Market Overview: Mega Filtration Consolidation, Cleanroom Expansion, and Industrial Emission Controls Reshape Bag Filter Market

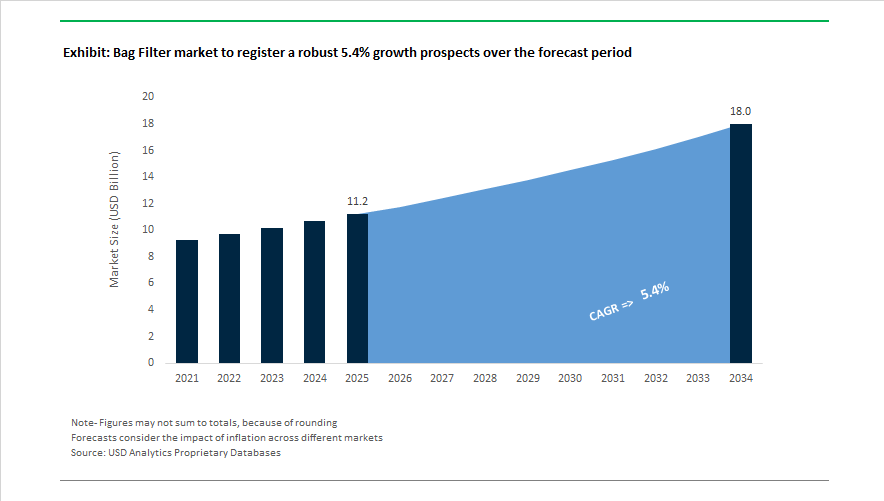

The bag filter market is valued at $11.2 billion in 2025 and is projected to reach $18 billion by 2034, registering a 5.4% CAGR. Market expansion is closely tied to industrial dust collection systems, baghouse filtration, air pollution control equipment, liquid bag filters, HVAC filtration, cleanroom filtration, pulse-jet baghouses, and high-temperature filter media. Structural consolidation accelerated in November 2025 when Parker Hannifin entered a definitive agreement to acquire Filtration Group Corporation for $9.25 billion, a transaction expected to close in 2026. This move expands Parker’s footprint in industrial filtration systems, aftermarket filter bags, and life sciences filtration technologies, strengthening global supply capabilities. Earlier, in 2024, Donaldson Company completed the acquisition of Univercells Technologies, integrating high-containment filtration platforms for advanced bioprocessing applications.

Product innovation intensified during 2025 as manufacturers focused on high-efficiency filter media, energy-efficient baghouse operation, and oil-absorbing filter technologies. In March 2025, Eaton introduced SENTINEL MAXPO and DURAGAF MAXPOXL polypropylene needle felt filter bags with melt-blown inner cores, enabling dual particle retention and oil absorption in paints and coatings lines. The company also launched TOPCART HF multi-cartridge housings in 2025, applying bag-style filtration principles to high-flow industrial water treatment and hydrogen pretreatment systems. Micronics Engineered Filtration Group expanded engineered baghouse solutions in 2025 to reduce pressure drop in cement and waste-to-energy plants, cutting fan energy consumption. BWF Envirotec advanced high-temperature Aramid and PTFE-coated filter bags in 2025, targeting biomass and incineration plants operating under severe thermal stress. Meanwhile, Freudenberg Performance Materials unified its global filter media portfolio under the Filtura brand in 2024, emphasizing customized nonwoven media for both air and liquid bag filtration.

Regional manufacturing and policy drivers reinforced demand through 2025–2026. Camfil expanded its Manesar facility in September 2025 with a new HEPA and ULPA production line, strengthening supply of high-efficiency pocket and bag filters for pharmaceutical cleanrooms. Later in 2025, Camfil introduced Hi-Flo XLT bag filters with recycled plastic frames and tapered pockets to improve airflow and meet Environmental Product Declaration requirements. Nederman MikroPul received Supplier of the Year recognition in February 2025 for long-term baghouse reliability in mineral processing. India’s National Clean Air Programme remained a central growth catalyst throughout 2025, pushing industries toward pulse-jet baghouses to meet a 40% particulate reduction target by 2026. Supporting this demand, Donaldson Company reported record fiscal performance in August 2025, citing mid-single digit growth in industrial air filtration for food processing and electronics manufacturing.

Trends and Opportunities Reshaping Growth in the Bag Filter Market

Market Trend: Mandated Retrofit and Capacity Upgrades Across the Cement Sector

Bag filters are becoming a regulatory necessity rather than an operational choice in high-emission industries, especially cement. In November 2025, GCCA confirmed a 25% reduction in CO₂ intensity since 1990. A key driver of this decarbonization progress is the transition from traditional ESP systems to Pulse-Jet Bag Houses engineered for sub-30 mg/Nm³ particulate emission levels.

India is a frontline example. Enforcement of 24x7 continuous monitoring (CEMS) by the CPCB compelled companies like Dalmia Cement to deploy multiple large bag houses and nuisance-dust collectors across more than 30 transfer locations per facility to comply with revised standards. North America is undergoing a parallel modernization cycle following the divestment and restructuring of FLSmidth’s cement division into Fuller Technologies in November 2025. Pacific Avenue Capital Partners is strategically focusing on monetizing retrofit demand by targeting the aging installed base that requires upgrades to remain eligible for industrial licenses and ESG financing.

Market Trend: Shift Toward High-Temperature and Chemically Resistant Filter Media

A structural shift in fuel mix toward biomass, MSW pellets, and waste-heat recovery is changing flue gas profiles. Operators in Waste-to-Energy and power generation now require engineered filtration materials capable of resisting acidic gas attack and temperature fluctuations above 260°C.

Policy is shaping this shift. India’s 2025 biomass co-firing mandate requires thermal plants to incorporate 5–7% biomass pellets, producing flue gas with higher chloride and moisture loads. Conventional polyester fabrics are failing prematurely, pushing procurement toward PTFE, P84® polyimide, and specialty glass felt blends.

At the 2025 Industrial Flue Gas Filtration Symposium, BWF Envirotec launched needlona BLUE, an engineered needle-felt media with a 10% lower CO₂ footprint and extended lifecycle performance. For operators facing rising carbon taxes and EU Green Deal-linked financial disclosures, lifecycle savings and ESG-scoring advantages are becoming key selection criteria. One talking point among OEMs is the shift from "purchase cost" to "cost per operational hour" as the new benchmark for media procurement.

Market Opportunity: ATEX-Certified Filtration Systems for Gigafactories and Battery Material Processing

Lithium-ion battery production is redefining particulate safety requirements. Cathode powders like NMC and LFP, as well as metallic anode materials, pose dust-explosion and worker-exposure risks. Since 2024, gigafactories have required ATEX-rated filtration solutions with fine-particle capture capability below 0.3 microns.

Donaldson Company’s Pune Experience Centre showcases a new wave of modular explosion-proof baghouses with embedded particulate-load sensors and automatic suppression systems. This technology is optimized for powder reclamation — providing a direct profit lever for cathode-active material plants where material recovery can offset filtration costs.

OEMs participating in the 2025 China–EU Battery Roundtable emphasized that filter manufacturers offering validated product-purity protocols (ISO-16232 cleanliness specifications) will win long-term supply contracts. For bag filter manufacturers, positioning as a contamination-control partner rather than a consumable supplier unlocks higher margin recurring revenue.

Market Opportunity: Filtration Infrastructure for Direct Air Capture (DAC) and Carbon Utilization

Direct Air Capture markets represent a future-facing filtration vertical. DAC units using solid sorbents require ultra-clean intake air to prevent fouling. With the world’s largest DAC plant in the United States scheduled to reach 500 kt CO₂ per year capacity in 2025, procurement for pre-filtration and sorbent-protection systems will scale rapidly. In parallel, Climeworks’ Zurich Innovation Center, inaugurated in December 2025, is dedicated to filtration efficiency optimization for DAC scale-up, signaling a pipeline of commercial filtration specifications soon to become industry standards.

Emerging research is broadening the addressable market beyond centralized DAC. In October 2025, Science Advances highlighted the potential of embedding carbon-capture filter media in existing HVAC systems using PEI-coated nanofiber technology. If adopted globally in institutional buildings, it could remove up to 596 million tons of CO₂ annually. For filter-bag manufacturers, this represents entry into a previously untapped built-environment infrastructure market, radically expanding demand beyond industrial stack filtration.

