Market Overview: Silicon-Anode Breakthroughs and Graphite Supply Chain Shifts Redefining the USD 153 Billion Battery Anode Materials Market (CAGR 30.7%)

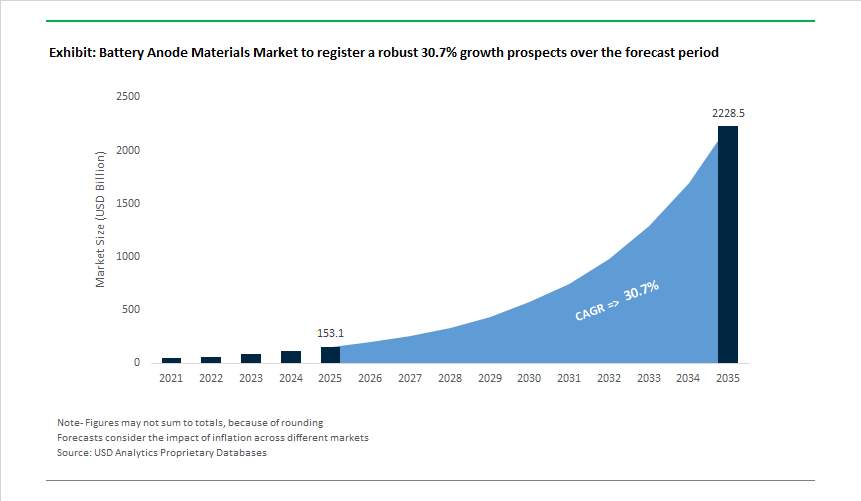

The Battery Anode Materials Industry is standing at USD 153.1 billion in 2025 and is on track to reach USD 2,227.1 billion by 2035, expanding at an exceptional 30.7% CAGR as electric mobility, energy storage, and battery manufacturing enter a phase of industrial-scale expansion. Today, anode materials are no longer viewed as commodity battery inputs; they are becoming range-defining, charging-speed-limiting, and geopolitically sensitive materials that directly determine EV competitiveness and national energy security.

The industry is moving decisively beyond a graphite-only paradigm. Silicon-graphite (Si-C) composite anodes are now being integrated into commercial lithium-ion cells, delivering 20-30% higher cell-level energy density compared with conventional graphite anodes. This improvement is directly enabling EV driving ranges beyond 600 km per charge, a benchmark that has become central to OEM product roadmaps in the premium and mass-market EV segments alike. Silicon is being deployed not as a full replacement, but as a strategic additive, with silicon content rising steadily as binder chemistry, particle engineering, and coating technologies mature.

At the same time, artificial graphite is gaining strategic importance as fast-charging requirements intensify. EV OEMs are now specifying battery systems capable of charging from 10% to 80% state-of-charge in under 15 minutes, a performance target that places severe stress on natural graphite structures. Artificial graphite, with its controlled crystallinity, higher purity, and predictable particle morphology, is increasingly selected to meet these ultrafast charging mandates while maintaining cycle stability. Although artificial graphite carries a 15-30% cost premium, it is becoming indispensable for high-performance EV platforms, commercial fleets, and next-generation energy storage systems.

Supply chain dynamics are reshaping competitive positioning across the industry. China currently controls approximately 80-85% of global anode material refining and processing capacity, making anode supply one of the most geographically concentrated segments of the battery value chain. Today, North America, Europe, and parts of Asia-Pacific are actively investing in localized anode processing, synthetic graphite graphitization plants, and silicon material production to reduce exposure to supply disruptions, trade restrictions, and price volatility. Anode materials have thus moved from procurement decisions into the realm of industrial policy and strategic sourcing.

Silicon’s fundamental materials challenge is also driving innovation intensity. Pure silicon undergoes volumetric expansion of up to 300% during lithiation, which historically caused rapid capacity fade, particle fracture, and safety risks. Today, commercial progress is being achieved through nano-structured silicon, silicon-carbon composites, elastic binders, and protective coatings, all designed to absorb expansion while preserving electrical contact and solid electrolyte interphase stability.

