining durability in premium EV segments.

The market is also driven by strong integration with the battery ecosystem. Collaborations between coating companies and battery manufacturers are enabling EMI-shielding coatings for electronic protection and thermal-indicator paints that detect battery hotspots. Significant investments in smart wiring harness production are further advancing integrated shielding and coating systems. Regulatory standards such as the K-EV Safety Standard are enforcing high-performance requirements, including flame resistance for high-voltage systems. Additionally, the adoption of non-leaching antiviral coatings for ride-sharing vehicles highlights the growing role of multifunctional specialty coatings in modern mobility.

Automotive Specialty Coatings Market Report Scope

Automotive Specialty Coatings market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4 Billion

|

|

Market Size (2032)

|

$5.2 Billion

|

|

Market Growth Rate

|

3.8%

|

|

Segments

|

By Functional Category (Thermal Management Coatings, Smart and Adaptive Coatings, Functional Electronics Coatings, Aesthetic Specialty Finishes, Protective Specialty Coatings), By Resin Chemistry (Polyurethane (PU), Epoxy, Acrylic, Silicone and Silane-Modified, Fluoropolymers, Nano-Ceramics), By Technology (Water-borne, Solvent-borne, Powder Coatings, UV-Cured and Radiation Curable, Vapor Deposition), By Application Area (Exterior Body and Trim, Powertrain and Under-the-Hood, EV Battery and Power Electronics, Interior Cabin, Chassis and Wheels), By Vehicle Type (Passenger Vehicles, Light and Heavy Commercial Vehicles, Autonomous Mobility)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

PPG Industries, Inc., Akzo Nobel N.V., BASF SE, Axalta Coating Systems Ltd., The Sherwin-Williams Company, Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd., Mankiewicz Gebr. & Co., Sika AG, Fujikura Kasei Co., Ltd., Beckers Group, Henkel AG & Co. KGaA, 3M Company, KCC Corporation, Red Spot Paint & Varnish Co., Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Automotive Specialty Coatings Market Segmentation

By Functional Category

- Thermal Management Coatings

- Smart and Adaptive Coatings

- Functional Electronics Coatings

- Aesthetic Specialty Finishes

- Protective Specialty Coatings

By Resin Chemistry

- Polyurethane (PU)

- Epoxy

- Acrylic

- Silicone and Silane-Modified

- Fluoropolymers

- Nano-Ceramics

By Technology

- Water-borne

- Solvent-borne

- Powder Coatings

- UV-Cured and Radiation Curable

- Vapor Deposition

By Application Area

- Exterior Body and Trim

- Powertrain and Under-the-Hood

- EV Battery and Power Electronics

- Interior Cabin

- Chassis and Wheels

By Vehicle Type

- Passenger Vehicles

- Light and Heavy Commercial Vehicles

- Autonomous Mobility

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Automotive Specialty Coatings Market

- PPG Industries, Inc.

- Akzo Nobel N.V.

- BASF SE

- Axalta Coating Systems Ltd.

- The Sherwin-Williams Company

- Nippon Paint Holdings Co., Ltd.

- Kansai Paint Co., Ltd.

- Mankiewicz Gebr. & Co.

- Sika AG

- Fujikura Kasei Co., Ltd.

- Beckers Group

- Henkel AG & Co. KGaA

- 3M Company

- KCC Corporation

- Red Spot Paint & Varnish Co., Inc.

*- List not Exhaustive

Table of Contents: Automotive Specialty Coatings Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Automotive Specialty Coatings Market Landscape & Outlook (2025–2032)

