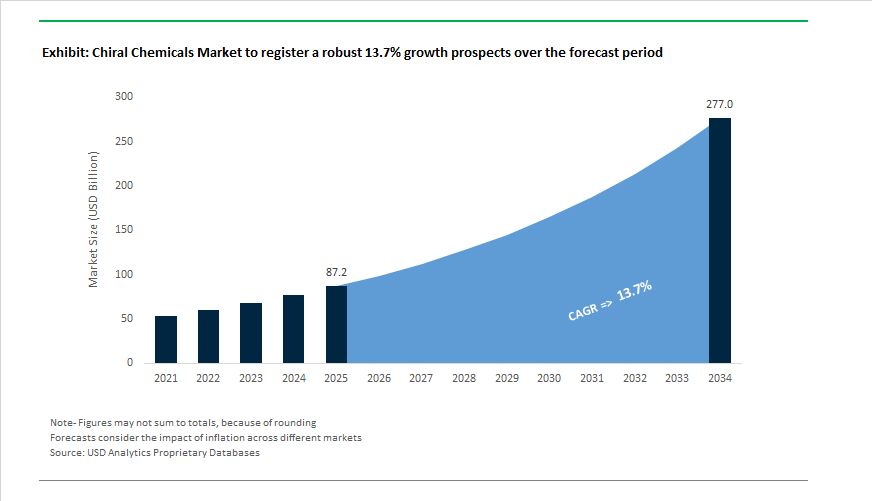

Chiral Chemicals Market Outlook 2025–2034: $87.2 Billion to $276.9 Billion at 13.7% CAGR Fueled by Asymmetric Synthesis and AI-Enabled Drug Development

The global Chiral Chemicals Market is projected to expand from $87.2 billion in 2025 to $276.9 billion by 2034, registering a robust CAGR of 13.7%. This accelerated growth trajectory reflects structural shifts in pharmaceutical R&D, where enantiomeric purity, stereoselective catalysis, and advanced asymmetric synthesis have become central to drug efficacy and regulatory compliance. As over half of new small-molecule APIs exhibit chirality, demand for enantiopure intermediates, chiral catalysts, and high-precision analytical tools continues to rise across oncology, CNS, antiviral, and cardiovascular therapeutic pipelines.

Regulatory tightening is materially influencing procurement strategies. In August 2025, the U.S. FDA introduced updated guidelines requiring more granular documentation of enantiomeric impurities in active pharmaceutical ingredients. These revised chiral purity standards are increasing reliance on high-resolution chiral chromatography, supercritical fluid chromatography (SFC), and tandem mass spectrometry techniques. In February 2025, Bristol Myers Squibb unveiled an advanced SFC-MS/MS methodology to improve enantiomer detection in complex biological matrices during clinical development. Complementing analytical innovation, Daicel Chiral Technologies launched ultra-fast SFC columns in 2024, enabling higher throughput enantiomer separation for both analytical and preparative-scale applications. These developments are reinforcing chromatography equipment, chiral stationary phases, and analytical services as critical revenue pillars within the chiral chemicals ecosystem.

Strategic consolidation and AI integration are redefining competitive positioning. In June 2025, XtalPi acquired Liverpool ChiroChem, integrating automated chiral synthesis capabilities into AI-driven drug discovery platforms to accelerate enantiopure building block identification. Solvias introduced AI-assisted chiral resolution software in 2024, reducing early-stage development time for racemic mixture separation by up to 25% through predictive ligand and solvent modeling. In February 2025, Ecovyst partnered with ChiralVision to advance industrial-scale biocatalysis via enzyme immobilization technologies that enhance catalyst stability and reuse. Earlier, in early 2024, Codexis and Ginkgo Bioworks announced collaboration to engineer next-generation biocatalysts, leveraging cell programming platforms to reduce reaction steps and lower environmental intensity in asymmetric synthesis workflows. These initiatives indicate a structural convergence between computational chemistry, synthetic biology, and scalable manufacturing.

