Canada’s water treatment chemicals market is shaped by its vast geography, extreme climatic variations, and stringent environmental standards, making it one of the most technologically diverse and regulation-sensitive landscapes globally. In the municipal sector, treatment strategies are highly customized to address source-specific water quality challenges. For example, polyaluminum chloride (PACl) remains the coagulant of choice in many treatment plants, especially for algae-laden waters from the Great Lakes. It is typically dosed at 10–40 mg/L to consistently achieve effluent turbidity targets of <0.3 NTU, in line with Health Canada’s Guidelines for Canadian Drinking Water Quality (GDWQ). The GDWQ emphasizes that water leaving conventional or direct filtration systems should meet this turbidity threshold to ensure effective pathogen removal. Compared to alum, PACl generates 20–30% less sludge, thereby reducing downstream handling and disposal costs a benefit aligned with the sustainability goals of provincial regulators such as Ontario’s Ministry of Environment, Conservation and Parks (MOECP).

However, the country’s long, cold winters impose operational constraints. Water temperatures below 4°C increase viscosity and hinder coagulation kinetics, requiring 15–25% higher chemical dosages and often the addition of cationic polymers for performance optimization. Findings from the American Water Works Association (AWWA) and industry case studies corroborate these adaptations in cold-climate operations. In terms of disinfection, chloramine residuals are commonly used in cities like Toronto to control biofilm growth in vast distribution networks offering long-lasting protection compared to free chlorine.

In the industrial sector, Canada’s oil sands and mining industries are major consumers of treatment chemicals. Tailings and acid rock drainage (ARD) drive demand for robust chemical solutions. In oil sands tailings management, gypsum-based coagulation at 300–800 kg/1,000 m³ is widely used to consolidate over 70% of suspended solids within 90 days, complying with Alberta Energy Regulator (AER) Directive 085, which governs fluid tailings reduction in oil sands mining.

Canada’s wastewater and reuse infrastructure is evolving rapidly, particularly with a focus on nutrient recovery and decentralized treatment a necessity in Arctic and Indigenous communities. Ottawa’s Robert O. Pickard Environmental Centre exemplifies this trend with full-scale struvite recovery, using magnesium chloride and sodium hydroxide at pH 8.8 to capture over 90% of phosphorus, yielding more than 8,000 tons of recoverable fertilizer annually. Meanwhile, membrane-based systems are increasingly optimized through precision biofouling control, highlighting the market’s shift toward operational efficiency. For remote regions such as Nunavut, electrochemical chlorine generation using seawater has replaced the need for bulky chemical transport, showcasing the adoption of autonomous, on-site chemical systems in hard-to-reach areas.

The country is also a leader in green chemistry adoption. Innovations such as lignin-based flocculants developed by FPInnovations have shown excellent performance at 5–20 mg/L dosages, matching synthetic PAM efficiency while achieving over 90% biodegradability under OECD 301F protocols. This transition supports Canada’s broader push toward environmentally benign alternatives in both municipal and industrial settings.

In permafrost zones, challenges such as elevated iron and manganese levels in thawing groundwater are increasingly common. Utilities address this with pre-oxidation and catalytic filtration techniques. Additionally, ice-blocked intake systems have driven the development of eco-friendly deicers, such as beet juice-derived glycols, which present lower aquatic toxicity than traditional options. Indigenous water security programs are trialing mobile UV/ceramic filtration units, capable of handling turbidities >300 NTU without chemical input. These units aim to improve water access in First Nations communities by offering portable, chemical-free solutions suited to remote geographies.

Looking ahead, Canada continues to foster unique technological frontiers. Phage-based biocides, pioneered by institutions like McGill University, offer a precision approach to Legionella control at concentrations as low as 0.1 ppm without residual chemical accumulation. Meanwhile, Natural Resources Canada (NRCan) is exploring the use of carbon capture byproducts, such as mineralized CO₂, for potential integration into water treatment workflows further aligning the sector with national decarbonization goals.

