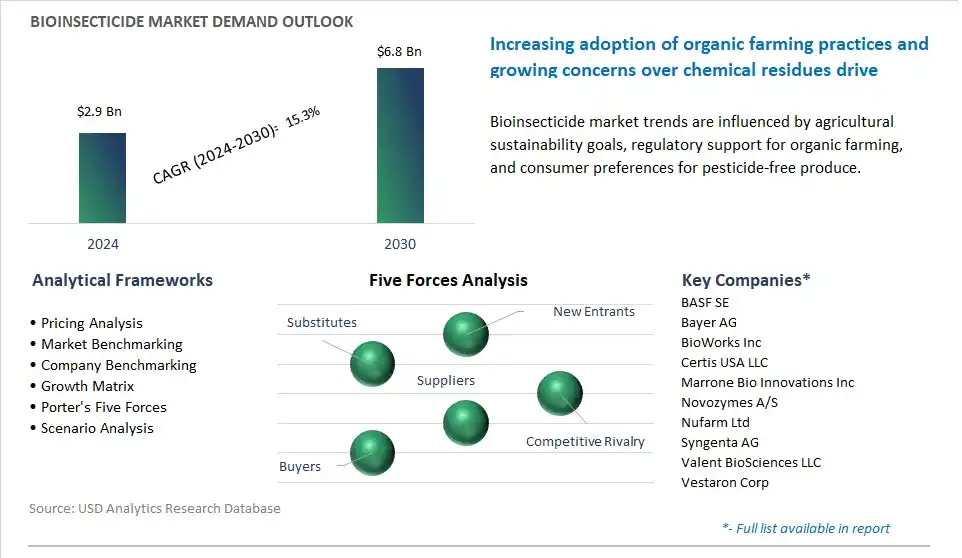

The global Bioinsecticide Market is poised to register a 15.3% CAGR from $2.9 Billion in 2024 to $6.8 Billion in 2030.

The global Bioinsecticide Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Source (Microbials, Plants, Others), By Application (Cereals & Grains, Oilseed and Pulses, Fruits and Vegetables, Others).

An Introduction to Global Bioinsecticide Market in 2024

The market for bioinsecticides is witnessing growth driven by the increasing demand for safe, eco-friendly pest management solutions in agriculture, horticulture, and public health sectors. Key trends shaping the future of the industry include innovations in microbial strains, formulation technologies, and application methods to meet the requirements for effective, selective, and sustainable insect control. Advanced bioinsecticides offer benefits such as target specificity, environmental compatibility, and minimal residual effects, making them essential for integrated pest management (IPM) programs and organic farming practices. Moreover, the integration of biotechnological tools, such as genetic engineering, fermentation, and encapsulation, enhances bioinsecticide efficacy, stability, and shelf-life, enabling producers to offer products with improved performance characteristics and application flexibility. Additionally, the growing emphasis on food safety, residue regulations, and biodiversity conservation drives market demand for bioinsecticides that provide alternatives to conventional chemical pesticides, minimize environmental impact, and support ecosystem resilience. As farmers, growers, and pest control professionals seek solutions to manage insect pests while minimizing risks to human health and the environment, the bioinsecticide market is poised for continued growth and innovation as a sustainable and effective tool for crop protection and public health management.

Bioinsecticide Market Competitive Landscape

The market report analyses the leading companies in the industry including BASF SE, Bayer AG, BioWorks Inc, Certis USA LLC, Marrone Bio Innovations Inc, Novozymes A/S, Nufarm Ltd, Syngenta AG, Valent BioSciences LLC, Vestaron Corp.

Bioinsecticide Market Dynamics

Bioinsecticide Market Trend: Growing Preference for Sustainable Pest Control Solutions

A prominent trend in the bioinsecticide market is the growing preference for sustainable pest control solutions. With increasing concerns about environmental and human health, there is a rising demand for bio-based alternatives to synthetic pesticides. Bioinsecticides, derived from natural sources such as plants, bacteria, fungi, or insect predators, offer effective pest control while minimizing environmental impact and reducing chemical residues in food and soil. This trend is driven by consumer awareness, regulatory restrictions on synthetic pesticides, and industry initiatives towards sustainable agriculture, shaping the future of the bioinsecticide market towards greater adoption of environmentally friendly pest management solutions.

