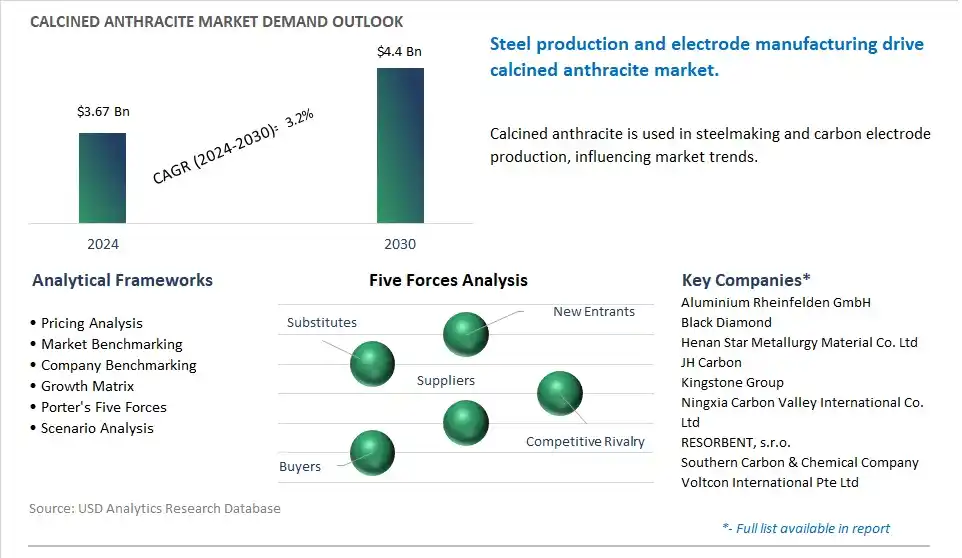

The global Calcined Anthracite Market is poised to register a 3.2% CAGR from $3.67 Billion in 2024 to $4.4 Billion in 2030.

The global Calcined Anthracite Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Calcination (Gas, Electrical), By Application (Pulverized Coal Injection, Basic Oxygen Steel Making (BOS), Electric Arc Furnace, Others).

An Introduction to Global Calcined Anthracite Market in 2024

The calcined anthracite market is witnessing steady growth driven by its diverse applications in the steel, foundry, and carbon products industries. Key trends shaping the future of the industry include the increasing demand for high-quality calcined anthracite as a recarburizing agent in the production of steel and iron alloys, particularly in electric arc furnaces (EAFs) and cupola furnaces. As steelmakers seek to improve product quality, reduce energy consumption, and meet stringent carbon emission standards, there's a growing preference for calcined anthracite due to its low ash and sulfur content, high carbon content, and consistent particle size distribution. Moreover, the expanding use of calcined anthracite in water filtration, cathodic protection, and carbon electrode manufacturing applications is driving market growth. Additionally, advancements in calcination technologies and raw material sourcing are enhancing product quality and process efficiency, while the integration of sustainable practices in mining and processing operations is supporting the market's long-term sustainability and environmental stewardship goals.

Calcined Anthracite Market Competitive Landscape

The market report analyses the leading companies in the industry including Aluminium Rheinfelden GmbH, Black Diamond, Henan Star Metallurgy Material Co. Ltd, JH Carbon, Kingstone Group, Ningxia Carbon Valley International Co. Ltd, RESORBENT, s.r.o., Southern Carbon & Chemical Company, Voltcon International Pte Ltd.

Calcined Anthracite Market Dynamics

Calcined Anthracite Market Trend: Growing Demand for High-Quality Carbon Additives

A prominent trend in the calcined anthracite market is the growing demand for high-quality carbon additives. Calcined anthracite, produced by calcining anthracite coal at high temperatures, is widely used as a carbon additive in the production of steel and other metals. With increasing emphasis on quality control, process optimization, and environmental compliance in metallurgical industries, there is a rising demand for calcined anthracite with consistent chemical composition, low ash content, and high carbon purity. Manufacturers are seeking reliable sources of calcined anthracite that can enhance the performance and efficiency of metal smelting processes, reduce energy consumption, and minimize environmental emissions. As a result, there is a trend towards sourcing premium-grade calcined anthracite from reputable suppliers who can meet stringent quality standards and provide technical support to optimize production processes and achieve desired metallurgical outcomes.

