Market Overview: Battery Coating Market Size, Growth Rate, and Technology Transition Outlook (2025–2034)

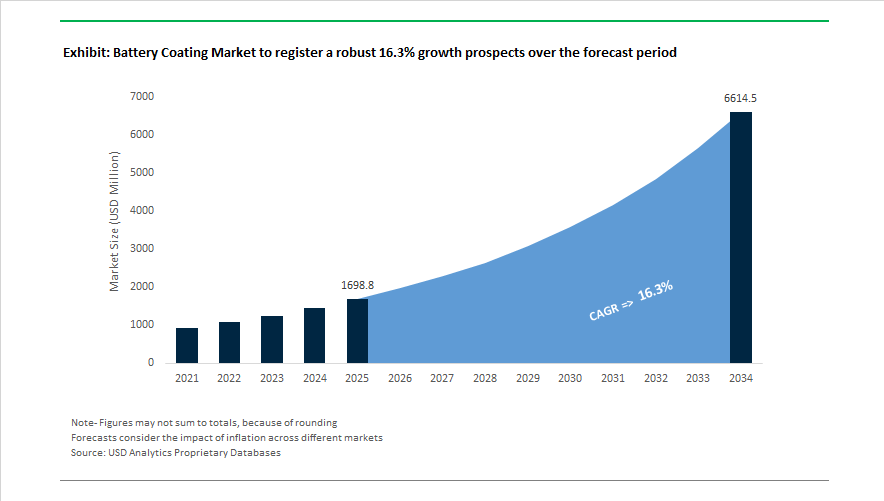

The battery coating market is entering a scale-driven industrialization phase aligned with global EV battery manufacturing expansion and next-generation cell architecture development. Market value is projected to rise from USD 1,698.8 Million in 2025 to USD 6,612.4 Million by 2034, registering a CAGR of 16.3% , driven by rapid adoption of dry electrode coating, ceramic separator coatings, advanced binder chemistries, and high-performance conductive layers. Coating technologies have moved from being a supporting material function to a core enabler of energy density, battery safety, fast charging capability, and manufacturing efficiency. Production line optimization has become a primary investment focus, highlighted by the 2024 launch of the GigaCoater system by Dürr Group, enabling simultaneous two-sided electrode coating to improve throughput and coating uniformity for 4680-format cells. Industrial decarbonization pressure is also reshaping coating processes. In October 2024, AM Batteries introduced a solvent-free spray coating process backed by Toyota and Porsche, cutting energy use and CO2 emissions by 40% through elimination of NMP-based drying stages. Similarly, pilot work between Solvay and Volkswagen in 2024 demonstrated 30% lower energy consumption via polymer-based dry electrode application.

The market’s innovation curve accelerated further in 2025 as performance coatings became central to EV safety and lifecycle durability. In July 2024, SK Innovation introduced ceramic-coated separator technology enhancing thermal stability in high-nickel batteries, addressing fire risk and structural deformation under heat stress. Conductive and dielectric coatings are also gaining strategic importance. In September 2024, Henkel debuted a conductive coating enabling adhesion in dry battery electrode processing, reducing factory floor space by up to 60% . In April 2025, BASF expanded U.S. production of Licity anode binders, supporting silicon-rich anode coatings that enhance cycle stability and fast charging. Coating lifespan and material efficiency are also improving. In September 2025, AkzoNobel and NIO received the Altair Enlighten Award for a powder coating that tripled battery shield service life while reducing coating thickness by 70% , already deployed on more than 80,000 EVs since late 2024.

Strategic R&D infrastructure and regional supply localization are defining competitive positioning. In March 2024, Arkema expanded Kynar PVDF capacity in Kentucky to meet North American gigafactory demand for cathode binders. The company strengthened its technology leadership in September 2025 by opening a battery dry coating laboratory in Normandy, focusing on direct calendering and electrodeposition methods that reduce solvent use and carbon intensity. In February 2026, Arkema signed an MoU with Senior to collaborate on controlled deposition processes and semi-solid battery manufacturing, signaling movement toward next-generation electrode architectures. Regional application support is also scaling. Henkel opened a North American Battery Application Center in Michigan in September 2025 to support dielectric and safety coating deployment for U.S. EV OEMs. Material science startups are transitioning to commercialization, illustrated by Volexion appointing new leadership in June 2025 to scale graphene-based cathode coatings that improve conductivity without altering existing wet production lines.