Bag Filter Market Share and Segmentation Insights

Type-Based Market Share: Pulse Jet Bag Filters Command 68% Amid Industrial Efficiency Upgrades

In 2025, pulse jet bag filters capture 68% of the global bag filter market, firmly establishing themselves as the preferred dust collection technology across cement plants, coal-fired power stations, and high-volume industrial processing units. Their high-energy compressed air cleaning mechanism enables continuous operation at elevated air-to-cloth ratios, reducing maintenance downtime and enhancing particulate capture efficiency under stringent emission norms. This operational advantage continues to drive large-scale substitution of reverse air and shaker systems. Reverse air bag filters represent a mature and declining segment, primarily retained in legacy metallurgical and high-temperature gas filtration applications, where system inertia and capital constraints limit retrofits. Shaker bag filters are increasingly confined to niche, low-temperature, intermittent-duty operations such as woodworking and small grain handling facilities, as offline cleaning requirements restrict throughput in continuous industrial environments.

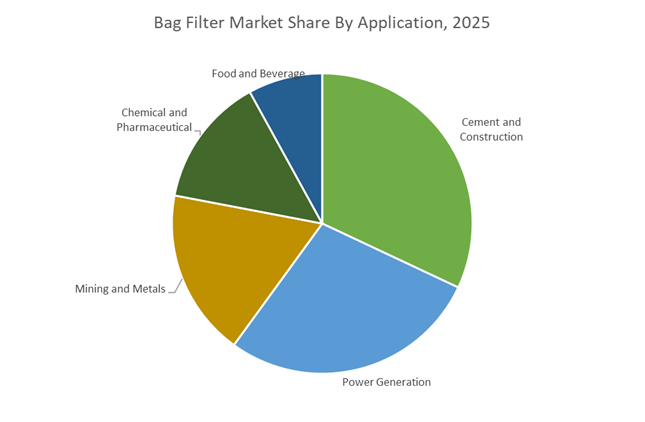

Application-Based Market Share: Cement Leads While Mining and Specialty Chemicals Create Premium Demand

By application, cement and construction account for 32% of global bag filter demand in 2025, supported by kiln dust collection, raw mill grinding, and clinker cooling operations. Infrastructure expansion in India and China, combined with tightening CPCB and environmental emission standards, continues to anchor pulse jet adoption. Power generation shows regional divergence, with sustained demand in Asia-Pacific coal fleets, while biomass and waste-to-energy projects offset declines in the US and Europe. Mining and metals remain a heavy-duty segment, driven by bauxite, copper, and iron ore processing, often utilizing abrasion-resistant media and retaining some reverse air installations for high-temperature gas streams. Chemical and pharmaceutical applications form a high-value niche, requiring explosion-proof systems and compliant filtration media, particularly in lithium and cathode material production. Food and beverage applications emphasize hygienic stainless-steel designs, serving milk powder and starch handling with premium-priced, lower-volume systems.

Bag Filter Market Competitive Landscape

The global bag filter market in 2026 is being reshaped by connected filtration, energy-efficient media, utilities-independent dust collection, and lifecycle-driven sustainability metrics. Leading manufacturers are moving beyond commodity filter bags toward IIoT-enabled monitoring, ultra-low pressure drop designs, antimicrobial media, and high-capacity pleated formats. Demand is accelerating across cement, metals, pharmaceuticals, food & beverage, cleanrooms, and renewable energy, with Asia-Pacific emerging as the fastest-growing production and deployment hub. Competitive differentiation increasingly centers on total cost of ownership (TCO), predictive maintenance, ISO 16890 compliance, and advanced filter media such as ePTFE membranes and hydroentangled needle felts.

Connected filtration leadership and extended-life bag filters by Donaldson Company, Inc.

Donaldson sets the industry benchmark in smart baghouse filtration through its iCue™ Connected Filtration platform, enabling real-time monitoring of differential pressure and dust loading for condition-based maintenance. Its flagship Dura-Life™ bag filters use hydroentanglement technology to create finer pores, delivering superior surface loading and up to three times longer service life than standard polyester bags. Strategically, Donaldson focuses on reducing compressed air consumption during pulse-jet cleaning to optimize total cost of ownership. The company strengthened its APAC footprint by opening an Experience Centre in Chakan, Pune, providing localized engineering, rapid prototyping, and application support for India’s fast-expanding manufacturing and process industries.