Bioinsecticide Market Driver: Regulatory Pressure and Consumer Demand for Safer Products

The primary driver behind the growth of the bioinsecticide market is regulatory pressure and consumer demand for safer pest control products. Governments worldwide are implementing stricter regulations on pesticide use to protect human health, wildlife, and the environment. Additionally, consumers are becoming more conscious of the potential health risks associated with chemical pesticides and are seeking safer alternatives. Bioinsecticides, being inherently less toxic and environmentally friendly, align with regulatory requirements and consumer preferences for safer and more sustainable pest management solutions. This driver is fueled by increasing public awareness of pesticide-related health risks, regulatory bans on hazardous pesticides, and market demand for organic and sustainably produced food, stimulating market growth and investment in bioinsecticide technologies.

Bioinsecticide Market Opportunity: Expansion into Organic Agriculture and Non-Crop Applications

An opportunity for market growth within the bioinsecticide sector lies in the expansion into organic agriculture and non-crop applications. While bioinsecticides are widely used in conventional agriculture to control pests on crops such as fruits, vegetables, and grains, there are untapped opportunities in organic farming and non-agricultural sectors such as forestry, public health, and household pest control. Bioinsecticides offer advantages such as organic certification, low toxicity to beneficial organisms, and compatibility with integrated pest management (IPM) practices, making them ideal for use in organic farming systems. By developing specialized formulations and application methods tailored to the needs of organic growers and non-agricultural users, bioinsecticide manufacturers can capitalize on the growing demand for organic products, expand their market presence, and diversify their product portfolios to meet evolving pest management needs. Additionally, collaboration with organic certifiers, agricultural extension services, and public health agencies enables bioinsecticide suppliers to address market needs, comply with regulatory requirements, and drive market expansion in emerging sectors.

Bioinsecticide Market Share Analysis: Microbials segment generated the highest revenue in the industry

The Microbials segment is the largest segment in the Bioinsecticide Market for diverse compelling reasons. The microbials, including bacteria, fungi, viruses, and protozoa, are widely recognized for their efficacy in controlling insect pests while offering diverse advantages over conventional chemical insecticides. Microbial bioinsecticides act through various mechanisms such as pathogenicity, parasitism, and toxin production, targeting specific pests with minimal impact on non-target organisms and the environment. Additionally, microbial bioinsecticides exhibit high specificity, targeting pests at different life stages while sparing beneficial insects, pollinators, and natural enemies. In addition, microbial bioinsecticides are compatible with integrated pest management (IPM) strategies and organic farming practices, providing growers with effective pest control options while meeting regulatory requirements and consumer preferences for sustainable agriculture. Further, advancements in microbial strain selection, formulation technologies, and application methods enhance the performance, shelf life, and efficacy of microbial bioinsecticides, further driving their adoption in agriculture. As growers increasingly seek alternatives to conventional chemical pesticides to address pest resistance, environmental concerns, and regulatory restrictions, the Microbials segment maintains its dominance as the largest segment in the Bioinsecticide Market, supporting the growth of sustainable pest management practices.

Bioinsecticide Market Share Analysis: Fruits and Vegetables Segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The Fruits and Vegetables segment is the fastest-growing segment in the Bioinsecticide Market for diverse compelling reasons. The fruits and vegetables are highly susceptible to insect pest infestations, leading to significant yield losses, post-harvest losses, and quality deterioration. Additionally, consumers and regulatory agencies are increasingly concerned about pesticide residues in food products, driving the demand for safer and more sustainable pest control solutions in fruit and vegetable production. In addition, the adoption of integrated pest management (IPM) practices and organic farming methods in the fruit and vegetable sector creates opportunities for bioinsecticides as effective alternatives to conventional chemical pesticides. Further, the growing consumer demand for organic and pesticide-free fruits and vegetables further stimulates the market for bioinsecticides in this segment. As growers prioritize sustainable pest management practices to meet consumer preferences, regulatory requirements, and market demands, the Fruits and Vegetables segment experiences rapid growth in the Bioinsecticide Market.

Bioinsecticide Market Report Segmentation

By Source

Microbials

Plants

Others

By Application

Cereals & Grains

Oilseed and Pulses

Fruits and Vegetables

Others

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Bioinsecticide Companies Profiled in the Market Study

BASF SE

Bayer AG

BioWorks Inc

Certis USA LLC

Marrone Bio Innovations Inc

Novozymes A/S

Nufarm Ltd

Syngenta AG

Valent BioSciences LLC

Vestaron Corp

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Bioinsecticide Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Bioinsecticide Market Size Outlook, $ Million, 2021 to 2030

3.2 Bioinsecticide Market Outlook by Type, $ Million, 2021 to 2030

3.3 Bioinsecticide Market Outlook by Product, $ Million, 2021 to 2030

3.4 Bioinsecticide Market Outlook by Application, $ Million, 2021 to 2030

3.5 Bioinsecticide Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Bioinsecticide Industry

4.2 Key Market Trends in Bioinsecticide Industry

4.3 Potential Opportunities in Bioinsecticide Industry

4.4 Key Challenges in Bioinsecticide Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Bioinsecticide Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Bioinsecticide Market Outlook by Segments

7.1 Bioinsecticide Market Outlook by Segments, $ Million, 2021- 2030

By Source

Microbials

Plants

Others

By Application

Cereals & Grains

Oilseed and Pulses

Fruits and Vegetables

Others

8 North America Bioinsecticide Market Analysis and Outlook To 2030

8.1 Introduction to North America Bioinsecticide Markets in 2024

8.2 North America Bioinsecticide Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Bioinsecticide Market size Outlook by Segments, 2021-2030

By Source

Microbials

Plants

Others

By Application

Cereals & Grains

Oilseed and Pulses

Fruits and Vegetables

Others

9 Europe Bioinsecticide Market Analysis and Outlook To 2030

9.1 Introduction to Europe Bioinsecticide Markets in 2024

9.2 Europe Bioinsecticide Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Bioinsecticide Market Size Outlook by Segments, 2021-2030

By Source

Microbials

Plants

Others

By Application

Cereals & Grains

Oilseed and Pulses

Fruits and Vegetables

Others

10 Asia Pacific Bioinsecticide Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Bioinsecticide Markets in 2024

10.2 Asia Pacific Bioinsecticide Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Bioinsecticide Market size Outlook by Segments, 2021-2030

By Source

Microbials

Plants

Others

By Application

Cereals & Grains

Oilseed and Pulses

Fruits and Vegetables

Others

11 South America Bioinsecticide Market Analysis and Outlook To 2030

11.1 Introduction to South America Bioinsecticide Markets in 2024

11.2 South America Bioinsecticide Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Bioinsecticide Market size Outlook by Segments, 2021-2030

By Source

Microbials

Plants

Others

By Application

Cereals & Grains

Oilseed and Pulses

Fruits and Vegetables

Others

12 Middle East and Africa Bioinsecticide Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Bioinsecticide Markets in 2024

12.2 Middle East and Africa Bioinsecticide Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Bioinsecticide Market size Outlook by Segments, 2021-2030

By Source

Microbials

Plants

Others

By Application

Cereals & Grains

Oilseed and Pulses

Fruits and Vegetables

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

BASF SE

Bayer AG

BioWorks Inc

Certis USA LLC

Marrone Bio Innovations Inc

Novozymes A/S

Nufarm Ltd

Syngenta AG

Valent BioSciences LLC

Vestaron Corp

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Source

Microbials

Plants

Others

By Application

Cereals & Grains

Oilseed and Pulses

Fruits and Vegetables

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)