Market Overview: Blowing Agents Market Growth Fueled by HFO Capacity Additions, Low-GWP Formulations, and Supply Chain Localization (2025–2034)

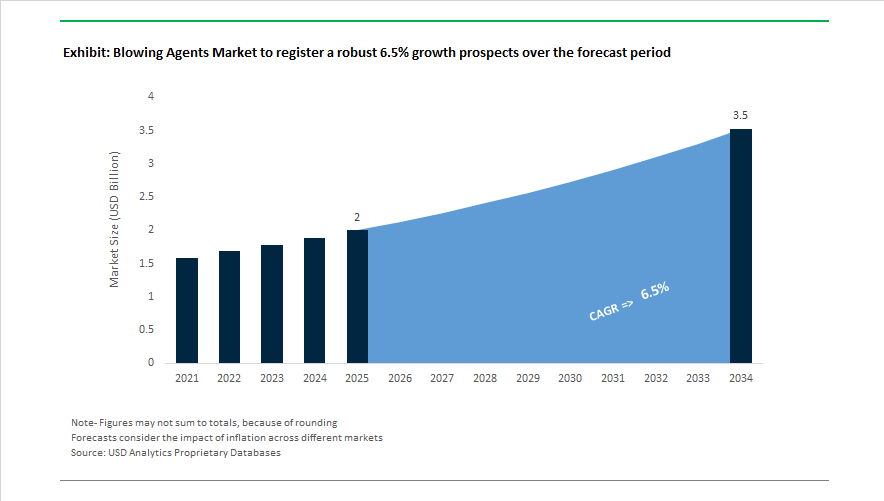

The blowing agents market is projected to expand from USD 2 billion in 2025 to USD 3.5 billion by 2034, registering a CAGR of 6.5% supported by accelerating adoption of hydrofluoroolefin blowing agents, low-global-warming-potential foam technologies, and energy-efficient insulation systems. Market momentum strengthened in 2024 when Solvay inaugurated production of its Alve-One chemical blowing agent in Italy, providing an eco-friendly alternative to traditional azodicarbonamide for automotive interiors and footwear foams. In February 2024, BASF launched an HFO-blown PIR insulation system in Japan with TATUMI Industrial, delivering enhanced fire performance and thermal efficiency for cold storage and data center infrastructure. During mid-2023 through 2024, Dow completed polyurethane systems capacity expansion to serve construction demand reliant on advanced blowing agent technologies for high R-value insulation.

Industrial transformation accelerated through 2025 with major HFO investments and corporate restructuring. In May 2025, Chemours partnered with Navin Fluorine International to manufacture Opteon specialty fluids in India, leveraging HFO chemistry platforms common to next-generation blowing agents. In August 2025, Arkema opened a $60 million Forane 1233zd HFO plant in Kentucky, raising North American output to 15 kilotons per year for appliance and spray foam markets. The same month, Arkema converted a legacy R134a line to HFO 1233zd, reflecting rapid HFC phase-down compliance. In August 2025, Chemours signed a strategic supply agreement with SRF Limited to secure fluorochemical capacity, while Honeywell finalized the October 2025 spin-off of its Advanced Materials business into Solstice Advanced Materials, creating a dedicated HFO blowing agent company focused on sustainability technologies.

Regulatory changes and manufacturing optimization are shaping the competitive landscape entering 2026. In January 2025, new U.S. tariff measures on fluorinated intermediates prompted producers to localize supply chains and diversify sourcing. In February 2025, Honeywell deployed generative AI through its Forge Production Intelligence platform to improve yield and energy efficiency in HFO synthesis. In July 2024, BASF and Dow initiated collaboration on low-GWP blowing agent formulations to meet stringent building efficiency standards. Regulatory developments continued in November 2025 when the European Chemicals Agency advanced discussions on ethanol-based specialty agents, with final labeling decisions expected in early 2026.

Strategic Market Trends Reshaping Blowing Agent Selection and Manufacturing Models

Kigali Amendment Enforcement Accelerates Global Shift From HFCs to HFO-Based Blowing Agents

International decarbonization frameworks are now directly transforming blowing agent procurement in the insulation, appliances, and refrigeration industries. The Kigali Amendment reached an implementation tipping point in late 2025, with more than 165 countries enforcing mandatory HFC phase-downs. Article 5 (Group 2) economies began their consumption freeze in September 2025, requiring baselines to be calculated on 2024–2026 usage averages. This has triggered accelerated demand for low-GWP HFO blowing agents, particularly HFO-1233zd and HFO-1336mzz, which are used as direct replacements for legacy HFC-245fa in rigid polyurethane foam. Strategically, industrial suppliers are restructuring portfolios to capitalize on this shift. Honeywell’s October 2025 spin-off of Solstice Advanced Materials demonstrates the market’s commercial magnitude. The standalone entity reported that HFO-linked revenue fundamentals drove USD 1.3 billion in 2024 sales and has deployed 2025 capital expenditure toward HFO production capacity in proximity to insulation and composites manufacturing clusters.

Hybrid Co-Blowing Agent Systems Gain Favor for Thermal Conductivity Optimization

To balance cost efficiency with sustainability performance, rigid foam manufacturers are increasingly adopting hybrid blowing agent systems that blend HFOs with hydrocarbons (such as cyclopentane) or CO2. This co-formulation approach supports lower thermal conductivity (k-factor) while reducing system cost. METI Japan studies from November 2025 reported that residential rigid polyurethane foam has achieved weighted-average GWP values of 17.3 using HFO-water hybridization, equating to more than 90% reduction versus HFC-134a baselines. Simultaneously, global case studies presented at K2025 (Düsseldorf) evidenced that hybrid systems using HFO-1234ze and cyclopentane can decrease total blowing agent expenditure by 15 to 20 percent, while maintaining strength and dimensional stability in commercial refrigeration foam panels. This positions hybrid systems as an operational bridge for manufacturers still adapting to 2025 EU climate compliance limits of GWP below 750 for split AC applications.

Chemical Blowing Agents Enable EV Lightweighting and Electric Range Enhancement

Electric Vehicle (EV) OEMs are expanding their adoption of Chemical Blowing Agents (CBAs) in Foam Injection Molding (FIM) to reduce polymer usage and enhance structural efficiency in interior and exterior components. Microcellular foaming platforms such as MuCell and Gentrex demonstrated in August 2025 that CBAs can lower material consumption in automotive door modules by 10 to 30%. Reduced mass directly supports drivetrain efficiency; every 10% vehicle-weight reduction translates to a 6 to 8% increase in driving range. Beyond weight reduction, CBAs improve processing economics by lowering injection pressure and clamp force requirements by 25 to 50 percent, enabling production scale-up using smaller presses (for example, a 300-ton press instead of a 500-ton press), which lowers both energy demand and capital expenditure for Tier-1 suppliers.

Solid ADC and OBSH Blowing Agents Gain Momentum in Passive Fire Protection and Intumescent Coatings

Urban construction, downstream petrochemicals, and LNG infrastructure are fueling demand for solid blowing agents such as Azodicarbonamide (ADC) and OBSH for specialized passive fire protection systems. These blowing agents function as heat-responsive expansion catalysts, contributing to intumescent carbonaceous char formation that protects structural steel. Within the USD 1.43 billion intumescent coatings market in 2025, adoption is rising fastest in geographies facing high-density urbanization and stringent refinery safety mandates. Gulf Coast and Middle Eastern energy projects now specify hydrocarbon-rated epoxy systems designed to withstand temperatures above 1,100°C. OBSH-based formulations are increasingly preferred to ensure stable char morphology and extend insulation time to approximately 120 minutes, preserving structural integrity and enabling personnel evacuation in critical fire events.

Blowing Agents Market Share and Segmentation Insights

Market Share by Product Type: Hydrocarbons Lead Volume as HFOs Disrupt High-GWP Legacy Systems

Hydrocarbons command 41% of the Blowing Agents Market in 2025, led by cyclopentane adoption in rigid polyurethane foams for appliances and construction insulation, favored for low cost, zero ozone depletion, and low global warming potential despite flammability constraints. Hydrofluoroolefins are the fastest-growing segment, gaining rapid traction in spray foam, panel boards, and XPS insulation as HFO-1233zd(E) and HFO-1336mzz(Z) replace legacy HFCs under Kigali Amendment-driven phase-downs. Hydrofluorocarbons are in structural decline as regulatory taxes and bans accelerate substitution. Inert gases such as CO₂ and nitrogen support niche XPS and phenolic foam applications, while natural and specialty agents including water, methyl formate, and methylal expand in integral skin and one-component foams. HCFCs retain only residual demand in legacy systems, with global consumption continuing to contract sharply.

