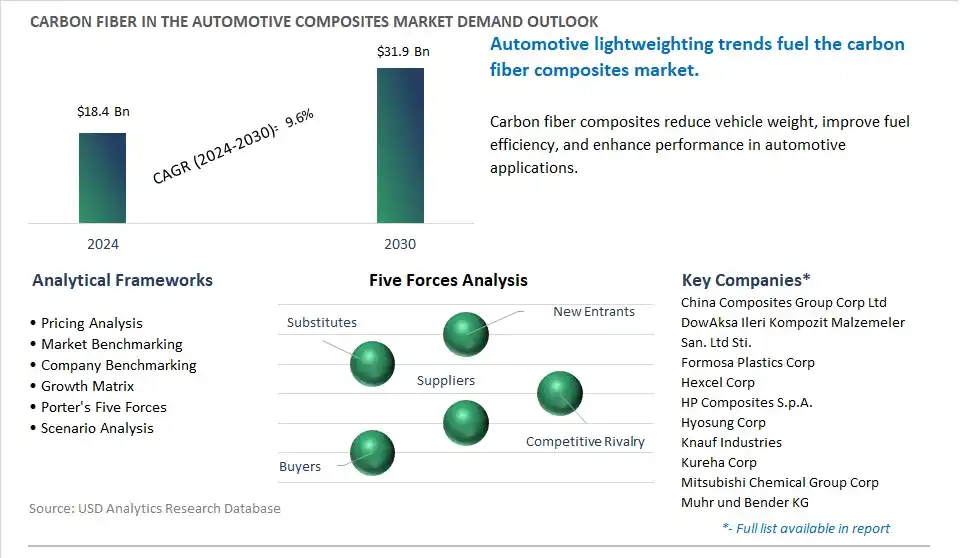

The global Carbon Fiber in the Automotive Composites Market is poised to register a 9.6% CAGR from $18.4 Billion in 2024 to $31.9 Billion in 2030.

The global Carbon Fiber in the Automotive Composites Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Material (Long Fiber Thermoplastic, Sheet Moulding Compound, Prepreg, Short Fiber Thermoplastic, Others), By Application (Exterior Components, Interior Components, Structural and Powertrains, Chassis Systems, Others).

An Introduction to Global Carbon Fiber in the Automotive Composites Market in 2024

The market for carbon fiber in automotive composites is experiencing significant growth, driven by the automotive industry's focus on lightweighting, fuel efficiency, and emission reduction. Key trends shaping the future of the industry include advancements in carbon fiber production technology, resin systems, and composite manufacturing processes, enabling the development of lightweight automotive components that offer superior strength, stiffness, and crashworthiness compared to traditional materials such as steel and aluminum. Additionally, there is a growing emphasis on electric and hybrid vehicles, where reducing vehicle weight is crucial for extending range and improving energy efficiency, driving the adoption of carbon fiber composites in applications such as body panels, chassis components, and structural reinforcements. Moreover, advancements in recycling technologies, lifecycle assessment, and circular economy initiatives are driving innovation in carbon fiber recycling and reuse, promoting the development of sustainable supply chains and closed-loop material cycles that minimize environmental impact and reduce carbon footprint in automotive manufacturing. Furthermore, collaborations between automotive OEMs, carbon fiber suppliers, and research institutions are shaping the development of next-generation carbon fiber composites tailored for automotive applications, driving market growth and competitiveness in the global automotive industry. Overall, the future of carbon fiber in automotive composites lies in continuous research and development efforts to improve material properties, reduce production costs, and scale up manufacturing capacity to meet the growing demand for lightweight solutions in the automotive sector while addressing sustainability and environmental challenges.

Carbon Fiber in the Automotive Composites Market Competitive Landscape

The market report analyses the leading companies in the industry including China Composites Group Corp Ltd, DowAksa Ileri Kompozit Malzemeler San. Ltd Sti., Formosa Plastics Corp, Hexcel Corp, HP Composites S.p.A., Hyosung Corp, Knauf Industries, Kureha Corp, Mitsubishi Chemical Group Corp, Muhr und Bender KG, Plasan Sasa Ltd, Revchem Composites Inc, SAERTEX GmbH and Co.KG, Saudi Basic Industries Corp, SGL Carbon SE, Shenzhen KIY Carbon Co. Ltd, Solvay SA, Teijin Ltd, Toray Industries Inc.

Carbon Fiber in the Automotive Composites Market Dynamics

Carbon Fiber in the Automotive Composites Market Trend: Increasing Demand for Lightweight Materials in Automotive Manufacturing

In the Carbon Fiber in the Automotive Composites market, a prominent trend is the increasing demand for lightweight materials in automotive manufacturing. Carbon fiber composites offer significant weight savings compared to traditional materials like steel and aluminum, leading to improved fuel efficiency, performance, and range in vehicles. This trend is driven by stricter fuel economy regulations, rising consumer preference for fuel-efficient and environmentally friendly vehicles, and the growing adoption of electric and hybrid vehicles. As automakers strive to meet emission targets and enhance vehicle performance, there's a rising market demand for carbon fiber composites as a key solution for lightweighting automotive components and structures.