2.1. Introduction to Automotive Specialty Coatings Market

2.2. Market Valuation and Growth Projections (2025–2032)

2.3. Market Drivers: EV Adoption, Interior Comfort Trends, and Functional Coating Demand

2.4. Regulatory Landscape: NMP Phase-Out, REACH and TSCA Compliance

2.5. Technology Evolution: Multi-Functional Coatings, Sensor Compatibility, and Sustainable Formulations

3. Innovations Reshaping the Automotive Specialty Coatings Market

3.1. Trend: Bio-Based and Low-VOC Specialty Coatings for Sustainable Mobility

3.2. Trend: Smart and Functional Coatings for ADAS, IME, and Interior Surfaces

3.3. Opportunity: Zinc-Flake and Chromium-Free Coatings for High-Performance Corrosion Protection

3.4. Opportunity: Anti-Scratch, Anti-Fingerprint, and Self-Healing Coatings for Premium Interiors

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. R&D and Material Innovation

4.3. Sustainability and ESG Strategies

4.4. Market Expansion and Regional Focus

5. Market Share and Segmentation Insights: Automotive Specialty Coatings Market

5.1. By Functional Category

5.1.1. Thermal Management Coatings

5.1.2. Smart and Adaptive Coatings

5.1.3. Functional Electronics Coatings

5.1.4. Aesthetic Specialty Finishes

5.1.5. Protective Specialty Coatings

5.2. By Resin Chemistry

5.2.1. Polyurethane (PU)

5.2.2. Epoxy

5.2.3. Acrylic

5.2.4. Silicone and Silane-Modified

5.2.5. Fluoropolymers

5.2.6. Nano-Ceramics

5.3. By Technology

5.3.1. Water-borne

5.3.2. Solvent-borne

5.3.3. Powder Coatings

5.3.4. UV-Cured and Radiation Curable

5.3.5. Vapor Deposition

5.4. By Application Area

5.4.1. Exterior Body and Trim

5.4.2. Powertrain and Under-the-Hood

5.4.3. EV Battery and Power Electronics

5.4.4. Interior Cabin

5.4.5. Chassis and Wheels

5.5. By Vehicle Type

5.5.1. Passenger Vehicles

5.5.2. Light and Heavy Commercial Vehicles

5.5.3. Autonomous Mobility

6. Country Analysis and Outlook of Automotive Specialty Coatings Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. UK

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Automotive Specialty Coatings Market Size Outlook by Region (2025–2032)

7.1. North America Automotive Specialty Coatings Market Size Outlook to 2032

7.1.1. By Functional Category

7.1.2. By Resin Chemistry

7.1.3. By Technology

7.1.4. By Application Area

7.1.5. By Vehicle Type

7.2. Europe Automotive Specialty Coatings Market Size Outlook to 2032

7.2.1. By Functional Category

7.2.2. By Resin Chemistry

7.2.3. By Technology

7.2.4. By Application Area

7.2.5. By Vehicle Type

7.3. Asia Pacific Automotive Specialty Coatings Market Size Outlook to 2032

7.3.1. By Functional Category

7.3.2. By Resin Chemistry

7.3.3. By Technology

7.3.4. By Application Area

7.3.5. By Vehicle Type

7.4. South America Automotive Specialty Coatings Market Size Outlook to 2032

7.4.1. By Functional Category

7.4.2. By Resin Chemistry

7.4.3. By Technology

7.4.4. By Application Area

7.4.5. By Vehicle Type

7.5. Middle East and Africa Automotive Specialty Coatings Market Size Outlook to 2032

7.5.1. By Functional Category

7.5.2. By Resin Chemistry

7.5.3. By Technology

7.5.4. By Application Area

7.5.5. By Vehicle Type

8. Company Profiles: Leading Players in the Automotive Specialty Coatings Market

8.1. PPG Industries, Inc.

8.2. Akzo Nobel N.V.

8.3. BASF SE

8.4. Axalta Coating Systems Ltd.

8.5. The Sherwin-Williams Company

8.6. Nippon Paint Holdings Co., Ltd.

8.7. Kansai Paint Co., Ltd.

8.8. Mankiewicz Gebr. & Co.

8.9. Sika AG

8.10. Fujikura Kasei Co., Ltd.

8.11. Beckers Group

8.12. Henkel AG & Co. KGaA

8.13. 3M Company

8.14. KCC Corporation

8.15. Red Spot Paint & Varnish Co., Inc.

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures