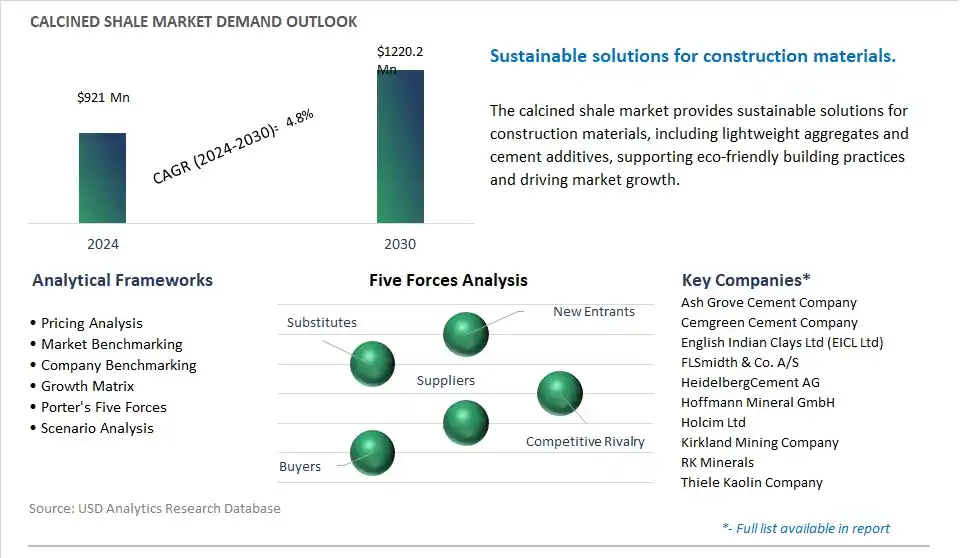

The global Calcined Shale Market is poised to register a 4.8% CAGR from $921 Million in 2024 to $1220.2 Million in 2030.

The global Calcined Shale Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Application (Ceramics, Fillers, Supplementary Cementitious Material (SCM), Desiccant, Others), By End-User (Paint & Coatings, Agrochemicals, Cement & Materials, Others).

An Introduction to Global Calcined Shale Market in 2024

The market for calcined shale is transforming construction by offering sustainable building materials that provide strength, durability, and environmental benefits. Key trends shaping the future of this industry include advancements in shale calcination processes, such as high-temperature treatment and mineralogical optimization, which enhance the pozzolanic properties and reactivity of shale materials for use in cementitious applications. Additionally, developments in shale-based construction products, including lightweight aggregates, supplementary cementitious materials (SCMs), and geopolymer binders, offer alternatives to traditional construction materials such as sand, gravel, and Portland cement, reducing carbon emissions and natural resource depletion in construction projects. Moreover, the adoption of shale-based construction solutions contributes to the circular economy by utilizing waste materials from mining and industrial processes, reducing landfill waste and promoting resource efficiency. As builders, architects, and developers increasingly prioritize sustainability, resilience, and environmental stewardship in construction projects, the demand for innovative calcined shale products is expected to grow, driving further research, development, and market adoption in this emerging segment of the construction materials industry.

Calcined Shale Market Competitive Landscape

The market report analyses the leading companies in the industry including Ash Grove Cement Company, Cemgreen Cement Company, English Indian Clays Ltd (EICL Ltd), FLSmidth & Co. A/S, HeidelbergCement AG, Hoffmann Mineral GmbH, Holcim Ltd, Kirkland Mining Company, RK Minerals, Thiele Kaolin Company.

Calcined Shale Market Dynamics

Calcined Shale Market Trend: Increased Demand for Sustainable Construction Materials

A prominent trend in the calcined shale market is the increased demand for sustainable construction materials. Calcined shale, known for its lightweight and high-strength properties, is gaining popularity as an eco-friendly alternative to traditional construction materials such as cement and concrete. With growing awareness of environmental issues and the need for sustainable building practices, architects, engineers, and developers are turning to calcined shale-based products for various applications including lightweight aggregates, structural fill, and soil stabilization. This is driven by the need to reduce carbon footprint, conserve natural resources, and achieve green building certifications, leading to market growth and expansion of calcined shale products.