Carbon Fiber in the Automotive Composites Market Driver: Regulatory Pressure for Fuel Efficiency and Emissions Reduction

A significant driver in the Carbon Fiber in the Automotive Composites market is regulatory pressure for fuel efficiency and emissions reduction. Governments around the world are implementing stringent regulations and emission standards to address climate change and air pollution, driving automakers to develop vehicles with lower fuel consumption and reduced greenhouse gas emissions. This driver is fueled by factors such as the Paris Agreement commitments, corporate average fuel economy (CAFE) standards, and vehicle emissions regulations in major automotive markets. Carbon fiber composites offer automakers a viable solution to meet these regulatory requirements by reducing vehicle weight and improving fuel efficiency without compromising safety or performance, driving the market demand for carbon fiber materials in automotive applications.

Carbon Fiber in the Automotive Composites Market Opportunity: Penetration into Mainstream Vehicle Models and Mass Production

A promising opportunity within the Carbon Fiber in the Automotive Composites market lies in penetration into mainstream vehicle models and mass production. While carbon fiber composites have been predominantly used in high-end sports cars and luxury vehicles due to cost constraints, advancements in manufacturing technologies and economies of scale are making carbon fiber more accessible for mass-market vehicles. Opportunities exist in collaborating with automakers to integrate carbon fiber components into mainstream vehicle models such as sedans, SUVs, and trucks, leveraging the benefits of lightweighting to improve fuel economy and performance across a broader range of vehicle segments. By targeting mass production and offering cost-effective carbon fiber solutions, manufacturers can capitalize on this opportunity to expand their market presence, increase adoption of carbon fiber composites in the automotive industry, and drive growth in the carbon fiber automotive composites market.

Carbon Fiber in the Automotive Composites Market Share Analysis: Prepreg material generated the highest revenue in 2024

The largest segment in the Carbon Fiber in the Automotive Composites Market is the Prepreg material segment. This dominance is. prepreg carbon fiber materials offer superior mechanical properties, including high strength, stiffness, and impact resistance, making them well-suited for structural automotive components requiring lightweight and high-performance materials. Prepregs consist of carbon fibers pre-impregnated with a resin matrix, epoxy or thermoplastic resin, which ensures uniform resin distribution and optimal fiber alignment during the manufacturing process, resulting in consistent and high-quality composite parts. Additionally, prepreg carbon fiber materials offer excellent dimensional stability, fatigue resistance, and corrosion resistance, making them ideal for use in automotive applications where durability and reliability are essential. Further, advancements in prepreg manufacturing technology, such as automated layup processes, improved resin formulations, and advanced curing techniques, have enhanced the efficiency, productivity, and cost-effectiveness of producing prepreg composite components for automotive use. Furthermore, the growing demand for lightweight materials to improve fuel efficiency, reduce emissions, and enhance vehicle performance drives the adoption of prepreg carbon fiber composites in automotive manufacturing. Therefore, the Prepreg material segment continues to lead the Carbon Fiber in the Automotive Composites Market due to its superior performance characteristics, reliability, and extensive application across various automotive components.

Carbon Fiber in the Automotive Composites Market Share Analysis: Structural and Powertrains segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The fastest-growing segment in the Carbon Fiber in the Automotive Composites Market is the Structural and Powertrains application segment. There is an increasing trend towards lightweighting in the automotive industry to improve fuel efficiency, reduce emissions, and enhance vehicle performance. Carbon fiber composites offer significant weight savings compared to traditional materials like steel and aluminum while maintaining high strength and stiffness, making them ideal for structural components and powertrain parts. Further, as automotive manufacturers strive to meet stringent emissions regulations and customer demands for greener vehicles, they are increasingly turning to carbon fiber composites to reduce vehicle weight and improve overall efficiency. Additionally, advancements in carbon fiber manufacturing technology, such as automated layup processes, resin infusion techniques, and hybrid material solutions, have lowered production costs and improved manufacturing efficiency, making carbon fiber composites more attractive for structural and powertrain applications. Further, the increasing adoption of electric and hybrid vehicles, which require lightweight yet durable components to maximize battery range and performance, further drives the demand for carbon fiber composites in structural and powertrain applications. Therefore, the Structural and Powertrains application segment presents significant growth opportunities in the Carbon Fiber in the Automotive Composites Market, driven by the imperative for lightweighting, regulatory compliance, and technological advancements in automotive manufacturing.

Carbon Fiber in the Automotive Composites Market Report Segmentation

By Material

Long Fiber Thermoplastic

Sheet Moulding Compound

Prepreg

Short Fiber Thermoplastic

Others

By Application

Exterior Components

Interior Components

Structural and Powertrains

Chassis Systems

Others

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Carbon Fiber in the Automotive Composites Companies Profiled in the Market Study

China Composites Group Corp Ltd

DowAksa Ileri Kompozit Malzemeler San. Ltd Sti.

Formosa Plastics Corp

Hexcel Corp

HP Composites S.p.A.