Canada’s water treatment chemicals market is undergoing a transformation driven by evolving environmental regulations and increased demand from critical resource sectors. The federal government’s ongoing actions to address per- and polyfluoroalkyl substances (PFAS) have intensified in 2024, particularly following the release of Health Canada’s draft screening assessments under the Canadian Environmental Protection Act (CEPA). These assessments identified several PFAS compounds, including PFOS and PFOA, as potentially harmful to human health and the environment, prompting a shift toward restrictions on their use and discharge. While a full federal ban has yet to be finalized, provinces such as Nova Scotia have introduced their own highly stringent standards, with maximum acceptable concentrations for PFAS in drinking water as low as 0.0002 mg/L, surpassing most other jurisdictions in North America.

This regulatory tightening has accelerated the adoption of alternative technologies such as advanced oxidation processes (AOPs), bio-based coagulants, and fluorine-free surfactants in municipal and industrial treatment systems. Municipal utilities are increasingly considering alternatives like plant-derived flocculants to meet stringent discharge limits without compromising performance. Companies such as Solenis and Ecolab have responded by marketing certified PFAS-free solutions for both conventional and advanced water treatment applications.

Simultaneously, Canada’s mining sector especially lithium, nickel, and rare earth operations identified in the federal Critical Minerals Strategy (2023–2025) has created significant demand for chemical solutions capable of managing high-total-dissolved-solids (TDS) water, heavy metals, and acidic drainage. Treatment of process water and tailings ponds requires brine-resistant antiscalants, selective metal precipitants, and corrosion inhibitors engineered for aggressive water chemistries. These needs are particularly evident in new extraction zones in Québec and Northern Ontario, where elevated concentrations of manganese, sulfates, and fluoride challenge conventional chemistry.

In addition, provincial policies such as British Columbia’s “Polluter Pays” principles, reinforced through environmental liability regulations, have made companies financially responsible for PFAS and other legacy contaminants. This has led to increased adoption of digital compliance platforms and automated chemical dosing systems that support real-time monitoring and documentation especially in Ontario, where amendments to the Water Opportunities Act are driving utilities toward smart water infrastructure.

Growing pressure from industrial buyers is also shaping the chemical supply chain. A 2024 industry survey by the Canadian Manufacturers & Exporters (CME) indicated that more than 60% of industrial buyers now require verifiable PFAS-free certification from their suppliers, indicating a long-term shift in procurement standards. As a result, water treatment chemical providers must not only innovate for performance but also meet rising transparency and traceability demands.

Canada’s oil sands industry centered in Alberta remains a highly specialized application area for water treatment chemicals, with unique operational challenges and regulatory pressures fostering a premium chemicals segment. Thermal in-situ recovery methods such as steam-assisted gravity drainage (SAGD) require vast quantities of water, most of which is sourced, treated, and recycled within closed-loop systems. Increasing environmental scrutiny and upcoming federal and provincial water reuse targets have forced operators to increase water recycling rates while controlling scaling, corrosion, and fouling in high-temperature environments.

The recently proposed Oil Sands Emissions Limit Act (2025) is expected to formalize a 90% water reuse mandate for SAGD operations, aligning environmental goals with circular economy principles. This creates a growing opportunity for thermally stable antiscalants and corrosion inhibitors, particularly those capable of operating at temperatures exceeding 250°C, where conventional polymers like polyacrylates degrade. In these harsh conditions, inhibitors must manage scaling caused by silica, bicarbonates, and residual hydrocarbons substances that precipitate readily under thermal stress.

Chemical suppliers are responding with formulations engineered for thermal endurance, such as Veolia’s Hydrex™ 9912 series and specialty phosphonates from Kurita and Solenis tailored for high-silica environments. These solutions are validated by performance trials at oil sands facilities such as Suncor’s and CNRL’s operational sites. Furthermore, nanotechnology-based dispersants, bio-derived additives, and real-time chemical dosing systems are being piloted to reduce chemical overuse and improve heat exchanger efficiency.

Technologies integrating sensor-based monitoring and predictive AI like Kemira’s ChemBrain™ platform are being tested to optimize dosing using input parameters like TOC, pH, and conductivity. Indigenous partnerships have also become a differentiator in chemical procurement. For example, Nalco Water has collaborated with local First Nations on sourcing plant-based components for dispersants, aligning with ESG expectations and enhancing stakeholder trust.

Canada’s water treatment chemicals market is complex and varies greatly by region. This situation arises from its vast geography, bilingual governance, scattered population centers, and the combined demand from both industrial and municipal sectors. The market includes global multinationals, large Canadian manufacturers, regional specialists, and Indigenous-owned companies. Each player uses its own strengths to meet the growing and regulated needs for water treatment across the country.

Alberta’s oil sands sector is a key driver of demand for water treatment chemicals, especially for Steam-Assisted Gravity Drainage (SAGD) operations. Leading suppliers here have created specialized high-performance chemical formulations, particularly scale inhibitors, biocides, and coagulants, which can withstand the high temperatures and hardness typically found in process water during oil sands extraction. This specialized market needs close technical collaboration with companies like Suncor and Imperial Oil, and it faces pressures from fluctuating oil prices and rising costs related to emissions. Meanwhile, stable demand continues in power generation and pulp and paper sectors across Ontario, Quebec, and the Maritimes. Large utilities and mills depend on embedded chemical expertise, bundled service contracts, and strong logistics coordination.

Municipal water treatment in Canada is highly localized and increasingly focused on performance, especially in major cities like Toronto, Vancouver, and Montréal. Suppliers with strong positions in coagulant and bulk disinfection chemical supplies (like PAC, ferric chloride, and sodium hypochlorite) benefit from stable contracts. This is especially true if they operate near local manufacturing and maintain cost-effective transport networks. For Ontario and Quebec, being close to the Great Lakes and linked with U.S. plants in states like Michigan and Ohio boosts the resilience and cost-effectiveness of their supply chains. However, pricing remains tough due to rising energy costs and increasing demands for bio-based, low-residue options as part of sludge reduction and PFAS removal efforts.

The market is moving toward combined water solutions that integrate chemicals with advanced treatment systems. Suppliers offering membrane bioreactors (MBR), nutrient recovery technologies, or smart monitoring tools (like TRASAR and ZeeLung®) are gaining a competitive edge, especially in larger industrial sites and upgrades to municipal treatment plants. Bundled services that connect chemical performance to real-time monitoring and compliance help utilities and private operators meet federal wastewater discharge rules and greenhouse gas reduction goals. These all-in-one solutions also serve as a strategic way to avoid commoditization and stand out in high-stakes procurement situations.

Canada’s large landmass and many remote communities, particularly in the North and Indigenous territories, make efficient distribution and logistics highly important. National distributors, along with those experienced in serving remote mines, resorts, and Indigenous infrastructure, play a crucial role in closing access gaps. Some have integrated into Indigenous procurement networks, helping the federal government eliminate long-term boil water advisories through ISC-funded plant upgrades. In these areas, flexibility in delivery, chemical packaging, and small-batch customization becomes essential, especially for serving decentralized utilities and unique water systems.

Beyond simple supply, Canadian niche firms are growing by tackling unique wastewater challenges. Issues like landfill leachate treatment, scaling in food processing effluent, or dealing with dissolved solids in desalination for remote communities often require rapid, customized chemical solutions that larger companies may not provide. Agile formulators with blending capabilities and knowledge of regulations (especially regarding imported substances or biocides) have developed loyal customer bases by addressing complex treatment problems quicker than standard suppliers. Their emergence reflects a broader movement toward decentralized and application-specific procurement in Canada's water-intensive industries.

Environmental regulations and sustainability mandates are changing competitive priorities in Canada. Stricter federal guidelines about PFAS, microplastics, and waterborne pathogens have compelled utilities and industries to rethink legacy chemicals and seek bio-based or low-carbon alternatives. At the same time, carbon taxes and rising energy costs are affecting the economics of chlor-alkali and other energy-heavy production methods, squeezing profit margins and pushing for supply chain changes. In response, top suppliers are testing green chemistry innovations, especially in coagulants and corrosion inhibitors, while creating ESG-focused chemical programs for municipalities and companies with net-zero goals.

