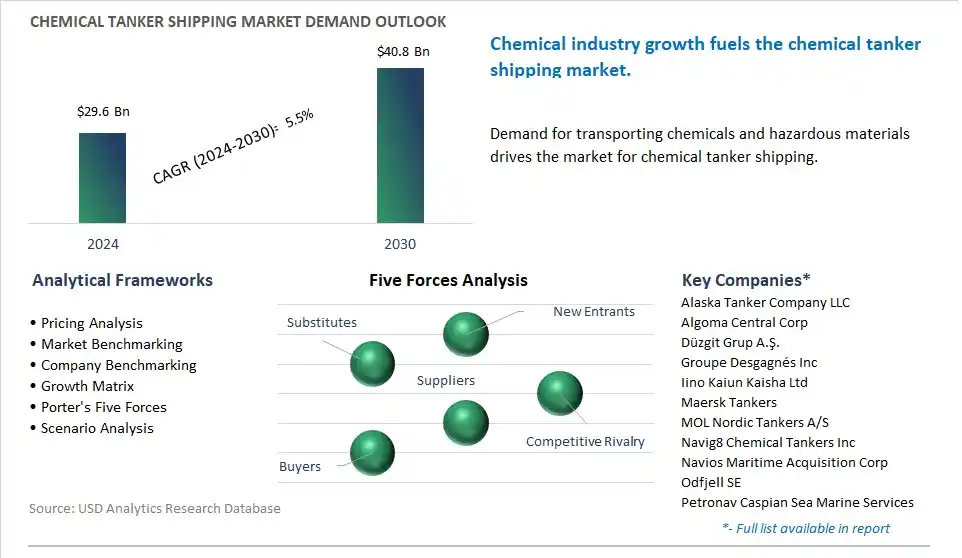

The global Chemical Tanker Shipping Market is poised to register a 5.5% CAGR from $29.6 Billion in 2024 to $40.8 Billion in 2030.

The global Chemical Tanker Shipping Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Product (Organic Chemicals, Inorganic Chemicals, Vegetable Oils and Fats, Others), By Shipment (Inland, Coastal, Deep Sea), By Cargo Type (IMO I, IMO II, IMO III), By Coating (Stainless Steel Tanks, Epoxy Coated Tankers).

An Introduction to Global Chemical Tanker Shipping Market in 2024

The chemical tanker shipping market is experiencing significant growth driven by global trade, chemical production, and regulatory compliance requirements. Key trends shaping the future of the industry include the increasing demand for specialized chemical tankers equipped with advanced cargo handling systems, safety features, and environmental safeguards. As chemical producers and shippers seek to transport a diverse range of hazardous and non-hazardous chemicals safely and efficiently, there's a growing need for vessels capable of meeting stringent regulations and industry standards. Moreover, advancements in vessel design, propulsion systems, and cargo monitoring technologies are enhancing operational efficiency, reducing emissions, and minimizing environmental impact, driving market growth. Additionally, the rising adoption of digitalization and data analytics is optimizing route planning, voyage optimization, and fleet management, enabling shipping companies to improve cost-effectiveness and customer service. Furthermore, the integration of sustainability initiatives such as ballast water treatment, fuel efficiency measures, and carbon footprint reduction is aligning with industry efforts to promote responsible and environmentally friendly chemical tanker shipping practices.

Chemical Tanker Shipping Market Competitive Landscape

The market report analyses the leading companies in the industry including Alaska Tanker Company LLC, Algoma Central Corp, Düzgit Grup A.Åž., Groupe Desgagnés Inc, Iino Kaiun Kaisha Ltd, Maersk Tankers, MOL Nordic Tankers A/S, Navig8 Chemical Tankers Inc, Navios Maritime Acquisition Corp, Odfjell SE, Petronav Caspian Sea Marine Services Private Ltd, Stena Bulk AB, Stolt-Nielsen Ltd, Uni-Tankers A/S, UPT United Product Tankers GmbH & Co. KG.

Chemical Tanker Shipping Market Dynamics

Chemical Tanker Shipping Market Trend: Increasing Demand for Environmentally Friendly Shipping Solutions

In recent years, there has been a notable trend towards sustainability and environmental responsibility in the shipping industry, particularly in the realm of chemical tanker shipping. With growing awareness of the ecological impact of traditional fuel sources, there is a significant shift towards cleaner alternatives such as LNG (liquefied natural gas) and biofuels. This trend is driven not only by regulatory pressures but also by consumer demand for greener transportation options. Consequently, chemical tanker operators are investing in eco-friendly technologies and retrofitting their vessels to meet stringent emission standards, positioning themselves as leaders in sustainable shipping solutions.

Chemical Tanker Shipping Market Driver: Global Economic Expansion and Trade Growth

The chemical tanker shipping market is heavily influenced by global economic conditions and trade dynamics. As economies expand and international trade volumes increase, the demand for chemicals and petrochemicals rises accordingly. This demand is further propelled by population growth, urbanization trends, and the ongoing industrialization of emerging markets. Additionally, advancements in technology and manufacturing processes are driving innovation and diversification within the chemical industry, leading to a wider array of products requiring transportation. Consequently, chemical tanker operators are experiencing heightened demand for their services, particularly on key trade routes, driving fleet expansion and investment in new vessels.

Chemical Tanker Shipping Market Opportunity: Embracing Digitalization and Automation

Amidst the evolving landscape of chemical tanker shipping, there lies a significant opportunity for industry players to embrace digitalization and automation technologies. By harnessing the power of data analytics, artificial intelligence, and IoT (Internet of Things), operators can optimize vessel performance, enhance safety standards, and streamline operational efficiency. Real-time monitoring systems can provide valuable insights into cargo conditions, fuel consumption, and route optimization, enabling proactive decision-making and cost savings. Furthermore, automation solutions such as unmanned vessels and autonomous navigation systems hold the potential to revolutionize the industry by reducing human error, lowering operational costs, and improving overall sustainability. Embracing these technological advancements presents a compelling opportunity for chemical tanker shipping companies to gain a competitive edge in a rapidly evolving market landscape.

Chemical Tanker Shipping Market Share Analysis: Organic Chemicals segment generated the highest revenue in the industry

Among the delineated segments based on product type, Organic Chemicals emerge as the largest segment in the Chemical Tanker Shipping Market, driven by diverse pivotal factors. Organic chemicals encompass a wide range of substances derived from carbon-based compounds, including solvents, intermediates, polymers, and specialty chemicals, which are vital raw materials for various industries, such as pharmaceuticals, petrochemicals, and agrochemicals. The dominance of organic chemicals in the Chemical Tanker Shipping Market is driven by organic chemicals constitute a significant portion of global chemical trade volumes, driven by the widespread use of organic compounds in manufacturing processes and end-user applications. The transport of organic chemicals via chemical tankers is essential for ensuring a secure and reliable supply chain, enabling manufacturers to access raw materials from diverse sources and optimize production efficiency. Additionally, organic chemicals often require specialized handling and transportation due to their hazardous or sensitive nature, making chemical tankers equipped with proper containment, safety, and environmental protection systems indispensable for their transport. In addition, the global demand for organic chemicals is driven by factors such as population growth, urbanization, industrialization, and technological advancements, which stimulate consumption across diverse sectors. Further, the strategic importance of organic chemicals in critical industries, including healthcare, agriculture, and manufacturing, ensures sustained demand for chemical tanker shipping services. As a result, the Organic Chemicals segment maintains its dominance in the Chemical Tanker Shipping Market, reflecting its pivotal role in facilitating global trade and industrial activities while adhering to stringent safety and environmental regulations.

Chemical Tanker Shipping Market Share Analysis: Deep Sea Shipments Segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

Among the delineated segments based on shipment type, Deep Sea Shipments emerge as the fastest-growing segment in the Chemical Tanker Shipping Market, driven by diverse compelling factors. Deep sea shipments involve the transportation of chemical cargoes over long distances, between continents or across major oceanic routes. The growth of deep sea shipments can be attributed to diverse key trends in the chemical industry and global trade. The the globalization of chemical production and supply chains has led to increased demand for long-distance transportation of chemicals from production hubs to consumption centers worldwide. Additionally, the expansion of chemical manufacturing capacities in regions with abundant feedstock and lower production costs, such as Asia and the Middle East, has resulted in the need for efficient transportation solutions to export chemical products to distant markets. In addition, advancements in shipping technologies, vessel designs, and logistics management have improved the efficiency, reliability, and safety of deep sea chemical tanker operations, making them increasingly attractive for chemical producers and shippers. Further, the growing demand for specialty chemicals, including high-value and niche products, drives the need for reliable and specialized transportation services, such as deep sea chemical tanker shipping, to meet customer requirements. As a result, the Deep Sea Shipments segment experiences rapid growth in the Chemical Tanker Shipping Market, reflecting its pivotal role in facilitating global chemical trade and supply chain logistics across vast maritime routes.

Chemical Tanker Shipping Market Share Analysis: IMO II Cargo Segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

Among the delineated segments based on cargo type, IMO II Cargo is the fastest-growing segment in the Chemical Tanker Shipping Market, driven by diverse compelling factors. IMO II cargoes consist of moderate hazard chemicals that require special handling and transportation precautions due to their potential to cause pollution or harm if released into the environment. The rapid growth of IMO II cargo shipments is driven by the increasing demand for specialty chemicals and intermediates, including petrochemicals, solvents, and industrial chemicals, drives the need for specialized transportation services to ensure safe and compliant handling of these products. Additionally, regulatory requirements and industry standards mandate stringent safety and environmental protection measures for the transportation of hazardous chemicals, leading to the preference for dedicated chemical tankers equipped with advanced containment, monitoring, and emergency response systems. In addition, the globalization of chemical supply chains and the expansion of chemical manufacturing capacities in emerging markets fuel the demand for reliable and efficient transportation solutions for IMO II cargoes across international trade routes. Further, advancements in vessel design, technology, and operational practices enhance the safety, efficiency, and sustainability of IMO II cargo shipments, further driving market growth. As chemical producers and shippers prioritize safety, compliance, and reliability in transporting hazardous chemicals, the IMO II Cargo segment experiences rapid growth in the Chemical Tanker Shipping Market, reflecting its critical role in ensuring the safe and sustainable movement of chemical products worldwide.

Chemical Tanker Shipping Market Report Segmentation

By Product

Organic Chemicals

Inorganic Chemicals

Vegetable Oils and Fats

Others

By Shipment

Inland

Coastal

Deep Sea

By Cargo Type

IMO I

IMO II

IMO III

By Coating

Stainless Steel Tanks

Epoxy Coated Tankers

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Chemical Tanker Shipping Companies Profiled in the Market Study

Alaska Tanker Company LLC

Algoma Central Corp

Düzgit Grup A.Åž.

Groupe Desgagnés Inc

Iino Kaiun Kaisha Ltd

Maersk Tankers

MOL Nordic Tankers A/S

Navig8 Chemical Tankers Inc

Navios Maritime Acquisition Corp

Odfjell SE

Petronav Caspian Sea Marine Services Private Ltd

Stena Bulk AB

Stolt-Nielsen Ltd

Uni-Tankers A/S

UPT United Product Tankers GmbH & Co. KG

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Chemical Tanker Shipping Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Chemical Tanker Shipping Market Size Outlook, $ Million, 2021 to 2030

3.2 Chemical Tanker Shipping Market Outlook by Type, $ Million, 2021 to 2030

3.3 Chemical Tanker Shipping Market Outlook by Product, $ Million, 2021 to 2030

3.4 Chemical Tanker Shipping Market Outlook by Application, $ Million, 2021 to 2030

3.5 Chemical Tanker Shipping Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Chemical Tanker Shipping Industry

4.2 Key Market Trends in Chemical Tanker Shipping Industry

4.3 Potential Opportunities in Chemical Tanker Shipping Industry

4.4 Key Challenges in Chemical Tanker Shipping Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Chemical Tanker Shipping Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Chemical Tanker Shipping Market Outlook by Segments

7.1 Chemical Tanker Shipping Market Outlook by Segments, $ Million, 2021- 2030

By Product

Organic Chemicals

Inorganic Chemicals

Vegetable Oils and Fats

Others

By Shipment

Inland

Coastal

Deep Sea

By Cargo Type

IMO I

IMO II

IMO III

By Coating

Stainless Steel Tanks

Epoxy Coated Tankers

8 North America Chemical Tanker Shipping Market Analysis and Outlook To 2030

8.1 Introduction to North America Chemical Tanker Shipping Markets in 2024

8.2 North America Chemical Tanker Shipping Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Chemical Tanker Shipping Market size Outlook by Segments, 2021-2030

By Product

Organic Chemicals

Inorganic Chemicals

Vegetable Oils and Fats

Others

By Shipment

Inland

Coastal

Deep Sea

By Cargo Type

IMO I

IMO II

IMO III

By Coating

Stainless Steel Tanks

Epoxy Coated Tankers

9 Europe Chemical Tanker Shipping Market Analysis and Outlook To 2030

9.1 Introduction to Europe Chemical Tanker Shipping Markets in 2024

9.2 Europe Chemical Tanker Shipping Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Chemical Tanker Shipping Market Size Outlook by Segments, 2021-2030

By Product

Organic Chemicals

Inorganic Chemicals

Vegetable Oils and Fats

Others

By Shipment

Inland

Coastal

Deep Sea

By Cargo Type

IMO I

IMO II

IMO III

By Coating

Stainless Steel Tanks

Epoxy Coated Tankers

10 Asia Pacific Chemical Tanker Shipping Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Chemical Tanker Shipping Markets in 2024

10.2 Asia Pacific Chemical Tanker Shipping Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Chemical Tanker Shipping Market size Outlook by Segments, 2021-2030

By Product

Organic Chemicals

Inorganic Chemicals

Vegetable Oils and Fats

Others

By Shipment

Inland

Coastal

Deep Sea

By Cargo Type

IMO I

IMO II

IMO III

By Coating

Stainless Steel Tanks

Epoxy Coated Tankers

11 South America Chemical Tanker Shipping Market Analysis and Outlook To 2030

11.1 Introduction to South America Chemical Tanker Shipping Markets in 2024

11.2 South America Chemical Tanker Shipping Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Chemical Tanker Shipping Market size Outlook by Segments, 2021-2030

By Product

Organic Chemicals

Inorganic Chemicals

Vegetable Oils and Fats

Others

By Shipment

Inland

Coastal

Deep Sea

By Cargo Type

IMO I

IMO II

IMO III

By Coating

Stainless Steel Tanks

Epoxy Coated Tankers

12 Middle East and Africa Chemical Tanker Shipping Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Chemical Tanker Shipping Markets in 2024

12.2 Middle East and Africa Chemical Tanker Shipping Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Chemical Tanker Shipping Market size Outlook by Segments, 2021-2030

By Product

Organic Chemicals

Inorganic Chemicals

Vegetable Oils and Fats

Others

By Shipment

Inland

Coastal

Deep Sea

By Cargo Type

IMO I

IMO II

IMO III

By Coating

Stainless Steel Tanks

Epoxy Coated Tankers

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Alaska Tanker Company LLC

Algoma Central Corp

Düzgit Grup A.Åž.

Groupe Desgagnés Inc

Iino Kaiun Kaisha Ltd

Maersk Tankers

MOL Nordic Tankers A/S

Navig8 Chemical Tankers Inc

Navios Maritime Acquisition Corp

Odfjell SE

Petronav Caspian Sea Marine Services Private Ltd

Stena Bulk AB

Stolt-Nielsen Ltd

Uni-Tankers A/S

UPT United Product Tankers GmbH & Co. KG

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Product

Organic Chemicals

Inorganic Chemicals

Vegetable Oils and Fats

Others

By Shipment

Inland

Coastal

Deep Sea

By Cargo Type

IMO I

IMO II

IMO III

By Coating

Stainless Steel Tanks

Epoxy Coated Tankers

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)