Calcined Anthracite Market Driver: Growth in Steel and Foundry Industries

A primary driver fueling the calcined anthracite market is the growth in steel and foundry industries worldwide. Calcined anthracite is a critical raw material used as a carbon additive in the production of high-quality steel, cast iron, and other metals. As global infrastructure development, urbanization, and industrialization drive demand for construction materials, automotive components, machinery, and consumer goods, there is a corresponding increase in steel and metal production. Calcined anthracite plays a vital role in steelmaking and foundry operations by enhancing the carbon content, heat conductivity, and mechanical properties of metal alloys, thereby improving product quality, consistency, and performance. Moreover, advancements in steelmaking technologies, such as electric arc furnaces and ladle metallurgy processes, are driving the demand for calcined anthracite with specific particle size distribution, sulfur content, and thermal stability to meet the requirements of modern steel production methods. As steel and foundry industries continue to expand globally, the demand for calcined anthracite as a carbon additive is expected to remain strong, providing market opportunities for producers and suppliers.

Calcined Anthracite Market Opportunity: Expansion into Alternative Applications and Emerging Markets

An opportunity within the calcined anthracite market lies in the expansion into alternative applications and emerging markets beyond traditional steel and foundry industries. While steelmaking and foundry applications represent the primary market for calcined anthracite, there is potential to explore new opportunities in sectors such as carbon products, refractories, and water treatment. Calcined anthracite can be utilized as a carbon source in the production of carbon electrodes, cathodes, and carbon blocks for applications in electric arc furnaces, aluminum smelting, and specialty graphite manufacturing. Additionally, calcined anthracite can be used as a carbon filter media in water treatment processes to remove contaminants and improve water quality in municipal, industrial, and environmental remediation applications. By diversifying product offerings and targeting emerging markets with specific technical requirements and performance criteria, calcined anthracite producers can expand their customer base, mitigate market risks, and capitalize on new growth opportunities in the global carbon additives market.

Calcined Anthracite Market Share Analysis: Gas Calcination segment generated the highest revenue in the industry

The Gas Calcination segment is the largest segment in the Calcined Anthracite Market for diverse compelling reasons. Gas calcination involves heating anthracite coal in a controlled atmosphere, using natural gas or other hydrocarbon gases, to remove impurities and volatile matter and produce calcined anthracite with high carbon content and low ash content. Gas calcination offers diverse advantages over electrical calcination, including lower operating costs, faster heating rates, and better control over temperature and atmosphere conditions. Additionally, gas calcination facilities are more widely available and established in regions with abundant natural gas resources, leading to greater production capacity and supply chain efficiency. In addition, gas-calcined anthracite is preferred in various industrial applications, including steel manufacturing, foundry operations, and electrode production, due to its superior quality, consistency, and performance characteristics. As a result of these factors, the Gas Calcination segment dominates the Calcined Anthracite Market as the largest segment.

Calcined Anthracite Market Share Analysis: Pulverized Coal Injection Segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The Pulverized Coal Injection (PCI) segment is the fastest-growing category in the Calcined Anthracite Market for diverse compelling reasons. The PCI is increasingly being adopted as a cost-effective and environmentally friendly method for reducing coke consumption and greenhouse gas emissions in blast furnaces used for steelmaking. Calcined anthracite, when pulverized into fine particles, serves as a substitute for metallurgical coke in the injection process, providing carbon and energy for the reduction of iron ore into molten iron. This process not only reduces the reliance on expensive coke but also improves furnace efficiency, productivity, and Over the forecast period steelmaking economics. Additionally, calcined anthracite offers advantages such as higher carbon content, lower sulfur content, and better thermal stability compared to other coal-based injection materials, making it well-suited for PCI applications. In addition, the global steel industry's continuous efforts to enhance energy efficiency, reduce emissions, and optimize raw material usage drive the growing demand for calcined anthracite in PCI systems. As steelmakers seek to improve their competitiveness and sustainability, the Pulverized Coal Injection segment experiences rapid growth in the Calcined Anthracite Market.