Energy-efficient clean air solutions from Camfil AB

Camfil dominates high-purity and critical air applications, serving life sciences, microelectronics, and nuclear facilities with ISO 16890-compliant bag filters. In early 2026, it launched the Next Generation Hi-Flo™ range, engineered for ultra-low pressure drop while maintaining high particulate capture efficiency. Camfil is also a leader in antimicrobial-treated bag filters for bioprocessing and healthcare environments where microbial control is essential. Its Camfil City digital platform integrates with building management systems to optimize AHU performance using real-time outdoor pollution data. Strategically, Camfil positions filtration as an energy-saving asset, helping commercial buildings achieve LEED and BREEAM sustainability certifications.

High-capacity liquid bag filtration expertise at Eaton Corporation

Eaton leads the liquid bag filter segment with its SENTINEL™ and DURAGAF™ series, featuring fully welded, bypass-free construction that prevents fiber migration in sensitive process fluids. Its HAYFLOW™ and MAX-LOAD™ pleated bags deliver up to ten times higher dirt-holding capacity than conventional bags, significantly reducing change-out frequency in chemical, food, and pharmaceutical operations. In 2025 and 2026, Eaton expanded its Sustainability Overview program, providing lifecycle analysis data to support customer Scope 3 emissions reporting. With full FDA and EC compliance and end-to-end traceability, Eaton remains a preferred supplier for pharmaceutical manufacturing and edible oil processing worldwide.

Harsh-duty dust collection innovation from Nederman Group

Through its MikroPul brand, Nederman is the global specialist in heavy-duty industrial baghouse systems for foundries, steel mills, and abrasive environments. At IFEX 2026, the company introduced its FS Flat-Bag Filter system, a reverse-air cleaning design that operates without compressed air, making it a utilities-independent solution for energy-intensive plants. Following the integration of EuroEquip, Nederman strengthened its source-capture and system-engineering capabilities for zero-emission shop floors. Its MCP SmartFilter platform combines multi-cassette dust collectors with Insight controls to provide predictive alerts for bag rupture risks, supporting regulatory compliance with CPCB, SPCB, and EPA emission standards.

Advanced filter media and near-zero emission bags by BWF Envirotec

BWF Envirotec is the global authority on filter media, supplying both finished bag filters and high-performance needle felts to OEMs worldwide. Its needlona® brand is the industry gold standard, with the 2026 needlona® BLUE line reducing manufacturing CO2 emissions by over 10%. BWF’s PM-Tec® ePTFE membrane bags achieve near-zero particulate emissions by capturing sub-micron dust directly on the media surface. With full vertical integration from synthetic fiber to ready-to-install filters, BWF delivers unmatched quality control. The company focuses on extreme-condition filtration, offering FireGuard® spark protection and CS29® acid-alkali resistance for cement and waste-to-energy plants.

Turnkey fluid and gas filtration systems from Parker Hannifin Corporation

Parker Hannifin brings engineering depth to the bag filter market through its Fulflo® liquid bag filters, widely used in oil and gas and high-viscosity chemical applications. The company leverages its global ParkerStore distribution network to provide local-for-local aftermarket support across industrial regions. In 2025 and 2026, Parker consolidated its Industrial Gas Filtration and Generation division to focus on clean-gas solutions for hydrogen production and carbon capture facilities. Its core strength lies in system integration, combining bag filters with sensors, valves, and hydraulics to deliver turnkey fluid management platforms for EV manufacturing, renewable energy, and advanced process industries.

United States Bag Filter Market: Consolidation, Life Sciences Demand, and Regulatory-Driven Innovation

The United States bag filter industry is undergoing a decisive structural transformation, led by large-scale inorganic growth, life sciences-driven filtration demand, and tightening environmental compliance. A landmark development is the definitive agreement by Parker-Hannifin Corporation to acquire Filtration Group from Madison Industries for USD 9.25 billion, announced in November 2025. This transaction represents one of the most significant consolidations in the industrial filtration space, substantially strengthening Parker’s position across industrial baghouse systems, HVAC filtration, and engineered bag filter solutions. The move reflects a broader U.S. trend toward portfolio-scale integration, allowing suppliers to address multi-industry demand from cement and metals to food processing and pharmaceuticals.

