Brazil Water Treatment Chemicals Market: Growth Forecast and Value Analysis

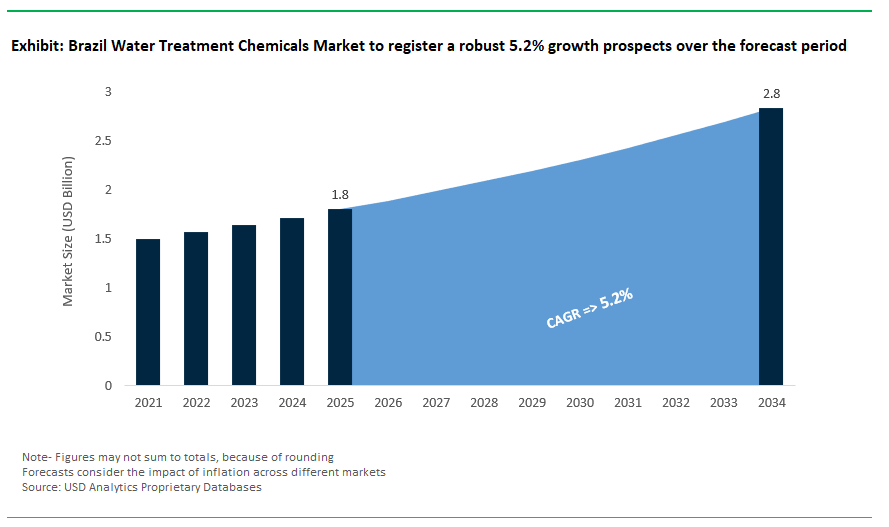

Brazil Water Treatment Chemicals Market Size is estimated at $1.8 Billion in 2025 and is forecast to register an annual growth rate (CAGR) of 5.2% to reach $2.8 Billion by 2034.

Brazil's water treatment chemicals market is undergoing a complex but dynamic evolution, driven by its vast territorial diversity, expanding industrial footprint, and a national regulatory overhaul under the 2020 Sanitation Law (Law No. 14.026/2020). This legislation sets ambitious targets for universal water access and sewage coverage by 2033, alongside promoting private sector investments, thereby triggering long-term shifts in both municipal and industrial water treatment strategies.

In municipal drinking water treatment, polyaluminum chloride (PACl) remains the coagulant of choice, particularly suited to the high turbidity levels (often >200 NTU) found in regions like the Amazon Basin. Its reliable performance achieving <1 NTU effluent turbidity at doses of 15–60 mg/L meets stringent ABNT NBR 15784 standards while remaining cost-competitive at R$2.50–4.00/kg, substantially undercutting imported aluminum salts. In industrial settings, the mining, ethanol, and heavy industries form core demand centers. For instance, iron and gold mines in Minas Gerais combat acid mine drainage (AMD) using lime dosing at pH 10–11, with over 95% metal removal rates. Mercury and arsenic removal, vital to meet IBAMA ecotoxicity guidelines, increasingly relies on sodium sulfide precipitation. Tailings densification driven by risk mitigation mandates post major dam failures employs anionic PAM dosed at 1–3 kg/ton to raise underflow solids concentration by over 70%, as pioneered by Vale. In Brazil’s ethanol-producing heartlands, Fenton’s reagent has gained favor for vinasse treatment, offering robust COD reduction in high-organic-load effluents.

Municipal and industrial wastewater reuse is surging, supported by utilities like SANEPAR which implement struvite recovery (via MgCl₂ and NaOH) to reclaim phosphorus from sludge, yielding over 5,000 tons/year of fertilizer and reinforcing Brazil’s circular economy goals. ZLD systems in textile clusters utilizing electrodialysis and crystallization achieve >95% water recovery when coupled with antiscalants (8–12 ppm), marking a shift to membrane-based reuse platforms.

Meanwhile, emerging contaminant management is rapidly scaling: GAC removes atrazine from agro-runoff at 0.4–0.8 g/kg efficiency, while UV/H₂O₂ AOPs tackle legacy pesticides in compliance with CONAMA 467. PFAS remediation, though nascent, is guided by CETESB protocols that endorse anion exchange resins with 1.0–1.5 mmol/g PFOS capacity, using NaCl/methanol regeneration due to limited thermal destruction infrastructure. The transition to green chemistry is also gaining ground, particularly in Ceará and Bahia, where locally-sourced cashew nut shell liquid (CNSL) inhibitors achieve over 80% corrosion protection at just 25 ppm, and chitosan flocculants (5–20 mg/L) are deployed for aquaculture wastewater under ABNT NBR 16171 norms. These developments underscore Brazil’s commitment to innovation, regulatory alignment, and sustainable growth across its water treatment chemicals ecosystem.

Market Trend: Sustainable Water Treatment Solutions Surge Amidst Stricter Environmental Regulations

Brazil’s water treatment chemicals market is experiencing a transformative shift, catalyzed by converging forces of regulatory enforcement, industrial sustainability mandates, and increasing water scarcity. The 2024 update to CONAMA Resolution 430 has imposed stringent thresholds for BOD, COD, and phosphorus levels, compelling industries to replace traditional phosphates, alum salts, and inorganic coagulants with environmentally safer, bio-based alternatives. Notably, sectors such as food & beverage, mining, and pulp & paper responsible for over 70% of Brazil’s industrial water consumption (ABES 2024) are adopting plant-based formulations and smart chemistry. A flagship example is Braskem’s partnership with Solenis, which piloted sugarcane bagasse-derived flocculants at Suzano’s pulp mills, achieving a 25% reduction in sludge generation and lowering landfill dependency. Local mandates, such as São Paulo’s phosphorus cap of 0.05 mg/L, have spurred demand for membrane-compatible corrosion inhibitors and low-PO4 blends. Nationally, the 2025 National Water Security Plan allocates R$4.2 billion for reuse infrastructure, creating a pull for closed-loop-ready antiscalants and non-residual disinfectants like Kemira’s ASX-3000. Enforcement is also tightening Minas Gerais’ 2025 effluent law introduces steep fines of up to R$10 million for non-compliance in heavy metal discharges, particularly targeting the mining sector. At the corporate level, global players such as Nestlé Brasil are embedding water reuse goals via “Zero Water” plants, relying on ozone-H₂O₂-based advanced oxidation processes (AOPs). Together, these dynamics are reshaping product development, embedding ESG-compliance in procurement metrics, and accelerating the shift to sustainable, smart, and circular water treatment solutions across Brazil’s industrial economy.

Market Opportunity: Amazon Mining Boom Fuels $320M Demand for Heavy Metal Removal Chemistries

The accelerating growth of both industrial and artisanal mining in Brazil’s Amazon Basin is creating a projected $320 million opportunity for specialized heavy metal removal chemistries. As extraction intensifies especially for gold, copper, and niobium water pollution challenges are mounting, particularly in managing methylmercury (MeHg), arsenic, and cyanide-metal complexes, which are poorly addressed by conventional precipitants and flocculants. This has paved the way for advanced, eco-certified chemistries. BASF’s Serafloc™ MG, a chitosan-derived mercury binder certified for Amazon biome use, delivers 98% MeHg removal and meets IBAMA’s strict 2024 mercury limit of 0.001 mg/L. The formalization of artisanal mining via Law 14.066/2024 has carved out a fast-growing R$150 million/year market for decentralized treatment solutions. For instance, Veolia’s MercX™ kits are tailored for remote deployment and integrate portable filtration with high-affinity adsorbents for mercury and lead. Major players like Vale are investing in lanthanum-based phosphate scavengers to comply with Pará State’s nutrient runoff limits, reducing eutrophication potential and cutting sludge-related costs by 40%. Smart chemical dosing is also gaining traction Ecolab’s 3D TRASAR™ arsenic-sensing system, deployed at Minas-Rio, fine-tunes ferric sulfate use in real time, enhancing safety and efficiency. Circular economy innovations are emerging as well: Lhoist’s ReActiv™, made from bauxite residue, is being used by Alcoa’s Juruti mine as a low-cost, high-capacity metal adsorbent. This convergence of regulatory stringency, decentralized deployment needs, and green mining mandates is transforming the Amazon Basin into a high-value frontier for digital, ESG-compliant, and locally optimized water treatment chemistries.

Competitive Landscape: Brazil Water Treatment Chemicals Market

The Brazilian water treatment chemicals market has a mix of competition. It includes multinational leaders, well-established domestic companies, and quick regional players. These companies operate in a tightly regulated, price-sensitive, and varied infrastructure environment shaped by Brazil's unique blend of industrial complexity, local governance, and climate differences. Companies gain an edge through vertical integration, knowledge of regulations, nearby technical services, and the ability to incorporate chemicals into broader treatment systems.

Control of coagulant production is a key advantage in Brazil’s public water treatment sector, which makes up a large part of overall chemical demand. Strategic acquisitions have strengthened this control. Major coagulant producers, with local manufacturing in São Paulo and Bahia, ensure reliable supply, price advantages, and better access to long-term state utility contracts. This is clear in partnerships with companies like SABESP, CEDAE, and COPASA, where contract details on federal procurement platforms show the extent of the supply networks. However, reliance on the public sector and payment stability exposes even the largest companies to budget fluctuations and procurement delays.

Brazil’s industrial water users, especially in oil and gas, energy, mining, and automotive, prefer suppliers who provide integrated solutions that combine chemicals with treatment technologies. Companies that excel in membrane bioreactor systems, efficient desalination, and custom dosing equipment are succeeding in securing contracts in refineries, power plants, and industrial sites. These providers use global technology, such as membrane systems and predictive analytics, alongside strong local execution to secure long-term contracts and service agreements. This approach not only enhances performance but also protects against being treated as a commodity.

Local companies maintain significant market share by closely working with key domestic industries like pulp and paper, sugar and ethanol, food and beverage, and chemical manufacturing. These firms customize formulations to comply with local operational and regulatory requirements, specifically ANVISA approvals for food-contact and potable water chemicals. They also have longstanding supply relationships with major industrial players. Their technical expertise in high-water-using sectors, such as paper and brewing, is hard to replicate. These companies also enjoy quick formulation abilities, direct technical service networks, and easy access to industrial clusters, particularly in the South and Southeast regions.

Multinational chemical suppliers often struggle to penetrate Brazil’s public and mid-tier industrial sectors due to price sensitivity and complex procurement processes. Although global technologies like real-time monitoring platforms and high-performance polymers are welcomed by international food, beverage, and pharmaceutical companies, they are less competitive in lower-margin municipal and industrial sectors. The cost of meeting Brazil's intricate biocide regulations, along with the need for local technical support and flexible logistics, creates high entry barriers for standardized products. As a result, multinationals often focus on high-margin niches or key clients in global value chains.

A large part of the Brazilian market is served by regional specialists and distributor networks that provide chemicals to smaller municipalities, SMEs, and niche applications. These players thrive by offering logistical flexibility, localized support, and access to specialty formulations or hard-to-find imports. Distributors in the Northeast and agribusiness sectors play a significant role in addressing infrastructure and procurement gaps where central contracts are not practical. Their strength lies in understanding regional dynamics, meeting fragmented demand, and maintaining a wide range of inventory for immediate market needs. Additionally, their knowledge of ANVISA and IBAMA regulations for biocides and additives gives certain players a competitive advantage in regulated areas.