In 2025, coagulants and flocculants are expected to lead the Canada water treatment chemicals market with a 29.8% market share, driven by their essential role in clarifying water and removing suspended solids in both municipal and industrial treatment facilities. Their dominance is attributed to widespread adoption in municipal wastewater treatment, where efficient removal of turbidity and particulate matter is critical to meet Canada’s stringent water quality regulations. Additionally, these chemicals are vital for sludge conditioning and improving solid-liquid separation efficiency in industrial effluent treatment processes. However, the most dynamic growth is forecasted in the membrane cleaning chemicals segment, which is projected to grow at a CAGR of 6.6% from 2025 to 2034. This rapid expansion reflects the increasing deployment of reverse osmosis (RO) and nanofiltration (NF) systems in Canada's industrial zones and municipal desalination plants. The need for maintaining membrane efficiency and minimizing fouling in these high-pressure systems is driving demand for specialized cleaning agents. Industries such as food and beverage, electronics, and pharmaceuticals are further amplifying this demand as they shift toward high-purity water processing systems.

.png)

The municipal sector holds the largest share of the Canada water treatment chemicals market, accounting for approximately 43.4% of total demand in 2025. This dominance is underpinned by government-backed investments in safe drinking water infrastructure, upgrades to wastewater treatment facilities, and regulatory mandates to reduce environmental discharge impacts. Canada's expansive municipal treatment networks, especially in densely populated provinces such as Ontario and Quebec, rely on chemicals such as coagulants, disinfectants, and pH adjusters to maintain consistent water quality and disinfection standards. On the growth front, industrial water treatment applications are expected to record the highest CAGR at 5.9% over the forecast period, led by water-intensive industries including oil & gas, mining, pulp & paper, and power generation. These sectors are increasingly focused on minimizing freshwater intake and improving wastewater reuse, spurring demand for corrosion inhibitors, biocides, antiscalants, and membrane treatment solutions. As environmental compliance tightens and sustainability becomes a competitive imperative, the industrial segment is poised to drive the next wave of chemical innovation and volume growth in Canada’s water treatment market.

|

Parameter |

Details |

|

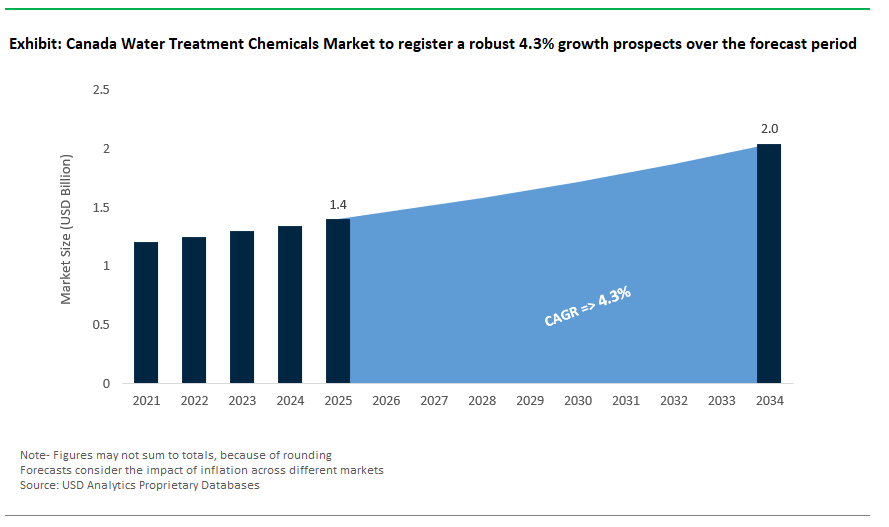

Market Size (2025) |

$1.4 Billion |

|

Market Size (2034) |

$2 Billion |

|

Market Growth Rate |

4.3% |

|

Segments |

By Type of Chemical (Coagulants and Flocculants, Corrosion and Scale Inhibitors, Biocides and Disinfectants, pH Adjusters and Softeners, Oxygen Scavengers, Defoamers and Antifoaming Agents, Membrane Cleaning Chemicals, Other Specialty Chemicals), By Application (Municipal Water Treatment, Industrial Water Treatment, Commercial Water Treatment), By End-User Industry (Municipal, Industrial), By Form of Chemical (Liquid, Powder/Solid |