Hyosung Corp

Knauf Industries

Kureha Corp

Mitsubishi Chemical Group Corp

Muhr und Bender KG

Plasan Sasa Ltd

Revchem Composites Inc

SAERTEX GmbH and Co.KG

Saudi Basic Industries Corp

SGL Carbon SE

Shenzhen KIY Carbon Co. Ltd

Solvay SA

Teijin Ltd

Toray Industries Inc

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Carbon Fiber in the Automotive Composites Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Carbon Fiber in the Automotive Composites Market Size Outlook, $ Million, 2021 to 2030

3.2 Carbon Fiber in the Automotive Composites Market Outlook by Type, $ Million, 2021 to 2030

3.3 Carbon Fiber in the Automotive Composites Market Outlook by Product, $ Million, 2021 to 2030

3.4 Carbon Fiber in the Automotive Composites Market Outlook by Application, $ Million, 2021 to 2030

3.5 Carbon Fiber in the Automotive Composites Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Carbon Fiber in the Automotive Composites Industry

4.2 Key Market Trends in Carbon Fiber in the Automotive Composites Industry

4.3 Potential Opportunities in Carbon Fiber in the Automotive Composites Industry

4.4 Key Challenges in Carbon Fiber in the Automotive Composites Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Carbon Fiber in the Automotive Composites Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Carbon Fiber in the Automotive Composites Market Outlook by Segments

7.1 Carbon Fiber in the Automotive Composites Market Outlook by Segments, $ Million, 2021- 2030

By Material

Long Fiber Thermoplastic

Sheet Moulding Compound

Prepreg

Short Fiber Thermoplastic

Others

By Application

Exterior Components

Interior Components

Structural and Powertrains

Chassis Systems

Others

8 North America Carbon Fiber in the Automotive Composites Market Analysis and Outlook To 2030

8.1 Introduction to North America Carbon Fiber in the Automotive Composites Markets in 2024

8.2 North America Carbon Fiber in the Automotive Composites Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Carbon Fiber in the Automotive Composites Market size Outlook by Segments, 2021-2030

By Material

Long Fiber Thermoplastic

Sheet Moulding Compound

Prepreg

Short Fiber Thermoplastic

Others

By Application

Exterior Components

Interior Components

Structural and Powertrains

Chassis Systems

Others

9 Europe Carbon Fiber in the Automotive Composites Market Analysis and Outlook To 2030

9.1 Introduction to Europe Carbon Fiber in the Automotive Composites Markets in 2024

9.2 Europe Carbon Fiber in the Automotive Composites Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Carbon Fiber in the Automotive Composites Market Size Outlook by Segments, 2021-2030

By Material

Long Fiber Thermoplastic

Sheet Moulding Compound

Prepreg

Short Fiber Thermoplastic

Others

By Application

Exterior Components

Interior Components

Structural and Powertrains

Chassis Systems

Others

10 Asia Pacific Carbon Fiber in the Automotive Composites Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Carbon Fiber in the Automotive Composites Markets in 2024

10.2 Asia Pacific Carbon Fiber in the Automotive Composites Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Carbon Fiber in the Automotive Composites Market size Outlook by Segments, 2021-2030

By Material

Long Fiber Thermoplastic

Sheet Moulding Compound

Prepreg

Short Fiber Thermoplastic

Others

By Application

Exterior Components

Interior Components

Structural and Powertrains

Chassis Systems

Others

11 South America Carbon Fiber in the Automotive Composites Market Analysis and Outlook To 2030

11.1 Introduction to South America Carbon Fiber in the Automotive Composites Markets in 2024

11.2 South America Carbon Fiber in the Automotive Composites Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Carbon Fiber in the Automotive Composites Market size Outlook by Segments, 2021-2030

By Material

Long Fiber Thermoplastic

Sheet Moulding Compound

Prepreg

Short Fiber Thermoplastic

Others

By Application

Exterior Components

Interior Components

Structural and Powertrains

Chassis Systems

Others

12 Middle East and Africa Carbon Fiber in the Automotive Composites Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Carbon Fiber in the Automotive Composites Markets in 2024

12.2 Middle East and Africa Carbon Fiber in the Automotive Composites Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Carbon Fiber in the Automotive Composites Market size Outlook by Segments, 2021-2030

By Material

Long Fiber Thermoplastic

Sheet Moulding Compound

Prepreg

Short Fiber Thermoplastic

Others

By Application

Exterior Components

Interior Components

Structural and Powertrains

Chassis Systems

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

China Composites Group Corp Ltd

DowAksa Ileri Kompozit Malzemeler San. Ltd Sti.

Formosa Plastics Corp

Hexcel Corp

HP Composites S.p.A.

Hyosung Corp

Knauf Industries

Kureha Corp

Mitsubishi Chemical Group Corp

Muhr und Bender KG

Plasan Sasa Ltd

Revchem Composites Inc

SAERTEX GmbH and Co.KG

Saudi Basic Industries Corp

SGL Carbon SE

Shenzhen KIY Carbon Co. Ltd

Solvay SA

Teijin Ltd

Toray Industries Inc

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Material

Long Fiber Thermoplastic

Sheet Moulding Compound

Prepreg

Short Fiber Thermoplastic

Others

By Application

Exterior Components

Interior Components

Structural and Powertrains

Chassis Systems

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)