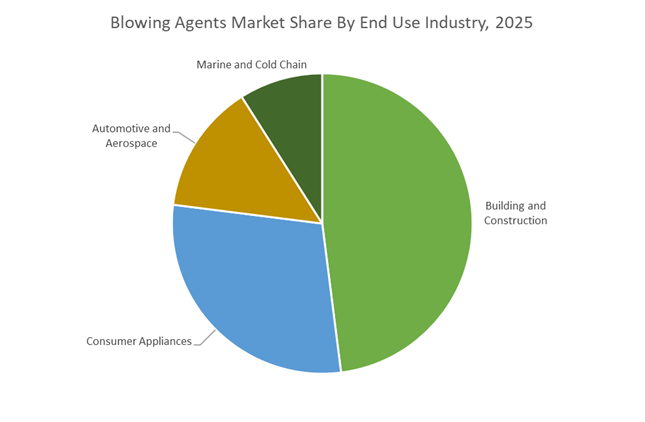

Market Share by End Use Industry: Construction Insulation Anchors Demand as EVs and Cold Chain Add Momentum

Building and construction represent 48% of blowing agent consumption in 2025, driven by polyurethane spray foam, PIR boards, and XPS panels aligned with energy efficiency codes, net-zero building mandates, and fire safety standards. Consumer appliances follow as refrigerators and freezers rely on cyclopentane-blown insulation, supported by replacement cycles and penetration in emerging markets. Automotive and aerospace form an expanding segment, utilizing water-blown and HFO-based foams for seating, acoustic insulation, and lightweight components, with EV battery thermal management emerging as a new growth vector. Marine and cold chain applications remain specialized but strategic, demanding high-performance insulation for refrigerated containers, cold storage, and pharmaceutical logistics, where HFO- and cyclopentane-based systems dominate due to moisture resistance and dimensional stability.

Competitive Landscape Analysis of the Blowing Agents Market

The global blowing agents market in 2026 is being reshaped by ultra-low GWP regulations, electrification, green building codes, and rapid growth in polyurethane foam insulation, EV components, and energy-efficient appliances. Competition now centers on HFO blowing agents, physical CO2 systems, mineral-based foaming technologies, and integrated foam solutions that deliver higher R-values, fire resistance, and reduced Scope 3 emissions. Market leaders are differentiating through sustainability pure-play strategies, hybrid HFO systems, AI-driven manufacturing, and closed-loop gas management, positioning blowing agents as critical enablers of next-generation construction materials, automotive lightweighting, footwear foams, and data center thermal management.

Honeywell International Inc. pioneers ultra-low GWP HFO blowing agents for sustainable insulation

Honeywell enters 2026 amid a major transformation, spinning off its Advanced Materials business to create a sustainability-focused blowing agent pure-play. Its Solstice® LBA remains a flagship HFO, delivering a GWP of 1 while improving polyurethane foam R-value by up to 6% , making it a benchmark for green building insulation. In 2025/2026, Honeywell embedded Generative AI into Forge Production Intelligence to maximize fluorinated molecule yields ahead of global demand growth. With a powerful HFO patent portfolio and deep OEM collaboration, Honeywell leads regulatory stewardship while accelerating adoption of next-generation blowing agents for HVAC, appliances, and construction.

The Chemours Company advances application-specific blowing solutions for EVs and data centers

Chemours leverages its Opteon™ and Freon™ platforms to serve high-performance foam and thermal management markets. In 2026, Opteon™ 1100 dominates premium spray foam applications due to superior thermal resistance and chemical stability. The company has shifted toward application-driven innovation, repurposing blowing agent chemistry into dielectric heat transfer fluids such as Opteon™ 2P50 for hyperscale data centers. Deep automotive integration positions Chemours as a key supplier for EV battery enclosure foams requiring fire retardancy and insulation. Its 2026 strategy emphasizes responsible manufacturing, legacy risk resolution, and targeted growth in semiconductors and next-generation refrigerants.

Arkema scales hybrid and bio-sourced blowing agents across Europe and Asia

Arkema has built a strong presence in low-GWP construction foams through its Forane® portfolio, with Forane® 1233zd widely adopted for high-pressure spray foam and appliance insulation. Expansion across Japan and South Korea reflects tightening energy-efficiency mandates and accelerated HCFC phase-outs. In early 2026, Arkema commercialized hybrid blowing systems combining HFOs with CO2 or water to balance cost and thermal performance. Its strategic focus on bio-sourced transitions includes integrating renewable feedstocks to reduce cradle-to-gate carbon footprints, reinforcing Arkema’s positioning in sustainable blowing agents for advanced building materials.