Trends and Opportunities Transforming the Battery Coating Market

Market Trend: Industry Migration Toward Aqueous and Dry-Process Electrode Manufacturing

Manufacturers are structurally shifting away from N-Methyl-2-pyrrolidone (NMP) due to its environmental impact and cost burden. Dry coating has become the strategic focal point because it removes energy-intensive evaporation steps and solvent recovery infrastructure, cutting production costs and emissions at gigafactory scale.

Volkswagen’s PowerCo Salzgitter gigafactory, commissioned in December 2025, is the first commercial facility to integrate solvent-free dry coating using Koenig & Bauer technology. The system targets a 30% reduction in factory energy use and a 15% cut in footprint by eliminating drying ovens entirely.

Tesla’s DBE (Dry Battery Electrode) effort faced multi-year mechanical roller durability challenges, yet by late 2024 the company confirmed successful stabilization. Tesla’s roadmap now targets 80 GWh of DBE-based output by 2026—a scale expected to enable a 56% cost-down versus legacy wet-coated 2170 cells. Parallel pilot lines are emerging in the EU: in February 2025, Dürr and Porsche subsidiary Cellforce partnered with LiCAP to test dry-press calendering at a plant designed to save nearly one ton of CO₂ emissions per 10 kWh battery manufactured.

For executive decision-makers, the implication is that any electrode coating supplier not compatible with solvent-free processing will lose qualification status in the next procurement cycle, especially as ESG-linked financing begins favoring dry-compatible supplier selection.

Market Trend: Ultra-Thin Ceramic Safety Coatings Become Standard for High-Nickel EV Batteries

Separator coatings are moving from optional add-ons to mandatory safety layers in lithium-ion batteries used in NMC811 and high-voltage EV packs. The performance frontier is ultra-thin ceramic layers (<2 µm) that provide thermal shutdown protection while keeping ionic pathways open.

In 2025, Asahi Kasei expanded Hipore™ ceramic-coating capacity to 1.2 billion m² per year, tailoring output toward North American EV value chains. Lab testing from mid-2025 shows Al₂O₃ and PAA-binder composites almost doubling thermal endurance: ceramic-coated polypropylene separators maintained open-circuit voltage for 937 seconds under heat shock, compared with just 453 seconds for uncoated substrates.

China is accelerating this trend through regulatory design. Its NEV (New Energy Vehicle) subsidy system now links qualification to pack-level energy density thresholds above 180 Wh/kg, prompting domestic suppliers to make ceramic coatings a baseline requirement and expanding ceramic separator capacity at 32% CAGR to reach 1,200 GWh localized output.

Market Opportunity: Conductive Coating Layers for Thick Electrodes and Fast-Charge EV Platforms

As OEMs increase electrode thickness beyond 150 µm to boost kWh per cell, conductivity becomes the limiting factor. Applying carbon-based coatings directly to current collectors is now seen as the most scalable approach to reducing interfacial resistance and enabling high-rate charging.

IEST benchmarks (2025) show that carbon-coated aluminum foil used in LFP cells meaningfully reduces charge-transfer resistance and internal polarization. This allows active layer thickness increases without sacrificing power performance—a prerequisite for mass-market EVs that require <15-minute charging targets.

Emerging materials are reshaping longevity. Three-dimensional carbon nanowall (CNW) coatings provide mechanical buffering that reduces particle cracking under silicon-rich anode expansion cycles, extending usable battery life by up to 20%. This provides a distinct ROI case for automakers shifting toward silicon integration but unwilling to sacrifice warranty periods.

Market Opportunity: Atomic Layer Deposition (ALD) for Cathode Surface Stabilization

Atomic Layer Deposition is becoming the dominant nano-coating pathway because it deposits pinhole-free, nanometer-scale protective layers on cathode active material grains. This is essential for NMC811 and LNMO chemistries prone to transition-metal dissolution at high voltages.

Forge Nano’s August 2025 announcement that it is supplying 100% U.S.-sourced ALD-coated 18650 cells to the Department of Defense marks a milestone—proving ALD cathodes can meet military-grade reliability and extreme-temperature cycling. Market share data confirms momentum: ALD now represents 44.2% of all battery-coating technology revenue globally as of 2025.