Capacity expansion and catalytic breakthroughs are broadening application scope beyond traditional pharmaceutical intermediates. Lonza inaugurated an advanced kilo lab in Switzerland in 2024, dedicated to cGMP production of complex chiral intermediates using integrated in silico route prediction and high-throughput screening. Evonik introduced a sustainable organocatalyst portfolio between late 2023 and 2024, optimized for continuous flow asymmetric synthesis aligned with green chemistry principles. In April 2025, research led by Fraser Stoddart demonstrated mechanically tunable chiral catenanes capable of reversible chirality control, signaling potential in smart materials and drug delivery platforms. In January 2026, researchers at the University of Science and Technology of China reported a palladium-catalyzed cascade cyclization process achieving high diastereo- and enantioselectivity for nitrogen-bridged ring systems critical to drug discovery. Simultaneously, Tanfac Industries approved a ₹495 crore investment in January 2026 to expand fluorinated chiral intermediate capacity in India, targeting 20,000 tonnes annually by November 2026. These combined advancements position the chiral chemicals market as one of the fastest-growing segments within specialty chemicals and pharmaceutical manufacturing through 2034.

Chiral Chemicals Market Trends and Drivers

Rapid Commercial Shift Toward Biocatalysis and Asymmetric Synthesis Driven by Waste Reduction and API Economics

The global chiral chemicals market is undergoing a fundamental transformation as manufacturers pivot away from traditional chiral resolution systems—processes historically associated with 50% molecular waste generation and high solvent consumption. Instead, the commercial focus is moving toward atom-efficient biocatalysis and asymmetric catalytic methods, enabling pharmaceutical firms to reduce cost-per-kg and shorten time-to-commercialization for high-value APIs.

In 2024, asymmetric synthesis dominated global production with over 30,000 metric tons manufactured, supported by 18,000 metric tons produced via biocatalysis. More than 120 companies have now integrated microbial fermentation and enzyme-catalyzed solutions into their enantioselective synthesis workflows, signaling widespread industrial scalability.

Strategic partnerships are becoming the primary accelerator of capability expansion. From 2024 to 2025, BASF SE and Hovione significantly deepened investments in enzymatic synthesis, while Codexis and Ginkgo Bioworks initiated a landmark collaboration to co-develop next-generation biocatalysts aimed at reducing reaction steps, improving yield, and decreasing environmental footprint. These ecosystem partnerships are positioning biocatalysis not only as a sustainability strategy, but as a core ROI lever for blockbuster pharmaceutical APIs entering late-stage trials.

Surge in Demand for Ultra-High-Purity Chiral Building Blocks for ADCs and mRNA Payload Manufacturing

As pharmaceutical pipelines move toward precision-focused oncology therapies, demand for chiral linkers and payload intermediates with ultra-high enantiomeric excess (ee) is accelerating. This has transitioned the chiral chemicals market into a mission-critical segment of the antibody drug conjugates (ADC) supply chain.

As of June 2025, 15 ADC therapies are approved for 16 indications, while more than 370 ADC candidates are in clinical trials—creating multibillion-dollar material flows for cleavable chiral linkers. The cleavable linker segment, dependent on complex chiral chemistry for selective payload release, is projected to command 60% of ADC-related material share in 2025.

Strategic capital deployment underscores market confidence. Pfizer’s multi-million-dollar expansion at its Kalamazoo site (August 2023) and Johnson & Johnson’s $2 billion acquisition of Ambrx Biopharma (2024) highlight how big pharma is vertically securing supply to avoid bottlenecks in oncology material availability. These investments signal that controlling chiral intermediates is becoming a competitive differentiator in clinical success rates and time-to-market acceleration.

Commercial-Scale Demand for Chiral Ligands in Next-Generation Circularly Polarized OLED (CP-OLED) Emitters

Beyond pharmaceuticals, a compelling commercial opportunity is emerging in the electronics sector—specifically CP-OLED displays, where chiral chemicals are required to produce next-generation circularly polarized light emitters. Traditional OLED systems lose ~50% of energy through polarizers, creating a strong incentive for materials innovation.

Groundbreaking research from Nature Photonics (November 2025) led by the University of Oxford demonstrated electrically switchable OLEDs emitting left-/right-handed circularly polarized light using organic polymer materials with chiral twisted structures.

In January 2025, studies on chiral perovskite quantum dots achieved external quantum efficiencies (EQE) of up to 16.8%, enabled through engineered high-purity chiral ligand-exchange chemistries. This opens a lucrative high-margin segment for chemical producers who can supply patent-protected ligands to consumer electronics, automotive HUD displays, and EV infotainment systems—unlocking a new non-pharmaceutical demand pillar for the chiral chemicals industry.

Rising Adoption of Enantiopure Agrochemicals to Support EU and Asia Regulatory Compliance

Regulatory change is unlocking multi-year opportunity pipelines in the agricultural chemicals market. Increasingly stringent residue, toxicity, and ecological benchmarks are forcing pesticide manufacturers to shift from racemic mixtures to single-isomer, enantiopure formulations, minimizing environmental impact while improving precision targeting.

