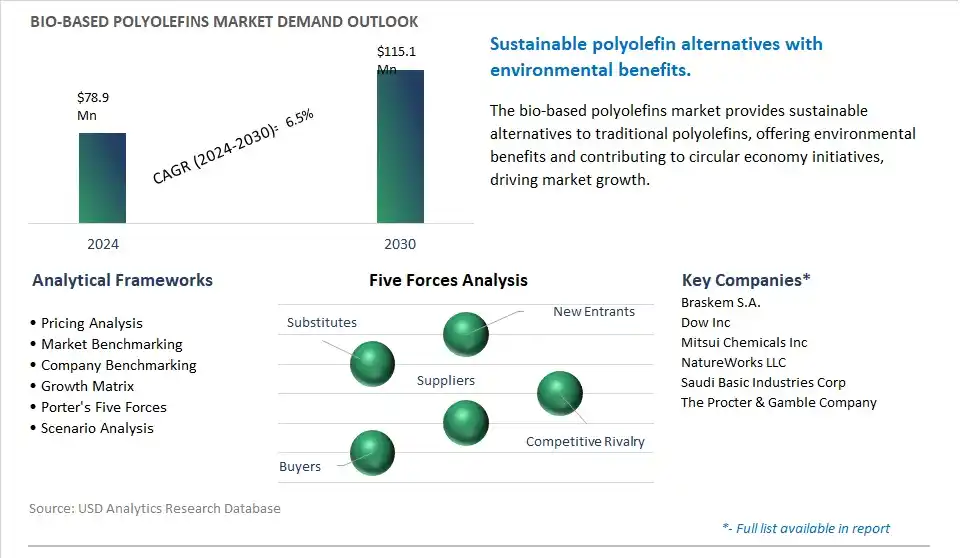

The global Bio-based Polyolefins Market is poised to register a 6.5% CAGR from $78.9 Million in 2024 to $115.1 Million in 2030.

The global Bio-based Polyolefins Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Type (Bio-Based Polyethylene, Bio-Based Polypropylene), By Application (Films, Bottles, Barrels, Tubes, Others).

An Introduction to Global Bio based Polyolefins Market in 2024

The market for bio-based polyolefins is advancing sustainability in packaging, manufacturing, and consumer goods industries as companies seek renewable alternatives to traditional polyolefin plastics. Key trends shaping the future of this industry include the development of polyolefin polymers derived from renewable feedstocks such as plant-based sugars, oils, and biomass, offering advantages in terms of biodegradability, carbon neutrality, and reduced environmental impact compared to fossil fuel-derived polyolefins. Additionally, advancements in polymerization techniques, catalysts, and process optimization enable the production of bio-based polyolefins with properties and performance comparable to traditional plastics, meeting the diverse needs of end-users and brand owners. Moreover, the adoption of sustainability certifications, eco-labeling initiatives, and regulatory mandates drives market demand for bio-based polyolefins, fostering innovation and market expansion in this sector. As industries strive to reduce plastic waste and environmental footprint, the demand for bio-based polyolefins is expected to continue growing, driving further innovation and market development in sustainable plastic materials.

Bio-based Polyolefins Market Competitive Landscape

The market report analyses the leading companies in the industry including Braskem S.A., Dow Inc, Mitsui Chemicals Inc, NatureWorks LLC, Saudi Basic Industries Corp, The Procter & Gamble Company.

Bio-based Polyolefins Market Dynamics

Bio-Based Polyolefins Market Trend: Surge in Demand for Sustainable Packaging Solutions

A prominent trend in the market for bio-based polyolefins is the surge in demand for sustainable packaging solutions. Polyolefins, including polyethylene and polypropylene, are widely used in packaging materials such as films, bottles, and containers due to their excellent properties like durability, flexibility, and moisture resistance. With increasing environmental concerns and the push for circular economy practices, there is a notable shift towards replacing traditional petroleum-based polyolefins with bio-based alternatives. Bio-based polyolefins, derived from renewable biomass sources such as plant oils or bio-based intermediates, offer a sustainable solution with reduced carbon footprint and lower environmental impact. As consumers and regulatory bodies prioritize sustainability, there is a growing demand for bio-based polyolefins in the packaging industry to address the need for eco-friendly and recyclable packaging materials.