Looking forward, value creation in the battery anode materials market is concentrating around three execution capabilities: scalable artificial graphite production, cost-optimized silicon integration, and regionally diversified supply chains. Companies that can industrialize silicon-rich anodes without sacrificing durability, secure non-Chinese refining capacity, and meet fast-charging and long-range performance targets are positioned to capture the most lucrative growth wave in the global battery ecosystem.

Market Analysis: Silicon Adoption Accelerates While Global Players Build Multi-Regional Anode Capacity

The recent two years represent a turning point for the global Battery Anode Materials Industry, characterized by a coordinated push toward silicon integration, non-China supply diversification, and new OEM-level offtake agreements. In August 2024, BTR New Energy Material Group inaugurated the first phase of its USD 478 million Indonesian facility, delivering an annual output of 80,000 tons, the largest anode plant outside China. This strategic move reduces reliance on Chinese refining and creates a Southeast Asian hub for Natural Graphite and Artificial Graphite production. During the same month, the U.S.-based Paraclete Energy launched Silo Silicon, claiming up to 300% higher energy density than graphite-a significant milestone for commercializing Silicon-rich anodes for EVs.

Momentum accelerated in January 2025, as SK On formalized a Joint Development Agreement with Urbix Inc. to develop high-performance North American graphite, highlighting the growing urgency for regionalized, ESG-compliant supply chains. By March 2025, BTR expanded further with investments in Morocco and the second phase of its Indonesian project, adding 60,000 tpa capacity and reinforcing global anode material decentralization. In October 2025, POSCO Future M signed its largest-ever anode supply agreement-approximately USD 470 million-confirming the scale of anode procurement needed for expanding EV manufacturing.

The innovation frontier advanced dramatically in December 2025, when POSCO Future M and Factorial Energy signed an MOU to collaborate on All-Solid-State Battery anodes, including Silicon-rich and Lithium-Metal anode technologies. This follows the CEO of Group14’s October 2025 industry forecast that Silicon Anodes will accelerate in penetration over the next 3-7 years. On the other hand, NextSource Materials’ November 2025 Abu Dhabi commissioning created the first large-scale CSPG-focused (Coated Spherical Purified Graphite) anode hub in the Middle East.

Battery Anode Materials Market Trends and Opportunities

Trend 1: Commercial Scale-Up of Silicon-Dominant Anodes Enabled by Scaffold Architectures

Silicon’s theoretical capacity (~3,579 mAh/g) has been known for decades, but its >300% volumetric expansion historically prevented commercial dominance. In 2025, that constraint is being structurally resolved through engineered scaffolds—porous carbon, polymer matrices, and elastic binders that decouple electrochemical expansion from mechanical failure.

A decisive milestone was reached in December 2025 when Sionic Energy and Group14 Technologies validated a graphite-free, 100% silicon-carbon anode delivering ~400 Wh/kg in 20 Ah large-format pouch cells, sustaining 1,200+ cycles. The architecture relies on a hard-carbon scaffold (SCC55™) that preserves particle connectivity and SEI stability—proving silicon-dominant anodes are no longer confined to coin-cell demonstrations.

Thermal robustness is emerging as an equally critical differentiator. Silicon-dominant anodes tested at 45–60°C show materially lower gas generation versus legacy graphite systems, enabling faster charge acceptance and longer calendar life—attributes increasingly demanded by eVTOL platforms and performance EVs operating under elevated thermal loads.

Consumer electronics have become the first large-scale proving ground. By late 2025, TDK and Amperex Technology Limited (ATL) accelerated deployment of third-generation silicon anodes in flagship smartphones, pushing volumetric energy density beyond 800 Wh/L. This transition marks silicon’s shift from a performance additive to a core anode constituent, setting the cost-learning curve for automotive-scale adoption.

Trend 2: Dry-Processed Anodes Reshaping Gigafactory Economics

Electrode manufacturing has become a focal point for cost and carbon reduction, with dry coating emerging as one of the most disruptive process shifts in battery manufacturing. Eliminating N-methyl-2-pyrrolidone (NMP) solvent systems removes drying ovens, solvent recovery, and associated energy loads—historically among the most capital- and energy-intensive steps in a gigafactory.