Scaling signals are accelerating. In June 2025, Volexion appointed a scale-focused CEO to transition graphene-enhanced ALD from lab-pilot to commercial throughput without requiring wholesale replacement of slurry-casting infrastructure. This indicates that ALD-based suppliers capable of retrofitting into existing production lines will capture the fastest time-to-revenue and highest margin pool.

Battery Coating Market Share and Segmentation Insights

Market Share by Coating Type: Electrode and Separator Coatings Lead Functional Material Adoption

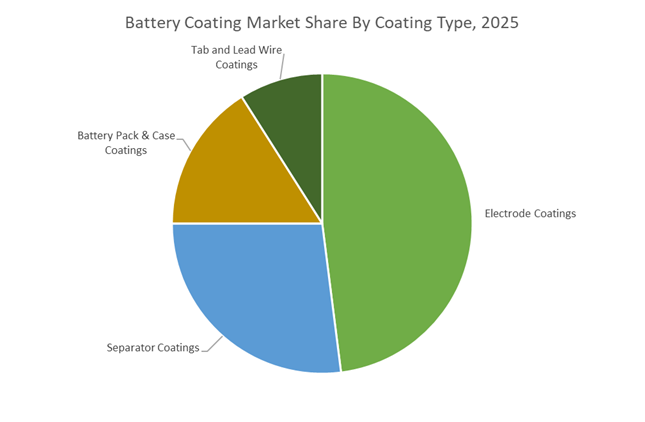

Electrode coatings account for the largest share of the Battery Coating Market at 48% in 2025, reflecting their direct impact on cathode and anode performance across lithium-ion battery manufacturing. Widely deployed PVDF and ceramic coatings enhance electrical conductivity, structural stability, and cycle life, making them essential for high-energy-density EV batteries. Separator coatings represent the second most critical segment, with alumina and boehmite ceramic layers now standard in advanced cells to improve thermal stability and prevent internal short circuits. Battery pack and case coatings are expanding rapidly as OEMs prioritize thermal management, electrical insulation, and fire resistance to comply with tightening EV safety regulations. Tab and lead wire coatings, while smaller in volume, remain vital for corrosion resistance and consistent current flow, with demand accelerating as manufacturers transition toward higher-voltage battery architectures and next-generation pack designs.

Market Share by End Use Industry: Automotive Electrification Anchors Volume Growth

Automotive dominates battery coating consumption with a 55% market share in 2025, driven by large-scale electric vehicle production and aggressive capacity expansions across global gigafactories. Coatings in this segment are engineered for fast charging, extended longevity, and operational safety under high thermal and mechanical stress. Consumer electronics continues to represent a substantial revenue stream, fueled by demand for ultra-thin, precision coatings that enable compact, high-energy batteries for smartphones, laptops, and wearables. Energy Storage Systems are emerging as a fast-growing application, adopting advanced coating technologies to enhance cycle life and safety in both grid-scale and residential installations, particularly in high-temperature environments. Aerospace and defense forms a specialized, high-value niche where battery coatings must deliver vibration resistance, wide temperature tolerance, and elevated safety margins for mission-critical power systems.

Competitive Landscape Analysis of the Battery Coating Market

The battery coating market is evolving rapidly as electric vehicle manufacturers demand higher thermal protection, dielectric strength, recyclability, and automation-ready materials. Leading suppliers are moving beyond conventional surface treatments toward integrated functional coatings that enhance safety, enable fast disassembly, support high-voltage architectures, and reduce manufacturing energy intensity. Competitive differentiation now centers on digital traceability, low-temperature processing, powder coating efficiency, separator protection, and system-level integration with gigafactory workflows. Strategic investments in AI-enabled coating simulation, PFAS-free formulations, and circular battery design are reshaping supplier partnerships across EV OEMs, battery cell manufacturers, and energy storage platforms.