Bio-Based Polyolefins Market Driver: Regulatory Mandates and Corporate Sustainability Initiatives

A key driver behind the demand for bio-based polyolefins is regulatory mandates and corporate sustainability initiatives aimed at reducing plastic waste and promoting the use of renewable resources. Governments worldwide are implementing regulations and policies to encourage the adoption of bio-based materials, including polyolefins, in various industries. Additionally, companies are setting ambitious sustainability goals and commitments to reduce their environmental footprint and enhance their corporate social responsibility (CSR) efforts. Bio-based polyolefins align with these regulatory requirements and sustainability objectives by offering a renewable and eco-friendly alternative to conventional polyolefins derived from fossil fuels. As regulatory pressure increases and consumer preferences shift towards sustainable products, the demand for bio-based polyolefins is expected to rise, driving market growth and investment in the industry.

Bio-Based Polyolefins Market Opportunity: Expansion into High-Value Applications and Emerging Markets

An emerging opportunity in the market for bio-based polyolefins lies in expansion into high-value applications and emerging markets. While bio-based polyolefins are already widely used in packaging materials, there is potential for growth in new sectors and niche markets. Opportunities exist to develop bio-based polyolefins with tailored properties and functionalities to meet the needs of specialized industries such as automotive, construction, and consumer goods. Additionally, bio-based polyolefins can capture market share in emerging applications such as 3D printing, medical devices, and durable goods where sustainability and performance are critical factors. By investing in research and development of novel formulations, partnerships with end-users, and market expansion strategies, manufacturers of bio-based polyolefins can capitalize on new opportunities and drive the adoption of sustainable plastics in diverse industries.

Bio-based Polyolefins Market Ecosystem

In the bio-based polyolefins market, various stages involve different companies contributing to the sustainable production and distribution of bio-based polyethylene (PE) and polypropylene (PP). Feedstock production relies on sugarcane growers including Raízen and Tereos, corn farmers, cassava producers including the Thai Tapioca Starch Factory, and companies specializing in feedstock production for bioplastics including Braskem and ISCC System.

Pre-treatment processes are managed by specialized companies including LIG Renewable Fuels and Quadrise Fuels International, potentially followed by bio-based monomer production by bio-based chemical companies including Myriant Corporation and Metabolic Institute, and integrated polyolefin producers including Braskem. Alternatively, Braskem utilizes sugarcane ethanol for bio-PE production, while companies including Lanzatech and LyondellBasell are developing technologies for bio-based propylene production through fermentation. Polymerization, compounding, quality control, distribution, and sales networks involve established polyolefin producers including Dow, ExxonMobil, and LyondellBasell, alongside bio-based polyolefin producers including Braskem, logistic companies, and distributors focusing on sustainable materials. In end-use applications, bio-based polyolefins find usage in packaging, consumer goods, automotive parts, and various other industries, with manufacturers adopting bio-based solutions across different sectors.

Bio-Based Polyolefins Market Share Analysis: Bio-Based Polyethylene held the dominant revenue share in 2024

Among the types in the Bio-Based Polyolefins Market, Bio-Based Polyethylene is the largest segment, driven by diverse significant factors contributing to its dominance. Bio-based polyethylene is widely utilized in various industries due to its versatility, durability, and recyclability. It finds extensive applications in packaging, automotive, construction, and consumer goods industries for manufacturing products such as bottles, containers, films, pipes, and automotive parts. The dominance of Bio-Based Polyethylene can be attributed to diverse factors, including the established infrastructure for polyethylene production, availability of feedstock from renewable sources, and favorable properties of bio-based polyethylene, such as mechanical strength, thermal stability, and resistance to chemicals. In addition, the increasing consumer demand for eco-friendly and sustainable products, coupled with regulatory initiatives promoting the use of bio-based materials, further drive the adoption of Bio-Based Polyethylene. As industries continue to prioritize sustainability and seek alternatives to conventional plastics, the dominance of Bio-Based Polyethylene in the Bio-Based Polyolefins Market is expected to persist, offering manufacturers and suppliers significant opportunities for growth and market expansion.