In early 2025, technical disclosures from LG Energy Solution indicated that dry electrode adoption can reduce manufacturing costs by 17–30%, while shrinking factory footprints by >10,000 m² per facility. These savings compound at scale, directly improving project IRRs for next-generation gigafactories in Europe and North America.

From an energy standpoint, collaborative work led by Oak Ridge National Laboratory shows that dry processing cuts electrode-stage energy consumption by over 75%. This is strategically aligned with the EU Battery Passport (2027), which requires granular reporting of lifecycle carbon intensity—making wet slurry processes increasingly unattractive for export-oriented OEMs.

Dry processing also delivers electrochemical advantages. Thicker, denser anodes can be manufactured without binder migration, improving electrode uniformity and increasing the active-to-inactive material ratio. The result is a 5–7% Bill of Materials reduction, driven by lower usage of copper foil and separators—an underappreciated but meaningful lever in high-volume EV cell economics.

Opportunity 1: Onshoring Synthetic Graphite Under the Inflation Reduction Act

Policy-driven supply-chain restructuring is creating a once-in-a-generation opening for domestic synthetic graphite production. The extension of U.S. Treasury graphite sourcing requirements to 2027, combined with Foreign Entity of Concern (FEOC) rules, has shifted procurement strategies from lowest-cost sourcing to regulatory-aligned resilience.

In 2025, General Motors signed a multi-billion-dollar long-term supply agreement with Vianode for IRA-compliant synthetic graphite. Vianode’s North American facility—targeting production by 2027—is designed to supply anode material for up to 3 million EVs annually by 2030, while delivering a ~90% lower CO₂ footprint than conventional graphite production routes.

Federal backing is accelerating innovation beyond traditional Acheson furnaces. The U.S. Department of Energy has expanded ARPA-E support for processes such as electrochemical graphitization, including grants to Solidion Technology, which aims to convert biomass-derived carbon into battery-grade graphite at dramatically lower energy intensity.

By mid-2025, private-sector commitments to North American battery manufacturing exceeded $223 billion, with a growing share directed upstream into anode-ready materials. Synthetic graphite is no longer viewed as a commodity—it is becoming a strategic enabler for EV tax credit eligibility.

Opportunity 2: Lithium Metal Anodes as the Keystone for Solid-State Batteries

Solid-state batteries (SSBs) are re-centering the anode roadmap around lithium metal, where capacity (~3,860 mAh/g) and ultra-thin form factors unlock energy densities unattainable with intercalation materials.

Peer-reviewed studies in 2025 confirm that SSBs with lithium-metal anodes have surpassed 400 Wh/kg in pouch formats—nearly 2× the specific energy of conventional graphite-based lithium-ion cells. The central challenge remains dendrite suppression and interface stability rather than raw capacity.

Material innovation is advancing rapidly. Startups such as novali and Solidion Technology are pairing lithium metal with nanocoated separators and engineered interlayers to stabilize high-rate cycling. In parallel, Samsung researchers demonstrated >1,000 stable cycles using silver–carbon composite anodes that regulate lithium deposition during fast charging—an important signal for automotive viability.

Commercial timelines are tightening. Multiple developers are targeting pilot-scale lithium-metal cells by 2026 for aerospace and premium consumer electronics, with vehicle qualification programs extending toward 2035. This trajectory creates a parallel opportunity in high-purity lithium refining, including Direct Lithium Extraction and Refining (DLE-R) routes capable of producing foil-grade lithium with ultra-low impurity thresholds.