Calcined Shale Market Driver: Infrastructure Development Projects

A key driver behind the demand for calcined shale is the ongoing infrastructure development projects worldwide. As governments and private sectors invest in transportation, utilities, and public infrastructure projects to support economic growth and urbanization, there is a significant need for construction materials that offer cost-effectiveness, durability, and sustainability. Calcined shale, with its abundance, low cost, and favorable engineering properties, is well-suited for various infrastructure applications such as road construction, embankments, retaining walls, and erosion control. The demand for calcined shale is further fueled by its ability to improve soil stability, reduce construction time, and enhance project efficiency, driving market growth and investment in shale mining and processing facilities.

Calcined Shale Market Opportunity: Innovation in Value-Added Products

An emerging opportunity in the calcined shale market lies in the innovation of value-added products and applications. While calcined shale is primarily used in construction and civil engineering projects, there is potential to explore new markets and applications for shale-based products. Manufacturers aim to capitalize on this opportunity by investing in research and development of innovative solutions such as lightweight concrete additives, geopolymer materials, and soil remediation products that leverage the unique properties of calcined shale. Additionally, there is an opportunity to explore niche markets such as horticulture, landscaping, and industrial applications where shale-based products can offer benefits such as moisture retention, soil stabilization, and thermal insulation. By diversifying product offerings and exploring new applications, suppliers can expand their market reach, mitigate risks, and capture additional revenue streams in the evolving landscape of sustainable construction materials. Embracing innovation in value-added products can drive market differentiation and competitiveness, positioning calcined shale as a versatile and sustainable solution for diverse industries and applications.

Calcined Shale Market Ecosystem

The Calcined Shale market encompasses a well-established value chain involving distinct stages from raw material acquisition to end-use applications across various sectors. Initially, shale extraction is undertaken by mining companies or independent quarry operators, followed by processing and crushing to prepare the shale for further treatment, which is managed in-house or by dedicated crushing and screening companies.

Calcination, the pivotal stage where the shale undergoes heating to enhance its properties, is typically conducted by calcined shale manufacturers or integrated mining companies, with established building material companies including LafargeHolcim having in-house capabilities. Further processing, including grinding and classification, is handled by calcined shale manufacturers to achieve desired particle sizes. Distribution channels involve building material distributors including Builders FirstSource and direct sales to industrial users.

End-use applications span construction, cement manufacturing, agriculture, paints and coatings, and other industries, highlighting the versatility of calcined shale. Key considerations include regional variations in company involvement, adherence to mining regulations, and the influence of shale quality on the final product's properties and applications.

Calcined Shale Market Share Analysis: Supplementary Cementitious Material (SCM) held the dominant revenue share in 2024

In the Calcined Shale Market, the largest segment is the Supplementary Cementitious Material (SCM) application. This dominance stems from the widespread use of calcined shale as a pozzolanic material in the production of concrete and cementitious products. Calcined shale, when finely ground and mixed with Portland cement, exhibits pozzolanic properties similar to fly ash and silica fume, enhancing the strength, durability, and sustainability of concrete. As an SCM, calcined shale improves the workability of concrete mixes, reduces heat of hydration, and mitigates alkali-silica reaction, contributing to the long-term performance and resilience of concrete structures. The use of calcined shale as an SCM also helps reduce the carbon footprint of concrete production by decreasing the reliance on Portland cement, which is associated with significant CO2 emissions. Additionally, the increasing emphasis on sustainable construction practices and green building initiatives worldwide drives the demand for alternative cementitious materials like calcined shale. In addition, ongoing research and development efforts focused on optimizing the properties and performance of calcined shale-based cementitious blends further support its dominance in the market. Overall, the Supplementary Cementitious Material (SCM) application segment holds a significant share in the Calcined Shale Market due to its pivotal role in enhancing the quality and sustainability of concrete construction.

Calcined Shale Market Share Analysis: Cement and Materials is the fastest growing market segment over the forecast period to 2030

In the Calcined Shale Market, the fastest-growing segment is the Cement and Materials end-user category. This growth can be attributed to diverse factors contributing to the increasing demand for calcined shale in cement and construction materials applications. Calcined shale is extensively utilized as a supplementary cementitious material (SCM) in the production of cement, concrete, and related materials. As environmental concerns and regulations drive the need for sustainable construction practices, the use of alternative cementitious materials like calcined shale becomes more prevalent. Calcined shale offers diverse advantages in cement and concrete formulations, including improved compressive strength, reduced permeability, and enhanced durability of concrete structures. Additionally, calcined shale helps to mitigate the environmental impact of cement production by reducing CO2 emissions and energy consumption. In addition, the growing construction activities, infrastructure development projects, and urbanization worldwide further propel the demand for calcined shale in cement and construction materials applications. As a result, the Cement and Materials segment experiences rapid growth in the Calcined Shale Market, driven by its crucial role in enhancing the performance and sustainability of cementitious products.