Bio-Based Polyolefins Market Share Analysis: Films is the fastest growing market segment over the forecast period to 2030

Among the applications in the Bio-Based Polyolefins Market, the Films segment is the fastest-growing, driven by diverse key factors contributing to its rapid expansion. Bio-based polyolefin films find extensive use in various industries for packaging, agricultural, and industrial applications due to their versatility, flexibility, and barrier properties. The film segment experiences rapid growth due to increasing consumer demand for sustainable and eco-friendly packaging solutions, coupled with regulatory mandates promoting the use of bio-based materials. Additionally, advancements in film manufacturing technology have enhanced the performance and cost-effectiveness of bio-based polyolefin films, making them competitive alternatives to conventional petroleum-based films. In addition, the versatility of bio-based polyolefin films allows for customization to meet specific packaging requirements, further fueling their adoption across industries. As industries continue to prioritize sustainability and seek alternatives to conventional plastics, the Films segment in the Bio-Based Polyolefins Market is expected to experience sustained growth, presenting significant opportunities for manufacturers and suppliers to meet market demands and drive further innovation.

Bio-based Polyolefins Market Report Scope-

By Type

Bio-Based Polyethylene

Bio-Based Polypropylene

By Application

Films

Bottles

Barrels

Tubes

Others

Bio-based Polyolefins Market Companies Profiled

Braskem S.A.

Dow Inc

Mitsui Chemicals Inc

NatureWorks LLC

Saudi Basic Industries Corp

The Procter & Gamble Company

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Bio-based Polyolefins Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Bio-based Polyolefins Market Size Outlook, $ Million, 2021 to 2030

3.2 Bio-based Polyolefins Market Outlook by Type, $ Million, 2021 to 2030

3.3 Bio-based Polyolefins Market Outlook by Product, $ Million, 2021 to 2030

3.4 Bio-based Polyolefins Market Outlook by Application, $ Million, 2021 to 2030

3.5 Bio-based Polyolefins Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Bio-based Polyolefins Industry

4.2 Key Market Trends in Bio-based Polyolefins Industry

4.3 Potential Opportunities in Bio-based Polyolefins Industry

4.4 Key Challenges in Bio-based Polyolefins Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Bio-based Polyolefins Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Bio-based Polyolefins Market Outlook by Segments

7.1 Bio-based Polyolefins Market Outlook by Segments, $ Million, 2021- 2030

By Type

Bio-Based Polyethylene

Bio-Based Polypropylene

By Application

Films

Bottles

Barrels

Tubes

Others

8 North America Bio-based Polyolefins Market Analysis and Outlook To 2030

8.1 Introduction to North America Bio-based Polyolefins Markets in 2024

8.2 North America Bio-based Polyolefins Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Bio-based Polyolefins Market size Outlook by Segments, 2021-2030

By Type

Bio-Based Polyethylene

Bio-Based Polypropylene

By Application

Films

Bottles

Barrels

Tubes

Others

9 Europe Bio-based Polyolefins Market Analysis and Outlook To 2030

9.1 Introduction to Europe Bio-based Polyolefins Markets in 2024

9.2 Europe Bio-based Polyolefins Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Bio-based Polyolefins Market Size Outlook by Segments, 2021-2030

By Type

Bio-Based Polyethylene

Bio-Based Polypropylene

By Application

Films

Bottles

Barrels

Tubes

Others

10 Asia Pacific Bio-based Polyolefins Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Bio-based Polyolefins Markets in 2024

10.2 Asia Pacific Bio-based Polyolefins Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Bio-based Polyolefins Market size Outlook by Segments, 2021-2030

By Type

Bio-Based Polyethylene

Bio-Based Polypropylene

By Application

Films

Bottles

Barrels

Tubes

Others

11 South America Bio-based Polyolefins Market Analysis and Outlook To 2030

11.1 Introduction to South America Bio-based Polyolefins Markets in 2024

11.2 South America Bio-based Polyolefins Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Bio-based Polyolefins Market size Outlook by Segments, 2021-2030

By Type

Bio-Based Polyethylene

Bio-Based Polypropylene

By Application

Films

Bottles

Barrels

Tubes

Others

12 Middle East and Africa Bio-based Polyolefins Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Bio-based Polyolefins Markets in 2024

12.2 Middle East and Africa Bio-based Polyolefins Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Bio-based Polyolefins Market size Outlook by Segments, 2021-2030

By Type

Bio-Based Polyethylene

Bio-Based Polypropylene

By Application

Films

Bottles

Barrels

Tubes

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Braskem S.A.

Dow Inc

Mitsui Chemicals Inc

NatureWorks LLC

Saudi Basic Industries Corp

The Procter & Gamble Company

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Type

Bio-Based Polyethylene

Bio-Based Polypropylene

By Application

Films

Bottles

Barrels

Tubes

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)