Between 2023 and 2024, global investment of over $870 million flowed into R&D for enantiopure pesticides, expected to deliver 700+ new chiral agrochemical variants by 2026. Major players such as BASF and Evonik are prioritizing selective herbicides that target weeds without damaging non-target plant species or soil ecosystems.

Under the EU’s revised CLP Regulation (December 2024), new classification and labeling rules will legally apply beginning July 2026, accelerating commercial de-selection of racemic pesticides. Only biologically active enantiomers are expected to gain approval under tightened residue control policies.

Competitive Landscape of the Chiral Chemicals Market

The Chiral Chemicals Market is shaped by vertically integrated chemical majors and highly specialized CDMOs advancing asymmetric synthesis, enantioselective purification, and sustainable chiral manufacturing. Market leaders are investing heavily in Zero Product Carbon Footprint (ZeroPCF) production, AI-enabled enantioselectivity prediction, continuous flow chemistry, and biocatalysis to support pharmaceutical intermediates, crop protection actives, and high-purity APIs. Competitive differentiation increasingly centers on optical purity above 99.5%, lab-to-production integration, circular catalyst recovery, and global CDMO networks. With rising demand for single-enantiomer drugs and ESG-compliant manufacturing, the Competitive Landscape continues to evolve toward greener feedstocks, scalable chiral platforms, and advanced molecular characterization.

BASF drives ZeroPCF chiral intermediates through Verbund-integrated synthesis

BASF remains a dominant force in chiral chemicals via its Intermediates division and ChiPros® portfolio of high-purity chiral amines, alcohols, and acids for pharmaceuticals and crop protection. In September 2024, BASF launched its “Winning Ways” strategy, prioritizing Green Transformation by shifting chiral production toward ZeroPCF using renewable raw materials through biomass balance. The company recently expanded ChiPros® with naphthylethylamines and methoxyphenyl-ethylamines exceeding 99.5% optical purity. BASF’s Verbund integration enables seamless access to acetylene and chlorine feedstocks, strengthening supply reliability and cost efficiency across complex chiral synthesis chains.

Daicel dominates chiral separations with global CSP leadership and CDMO scale

Daicel, through Daicel Chiral Technologies, leads the global market for enantioselective chromatography and chiral separation. The company owns the world’s largest portfolio of Chiral Stationary Phases, including CHIRALPAK® and CHIRALCEL®, widely used from early drug discovery to commercial purification. Daicel operates a specialized CDMO network spanning the US, Europe, India, and China, supporting regional pharmaceutical ecosystems. As of 2026, Daicel expanded partnerships with academic institutions to integrate needle-free injection technology with chiral drug delivery platforms, reinforcing its position at the intersection of separation science and advanced therapeutics.

Merck integrates AI-driven chiral synthesis with lab-to-production workflows

Through its Life Science business MilliporeSigma, Merck delivers one of the most comprehensive toolsets for chiral synthesis and purification worldwide. The company invests approximately €2.7 to €3.0 billion annually in R&D and Capex, targeting high-margin chromatography resins and consumables. Merck now applies AI and machine learning to predict enantioselectivity and optimize catalyst selection, reducing time-to-batch by up to 30%. Under its Level Up program, over €1.5 billion has been deployed to expand single-use and filtration capacity across France, Ireland, and the US, enabling a fully integrated lab-to-production chiral workflow.

Solvias advances asymmetric catalysis for next-generation chiral therapeutics

Solvias is a specialized CDMO recognized for asymmetric catalysis and proprietary chiral ligand technologies. The company offers high-performance catalysts supporting diverse synthesis pathways for complex APIs. In late 2025, Solvias achieved cGMP readiness at its 50,000 sq. ft. Center of Excellence in North Carolina, targeting biologics and chiral drug release testing. In 2026, Solvias began release testing for the world’s first CRISPR-based gene-editing therapies, highlighting its move into ultra-complex molecular characterization. Growth in solid-state chemistry services further strengthens its ability to optimize physical stability of chiral active pharmaceutical ingredients.

Cambrex scales complex chiral APIs through continuous flow chemistry

Cambrex is a global CDMO specializing in small-molecule drug substances and complex chiral intermediates, producing over 90 generic APIs via batch and continuous flow synthesis. The integration of Snapdragon Chemistry significantly enhanced Cambrex’s continuous flow capabilities, enabling safer and more scalable chiral reactions. Recent innovations include telescoped hybrid batch-flow synthesis for benzofurans, reducing waste while improving process safety. Cambrex also brings deep expertise in Highly Potent APIs and controlled substances, where chiral purity is a critical regulatory requirement, positioning the company as a preferred partner for late-stage pharmaceutical manufacturing.