Market changes are speeding up related to ESG-linked purchasing. Industrial buyers and state agencies are starting to favor bio-based inhibitors, low-carbon additives, and sustainable formulations. This shift is driving innovation in biodegradable coagulants and green cooling water chemistries, especially among companies serving global manufacturers with sustainability requirements. At the same time, the growth of desalination, particularly in drought-prone regions of Northeastern Brazil and offshore oil platforms, is attracting attention from global solution providers who can combine membrane systems with chemical treatment offerings. Meanwhile, the complex challenges of industrial wastewater in sectors like mining and petrochemicals are increasing demand for specialized defoamers, deposit inhibitors, and specific process polymers.

Brazil Water Treatment Chemicals Market – Segmentation Insights (2025–2034)

Brazil Water Treatment Chemicals Market: Dominance of Coagulants and Rapid Growth in Membrane Cleaners

In the Brazil water treatment chemicals market, coagulants and flocculants command the highest market share at 34.3% in 2025, driven by their extensive application in clarifying highly turbid river water, especially in regions like the Amazon Basin. These chemicals are essential in both municipal and industrial wastewater treatment processes, ensuring the removal of suspended solids and particulates. Their dominance is supported by Brazil’s large-scale investments in public sanitation and water infrastructure modernization. However, the fastest-growing segment is membrane cleaning chemicals, projected to register a CAGR of 7.1% between 2025 and 2034. This surge is fueled by Brazil’s growing reliance on reverse osmosis (RO) and nanofiltration (NF) systems in both desalination and industrial water reuse applications. As industries increasingly adopt advanced membrane technologies for process optimization and regulatory compliance, the demand for specialized cleaning agents is accelerating, especially in sectors like electronics, food processing, and power generation.

.png)

Brazil Water Treatment Chemicals Market: Municipal Sector Leads, Mining Emerges as Fastest-Growing End-User

From an end-user perspective, the municipal sector remains the largest consumer of water treatment chemicals in Brazil, accounting for a market share of 31.8% in 2025. This leadership stems from robust public investments under initiatives such as the Novo Marco do Saneamento, which mandates universal access to clean water and effective wastewater treatment across urban and rural areas. Coagulants, disinfectants, and pH adjusters are widely used in municipal treatment plants to meet stringent potable water and effluent discharge standards. On the other hand, the mining and metallurgy sector is the fastest-growing end-user, expected to grow at a CAGR of 6.7% through 2034. Brazil’s position as a global leader in iron ore and other mineral exports is driving the adoption of water treatment chemicals for tailings management, zero-liquid discharge systems, and recycling-intensive operations. With increasing regulatory oversight and environmental concerns over water-intensive mining activities, the sector is adopting advanced chemical solutions for sustainable resource use and compliance with national water reuse policies.

Brazil Water Treatment Chemicals Report Scope

Brazil Water Treatment Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.8 Billion

|

|

Market Size (2034)

|

$2.8 Billion

|

|

Market Growth Rate

|

5.2%

|

|

Segments

|

By Type of Chemical (Coagulants and Flocculants, Biocides and Disinfectants, pH Adjusters and Softeners, Scale and Corrosion Inhibitors, Defoamers and Antifoaming Agents, Oxygen Scavengers, Membrane Cleaning Chemicals, Other Specialty Chemicals), By Application (Municipal Water and Wastewater Treatment, Industrial Water Treatment), By End-User Industry (Municipal, Oil and Gas, Power Generation, Mining and Metallurgy, Food and Beverage, Chemical and Petrochemical, Pulp and Paper, Pharmaceutical, Automotive, Textile, Electronics Manufacturing and Data Centers, Others), By Form of Chemical (Liquid, Powder/Solid), By Sales Channel/Distribution (Direct Sales, Distributors/Channel Partners

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ecolab Inc. (U.S.), Solenis LLC (U.S.), Kemira Oyj (Finland), SNF Floerger (France), BASF SE (Germany), Kurita Water Industries Ltd. (Japan), Italmatch Chemicals S.p.A. (Italy), Buckman (U.S.), Clariant AG (Switzerland), The Dow Chemical Company (U.S.), Veolia Water Technologies (France), Basequímica (Brazil),

|

Brazil Water Treatment Chemicals Market Segmentation

By Type of Chemical

- Coagulants and Flocculants

- Biocides and Disinfectants

- pH Adjusters and Softeners

- Scale and Corrosion Inhibitors

- Defoamers and Antifoaming Agents

- Oxygen Scavengers

- Membrane Cleaning Chemicals

- Other Specialty Chemicals

By Application

- Municipal Water and Wastewater Treatment

- Drinking Water Treatment

- Municipal Wastewater Treatment

- Industrial Water Treatment

- Cooling Water Treatment

- Boiler Water Treatment

- Process Water Treatment

- Industrial Wastewater Treatment

- Water Desalination

By End-User Industry

- Municipal

- Oil and Gas

- Power Generation

- Mining and Metallurgy

- Food and Beverage

- Chemical and Petrochemical

- Pulp and Paper

- Pharmaceutical

- Automotive

- Textile

- Electronics Manufacturing and Data Centers

- Others

By Form of Chemical

By Sales Channel/Distribution

- Direct Sales

- Distributors/Channel Partners

Top Companies in Brazil Water Treatment Chemicals Market

- Ecolab Inc. (U.S.)

- Solenis LLC (U.S.)

- Kemira Oyj (Finland)

- SNF Floerger (France)

- BASF SE (Germany)

- Kurita Water Industries Ltd. (Japan)

- Italmatch Chemicals S.p.A. (Italy)

- Buckman (U.S.)

- Clariant AG (Switzerland)

- The Dow Chemical Company (U.S.)

- Veolia Water Technologies (France)

- Basequímica (Brazil)

* List Not Exhaustive

Research Coverage

This report by USDAnalytics investigates the evolving dynamics of the Brazil Water Treatment Chemicals Market, offering comprehensive analysis reviews of municipal and industrial segments, competitive frameworks, and sustainability-driven innovations. It highlights breakthroughs in PFAS remediation, membrane cleaning chemistry, and heavy metal removal technologies, along with ESG-compliant product development. This report is an essential resource for senior professionals, strategists, and investors seeking actionable insights into Brazil’s sanitation law-driven reforms, water reuse mandates, and advanced treatment adoption.

Scope Includes:

- Segmentation By Type of Chemical: Coagulants & Flocculants, Biocides & Disinfectants, pH Adjusters & Softeners, Scale & Corrosion Inhibitors, Defoamers & Antifoaming Agents, Oxygen Scavengers, Membrane Cleaning Chemicals, Other Specialty Chemicals

- Segmentation By Application: Municipal Water & Wastewater (Drinking Water, Municipal Wastewater), Industrial Water Treatment (Cooling, Boiler, Process, Industrial Wastewater, Water Desalination)

- Segmentation By End-User: Municipal, Oil & Gas, Power Generation, Mining & Metallurgy, Food & Beverage, Chemical & Petrochemical, Pulp & Paper, Pharmaceutical, Automotive, Textile, Electronics Manufacturing & Data Centers, Others

- Segmentation By Form: Liquid, Powder/Solid

- Segmentation By Distribution Channel: Direct Sales, Distributors/Channel Partners

- Study Period: Historic: 2021–2024; Forecast: 2025–2034

- Companies: Ecolab Inc., Solenis LLC, Kemira Oyj, SNF Floerger, BASF SE, Kurita Water Industries, Italmatch Chemicals, Buckman, Clariant AG, The Dow Chemical Company, Veolia Water Technologies, Basequímica.

Methodology

Our methodology integrates bottom-up market sizing, validated through in-depth interviews with utility operators, industrial buyers, and chemical manufacturers across Brazil. Primary data is reinforced with secondary research drawn from national regulations (CONAMA, IBAMA), industrial water use surveys, and trade statistics. Forecast models employ multi-variable regression using indicators like infrastructure CAPEX, sanitation law compliance, and ESG investment trends. Data triangulation ensures accuracy, while trend mapping captures future shifts toward membrane-based treatment, PFAS remediation, and bio-based chemistries.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements