Market Overview: Circular Gypsum Recycling, Renewable Manufacturing, and Acoustic Innovation Reshape Ceiling Tiles Market

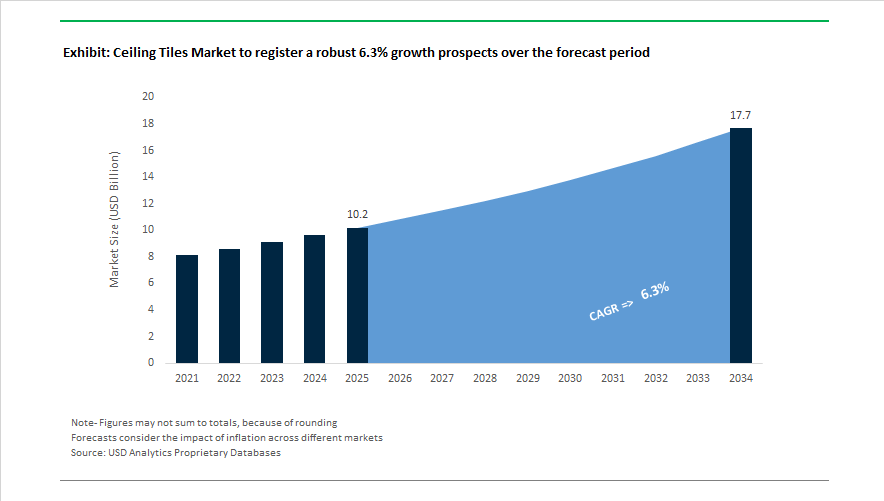

The Ceiling Tiles Market is projected to grow from USD 10.2 billion in 2025 to USD 17.7 billion by 2034, registering a CAGR of 6.3% as demand rises for acoustic ceiling systems, mineral fiber ceiling tiles, metal ceiling panels, and sustainable gypsum boards in commercial infrastructure, healthcare, education, and office renovation projects. In 2024, Saint-Gobain inaugurated its first plasterboard plant powered entirely by renewable electricity in North America, lowering embodied carbon for gypsum ceiling products and aligning with LEED and BREEAM green building certifications. During the same year, Hunter Douglas Architectural introduced its 2024 to 2026 product guide, organizing ceiling systems under Luxalon metal, HeartFelt felt, and Derako wood brands to simplify sustainable material selection for architects.

Pricing and capacity strategy defined 2025 developments. Rockfon implemented a 7% price increase on stone wool ceiling tiles in February 2025, reflecting rising logistics and mineral input costs. In July 2025, Knauf unified Knauf Insulation and Knauf Ceiling Solutions at its Illange site in France to strengthen integrated R&D for acoustic and thermal ceiling systems. October 2025 saw Rockfon launch its redesigned Canva wall and ceiling panels with AKUART, introducing lighter modular acoustic solutions designed for disassembly and reuse in office retrofits. In December 2025, Saint-Gobain expanded its construction materials footprint in Indonesia to localize production of Gyproc and metal ceiling systems for Southeast Asia’s commercial building pipeline. The same month, Armstrong World Industries received recognition as one of America’s Greenest Companies for 2026, reflecting progress in recycled mineral fiber usage and low-VOC ceiling tile production.

Industry restructuring and circularity investments accelerated into 2026. Knauf and BSR Ingolstadt confirmed in January 2026 the development of Bavaria’s most advanced gypsum recycling facility, enabling recovery of construction waste gypsum for reuse in ceiling board manufacturing. In January 2026, Armstrong World Industries announced a leadership transition as part of its long-term strategy to accelerate digitalization and growth in modular ceiling solutions. ROCKWOOL Group, parent of Rockfon, reported strong 2025 performance and outlined €650 million in 2026 investments for capacity expansion and factory electrification in the United States and India. Knauf India strengthened market engagement earlier in October 2024 with the launch of its Delhi-NCR Experience Center for architects and contractors. Saint-Gobain also maintained its CDP A List climate rating in December 2025, reinforcing sustainability leadership across global gypsum and ceiling tile production.

Trends and Opportunities Transforming the Ceiling Tiles Market

Stricter Acoustic Compliance in Offices, Schools, and Hybrid Work Environments

Acoustics has moved from a design preference to a regulatory requirement for corporate, education, and public infrastructure projects. Tender specifications in North America and Europe now commonly require Noise Reduction Coefficient (NRC) values above 0.90 and Ceiling Attenuation Class (CAC) ratings above 35. These requirements are driven by post-occupancy performance data indicating that inadequate sound absorption can reduce employee cognitive focus by up to 66% and negatively affect student learning outcomes.

Manufacturers are responding with high-specification acoustic tile portfolios. Knauf Ceiling Solutions' June 2025 launch of TOPIQ® Alpha in the UK and Ireland exemplifies this shift. The laminated mineral series provides Class A acoustic absorption and 86% light reflectance, supporting LEED daylighting credits and contributing to lower artificial lighting demand—integrating acoustics and energy efficiency into a single specification narrative.

For market participants, acoustic capability is shifting from differentiator to minimum compliance. Growth is increasingly centered in ultra-absorption and combined acoustic-lighting performance systems targeted at open-plan environments, call centers, K–12 schools, and university learning spaces.

Decarbonization Drives PVC-Free and Bio-Based Ceiling Tiles

Sustainability-driven procurement is reshaping product portfolios under pressure from the EU’s Digital Product Passport (DPP), expanded REACH requirements, and U.S. sustainable building tax incentives. Buyers increasingly require verified traceability of chemical composition, embodied carbon, and recycled content.

Armstrong World Industries’ 2025 enhancements to CALLA® TEMPLOK® and ULTIMA® TEMPLOK® reflect this trend. Panels are now fully PVC-free and incorporate phase-change materials that deliver up to 15% energy savings by stabilizing indoor temperature fluctuation. Their qualification under sustainable incentive programs that enable tax reductions of up to 50% has strengthened contractor adoption.

Rockfon’s reported 64% recycled content in 2025 and ROCKWOOL’s recycling of 59,000 tonnes of stone wool waste demonstrate how circular material commitments are now core commercial levers rather than CSR claims. As governments enforce DPP starting January 2025, providers unable to verify source materials and environmental performance will lose access to government-funded and ESG-screened commercial tenders.

Healthcare Infrastructure Modernization: Hygienic, Anti-Ligature and Moisture-Resistant Tiles

Post-pandemic hospital upgrades and expansions represent one of the highest-margin demand segments. Ceiling tiles are no longer evaluated solely on hygiene but on behavioral safety, cleanability, lighting, and ventilation compatibility.

In September 2025, Armstrong’s METALWORKS™ Torsion Spring series entered the behavioral health space, engineered for anti-ligature performance and compliant with ASHRAE 170 ventilation standards. Moisture-resistant and smooth-surface systems are also gaining momentum in diagnostic facilities and laboratories. Saint-Gobain Gyproc’s Gyprex® Asepta series demonstrates the new standard: PVC-free antimicrobial finishes, 90% relative humidity tolerance, and >80% light reflectance enabling sterile operation and visual acuity.

Given that over 30% of US hospital stock is over 40 years old, modernization cycles will continue to create recurring replacement demand. Suppliers that package antimicrobial finishes, moisture performance, and energy optimization into a single product line will win procurement cycles over commodity tile manufacturers.

Smart Ceilings as Digital Infrastructure Platforms

The Ceiling Tiles Market is also intersecting with the growth of the smart building ecosystem. Tiles are increasingly being specified as platforms that host sensors, lighting, HVAC air-distribution modules, and RFID-based maintenance tracking.

Armstrong’s March 2025 Material Optimization Analysis within PROJECTWORKS® now enables architects to digitally pre-design sensor pathways and minimize waste material through Building Information Modeling (BIM). This directly supports compliance with the U.S. GSA P100 standards for federal buildings and aligns with commercial developers prioritizing operational efficiency through digital twins and remote facility management.

Saint-Gobain Ecophon and Armstrong (following its 2025 acquisition of Geometrik) are advancing acoustically transparent micro-perforated wood and felt systems that maintain NRC values up to 0.70. These solutions allow hidden embedding of IoT devices, speakers, and air sensors without compromising architectural aesthetics, a priority in premium office interiors and high-end hospitality.

Ceiling Tiles Market Share and Segmentation Insights

Market Share by Material: Mineral Fiber Anchors Volume While Metal and Bio-Based Panels Gain Design Traction

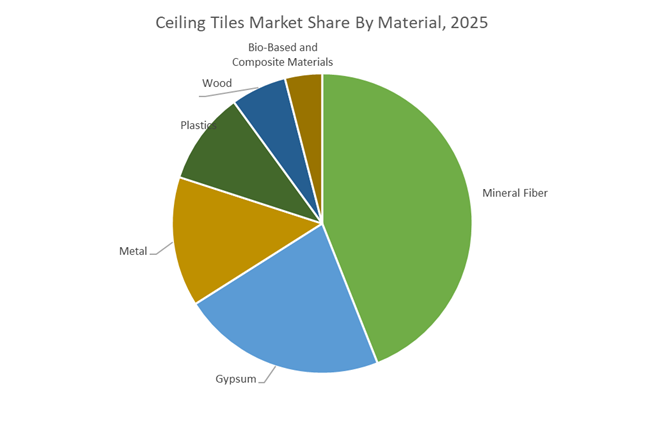

Mineral fiber ceiling tiles account for 44% of global demand in 2025, maintaining leadership due to their strong acoustic absorption, inherent fire resistance, and cost efficiency across commercial offices, schools, hospitals, and retail interiors. Composed of mineral wool, perlite, slag wool, and cellulose fibers, these tiles remain the default choice for suspended ceiling systems, with demand closely tracking non-residential construction activity. Gypsum holds the second-largest share, driven by residential drywall ceilings and moisture-resistant variants specified for kitchens and bathrooms. Metal ceiling tiles represent a fast-growing premium segment, particularly in healthcare, laboratories, and food processing, where hygiene, durability, and perforated acoustic designs are critical. Plastics serve moisture-prone and budget applications, while wood remains niche for high-end interiors. Bio-based and composite materials are the fastest-growing category, supported by LEED, BREEAM, and WELL certifications, though higher costs and limited manufacturing scale constrain near-term penetration.

Market Share by Property: Acoustic Tiles Lead as Energy-Saving Systems Emerge

Acoustic ceiling tiles dominate with 48% market share in 2025, reflecting rising demand for noise control and speech privacy in open-plan offices, education facilities, and healthcare environments. NRC and CAC ratings are now standard specification criteria, favoring mineral fiber and perforated metal systems. Fire-rated tiles represent the second-largest segment, driven by stringent life-safety codes in egress corridors and high-occupancy buildings. Moisture-resistant tiles are gaining share in hospitality, coastal construction, and healthcare, where mold and mildew resistance is increasingly mandated. Non-acoustic tiles continue to decline as acoustic comfort becomes a baseline expectation. Energy-saving ceilings remain the smallest but fastest-growing segment, incorporating high-reflectance coatings, radiant panels, and phase change materials to reduce lighting and HVAC loads, supported by ASHRAE 90.1, IECC compliance, and net-zero building targets.

Competitive Landscape of the Ceiling Tiles Market

The global ceiling tiles market in 2026 is increasingly defined by smart acoustic systems, thermal-regulating ceiling panels, circular building materials, and data-center-ready structural grids. Competition centers on high-NRC acoustic tiles, fire- and moisture-resistant ceilings, low-VOC mineral solutions, and digitally customized architectural systems. Market leaders are differentiating through phase change materials (PCM), Cradle to Cradle certification, IoT-enabled ceiling monitoring, and integrated construction ecosystems, addressing strong demand from commercial offices, healthcare facilities, data centers, education, and green buildings. Sustainability credentials such as Red List Free products, PVC-free tiles, and recyclability programs are now decisive factors shaping procurement across North America, Europe, and Asia-Pacific.

Smart thermal ceilings and data-center grids led by Armstrong World Industries

Armstrong World Industries enters 2026 as the North American technology leader in thermal-regulating ceiling tiles and smart structural grids. Its DynaMax LT Structural Grid with DataZone panels is engineered for colocation data centers, supporting extreme loads while optimizing airflow. The Templok® Calla® and Ultima® series integrate phase change materials, helping reduce HVAC energy consumption by up to 15% in green buildings. Following the acquisition of Parallel Architectural Products, Armstrong now offers unified interior-exterior architectural solutions. Its Sustain® portfolio targets PVC-free and Red List Free ceilings, aligning with federal low-carbon building incentives and reinforcing Armstrong’s leadership in commercial acoustic ceilings, energy-efficient ceiling systems, and smart building integration.

Multi-material ceiling ecosystems powered by Saint-Gobain

Saint-Gobain dominates 2026 through multi-material ceiling integration, combining gypsum, mineral wool, and glass technologies at global scale. The Rigiroc hybrid ceiling board supports heavy loads while maintaining fire and moisture resistance, addressing institutional construction needs. Its Ecophon range sets benchmarks in healthcare and clean rooms with biocidal surfaces and NRC above 0.90 for speech intelligibility. A major manufacturing investment in Western India strengthens Asia-Pacific supply for hospitals and education buildings. With FOSROC now integrated, Saint-Gobain delivers ceiling tiles as part of a broader construction chemicals ecosystem, positioning itself as a leader in fire-rated ceilings, acoustic healthcare solutions, and large-scale infrastructure interiors.

Circular design-driven ceiling systems from Knauf Ceiling Solutions

Knauf Ceiling Solutions advances a multi-material and circular economy strategy in 2026, expanding its Cradle to Cradle certified portfolio across mineral, metal, and wood-wool tiles. HERADESIGN® wood wool ceilings are widely adopted for biophilic offices and schools, blending organic aesthetics with high acoustic absorption. Knauf’s DesignScapes digital platform enables architects to customize shapes and colors before factory production, while its AI-powered Systemfinder instantly aligns projects with fire, seismic, and acoustic codes. This combination of sustainability, digitalization, and architectural flexibility positions Knauf as a preferred partner for custom acoustic ceilings, circular building interiors, and next-generation workspace design.

Stone wool acoustic leadership delivered by Rockfon

Rockfon specializes in stone wool ceiling technology, resolving the traditional trade-off between acoustics and fire safety. Its Rockfon® Mono® Acoustic system provides seamless monolithic ceilings achieving Class A sound absorption without visible grids. The Colors of Wellbeing collection introduces 34 nature-inspired shades tailored for wellness-focused workplaces. Thanks to non-organic composition, Rockfon dominates high-humidity applications such as pools and commercial kitchens where mold resistance is critical. As the only stone wool ceiling manufacturer in North America in 2026, Rockfon benefits from strong logistics advantages, reinforcing its position in fire-safe acoustic ceilings, moisture-resistant tiles, and healthcare-grade interiors.

IoT-enabled gypsum ceilings advanced by USG Corporation

USG Corporation maintains leadership in specialty wall and ceiling systems across the Americas, backed by Knauf ownership. In 2026, USG introduced IoT-enabled ceiling monitoring, detecting moisture buildup and structural shifts for commercial property managers. Its Mars™ and Halcyon™ high-reflectance tiles help retail spaces reduce lighting costs, while redesigned surface-mount and drop systems accelerate residential renovations through lightweight gypsum cores. Heavy investment in automated manufacturing has cut material waste by 20% while improving fire ratings. USG’s strategy emphasizes smart ceilings, DIY-friendly systems, and automated gypsum production, strengthening its footprint in renovation and commercial interiors.

Premium mineral ceilings engineered by OWA

OWA stands out in 2026 as Germany’s precision-focused mineral wool ceiling specialist serving premium institutional projects. Its OWAcoustic Octave 80 delivers NRC 0.80 with CAC 33 dB, supporting the rise of acoustic pods in open offices. OWAtecta metal tiles integrate seamlessly with mineral systems, enabling mixed-material designs within a single grid. With over two decades of plant-based organic binder technology, OWA leads the low-VOC and formaldehyde-free ceiling segment. Through its OWA green circle initiative, reclaimed tiles are recycled into new batches, reinforcing OWA’s position in sustainable mineral ceilings, acoustic workplace solutions, and circular renovation projects.

United States: PCM-Enabled HVAC Optimization, Buy Clean Mandates, and Architectural Specialization Drive Ceiling Tile Innovation

The United States ceiling tiles industry is advancing through energy-efficiency integration, green procurement mandates, and architectural diversification. In August 2024, the U.S. General Services Administration, in collaboration with the U.S. Department of Energy, initiated real-world performance trials of Phase Change Material (PCM) ceiling tiles supplied by Armstrong World Industries. These PCM-integrated ceiling systems are engineered to reduce HVAC loads by up to 15% by absorbing and releasing latent thermal energy, aligning with federal decarbonization targets for public buildings.

Armstrong expanded its Architectural Specialties portfolio in 2024–2025 through acquisitions of 3form, BOK Modern, and Zahner, moving beyond mineral fiber toward high-end metal and translucent resin ceiling systems. The federal Buy Clean initiative and state-level legislation in Washington and California are accelerating demand for low-embodied-carbon ceiling panels supported by third-party verified Environmental Product Declarations (EPDs). BIM-integrated product data now enables architects to simulate NRC, CAC, and fire ratings within digital twin environments, shortening the design-to-procurement cycle by approximately 20% . Armstrong reported record net sales of $1.4 billion in 2024, including a 17.7% Q4 increase, supported by strong architectural segment volumes. Capacity expansions in mineral fiber and rock wool manufacturing are underway to support growing healthcare and education infrastructure demand for bio-based and recycled-fiber acoustic ceiling panels.

India: BIS-Compliant Manufacturing, PLI-Driven Infrastructure Expansion, and Skill Development Acceleration

India’s ceiling tiles market is scaling alongside infrastructure investments and regulatory alignment. In September 2025, Knauf India announced full compliance of its plasterboard and ceiling portfolio with Bureau of Indian Standards (BIS) ISI norms, meeting strengthened safety and quality mandates. The launch of Knauf’s first Experience Center in Delhi-NCR in late 2024 provides architects and contractors with interactive demonstrations of suspended ceiling systems and advanced drywall technologies.

Workforce constraints are being addressed through collaboration with the National Skill Development Corporation, which partnered with Knauf to establish a specialized training academy in Gorakhpur focused on precision installation of suspended ceilings. The Production Linked Incentive (PLI) Scheme has catalyzed over ₹2 lakh crore in investments across manufacturing sectors as of September 2025, indirectly fueling demand for commercial ceiling tiles in electronics and pharmaceutical hubs. Urbanization, projected to reach 36% , is encouraging adoption of green building materials under the National Gati Shakti infrastructure framework. Global players such as Rockwool have expanded domestic capacity in 2025 to localize mineral wool production and reduce logistics costs through utilization of industrial by-products.

China: 300 Billion Yuan Green Building Target and 75% Energy Reduction Standards Elevate Ceiling Demand

China’s ceiling tiles industry is closely aligned with national green building revenue targets and energy-saving mandates. In September 2025, six government bodies including the Ministry of Industry and Information Technology announced a two-year growth plan targeting over 300 billion yuan (~$42.2 billion) in green building material revenues by 2026. Complementing this, Shanghai’s Residential Building Energy Saving Design Standard (DG/TJ08-205-2024), introduced in July 2024, mandates up to 75% energy reduction in new residential developments, driving adoption of high-thermal-resistance ceiling and roofing systems.

China’s decarbonization roadmap requires all new urban buildings to meet green standards by 2025, influencing procurement in public projects that dominate domestic construction demand. The green building materials market is projected to reach $38 billion by the end of 2025, propelled by Smart City initiatives and urbanization programs. Manufacturers are investing in advanced inorganic non-metallic materials and exporting technical standards to Belt and Road partner countries, reinforcing China’s leadership in cost-efficient, energy-saving ceiling tile systems.

France: Illange Mineral Ceiling Integration and RE2020-Driven Net-Zero Manufacturing

France’s ceiling tiles market is benefiting from industrial integration and climate regulation alignment. In July 2025, Knauf Group inaugurated a new ceiling solutions facility in Illange, Grand Est, integrating Knauf Insulation and Knauf Ceiling Solutions under one site. The facility utilizes on-site rock wool production and features a high-tech finishing line supplied by Biele Group, enabling automated laminating, trimming, and profiling for Soft Ceiling Tiles with enhanced acoustic performance.

French manufacturing upgrades increasingly rely on Electric Melting technology to reduce Scope 1 and Scope 2 emissions, with Rockwool investing in plant conversions to align with EU climate objectives. The RE2020 environmental regulation continues to stimulate demand for bio-sourced, recyclable ceiling systems in both residential and commercial construction, reinforcing France’s leadership in low-carbon building envelope materials.

Germany: BIM-Centric Specification Leadership and CO₂ Reduction Benchmarks

Germany’s ceiling tile industry leads in digital specification workflows and multi-material integration. BIM-compatible product data allows real-time validation of acoustic, thermal, and fire-resistance metrics during project design stages, improving project accuracy and procurement efficiency. Following the integration of Armstrong Ceiling Solutions into Knauf Ceiling Solutions, the unified European service model now delivers mineral, metal, and wood ceiling systems under a single technical support platform.

German production sites are at the forefront of carbon reduction, with Rockwool reporting a 20% reduction in absolute CO₂ emissions between 2019 and 2025 and targeting a 38% reduction by 2034. These sustainability benchmarks position Germany as a reference market for environmentally optimized mineral ceiling tiles within the EU framework.

Denmark: Circular Mineral Wool Recycling and €650 Million CAPEX Commitment

Denmark’s ceiling tile and mineral wool sector demonstrates resilience and circular leadership. Rockwool reported full-year 2025 sales of €3.88 billion, maintaining profitability despite global headwinds and asset transfers in early 2026. Danish firms are pioneering closed-loop recycling systems in which spent ceiling tiles from renovation projects are reclaimed and reprocessed into new mineral wool, delivering energy savings estimated at 100 times compared to virgin production.

In 2025, Danish industry leaders allocated €650 million in CAPEX toward capacity expansions and conversion to electric melting technologies, prioritizing strategic sites in the United States, India, and Romania. This investment underscores Denmark’s role as a global hub for sustainable ceiling tile manufacturing, advanced mineral fiber production, and circular construction materials innovation.

Ceiling Tiles Market Report Scope

Ceiling Tiles Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$10.2 Billion

|

|

Market Size (2034)

|

$17.7 Billion

|

|

Market Growth Rate

|

6.3%

|

|

Segments

|

By Material (Mineral Fiber, Gypsum, Metal, Wood, Plastics, Bio Based and Composite Materials), By Product Type (Lay In Ceilings, Concealed Grid Ceilings, Clip In Panels, Baffles and Blades, Clouds and Canopies), By Property (Acoustic, Non Acoustic, Fire Rated, Moisture Resistant, Energy Saving), By End User (Commercial, Institutional, Industrial, Residential)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Armstrong World Industries, Saint Gobain, Knauf Ceiling Solutions, Rockfon, USG Corporation, Hunter Douglas, SAS International, Georgia Pacific, Odenwald Faserplattenwerk, AWI Manufacturing, Siniat, CertainTeed, Techno Ceilings, Beijing New Building Materials, Gordon

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Ceiling Tiles Market Segmentation

By Material

- Mineral Fiber

- Gypsum

- Metal

- Wood

- Plastics

- Bio Based and Composite Materials

By Product Type

- Lay In Ceilings

- Concealed Grid Ceilings

- Clip In Panels

- Baffles and Blades

- Clouds and Canopies

By Property

- Acoustic

- Non Acoustic

- Fire Rated

- Moisture Resistant

- Energy Saving

By End User

- Commercial

- Institutional

- Industrial

- Residential

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Ceiling Tiles Industry

- Armstrong World Industries

- Saint Gobain

- Knauf Ceiling Solutions

- Rockfon

- USG Corporation

- Hunter Douglas

- SAS International

- Georgia Pacific

- Odenwald Faserplattenwerk

- AWI Manufacturing

- Siniat

- CertainTeed

- Techno Ceilings

- Beijing New Building Materials

- Gordon

*- List not Exhaustive