Henkel Adhesive Technologies pioneers debond-on-demand and digital battery coating ecosystems

Henkel enters 2026 as a premier end-to-end battery coating solutions provider, embedding functional coatings directly into EV pack architecture. Its Electrical Delamination Tapes enable debonding-on-demand through low-voltage activation, accelerating battery repair and recycling. The Loctite and Teroson portfolios now feature mica-replacement safety coatings offering thermal resistance up to 1,400°C while reducing pack weight. Henkel strengthened application validation by opening its North American Battery Application Center in Michigan, equipped with ABB robotics for automated dispensing trials. Through its Path.Era ecosystem, Henkel integrates digital battery passports into coatings, supporting EU circularity mandates and enhancing material traceability across gigafactory supply chains.

PPG Industries scales dielectric and fire-protection coatings for high-voltage EV platforms

PPG Industries has expanded beyond traditional paints to deliver total system battery coating solutions focused on electrical insulation and fire protection. Its CORATHERM and ENVIROCRON dielectric powder coatings support automated application on 800V battery architectures, ensuring high-voltage safety at production scale. In late 2025, PPG achieved REDCert² certification across key European sites, validating sustainable raw material sourcing for net-zero OEM programs. The launch of CORAGUARD SE 5300 introduced anti-blast underbody protection combining thermal shielding with impact resistance. Strategically, PPG emphasizes UV-curable dielectric coatings that reduce curing times from minutes to seconds, unlocking throughput gains in 2026 battery manufacturing lines.

Arkema advances internal battery protection with controlled deposition technologies

Arkema commands a critical position in internal battery coatings, supplying high-performance materials that safeguard electrodes and separators. In February 2026, Arkema signed an MoU with Senior to co-develop controlled deposition coatings that improve adhesion between separators and high-nickel electrodes. Its Kynar PVDF and Incellion acrylic systems provide chemical resistance and mechanical integrity for silicon-rich anodes. Recent low-temperature cell assembly coatings enable bonding at reduced heat, lowering manufacturing carbon footprints by up to 15%. Arkema’s core strength lies in semi-solid and dry electrode manufacturing, with specialized binders and coatings supporting emerging solvent-free battery production processes.

AkzoNobel delivers ultra-durable powder coatings for long-life battery systems

AkzoNobel has refocused its 2026 strategy on high-efficiency powder coatings that extend battery service life while minimizing material usage. In late 2025, its collaboration with NIO earned the Altair Enlighten Award for Interpon A1000, tripling shielding durability and reducing coating thickness by 70%. Through its Resicoat brand, AkzoNobel introduced single-spray powder coating technology that achieves dielectric strength in one pass, cutting manufacturing energy consumption by over two gigawatt-hours annually. The company prioritizes fifteen-year longevity coatings for battery swapping platforms and expanded its Shanghai Technology Center to localize advanced battery coating solutions for China’s high-volume EV market.

Asahi Kasei dominates separator coatings and expands into integrated EV battery platforms

Asahi Kasei is a hidden champion in battery separator coatings, strengthening its global footprint through a joint venture with Honda to build a C$1.5 billion integrated Hipore separator plant in Ontario. The company developed a nickel-coated absorption layer that mitigates electrode degradation, extending lithium-ion battery life. Its 2026 portfolio includes PFAS-free coating solutions and low-friction battery housing coatings that eliminate forever chemicals while maintaining chemical stability. Strategically, Asahi Kasei is advancing acetonitrile-based electrolyte integration, leveraging coating expertise to enable ultra-high-power cells and licensing proprietary high-ionic conductivity technologies to global battery manufacturers.

BASF strengthens electrocoat binders and AI-driven coating simulation

BASF applies its Verbund production model to deliver specialized binders and electrocoat resins forming the primary protection layers of EV battery housings. In early 2026, BASF optimized operations at its Caojing facility in Shanghai, doubling capacity for polyester and polyurethane resins used in battery component coatings. The company restructured its Battery Materials and Coatings units into standalone businesses, accelerating innovation while retaining enterprise-scale R&D. BASF’s Global Digital Hub in Hyderabad uses AI to simulate slurry coating dynamics at microscopic levels, enabling predictive process optimization. Its e-coat binders remain central to corrosion protection, safeguarding battery packs throughout their operational lifecycle.

China Battery Coating Market: Export Controls, Sodium-Ion Momentum, and Cost-Optimized Smart Coatings

China’s battery coating industry is entering a phase defined by sovereign control over materials, rapid chemistry diversification, and manufacturing cost optimization. Effective November 8, 2025, the Ministry of Commerce of the People's Republic of China implemented rigorous export licensing for lithium battery materials, covering cathode and anode precursors as well as specialized coating equipment. This move signals a decisive policy shift toward supply chain sovereignty, reshaping global sourcing strategies for battery coatings and reinforcing domestic capacity utilization.