Calcined Shale Market Report Scope-

By Application

Ceramics

Fillers

Supplementary Cementitious Material (SCM)

Desiccant

Others

By End-User

Paint & Coatings

Agrochemicals

Cement & Materials

Others

Calcined Shale Market Companies Profiled

Ash Grove Cement Company

Cemgreen Cement Company

English Indian Clays Ltd (EICL Ltd)

FLSmidth & Co. A/S

HeidelbergCement AG

Hoffmann Mineral GmbH

Holcim Ltd

Kirkland Mining Company

RK Minerals

Thiele Kaolin Company

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Calcined Shale Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Calcined Shale Market Size Outlook, $ Million, 2021 to 2030

3.2 Calcined Shale Market Outlook by Type, $ Million, 2021 to 2030

3.3 Calcined Shale Market Outlook by Product, $ Million, 2021 to 2030

3.4 Calcined Shale Market Outlook by Application, $ Million, 2021 to 2030

3.5 Calcined Shale Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Calcined Shale Industry

4.2 Key Market Trends in Calcined Shale Industry

4.3 Potential Opportunities in Calcined Shale Industry

4.4 Key Challenges in Calcined Shale Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Calcined Shale Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Calcined Shale Market Outlook by Segments

7.1 Calcined Shale Market Outlook by Segments, $ Million, 2021- 2030

By Application

Ceramics

Fillers

Supplementary Cementitious Material (SCM)

Desiccant

Others

By End-User

Paint & Coatings

Agrochemicals

Cement & Materials

Others

8 North America Calcined Shale Market Analysis and Outlook To 2030

8.1 Introduction to North America Calcined Shale Markets in 2024

8.2 North America Calcined Shale Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Calcined Shale Market size Outlook by Segments, 2021-2030

By Application

Ceramics

Fillers

Supplementary Cementitious Material (SCM)

Desiccant

Others

By End-User

Paint & Coatings

Agrochemicals

Cement & Materials

Others

9 Europe Calcined Shale Market Analysis and Outlook To 2030

9.1 Introduction to Europe Calcined Shale Markets in 2024

9.2 Europe Calcined Shale Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Calcined Shale Market Size Outlook by Segments, 2021-2030

By Application

Ceramics

Fillers

Supplementary Cementitious Material (SCM)

Desiccant

Others

By End-User

Paint & Coatings

Agrochemicals

Cement & Materials

Others

10 Asia Pacific Calcined Shale Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Calcined Shale Markets in 2024

10.2 Asia Pacific Calcined Shale Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Calcined Shale Market size Outlook by Segments, 2021-2030

By Application

Ceramics

Fillers

Supplementary Cementitious Material (SCM)

Desiccant

Others

By End-User

Paint & Coatings

Agrochemicals

Cement & Materials

Others

11 South America Calcined Shale Market Analysis and Outlook To 2030

11.1 Introduction to South America Calcined Shale Markets in 2024

11.2 South America Calcined Shale Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Calcined Shale Market size Outlook by Segments, 2021-2030

By Application

Ceramics

Fillers

Supplementary Cementitious Material (SCM)

Desiccant

Others

By End-User

Paint & Coatings

Agrochemicals

Cement & Materials

Others

12 Middle East and Africa Calcined Shale Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Calcined Shale Markets in 2024

12.2 Middle East and Africa Calcined Shale Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Calcined Shale Market size Outlook by Segments, 2021-2030

By Application

Ceramics

Fillers

Supplementary Cementitious Material (SCM)

Desiccant

Others

By End-User

Paint & Coatings

Agrochemicals

Cement & Materials

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Ash Grove Cement Company

Cemgreen Cement Company

English Indian Clays Ltd (EICL Ltd)

FLSmidth & Co. A/S

HeidelbergCement AG

Hoffmann Mineral GmbH

Holcim Ltd

Kirkland Mining Company

RK Minerals

Thiele Kaolin Company

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Application

Ceramics

Fillers

Supplementary Cementitious Material (SCM)

Desiccant

Others

By End-User

Paint & Coatings

Agrochemicals

Cement & Materials

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)