Johnson Matthey pioneers circular catalysis and biocatalytic chiral transformations

Johnson Matthey leads the high-end catalysis segment of the chiral chemicals market, leveraging global expertise in Platinum Group Metal catalysis for asymmetric hydrogenation. The company is advancing Circularity in Chemicals by supplying catalysts alongside closed-loop recovery systems for precious metals. As of 2026, Johnson Matthey expanded its biocatalysis platform, deploying engineered enzymes to perform chiral transformations under mild aqueous conditions aligned with ESG targets. Its integrated model combines catalyst supply with process development services, helping pharmaceutical clients scale from gram-level R&D to multi-ton commercial production.

Chiral Chemicals Market Share and Segmentation Insights

Technology Landscape: Asymmetric Synthesis Anchors Production as Biocatalysis Gains Rapid Industrial Traction

Asymmetric synthesis commands 40% of the Chiral Chemicals Market in 2025, reinforcing its position as the primary manufacturing route for single-enantiomer pharmaceutical intermediates. Continuous innovation in chiral ligands and metal-based catalysts has significantly improved reaction efficiency, making asymmetric synthesis highly cost-effective for complex APIs and fine chemicals. Biocatalytic processes now represent the second-largest segment, accelerating adoption as pharmaceutical manufacturers prioritize green chemistry, high stereoselectivity, and lower waste generation. Engineered enzymes such as ketoreductases and transaminases are increasingly replacing heavy-metal catalysis, simplifying downstream purification. Traditional resolution methods continue to lose relative share due to inherent yield losses and material inefficiencies, remaining relevant only for select racemic compounds. Analytical and separation technologies hold the smallest production share but play a critical enabling role through chiral HPLC and SFC, supporting quality control, R&D purification, and regulatory compliance for high-value drug candidates.

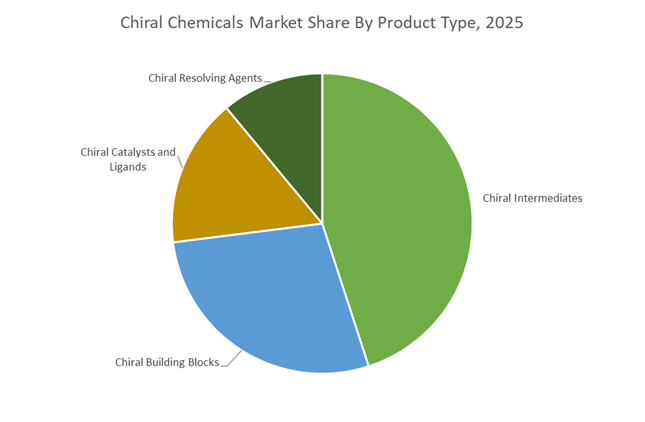

Product Segmentation: Chiral Intermediates Dominate While Catalysts Drive High-Value Innovation

Chiral intermediates account for 45% of total market revenue, reflecting strong demand from pharmaceutical companies developing therapies for cardiovascular disease, diabetes, and oncology. The outsourcing of advanced intermediate synthesis to CDMOs continues to expand this segment. Chiral building blocks form the foundational layer of synthesis pipelines, supporting pharma, agrochemicals, and flavors and fragrances, driven by large-volume consumption of amino alcohols, epoxides, and lactic acid derivatives. Chiral catalysts and ligands represent a high-value, low-volume category, where innovations in phosphoramidites and BINAP-type ligands unlock new asymmetric reactions despite premium pricing per kilogram. Chiral resolving agents remain the smallest segment, aligned with the decline of traditional resolution routes, and are increasingly confined to niche separations or backup purification strategies when asymmetric or biocatalytic synthesis proves impractical.

United States Chiral Chemicals Market: FDA-Driven Stereoisomeric Purity and Advanced CDMO Expansion

The United States Chiral Chemicals Market remains the global benchmark for enantiopure active pharmaceutical ingredient production, driven by stringent regulatory oversight and complex small-molecule drug pipelines. In 2025, the U.S. Food and Drug Administration intensified enforcement of stereoisomeric purity data requirements in New Drug Applications, compelling pharmaceutical manufacturers to implement advanced chiral chromatography, asymmetric synthesis, and enantioselective catalysis from early-stage clinical development. This regulatory rigor is accelerating demand for high-purity chiral intermediates, chiral reagents, and enantiomerically enriched building blocks across oncology and neurological therapeutics.