|

Study Period |

2019- 2024 and 2025-2034 |

|

Units |

Revenue (USD) |

|

Qualitative Analysis |

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking |

|

Companies |

Ecolab Inc. (U.S.), Solenis LLC (U.S.), Kemira Oyj (Finland), SNF Floerger (France), BASF SE (Germany), Veolia Water Technologies (France), ChemTreat, Inc. (U.S.), Brenntag Canada Inc. (Germany), Univar Solutions (U.S.), Buckman (U.S.), Guardian Chemicals (Canada), ClearTech (Canada), Accepta (UK), Canadian Crystalline (India), |

* List Not Exhaustive

This report by USDAnalytics investigates the dynamic landscape of the Canada Water Treatment Chemicals Market, offering comprehensive analysis reviews of market trends, technological breakthroughs, and competitive strategies across municipal and industrial segments. It highlights key drivers such as stricter PFAS regulations, mining sector growth, and the rise of integrated treatment solutions. This report is an essential resource for industry professionals seeking actionable insights on green chemistry adoption, ESG-driven procurement, and digital dosing innovations shaping Canada’s water treatment ecosystem.

Scope Includes:

Our methodology combines bottom-up and top-down market modeling, supported by primary interviews with utilities, chemical suppliers, and industrial operators, and secondary data from government regulations (Health Canada, CEPA), industry reports, and trade publications. Advanced forecasting models incorporate variables such as infrastructure CAPEX, regulatory compliance costs, and technological adoption trends. Data triangulation ensures accuracy, while ESG and digital transformation metrics are integrated to reflect emerging procurement priorities.

1. Executive Summary

2. Canada Water Treatment Chemicals Market Outlook (2025–2034)

3. Market Dynamics: Canada Water Treatment Chemicals

4. Competitive Landscape: Canada Water Treatment Chemicals Market

5. Market Segmentation Insights (2025–2034)

6. Top Companies in Canada Water Treatment Chemicals Market

7. Methodology & Appendix

Canada’s tightening federal and provincial PFAS limits, especially post-2024 draft assessments under CEPA and Nova Scotia’s 0.0002 mg/L standard, are driving utilities and industries to seek PFAS-free certifications, adopt advanced oxidation processes, and trial fluorine-free, bio-based alternatives. Suppliers must now prove product compliance, real-time traceability, and meet higher transparency demands in procurement.

Canada’s varied climates, from Arctic permafrost to humid southern cities, require regionally tailored chemical strategies—higher coagulant doses in winter, eco-friendly deicers in ice-prone zones, and specialty antiscalants for high-silica mining regions. Decentralized treatment, remote logistics, and Indigenous-led solutions also shape chemical selection and supply chain dynamics.

Alberta’s oil sands and Canada’s mining and pulp sectors drive high-performance chemical demand for scale inhibitors, corrosion control, and membrane cleaning. Upcoming mandates (like the Oil Sands Emissions Limit Act 2025) accelerate adoption of thermally stable, brine-resistant chemistries, while predictive dosing and bundled services help reduce chemical costs, emissions, and water footprints.

Suppliers are integrating chemicals with smart monitoring, MBR systems, and nutrient recovery for bundled, compliance-ready solutions. Local manufacturers leverage proximity for municipal contracts, while global players compete on ESG credentials, PFAS-free innovations, and technical partnerships—especially in remote or regulatory-challenged regions.

Coagulants and flocculants remain the largest segment (29.8% share in 2025), but membrane cleaning chemicals are growing fastest (6.6% CAGR), fueled by RO/NF expansion. The industrial sector leads growth (5.9% CAGR), driven by resource extraction, oil sands, and stricter reuse/recycling mandates, while municipal remains the core volume market.