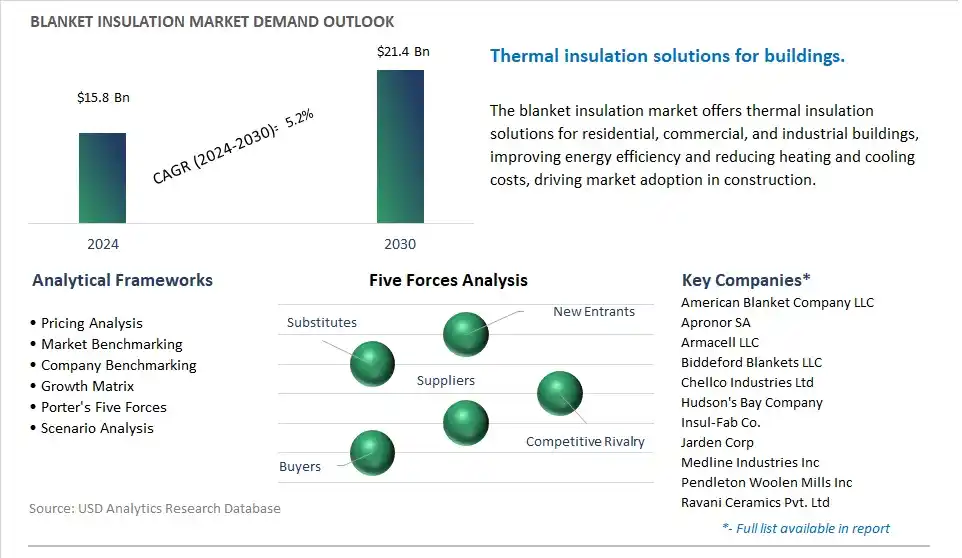

The global Blanket Insulation Market is poised to register a 5.2% CAGR from $15.8 Billion in 2024 to $21.4 Billion in 2030.

The global Blanket Insulation Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Application (Building & Construction, Transportation, Industrial, Appliances, Others).

An Introduction to Global Blanket Insulation Market in 2024

The market for blanket insulation is enhancing energy efficiency and comfort in buildings by providing effective thermal insulation solutions for walls, roofs, and floors. Key trends shaping the future of this industry include the development of blanket insulation materials with advanced thermal properties, such as high R-values and low thermal conductivity, optimizing energy conservation and reducing heating and cooling costs in residential, commercial, and industrial structures. Additionally, advancements in insulation manufacturing processes, fiber technology, and installation techniques enable the production and installation of blanket insulation that conforms seamlessly to building contours, minimizing thermal bridging and air leakage for superior insulation performance. Moreover, the adoption of energy efficiency regulations, green building certifications, and sustainability standards drives market demand for blanket insulation, fostering innovation and market expansion in this sector. As building owners, contractors, and architects prioritize energy-efficient building designs and occupant comfort, the demand for blanket insulation is expected to continue growing, driving further innovation and development of advanced insulation solutions in the construction industry.

Blanket Insulation Market Competitive Landscape

The market report analyses the leading companies in the industry including American Blanket Company LLC, Apronor SA, Armacell LLC, Biddeford Blankets LLC, Chellco Industries Ltd, Hudson's Bay Company, Insul-Fab Co., Jarden Corp, Medline Industries Inc, Pendleton Woolen Mills Inc, Ravani Ceramics Pvt. Ltd, Refmon Ltd, Shanghai Easun Group Co. Ltd, Thermaxx Jackets LLC, Urbanara GmbH.

Blanket Insulation Market Dynamics

Blanket Insulation Market Trend: Increasing Emphasis on Energy Efficiency in Buildings

A prominent trend in the market for blanket insulation is the increasing emphasis on energy efficiency in buildings. With growing awareness of climate change and the need to reduce energy consumption, building owners and developers are prioritizing energy-efficient construction practices. Blanket insulation, also known as batt insulation, offers an effective solution for thermal insulation in walls, floors, and attics, helping to reduce heat loss and improve indoor comfort while lowering heating and cooling costs. As energy codes and regulations become more stringent, and as consumers seek to reduce their carbon footprint, the demand for blanket insulation is expected to rise, driving market growth and innovation in the construction industry.

Blanket Insulation Market Driver: Retrofitting and Renovation Projects in Existing Buildings

A key driver behind the demand for blanket insulation is retrofitting and renovation projects in existing buildings. As aging buildings require upgrades to meet modern energy efficiency standards and improve occupant comfort, there is a growing need for insulation solutions that can be easily installed in walls, ceilings, and floors without major construction disruptions. Blanket insulation offers a cost-effective and efficient option for retrofitting projects, providing thermal insulation and acoustic insulation benefits while minimizing disruption to occupants and ongoing operations. With increasing investments in building upgrades and energy efficiency retrofits, the demand for blanket insulation is expected to continue growing, driving market expansion and investment in building materials and construction services.

Blanket Insulation Market Opportunity: Development of High-Performance and Sustainable Insulation Materials

An emerging opportunity in the market for blanket insulation lies in the development of high-performance and sustainable insulation materials. While traditional fiberglass and mineral wool batts dominate the market, there is potential for growth in exploring new materials that offer improved thermal performance, fire resistance, moisture management, and environmental sustainability. Opportunities exist to develop innovative insulation materials using recycled content, bio-based fibers, or aerogel technologies that offer superior insulation properties and reduced environmental impact. Additionally, advancements in manufacturing processes such as compression molding, spray-on insulation, or vacuum insulation panels can enable the production of thinner and lighter insulation products with enhanced performance characteristics. By investing in research and development of next-generation insulation materials and collaborating with architects, builders, and insulation contractors, suppliers of blanket insulation can capitalize on new opportunities and drive market growth in the construction industry, contributing to more energy-efficient and sustainable buildings.

Blanket Insulation Market Ecosystem

In the blanket insulation market, the Ecosystem encompasses diverse critical stages, each involving specific companies to ensure efficient production and application of insulation materials. Raw material production involves various entities, including mining companies for mineral wool, glass manufacturers for glass wool, recycling facilities for natural fibers including recycled cellulose, and chemical companies for synthetic fibers including polyester. Additionally, metal manufacturers and plastics producers supply facings including reflective foils or vapor barrier films. These materials are then processed in insulation manufacturing, where established manufacturers including Knauf Insulation and Johns Manville, as well as specialty producers including Rockwool, convert them into blanket insulation using methods including blowing, needling, and bonding.

Distribution and sales are facilitated by building material distributors, insulation distributors, and manufacturers with established distribution networks, delivering blanket insulation to construction projects. Installation, a crucial stage, involves insulation contractors specializing in building applications or construction companies with qualified insulation installation crews, ensuring proper placement to enhance thermal performance and energy efficiency while avoiding air gaps. Maintenance services involve periodic inspection by building inspectors or energy auditors and include minor repairs or replacement, provided by insulation contractors specializing in maintenance and repair, to uphold insulation effectiveness over time.

Blanket Insulation Market Share Analysis: Building and Construction held the dominant revenue share in 2024

In the Blanket Insulation Market, the largest segment is building and construction, and this dominance can be attributed to diverse key factors. Firstly, the construction industry is one of the largest consumers of insulation materials due to the significant need for thermal and acoustic insulation in buildings and structures. Blanket insulation, also known as batt insulation, is widely used in residential, commercial, and industrial construction projects for its ease of installation, versatility, and cost-effectiveness. In addition, increasing awareness about energy efficiency and sustainability in construction practices has led to a surge in demand for high-performance insulation materials like blanket insulation. Additionally, stringent building codes and regulations mandating the use of insulation to improve energy efficiency further drive the adoption of blanket insulation in building projects. Further, the growing trend of retrofitting existing buildings with insulation to enhance energy efficiency contributes to the growth of the building and construction segment in the Blanket Insulation Market. Overall, the building and construction segment holds the largest share in the market due to the indispensable role of insulation in enhancing building performance, energy efficiency, and occupant comfort.

Blanket Insulation Market Report Scope-

By Application

Building & Construction

Transportation

Industrial

Appliances

Others

Blanket Insulation Market Companies Profiled

American Blanket Company LLC

Apronor SA

Armacell LLC

Biddeford Blankets LLC

Chellco Industries Ltd

Hudson's Bay Company

Insul-Fab Co.

Jarden Corp

Medline Industries Inc

Pendleton Woolen Mills Inc

Ravani Ceramics Pvt. Ltd

Refmon Ltd

Shanghai Easun Group Co. Ltd

Thermaxx Jackets LLC

Urbanara GmbH

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Blanket Insulation Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Blanket Insulation Market Size Outlook, $ Million, 2021 to 2030

3.2 Blanket Insulation Market Outlook by Type, $ Million, 2021 to 2030

3.3 Blanket Insulation Market Outlook by Product, $ Million, 2021 to 2030

3.4 Blanket Insulation Market Outlook by Application, $ Million, 2021 to 2030

3.5 Blanket Insulation Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Blanket Insulation Industry

4.2 Key Market Trends in Blanket Insulation Industry

4.3 Potential Opportunities in Blanket Insulation Industry

4.4 Key Challenges in Blanket Insulation Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Blanket Insulation Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Blanket Insulation Market Outlook by Segments

7.1 Blanket Insulation Market Outlook by Segments, $ Million, 2021- 2030

By Application

Building & Construction

Transportation

Industrial

Appliances

Others

8 North America Blanket Insulation Market Analysis and Outlook To 2030

8.1 Introduction to North America Blanket Insulation Markets in 2024

8.2 North America Blanket Insulation Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Blanket Insulation Market size Outlook by Segments, 2021-2030

By Application

Building & Construction

Transportation

Industrial

Appliances

Others

9 Europe Blanket Insulation Market Analysis and Outlook To 2030

9.1 Introduction to Europe Blanket Insulation Markets in 2024

9.2 Europe Blanket Insulation Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Blanket Insulation Market Size Outlook by Segments, 2021-2030

By Application

Building & Construction

Transportation

Industrial

Appliances

Others

10 Asia Pacific Blanket Insulation Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Blanket Insulation Markets in 2024

10.2 Asia Pacific Blanket Insulation Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Blanket Insulation Market size Outlook by Segments, 2021-2030

By Application

Building & Construction

Transportation

Industrial

Appliances

Others

11 South America Blanket Insulation Market Analysis and Outlook To 2030

11.1 Introduction to South America Blanket Insulation Markets in 2024

11.2 South America Blanket Insulation Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Blanket Insulation Market size Outlook by Segments, 2021-2030

By Application

Building & Construction

Transportation

Industrial

Appliances

Others

12 Middle East and Africa Blanket Insulation Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Blanket Insulation Markets in 2024

12.2 Middle East and Africa Blanket Insulation Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Blanket Insulation Market size Outlook by Segments, 2021-2030

By Application

Building & Construction

Transportation

Industrial

Appliances

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

American Blanket Company LLC

Apronor SA

Armacell LLC

Biddeford Blankets LLC

Chellco Industries Ltd

Hudson's Bay Company

Insul-Fab Co.

Jarden Corp

Medline Industries Inc

Pendleton Woolen Mills Inc

Ravani Ceramics Pvt. Ltd

Refmon Ltd

Shanghai Easun Group Co. Ltd

Thermaxx Jackets LLC

Urbanara GmbH

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Application

Building & Construction

Transportation

Industrial

Appliances

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)