Market Share Analysis: Battery Anode Materials Market

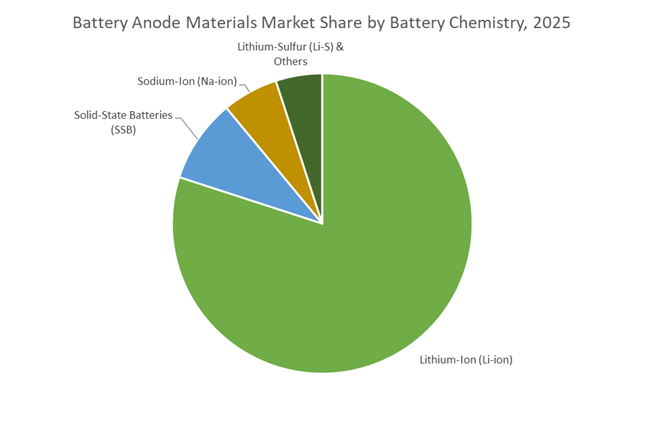

Market Share by Chemistry: Lithium-Ion Anodes Consolidate Dominance Through Silicon-Graphite Industrialization

Lithium-ion anode materials account for approximately 85% of total market share because the industry has crossed a structural threshold: silicon-graphite composites are now manufacturable at automotive scale without sacrificing cycle life or safety. The defining commercial metric is the 2,300 mAh/g specific capacity achieved by next-generation silicon anodes, as disclosed by BTR New Material Group in 2025—nearly six times the theoretical ceiling of graphite. This capacity uplift directly translates into higher cell-level energy density without altering lithium-ion pack architecture, keeping lithium-ion firmly ahead of solid-state alternatives still constrained by cost and yield. Equally critical is fast-charge compatibility: standardized natural-artificial graphite blends now support 10–12-minute 10–80% charging by stabilizing lithium diffusion and SEI formation, a prerequisite for mass-market EV adoption. The historical failure point of silicon—volumetric expansion—has also been neutralized at a commercial level, with silicon-carbon composites sustaining >80% capacity after 500 cycles, making them viable for 8–10-year automotive warranties. Finally, lithium-ion’s dominance is reinforced by manufacturing scale, led by POSCO Future M, whose 90,000-ton annual anode capacity signals supply reliability, bankability, and procurement confidence—conditions that alternative chemistries cannot yet match.

Market Share by Application: Automotive EVs Anchor Volume Through Range, Safety, and Supply-Chain Re-Design

Electric vehicles represent around 65% of total anode demand, driven not by incremental growth but by a structural redesign of EV performance targets and sourcing strategies. Automotive OEMs are now anchoring platforms around 300–350 Wh/kg cell energy density, the threshold required for 700 km-plus driving range, and this benchmark is only achievable with high-silicon lithium-ion anodes. Safety has become an equally decisive driver: 2025 validation data shows that advanced silicon-based anodes can delay thermal runaway peaks by ~110 minutes, materially improving passenger evacuation windows and regulatory approval prospects. Beyond performance, the automotive segment’s dominance is increasingly shaped by geopolitics and compliance economics. With China still controlling the majority of graphite processing, automakers are prioritizing IRA-compliant, non-Chinese anode supply, accelerating investment in African-sourced graphite refined in South Korea and Japan. This has triggered a decisive shift toward direct supply contracts between automakers and anode producers, bypassing traditional cell-maker intermediaries to lock in volume, pricing, and traceability. As a result, automotive demand is no longer cyclical—it is contractually secured, vertically integrated, and strategically protected—cementing EVs as the single most powerful demand engine in the global battery anode materials market.

Competitive Landscape: High-Capacity Graphite Leaders and Silicon-Innovation Specialists Reshape Global Anode Competition

The competitive environment in the Battery Anode Materials Industry is increasingly defined by production scale, supply-chain localization, silicon innovation, and the ability to meet OEM requirements for fast charging and high cycle life. Companies dominating this space maintain large global capacities, strong R&D portfolios, and secured offtake partnerships with tier-one EV battery manufacturers.

BTR New Energy Material Group Dominates Global Anode Production With Multi-Continent Expansion

BTR remains the undisputed global leader in both Natural Graphite and Artificial Graphite anode materials, holding the top position for 14 consecutive years. Its total production capacity stands at 575,000 tpa, supported by massive expansions in Indonesia (80,000 tpa Phase I, Phase II ongoing) and Morocco (60,000 tpa). BTR also invests heavily in Silicon-based materials including SiO composites, positioning itself strongly for the next wave of high-energy-density batteries. Its Indonesian facility-the largest outside China-strategically supports ASEAN and Western supply chain diversification, reducing geographic concentration risk in the EV Batteries landscape.