Calcined Anthracite Market Report Segmentation

By Calcination

Gas

Electrical

By Application

Pulverized Coal Injection

Basic Oxygen Steel Making (BOS)

Electric Arc Furnace

Others

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Calcined Anthracite Companies Profiled in the Market Study

Aluminium Rheinfelden GmbH

Black Diamond

Henan Star Metallurgy Material Co. Ltd

JH Carbon

Kingstone Group

Ningxia Carbon Valley International Co. Ltd

RESORBENT, s.r.o.

Southern Carbon & Chemical Company

Voltcon International Pte Ltd

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Calcined Anthracite Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Calcined Anthracite Market Size Outlook, $ Million, 2021 to 2030

3.2 Calcined Anthracite Market Outlook by Type, $ Million, 2021 to 2030

3.3 Calcined Anthracite Market Outlook by Product, $ Million, 2021 to 2030

3.4 Calcined Anthracite Market Outlook by Application, $ Million, 2021 to 2030

3.5 Calcined Anthracite Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Calcined Anthracite Industry

4.2 Key Market Trends in Calcined Anthracite Industry

4.3 Potential Opportunities in Calcined Anthracite Industry

4.4 Key Challenges in Calcined Anthracite Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Calcined Anthracite Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Calcined Anthracite Market Outlook by Segments

7.1 Calcined Anthracite Market Outlook by Segments, $ Million, 2021- 2030

By Calcination

Gas

Electrical

By Application

Pulverized Coal Injection

Basic Oxygen Steel Making (BOS)

Electric Arc Furnace

Others

8 North America Calcined Anthracite Market Analysis and Outlook To 2030

8.1 Introduction to North America Calcined Anthracite Markets in 2024

8.2 North America Calcined Anthracite Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Calcined Anthracite Market size Outlook by Segments, 2021-2030

By Calcination

Gas

Electrical

By Application

Pulverized Coal Injection

Basic Oxygen Steel Making (BOS)

Electric Arc Furnace

Others

9 Europe Calcined Anthracite Market Analysis and Outlook To 2030

9.1 Introduction to Europe Calcined Anthracite Markets in 2024

9.2 Europe Calcined Anthracite Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Calcined Anthracite Market Size Outlook by Segments, 2021-2030

By Calcination

Gas

Electrical

By Application

Pulverized Coal Injection

Basic Oxygen Steel Making (BOS)

Electric Arc Furnace

Others

10 Asia Pacific Calcined Anthracite Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Calcined Anthracite Markets in 2024

10.2 Asia Pacific Calcined Anthracite Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Calcined Anthracite Market size Outlook by Segments, 2021-2030

By Calcination

Gas

Electrical

By Application

Pulverized Coal Injection

Basic Oxygen Steel Making (BOS)

Electric Arc Furnace

Others

11 South America Calcined Anthracite Market Analysis and Outlook To 2030

11.1 Introduction to South America Calcined Anthracite Markets in 2024

11.2 South America Calcined Anthracite Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Calcined Anthracite Market size Outlook by Segments, 2021-2030

By Calcination

Gas

Electrical

By Application

Pulverized Coal Injection

Basic Oxygen Steel Making (BOS)

Electric Arc Furnace

Others

12 Middle East and Africa Calcined Anthracite Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Calcined Anthracite Markets in 2024

12.2 Middle East and Africa Calcined Anthracite Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Calcined Anthracite Market size Outlook by Segments, 2021-2030

By Calcination

Gas

Electrical

By Application

Pulverized Coal Injection

Basic Oxygen Steel Making (BOS)

Electric Arc Furnace

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Aluminium Rheinfelden GmbH

Black Diamond

Henan Star Metallurgy Material Co. Ltd

JH Carbon

Kingstone Group

Ningxia Carbon Valley International Co. Ltd

RESORBENT, s.r.o.

Southern Carbon & Chemical Company

Voltcon International Pte Ltd

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Calcination

Gas

Electrical

By Application

Pulverized Coal Injection

Basic Oxygen Steel Making (BOS)

Electric Arc Furnace

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)