BASF integrates blowing agents into complete foam system solutions

BASF approaches the market as a full system house, embedding blowing agents into proprietary foam platforms such as Lupranate® and Elastollan®. At Plastindia 2026, BASF highlighted Neopor® BMB grey insulation using biomass balance feedstocks to cut fossil inputs. The company also introduced supercritical fluid direct-injection for footwear, enabling high-performance midsoles without conventional chemical blowing agents. Through Ultrasim® simulation, customers can digitally model foam expansion in complex molds, reducing development cycles. BASF’s Green Verbund strategy applies Mass Balance carbon tracking, helping manufacturers achieve measurable Scope 3 emission reductions.

Solvay leads mineral-based, VOC-free foaming technologies

Solvay has carved out a unique niche with Alve-One®, a mineral-based, VOC-free blowing agent positioned as a safer alternative to azodicarbonamide under tightening EU REACH rules. Awarded the Solar Impulse Efficient Solution label in 2025/2026, Alve-One® can reduce CO2 emissions by up to tenfold versus traditional chemical agents. Solvay’s odorless foams are increasingly specified for premium automotive interiors, medical cushioning, and clean-label footwear. In 2026, the company dominates non-toxic building and consumer applications, reinforcing its leadership in hazard-free, recyclable foam components.

Linde accelerates physical CO2 blowing for circular foam production

Linde commands the physical blowing agent segment, supplying CO2 and nitrogen with precision metering systems for zero-GWP foam manufacturing. Its liquid CO2 blowing solutions are seeing renewed demand in 2026 for flexible foams and sustainable packaging. Integrated PLASTNUM technology enables tight control of cell size in XPS insulation, critical for thin-wall urban retrofits. Linde has also expanded green hydrogen and recaptured CO2 supply chains, enabling circular carbon loops for packaging producers. Its decarbonization strategy centers on energy-buffered manufacturing, supporting renewable-powered foam and insulation production worldwide.

United States Blowing Agents Market: Regulatory Enforcement Converting Legacy HFC Demand into HFO-Led Growth

The United States blowing agents industry is being structurally reshaped by regulatory enforcement under the AIM Act and parallel investments in next-generation fluorochemicals. As of January 1, 2025, the EPA’s Technology Transitions rule formally prohibited the manufacture and import of several high-GWP HFCs for foam applications, enforcing a GWP threshold of 150 across most polyurethane and extruded polystyrene uses. This regulatory hard stop has rapidly accelerated substitution toward hydrofluoroolefins and non-fluorinated alternatives, particularly in building insulation, cold storage, and appliance foams. Progress on the phase-down trajectory has been measurable. By September 30, 2025, U.S. HFC consumption was already tracked at 40% below the statutory baseline, reinforcing confidence in long-term compliance with the 85% reduction target set for 2036.

On the supply side, domestic HFO capacity additions are anchoring this transition. In August 2025, Arkema commissioned a new Forane® 1233zd unit in Calvert City, Kentucky, converting a legacy HFC asset into a dedicated HFO production line to serve North American insulation demand. Innovation is extending beyond conventional construction. Honeywell, through its partnership with Mighty Buildings, integrated Solstice Liquid Blowing Agent into 3D-printed housing panels, demonstrating material efficiency gains and measurable thermal performance improvements. Supporting additives capacity is also being reinforced. BASF expanded specialty amines production at its Geismar site to secure local supply chains for polyurethane foam systems, while Chemours received Department of Energy recognition for efficiency upgrades at its Corpus Christi HFO facility.

China Blowing Agents Market: Quota Discipline and Construction Demand Driving Dual-Track Transition

China’s blowing agents market in 2025 is characterized by the simultaneous tightening of HFC quotas and a peak in downstream construction activity. Throughout the year, the Ministry of Ecology and Environment progressively tightened HFC production allocations, forcing appliance and insulation manufacturers to accelerate adoption of cyclopentane and emerging HFO blends. This regulatory discipline coincided with a surge in rigid foam demand, as national construction spending reached an estimated $2.1 trillion in mid-2025, driving large-scale use of polyurethane insulation for energy-efficiency retrofits in urban housing stock.

Multinational and domestic suppliers are aligning capacity accordingly. Evonik doubled long-chain polyamide output at its Shanghai site in November 2025, indirectly supporting demand for high-performance blowing agents used in lightweight EV components and consumer goods foams. At the same time, chemical clusters in Jiangsu prioritized ultra-high-purity blowing agents for protective semiconductor packaging, reflecting the strategic role of electronics manufacturing. To reduce reliance on licensed imports, several Chinese producers initiated proprietary HFO-1234ze trials in mid-2025, signaling a clear policy-backed move toward domestic low-GWP blowing agent self-sufficiency.

India Blowing Agents Market: Export-Oriented HFO Manufacturing and Cooling-Led Diversification

India is emerging as a strategic global supply hub for next-generation blowing agents, leveraging scale, policy incentives, and export-oriented manufacturing. In 2024 and 2025, Honeywell and Navin Fluorine scaled production at their world-scale HFO facility, positioning India as a primary export base for Solstice technology across Asia-Pacific and the Middle East. This export momentum is reinforced by domestic adoption. Under the Production Linked Incentive scheme for white goods, global warming potential has been elevated as a core evaluation metric, directly incentivizing refrigerator and air-conditioner manufacturers to shift toward HFO-based blowing agents.

Beyond traditional foam applications, India is becoming a launchpad for advanced thermal management solutions. In May 2025, Chemours and Navin Fluorine signed a strategic agreement to manufacture Opteon two-phase immersion cooling fluids domestically, with commercial operations targeted for 2026. This positions blowing-agent chemistry at the center of AI data center cooling strategies. Meanwhile, rapid urbanization and appliance penetration supported a marked increase in hydrocarbon-based blowing agent adoption across domestic manufacturing in 2025, strengthening India’s role across both low-GWP fluorinated and natural blowing agent pathways.

European Union Blowing Agents Market: Regulatory Certainty Locking in HFO and Natural Agents

The European Union remains the most regulation-driven market for blowing agents, with the 2025 enforcement of the updated F-Gas Regulation effectively eliminating high-GWP fluorinated gases from most foam and stationary refrigeration uses. With a mandated GWP ceiling of 150, HFOs and natural agents have become the only viable long-term solutions for insulation, appliance, and construction applications. This regulatory certainty is reshaping investment and product strategies across the region.

Circularity is increasingly embedded in supply chains. In late 2024, Honeywell and Chemours expanded their joint reclaim and recycling program in Europe, enabling recovered HFO blends to be reused and supporting circular economy objectives. Downstream manufacturers are moving decisively. Ravago transitioned its Ravatherm XPS insulation production in 2025 to use Solstice GBA exclusively, aligning with zero-ODP and ultra-low-GWP building codes now embedded across EU member states.

Comparative Snapshot: Blowing Agents Industry by Country

Blowing Agents Market County Level Snapshot

|

Country / Region

|

Primary Policy Driver

|

Structural Market Shift

|

|

United States

|

AIM Act and EPA Technology Transitions

|

Rapid conversion from HFCs to domestic HFO capacity

|

|

China

|

HFC quota tightening and construction boom

|

Cyclopentane and emerging domestic HFO pathways

|

|

India

|

PLI incentives and export orientation

|

Global HFO supply hub plus advanced cooling fluids

|

|

European Union

|

F-Gas Regulation enforcement

|

Full lock-in to HFOs and natural blowing agents

|

Blowing Agents Market Report Scope

Blowing Agents Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2 Billion

|

|

Market Size (2034)

|

$3.5 Billion

|

|

Market Growth Rate

|

6.5%

|

|

Segments

|

By Product Type (Hydrofluoroolefins, Hydrocarbons, Hydrofluorocarbons, Hydrochlorofluorocarbons, Inert Gases, Natural and Specialty Agents), By Foam Type (Polyurethane Foam, Polystyrene Foam, Polyolefin Foam, Phenolic Foam), By Application (Building Insulation, Appliances, Automotive and Transportation, Packaging, Electronics), By End Use Industry (Building and Construction, Consumer Appliances, Automotive and Aerospace, Marine and Cold Chain)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Honeywell International, Chemours, Arkema, BASF, Evonik Industries, Solvay, Daikin Industries, Linde, Air Liquide, Huntsman Corporation, Dow, Navin Fluorine International, Sinochem Group, Zhejiang Juhua, Harp International

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Blowing Agents Market Segmentation

By Product Type

- Hydrofluoroolefins

- Hydrocarbons

- Hydrofluorocarbons

- Hydrochlorofluorocarbons

- Inert Gases

- Natural and Specialty Agents

By Foam Type

- Polyurethane Foam

- Polystyrene Foam

- Polyolefin Foam

- Phenolic Foam

By Application

- Building Insulation

- Appliances

- Automotive and Transportation

- Packaging

- Electronics

By End Use Industry

- Building and Construction

- Consumer Appliances

- Automotive and Aerospace

- Marine and Cold Chain

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Blowing Agents Industry

- Honeywell International

- Chemours

- Arkema

- BASF

- Evonik Industries

- Solvay

- Daikin Industries

- Linde

- Air Liquide

- Huntsman Corporation

- Dow

- Navin Fluorine International

- Sinochem Group

- Zhejiang Juhua

- Harp International

*- List not Exhaustive