POSCO Future M Builds Full-Stack Battery Material Integration With Massive Anode Expansion

POSCO Future M is the only Korean company operating a fully integrated system for both cathode and anode materials, offering unmatched supply-chain stability. The company aims to reach 114,000 tpa anode capacity by 2026, spanning Natural Graphite, Artificial Graphite, and Silicon materials. Its record USD ~470 million supply contract in October 2025 underscores strong OEM confidence in its anode capabilities. POSCO’s collaboration with Factorial Energy (December 2025) supports next-generation lithium-metal and solid-state batteries, demonstrating long-term positioning in ultra-high-energy-density chemistries.

Resonac (Showa Denko) Leads in High-Purity Artificial Graphite For Premium EV Cells

Resonac remains a global reference in Artificial Graphite anode engineering, leveraging decades of material science leadership since mass production began in 1998. Its proprietary pore-optimized particle structure enhances lithium-ion intercalation, enabling higher discharge capacities and improved low-temperature behavior. Resonac’s Artificial Graphite is particularly favored by Japanese and Korean battery manufacturers who prioritize safety, cycle stability, and long-duration performance-key requirements for premium EVs and high-end consumer electronics.

SK Materials Accelerates Silicon-Anode Commercialization Through Major Investments and SK On Integration

SK Materials has emerged as one of the strongest drivers of Silicon Anode innovation, supported by SK Group’s vertically integrated battery ecosystem. Its 850 billion KRW investment with Group14 Technologies positions it at the forefront of Silicon-Carbon composites, with early testing of SCC55 showing up to 5× capacity improvement over graphite. SK’s JDA with Urbix strengthens access to sustainable North American graphite, complementing its silicon strategy and securing supply for SK On’s rapidly expanding EV battery production footprint.

Hitachi Chemical (Resonac) Maintains Strong Legacy in Automotive-Grade Artificial Graphite

Hitachi Chemical, now part of Resonac, remains an influential supplier of Artificial Graphite anodes with a long-standing reputation for stability, purity, and high cycle life-characteristics essential for EV and HEV batteries. Its engineering strengths lie in particle coating technologies that minimize side reactions and enhance thermal stability, directly supporting high safety standards at elevated temperatures. Hitachi Chemical continues to be a preferred supplier for major Japanese OEMs, particularly for long-life, high-rate automotive applications.

China continues to anchor the global battery anode materials market in 2025, but its role has shifted decisively from volume-driven supplier to regulator of strategic supply. The implementation of Joint Decision No. 58 by the Ministry of Commerce (MOFCOM) and the General Administration of Customs in October 2025 formally classified artificial graphite and associated manufacturing equipment as dual-use items, mandating export licenses from November 8, 2025 onward. This policy is strategically aligned with China’s 15.5 million NEV production target, ensuring that high-purity anode materials—particularly synthetic graphite—are preferentially retained for domestic battery makers. For global OEMs, this has introduced a new layer of compliance risk and lead-time uncertainty, reinforcing China’s leverage across EV and grid-scale storage supply chains.

Simultaneously, China is accelerating its silicon-based anode transition to maintain technological leadership. BTR New Material Group has committed to expanding silicon-based anode capacity to 50,000 tons by 2028, while Shanghai Putailai (PTL) initiated a 12,100-ton silicon project, partially commissioned in early 2025. These investments are complemented by enforced efficiency upgrades under the 2024–2025 Energy Conservation Action Plan, pushing AI-driven kiln optimization and waste-heat recovery that have already reduced graphitization carbon intensity by ~18%. As a result, China is not only controlling exports but also redefining the cost–carbon–performance equation for next-generation anodes.

South Korea: Supply-Chain De-Risking and the Saemangeum Anode Hub

South Korea’s battery anode strategy in 2025 is defined by decoupling from Chinese upstream dependence while preserving high-performance leadership. A pivotal milestone was reached in October 2025 when POSCO Future M signed its largest-ever anode supply contract—671 billion won (~$470 million)—with a global automaker through 2031. Critically, this agreement pivots toward African-sourced natural graphite, processed domestically at the Saemangeum Industrial Complex, insulating Korean battery exports from Chinese-origin constraints and future trade disruptions.