Technology leadership is expanding beyond lithium-ion. In late December 2025, Contemporary Amperex Technology Co., Limited announced a dual-star strategy to mass-produce sodium-ion batteries by 2026. These systems rely on proprietary hard-carbon coatings to deliver energy densities of 175 Wh/kg and reliable performance down to minus 40 degrees Celsius, underscoring the role of advanced surface coatings in enabling alternative chemistries. Manufacturing innovation is also reducing costs. Shifang Intelligent Manufacturing replaced traditional blue PET insulation films with UV inkjet-printed insulation coatings in 2025, achieving a 30% reduction in material costs and ink utilization above 99%. In parallel, China’s 2025 technical roadmap is incentivizing lithium manganese iron phosphate preparation routes, which require advanced carbon-coating techniques to maintain conductivity under higher-voltage operating conditions. Together, export controls and coating-intensive chemistries are consolidating China’s leadership across both volume and innovation fronts.

United States Battery Coating Market: Precision Coatings, Domestic Capacity, and Silicon Readiness

The United States battery coating industry is progressing through precision process breakthroughs, domestic capacity expansion, and targeted R&D support for next-generation anodes. In September 2025, Argonne National Laboratory announced a breakthrough in atomic layer deposition, applying nanoscale glass-like coatings to sulfide-based solid electrolytes. This advance enables coating in ambient air and materially reduces the need for capital-intensive dry rooms, improving the economics of solid-state battery manufacturing.

Commercial scaling is following scientific progress. Volexion appointed new leadership in June 2025 to accelerate deployment of its graphene-based cathode coating technology, designed to extend cycle life without altering existing gigafactory lines. Binder and coating resin capacity is also expanding domestically. Arkema completed a 15% capacity expansion at its Calvert City, Kentucky facility across late 2024 and early 2025, specifically for Kynar® PVDF resins used as high-performance binders and coatings in electric vehicle batteries. At the anode interface, the United States Department of Energy extended R&D grants in late 2025 for elastic coatings that manage the extreme volume expansion of silicon-dominant anodes during fast-charging cycles. These initiatives collectively anchor the U.S. position in precision coating science and domestic supply resilience.

Germany Battery Coating Market: Solvent-Free Processing and Extreme Thermal Protection

Germany’s battery coating industry is characterized by solvent-free processing leadership and advanced thermal management solutions aligned with energy transition priorities. In 2025, a collaboration between Volkswagen and Solvay successfully piloted a dry electrode coating process that eliminates solvents, reduces manufacturing energy consumption by 30 percent, and removes the need for large-scale drying ovens. This approach directly addresses cost and sustainability pressures in gigafactory-scale electrode production.

Thermal protection innovation is advancing in parallel. Axalta Coating Systems introduced the Alesta® e-PRO powder coating line in October 2025, engineered to maintain structural integrity at direct flame temperatures up to 1200 degrees Celsius. These coatings are designed to delay or prevent thermal runaway in battery enclosures. With Germany operating approximately 66 GW of wind capacity, stationary storage is a major demand driver. In 2025, Jotun launched powder coatings rated for highly aggressive C5VH and CX environments, protecting grid-scale battery containers from corrosion under harsh operating conditions.

South Korea Battery Coating Market: Ceramic Separators, Solid-State Incentives, and Automated Insulation

South Korea continues to build competitive advantage through safety-focused coatings, government-backed solid-state priorities, and automation. In late 2024, SK Innovation through SK ie technology introduced a new generation of ceramic-coated separators that use ultra-thin alumina layers to prevent contraction and mitigate fire risk at elevated temperatures. This technology reinforces South Korea’s leadership in separator coatings for high-energy cells.

Policy alignment is accelerating innovation. In October 2025, the South Korean government designated solid-state battery coating technology as a national strategic technology, unlocking tax credits for development of sulfide-based electrolyte coatings. Manufacturing automation is also improving consistency. In 2025, Shenzhen Omijia and South Korean Tier-1 suppliers integrated UV inkjet insulation printing into production lines, replacing manual tape application and ensuring complete dielectric coverage for high-voltage battery packs. These developments emphasize safety, repeatability, and scale.