In February 2026, Lonza announced the full integration of its Advanced Synthesis portfolio, expanding bioconjugate and chiral intermediate capabilities at its Vacaville site. Meanwhile, Johnson & Johnson committed $1 billion toward a new Pennsylvania facility focused on cell therapy and complex molecule manufacturing, increasing structural reliance on chiral amino alcohols and stereochemically pure intermediates. U.S.-based CDMOs are adopting AI-driven predictive modeling for chiral separations, demonstrating 40 to 50% reductions in method development costs. Collaborative ecosystems involving institutions such as Massachusetts Institute of Technology and Stanford University are accelerating commercialization of next-generation chiral catalysts for green chemistry, reinforcing U.S. leadership in the global chiral chemicals market.

China Chiral Chemicals Market: Self-Sufficiency Strategy and Expansion of Biocatalytic Synthesis

China’s Chiral Chemicals Market is undergoing structural transformation from commodity chemical manufacturing to high-value specialty chiral intermediate production. National chemical industry growth plans for 2025 and 2026 prioritize polypropylene and specialty chemical capacity expansion, reducing reliance on imported high-purity feedstocks. Dedicated chiral synthesis lines are expanding rapidly in industrial hubs such as Nantong and Huizhou, supporting the domestic biotechnology boom and scaling production of enantiomerically pure pharmaceutical intermediates.

Chinese manufacturers are aggressively investing in biocatalysis and enzymatic resolution technologies to replace traditional metal-catalyzed asymmetric synthesis, aligning with increasingly strict environmental mandates and green chemistry targets. Recent breakthroughs in domestic chiral stationary phase production for HPLC columns are challenging long-standing Japanese and European dominance in analytical separation technologies. Facing Western tariffs, China is pivoting exports of chiral building blocks toward Southeast Asian pharmaceutical clusters to maintain global trade volumes. Sustained government incentives are encouraging local firms to increase R&D expenditure on single-enantiomer technology by more than 15% annually, strengthening China’s competitiveness in the global fine and specialty chiral chemicals market.

Germany Chiral Chemicals Market: Industrial Biotechnology Leadership and EU Regulatory Alignment

Germany continues to anchor the European Chiral Chemicals Market through its integration of industrial biotechnology and sustainable asymmetric synthesis. The Federal Ministry for Economic Affairs and Climate Action is finalizing policy measures to advance the Industrial Bioeconomy strategy, including streamlined regulations for genetic engineering in enzyme-catalyzed chiral synthesis. This framework supports large-scale biocatalytic production of chiral precursors and enantiopure intermediates for pharmaceutical and specialty chemical applications.

In February 2026, Evonik Industries confirmed a strategic pivot toward high-margin specialty chemicals and customized chiral solutions, reinforcing Germany’s role in precision chemistry. Despite softness in commodity chemicals, national pharmaceutical output increased by 3% in 2025, sustaining demand for high-purity chiral reagents. Initiatives led by CLIB - Cluster Industrial Biotechnology, including the ReCO2NWert project, leverage C1 feedstocks for sustainable chiral precursor production. Germany also plays a central role in implementing the EU One Substance One Assessment framework effective January 2026, streamlining safety evaluations for complex chiral molecules and strengthening regulatory harmonization across Europe. Increasing adoption of membrane-based chiral separations further enhances solvent efficiency and reduces energy intensity in large-scale production.

Switzerland Chiral Chemicals Market: Precision CDMO Dominance and Continuous Flow Asymmetric Synthesis

Switzerland commands a premium position in the global Chiral Chemicals Market through its dense cluster of advanced Contract Development and Manufacturing Organizations specializing in multi-step stereoselective synthesis. In January 2026, Lonza reported record 2025 sales of CHF 6.5 billion, with its Small Molecules and Advanced Synthesis divisions delivering margin expansion driven by demand for complex chiral APIs and high-purity intermediates. Swiss firms are increasingly adopting a One-Stop-Shop CDMO model, integrating chiral drug substance and drug product services to guarantee end-to-end stereochemical control.

Extensive deployment of continuous flow chemistry platforms for asymmetric hydrogenation enhances scalability and safety when handling volatile chiral intermediates. Leading Swiss companies achieved approximately 50% reductions in greenhouse gas and waste intensity in 2025 relative to 2018 baselines, largely through enzymatic chiral process optimization. Capital expenditure averaging nearly 20% of annual sales is directed toward specialized modalities that require ultra-high-purity chiral building blocks, reinforcing Switzerland’s leadership in high-value pharmaceutical chiral synthesis.

India Chiral Chemicals Market: Generic-Plus Strategy and Asymmetric Catalysis Expansion

India’s Chiral Chemicals Market is transitioning from volume-driven generic drug production to higher-value chiral intermediate and single-enantiomer manufacturing. Under India Chem 2024 and 2025 initiatives, the Ministry of Chemicals and Fertilizers designated the chemical sector as a strategic priority, promoting structural reforms to enhance fine chemistry R&D and technical workforce training. As of 2024, the Indian pharmaceutical industry attracted more than $22 billion in cumulative foreign direct investment, increasingly directed toward facilities specializing in chiral switching and enantioselective synthesis.

Domestic manufacturers are expanding asymmetric catalysis capabilities to reformulate racemic generics into active single-enantiomer drugs, improving therapeutic efficacy and regulatory acceptance in export markets. Rapid adoption of chiral HPLC systems is enabling Indian firms to meet heightened impurity profiling standards imposed by global regulators. With the national chemical industry targeting $300 billion in output by 2030, specialty chiral chemicals are positioned as a central growth driver within the Advantage Bharat industrial expansion strategy.

Japan Chiral Chemicals Market: Global Leadership in Chiral Chromatography and Analytical Innovation

Japan remains the dominant force in the global chiral chromatography segment, particularly in chiral stationary phase and HPLC column technologies. Japanese and European manufacturers collectively account for more than 75% of global revenue in the chiral HPLC column market as of 2025, reflecting sustained innovation and analytical precision leadership.

Japanese firms are advancing hybrid cyclodextrin-based stationary phases that deliver superior separation performance for polar chiral compounds, addressing long-standing challenges in pharmaceutical enantiomeric resolution. By 2026, integration of robotics and AI with Japanese chiral HPLC platforms reduced column screening timelines from weeks to days, accelerating drug development cycles. Manufacturers are also engineering stationary phases tailored for large peptide therapeutics, supporting a biologics market projected to exceed $75 billion by 2027. Beyond pharmaceuticals, Japan’s precision chiral chemicals are expanding into high-value flavors and fragrances, where enantiomer-specific synthesis enables differentiated olfactory profiles for premium consumer goods, reinforcing Japan’s technological dominance within the global chiral chemicals market.

Chiral Chemicals Market Report Scope

Chiral Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$87.2 Billion

|

|

Market Size (2034)

|

$276.9 Billion

|

|

Market Growth Rate

|

13.7%

|

|

Segments

|

By Technology (Traditional Resolution Methods, Asymmetric Synthesis, Biocatalytic Processes, Analytical and Separation Technologies), By Application (Pharmaceuticals, Agrochemicals, Flavors and Fragrances, Specialty Materials), By Product Type (Chiral Building Blocks, Chiral Catalysts and Ligands, Chiral Resolving Agents, Chiral Intermediates)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Johnson Matthey Plc, Daicel Corporation, Merck KGaA, Evonik Industries AG, Solvias AG, Codexis, Inc., W. R. Grace & Co., DuPont de Nemours, Inc., Symeres B.V., Chiracon GmbH, Kaival Chemicals Pvt. Ltd., Agilent Technologies, Inc., Takasago International Corporation, Strem Chemicals, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Chiral Chemicals Market Segmentation

By Technology

- Traditional Resolution Methods

- Asymmetric Synthesis

- Biocatalytic Processes

- Analytical and Separation Technologies

By Application

- Pharmaceuticals

- Agrochemicals

- Flavors and Fragrances

- Specialty Materials

By Product Type

- Chiral Building Blocks

- Chiral Catalysts and Ligands

- Chiral Resolving Agents

- Chiral Intermediates

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Chiral Chemicals Industry

- BASF SE

- Johnson Matthey Plc

- Daicel Corporation

- Merck KGaA

- Evonik Industries AG

- Solvias AG

- Codexis, Inc.

- W. R. Grace & Co.

- DuPont de Nemours, Inc.

- Symeres B.V.

- Chiracon GmbH

- Kaival Chemicals Pvt. Ltd.

- Agilent Technologies, Inc.

- Takasago International Corporation

- Strem Chemicals, Inc.

*- List not Exhaustive