Beyond graphite, South Korea is emerging as a front-runner in silicon anode commercialization. Daejoo Electronic Materials has scaled output in 2025 to support 800V EV platforms, enabling ultra-fast charging profiles (0–80% in under 15 minutes). This industrial push is reinforced by policy: the Ministry of Trade, Industry and Energy (MOTIE) has designated anode materials as National Strategic Technologies, unlocking up to 50% tax credits for R&D and localized manufacturing. Collectively, these measures position South Korea as a low-risk, high-performance anode supplier for global OEMs seeking alternatives to China.

United States: BIL-Funded Reshoring and FEOC-Driven Market Realignment

The U.S. battery anode materials market in 2025 is being reshaped by policy-enforced localization, anchored in the Bipartisan Infrastructure Law (BIL) and stringent Foreign Entity of Concern (FEOC) rules. In Spring 2025, the U.S. Department of Energy (DOE) launched the third round of its Battery Materials Processing and Manufacturing grants, allocating $725 million to close the domestic investment gap in synthetic graphite and silicon-anode precursors. Individual awards ranging from $50–$200 million are catalyzing greenfield and brownfield projects across the U.S. anode value chain.

Regulatory pressure is amplifying the impact. Updated 2025 Treasury guidance strictly enforces FEOC exclusions, disqualifying EVs containing more than de minimis graphite processed by FEOCs from the $7,500 federal tax credit. This has accelerated capital inflows into domestic players such as Anovion and Syrah Resources (U.S. operations). On the technology front, Group14 Technologies achieved a major milestone with its BAM-2 facility in Moses Lake, delivering the first commercial-scale batches of SCC57™ silicon–carbon anode material, while Sila Nanotechnologies advanced OEM qualification programs. Together, policy and technology are rapidly transforming the U.S. into a credible mine-to-anode ecosystem.

Canada: G7-Aligned Mine-to-Anode Integration

Canada’s anode materials strategy is built around ethical sourcing, vertical integration, and G7 alignment, positioning the country as North America’s sustainable anode hub. In November 2025, Canada announced $6.4 billion in funding for 26 critical mineral projects during its G7 Presidency, with flagship support directed toward Northern Graphite and Nouveau Monde Graphite (NMG) to establish fully integrated mine-to-anode operations in Quebec. These projects are strategically designed to supply U.S. battery plants seeking IRA-compliant materials.

Innovation is a parallel priority. In October 2025, Natural Resources Canada awarded $22 million across eight advanced anode R&D projects, including $3 million to HPQ Silicon for continuous SiOx production and $1.5 million to Nanode Battery Technologies for tin-based anode optimization. Infrastructure development is also advancing, with Northern Graphite and The BMI Group evaluating a Battery Anode Material (BAM) facility in Baie-Comeau, designed to process Canadian graphite into battery-grade spherical graphite for the U.S. market.

Australia: Mid-Stream Value Addition and “Green Anode” Positioning

Australia’s role in the battery anode materials market is evolving from raw material exporter to mid-stream processing powerhouse. A landmark step was taken in June 2025 when the South Australian government granted provisional development approval for Renascor Resources’ commercial-scale BAM facility. Anchored by the Siviour Deposit—the largest graphite reserve outside Africa—the project targets 100,000 tonnes per annum of Purified Spherical Graphite (PSG), positioning Australia as a strategic supplier to Western OEMs.

Financial backing underscores national priority. Renascor secured conditional approval for a $185 million loan from Australia’s $4 billion Critical Minerals Facility, explicitly supporting mid-stream value addition. Technologically, Australia is differentiating through HF-free purification processes, addressing environmental and ESG concerns tied to conventional hydrofluoric acid routes. By 2025, these developments have made Australian PSG particularly attractive to European and North American OEMs pursuing “Green Anode” certification and low-carbon battery supply chains.

European Union: Regulation-Led Transition to Low-Carbon and Recycled Anodes

The European Union is reshaping anode material demand through regulatory force rather than direct subsidies, embedding carbon transparency into battery economics. The enforcement of EU Battery Regulation 2023/1542 on February 18, 2025, mandates full carbon footprint disclosure for all EV batteries placed on the EU market, explicitly including emissions from energy-intensive graphite graphitization. This has materially altered supplier selection criteria for European cell manufacturers.