Japan Battery Coating Market: Solid-State Partnerships and Structural Coating Integration

Japan’s battery coating industry is advancing through strategic partnerships in solid-state electrolytes and structural coating integration. In October 2024, Toyota Motor Corporation and Idemitsu Kosan formalized a production partnership for sulfide-based solid electrolyte coatings, targeting commercialization of all-solid-state batteries by 2027. The collaboration highlights Japan’s strength in translating laboratory-scale coating chemistries into production-ready processes.

Portfolio expansion is reinforcing structural durability. In late 2025, UBE Corporation acquired the urethane systems business of LANXESS for USD 500 million. This acquisition integrates specialized polyurethane coatings for battery pack durability and vibration damping, broadening Japan’s coating capabilities beyond electrochemical interfaces to full system protection.

Country-Level Strategic Snapshot: Battery Coating Industry

Battery Coating Market County Level Snapshot

|

Country / Region

|

Strategic Focus

|

Key Developments

|

|

China

|

Supply control and chemistry diversification

|

Export licensing, sodium-ion hard-carbon coatings, UV inkjet insulation, LMFP carbon coatings

|

|

United States

|

Precision coatings and domestic scale

|

ALD solid electrolyte coatings, graphene cathodes, PVDF capacity, silicon-anode stabilizers

|

|

Germany

|

Solvent-free processing and thermal safety

|

Dry electrode coating pilots, flame-resistant powder coatings, stationary storage protection

|

|

South Korea

|

Safety-first coatings and automation

|

Ceramic-coated separators, solid-state incentives, inkjet insulation adoption

|

|

Japan

|

Solid-state partnerships and structural coatings

|

ASSB sulfide coatings, polyurethane systems for durability

|

Battery Coating Market Report Scope

Battery Coating Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1698.8 Million

|

|

Market Size (2034)

|

$6612.4 Million

|

|

Market Growth Rate

|

16.3%

|

|

Segments

|

By Coating Type (Electrode Coatings, Separator Coatings, Battery Pack and Case Coatings, Tab and Lead Wire Coatings), By Material Chemistry (Polyvinylidene Fluoride, Ceramic Materials, Carbon Based Materials, Polymeric Materials, Solid Electrolyte Interphase Materials), By Technology (Wet Coating, Dry Electrode Coating, Atomic Layer Deposition, Chemical and Physical Vapor Deposition, UV Inkjet Printing), By Battery Chemistry (Lithium Ion, Sodium Ion, Solid State Batteries, Lead Acid and Nickel Metal Hydride), By End Use Industry (Automotive, Consumer Electronics, Energy Storage Systems, Aerospace and Defense)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Arkema, BASF, Solvay, SK Innovation, Toyota Motor Corporation, Asahi Kasei, Axalta Coating Systems, Jotun, Contemporary Amperex Technology, Evonik Industries, Toray Industries, Mitsubishi Chemical Group, Xaar, Lead Intelligent Equipment, Nordson Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Battery Coating Market Segmentation

By Coating Type

- Electrode Coatings

- Separator Coatings

- Battery Pack and Case Coatings

- Tab and Lead Wire Coatings

By Material Chemistry

- Polyvinylidene Fluoride

- Ceramic Materials

- Carbon Based Materials

- Polymeric Materials

- Solid Electrolyte Interphase Materials

By Technology

- Wet Coating

- Dry Electrode Coating

- Atomic Layer Deposition

- Chemical and Physical Vapor Deposition

- UV Inkjet Printing

By Battery Chemistry

- Lithium Ion

- Sodium Ion

- Solid State Batteries

- Lead Acid and Nickel Metal Hydride

By End Use Industry

- Automotive

- Consumer Electronics

- Energy Storage Systems

- Aerospace and Defense

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Battery Coating Industry

- Arkema

- BASF

- Solvay

- SK Innovation

- Toyota Motor Corporation

- Asahi Kasei

- Axalta Coating Systems

- Jotun

- Contemporary Amperex Technology

- Evonik Industries

- Toray Industries

- Mitsubishi Chemical Group

- Xaar

- Lead Intelligent Equipment

- Nordson Corporation

*- List not Exhaustive