Parallel to consolidation, the U.S. market is seeing strong momentum from biopharmaceutical manufacturing. 3M Company finalized a USD 146 million investment in early 2025 to expand its biopharma filtration infrastructure, focusing on advanced liquid bag filters and high-purity membrane systems. This investment aligns with the rapid expansion of domestic biologics and sterile manufacturing capacity, where contamination control, single-use filtration, and high-retention bag filters are mission-critical. Product innovation is also accelerating. Camfil APC launched the Gold Series III dust collector in October 2025, integrating OmniPleat® media technology to extend filter life and reduce pulse-cleaning cycles in heavy-duty industrial environments. At the same time, Donaldson Company, Inc. strengthened its life sciences footprint in 2025 through the integration of Isolere Bio, enabling higher product quality and yield in pharmaceutical bag filter applications. Regulatory pressure remains a decisive catalyst. Following the 2025 update to U.S. EPA particulate matter standards, manufacturers are rapidly adopting fully welded, oil-absorbent bag filters such as Eaton’s DURAGAF range, reflecting a shift toward multifunctional filtration systems that combine fine particle capture with oil mist removal in a single step.

India Bag Filter Market: Manufacturing Scale-Up, Policy-Led Adoption, and Engineering-Centric Growth

India is emerging as one of the most strategically important markets for the bag filter industry, driven by rapid industrialization, policy-backed infrastructure development, and expanding domestic manufacturing capacity. A key milestone was the inauguration of Donaldson Company, Inc.’s 50,000-square-foot manufacturing facility in Pune in late 2024, which reached peak operational capacity in 2025. This facility serves as a regional hub for advanced air and bag filters, strengthening supply chain resilience across South Asia and reducing reliance on imports for high-performance filtration media.

Strategic acquisitions are reshaping India’s filtration ecosystem, particularly in high-purity and process-intensive sectors. The Thermax Group acquisition of a 51% stake in TSA Process Equipments in early 2025 significantly enhances its ability to deliver integrated filtration and water treatment solutions. This move is closely aligned with rising demand from personal care, specialty chemicals, and biopharmaceutical manufacturing, where consistent particulate control and regulatory compliance are essential. On the policy front, the Indian government’s NITI Aayog-led Global Value Chain framework has accelerated filtration adoption. In 2025, eight high-potential chemical clusters were established with mandatory requirements for pulse-jet bag filters featuring anti-static and chemical-resistant coatings, embedding advanced filtration directly into new industrial capacity. Technology development is also gaining pace. Eaton broke ground on its Global Engineering and Information Services facility in Chennai in March 2025, positioning India as a global R&D center for next-generation smart filtration monitoring, predictive maintenance, and digitally enabled baghouse systems.

China Bag Filter Market: Near-Zero Emission Policies and Digitized Filtration Compliance

China’s bag filter industry is being reshaped by aggressive environmental mandates and a strong policy push toward near-zero emission industrial operations. In November 2025, the BWF Envirotec Industrial Flue Gas Filtration Symposium held in Chongzuo underscored the country’s strategic shift toward filtration-led carbon and particulate reduction, particularly in cement, steel, and heavy manufacturing. The focus on near-zero emission technologies is driving demand for high-efficiency bag filters capable of ultra-fine dust capture under extreme operating conditions.

Large-scale industrial projects are reinforcing this momentum. BASF is integrating high-capacity industrial dust collection and baghouse systems into its Zhanjiang Verbund site, which is scheduled for major downstream plant startups in 2026. These installations reflect China’s preference for embedded, site-wide filtration architectures rather than retrofitted solutions. Regulatory oversight has intensified further with the Ministry of Ecology and Environment implementing the 2025 Green Production Mandate. This regulation requires real-time IoT monitoring of pressure differentials and operational parameters in all industrial baghouses, effectively pushing the market toward smart bag filters, sensor-enabled housings, and continuous emissions compliance. As a result, China is rapidly evolving from a volume-driven filtration market into one that prioritizes digitally monitored, performance-verified bag filter systems.

Germany Bag Filter Market: Sustainability-Led Innovation and High-Purity Industrial Demand

Germany represents the technology and sustainability frontier of the global bag filter industry, with strong emphasis on circular economy principles, renewable energy integration, and ultra-clean manufacturing. In late 2025, the BWF Group announced the strategic realignment of its filtration brands under the HEY-SIGN umbrella, focusing on felt-based filtration media and acoustic solutions derived from recycled fibers. This move highlights Germany’s leadership in sustainable filtration materials and lifecycle-driven product design.