Regulation is also catalyzing circular innovation. While mandatory recovery targets by end-2025 focus on lithium (65%) and cobalt/nickel (70%), the same framework has accelerated R&D into graphite recovery from black mass. In parallel, Vianode, backed by Hydro and Altor, ramped up renewable-powered synthetic graphite production in 2025, delivering anodes with a ~90% lower carbon footprint than conventional Chinese materials. As a result, the EU market is rapidly bifurcating toward low-carbon, traceable, and increasingly recycled anode supply.

2025 Strategic Matrix: Battery Anode Materials – National Comparison

Battery Anode Materials Strategic Matrix

|

Country / Region

|

Strategic Driver

|

2025 Key Milestone

|

Primary Anode Focus

|

|

China

|

Resource diplomacy & export control

|

MOFCOM Joint Decision No. 58

|

Synthetic graphite, Si–C

|

|

South Korea

|

Supply-chain de-risking

|

POSCO 671B won anode contract

|

Natural graphite, silicon

|

|

United States

|

Domestic reshoring

|

$725M DOE BIL Round 3

|

Synthetic graphite, silicon

|

|

Canada

|

G7-aligned integration

|

$6.4B critical minerals funding

|

Mine-to-anode graphite

|

|

Australia

|

Mid-stream value addition

|

Renascor BAM approval

|

Purified spherical graphite

|

|

European Union

|

Circular economy regulation

|

Mandatory carbon disclosure

|

Recycled & low-carbon anodes

|

Battery Anode Materials Market Report Scope

Battery Anode Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$153.1 Billion

|

|

Market Size (2035)

|

$2227.1 Billion

|

|

Market Growth Rate

|

30.7%

|

|

Segments

|

By Material Type (Natural Graphite, Synthetic Graphite, Silicon-Based Anodes, Lithium-Metal Anodes, Other Materials), By Battery Chemistry (Lithium-Ion, Sodium-Ion, Solid-State Batteries, Lithium-Sulfur), By Coating Type (Carbon-Coated Anodes, Polymer-Coated Anodes, Inorganic-Coated Anodes), By Application (Automotive, Consumer Electronics, Energy Storage Systems, Industrial & Specialty)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BTR New Material Group Co. Ltd., Ningbo Shanshan Co. Ltd., Hunan Zhongke Shinzoom Co. Ltd., Resonac Holdings Corporation, Mitsubishi Chemical Group Corporation, POSCO Future M, Hitachi Chemical, Alkegen, Group14 Technologies, Sila Nanotechnologies Inc., Amprius Technologies Inc., Nippon Carbon Co. Ltd., Talga Group, Syrah Resources Limited, GrafTech International Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Battery Anode Materials Market Segmentation

By Material Type

- Natural Graphite

- Synthetic Graphite

- Silicon-Based Anodes

- Lithium-Metal Anodes

- Other Materials

By Battery Chemistry

- Lithium-Ion (Li-ion)

- Sodium-Ion (Na-ion)

- Solid-State Batteries (SSB)

- Lithium-Sulfur (Li-S)

By Coating Type

- Carbon-Coated Anodes

- Polymer-Coated Anodes

- Inorganic-Coated Anodes

By Application

- Automotive

- Consumer Electronics

- Energy Storage Systems (ESS)

- Industrial & Specialty

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Battery Anode Materials Market

- BTR New Material Group Co., Ltd.

- Ningbo Shanshan Co., Ltd.

- Hunan Zhongke Shinzoom Co., Ltd.

- Resonac Holdings Corporation

- Mitsubishi Chemical Group Corporation

- POSCO Future M

- Hitachi Chemical

- Alkegen

- Group14 Technologies

- Sila Nanotechnologies Inc.

- Amprius Technologies, Inc.

- Nippon Carbon Co., Ltd.

- Talga Group

- Syrah Resources Limited

- GrafTech International Ltd.

*- List not Exhaustive