Energy transition goals are also reshaping production practices. German filtration specialists Wolftechnik and BWF Envirotec have transitioned their domestic manufacturing operations to 100% renewable energy as of 2025, aligning filtration production with the EU’s 2030 climate objectives. Beyond sustainability, high-tech manufacturing is creating niche but high-value demand. The expansion of Germany’s “Silicon Saxony” semiconductor ecosystem in 2025 has accelerated localized production of PTFE-membrane bag filters designed for ultra-fine particulate capture in cleanroom environments. This trend positions Germany as a critical supplier of precision bag filter solutions for electronics, semiconductors, and advanced manufacturing globally.

Thailand Bag Filter Market: ASEAN Production Base for Energy and Mining Filtration

Thailand is consolidating its role as a regional manufacturing and export hub for baghouse and industrial filtration solutions serving Southeast Asia. In late 2025, BWF Envirotec completed the handover of its new factory in Rayong, purpose-built to address rising demand from the energy, cement, and mining sectors across ASEAN. The facility enhances regional access to high-performance bag filters and modular baghouse systems, reducing lead times and supporting localized compliance with increasingly stringent environmental standards. Thailand’s strategic location, combined with expanding industrial capacity, positions it as a key node in the Southeast Asian bag filter supply chain.

Country-Level Strategic Snapshot: Bag Filter Industry

Bag Filter market County Level Snapshot

|

Country

|

Strategic Focus Area

|

Key Market Developments (2024–2025)

|

|

United States

|

Consolidation and life sciences filtration

|

Major M&A, biopharma investments, advanced dust collector innovation, stricter PM compliance

|

|

India

|

Manufacturing expansion and policy-led adoption

|

New production facilities, chemical cluster mandates, acquisitions, global engineering investments

|

|

China

|

Near-zero emissions and digital compliance

|

IoT-mandated baghouses, heavy industry decarbonization, large-scale industrial integrations

|

|

Germany

|

Sustainable and high-purity filtration

|

Circular economy media, renewable-powered production, semiconductor-grade bag filter demand

|

|

Thailand

|

ASEAN manufacturing and export hub

|

New regional factory supporting energy and mining filtration demand

|

Bag Filter Market Report Scope

Bag Filter market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$11.2 Billion

|

|

Market Size (2034)

|

$18 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Type (Pulse Jet Bag Filters, Shaker Bag Filters, Reverse Air Bag Filters), By Media Material (Polyester, Polypropylene, Aramid, Fiberglass, PTFE, Polyphenylene Sulfide), By Fluid Type (Air and Gas Filtration, Liquid Filtration), By Application (Power Generation, Cement and Construction, Mining and Metals, Chemical and Pharmaceutical, Food and Beverage), By Design (Single Bag Filter Housing, Multi Bag Filter Systems, Modular Systems)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Donaldson Company Inc, Parker Hannifin Corporation, Nederman Group, Camfil AB, BWF Envirotec, Eaton Corporation, Thermax Limited, Pall Corporation, Freudenberg Filtration Technologies, Babcock and Wilcox Enterprises, SUEZ, Lydall, AAF International, Filtration Group, Sefar AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Bag Filter Market Segmentation

By Type

- Pulse Jet Bag Filters

- Shaker Bag Filters

- Reverse Air Bag Filters

By Media Material

- Polyester

- Polypropylene

- Aramid

- Fiberglass

- PTFE

- Polyphenylene Sulfide

By Fluid Type

- Air and Gas Filtration

- Liquid Filtration

By Application

- Power Generation

- Cement and Construction

- Mining and Metals

- Chemical and Pharmaceutical

- Food and Beverage

By Design

- Single Bag Filter Housing

- Multi Bag Filter Systems

- Modular Systems

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Bag Filter Industry

- Donaldson Company Inc

- Parker Hannifin Corporation

- Nederman Group

- Camfil AB

- BWF Envirotec

- Eaton Corporation

- Thermax Limited

- Pall Corporation

- Freudenberg Filtration Technologies

- Babcock and Wilcox Enterprises

- SUEZ

- Lydall

- AAF International

- Filtration Group

- Sefar AG

*- List not Exhaustive