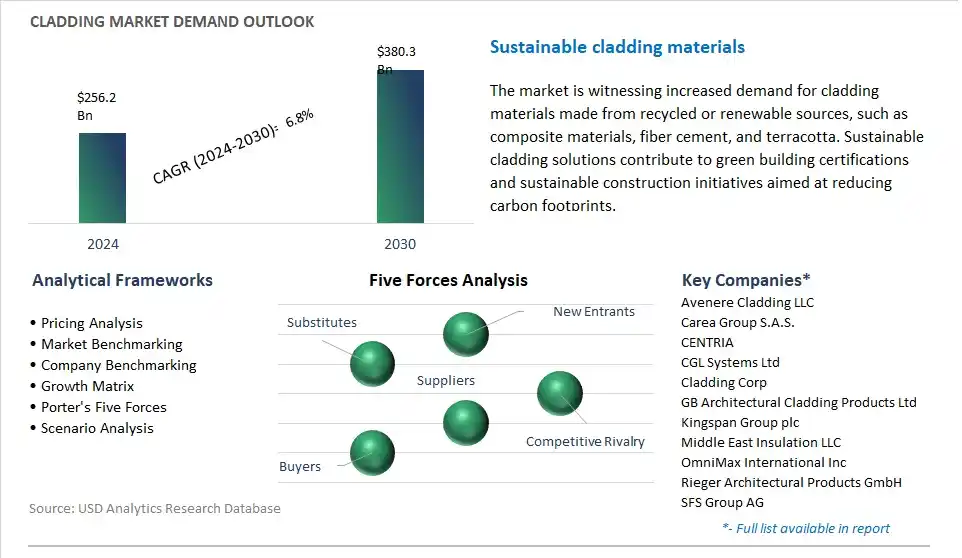

The global Cladding Market size stood at $256.2 Billion in 2024. Further, over the forecast period to 2030, the industry is poised to generate a revenue of $380.3 Billion in 2030, registering a growth rate (CAGR) of 6.8%.

Cladding Market study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments- By Product (Steel, Aluminum, Composite Materials, Fiber Cement, Terracotta, Ceramic, Others), By Application (Residential, Industrial, Commercial, Office, Institutional).

An Introduction to Cladding Market

The Cladding Market is experiencing steady growth is propelled by a combination of factors including urbanization, infrastructure development, and architectural trends favoring aesthetically appealing and durable building exteriors. Cladding materials, ranging from traditional options like brick and stone to modern alternatives such as metal, composite panels, and fiber cement, play a crucial role in enhancing the visual appeal, weather resistance, and thermal performance of structures. With a focus on sustainability and energy efficiency, there's a growing demand for cladding solutions that offer insulation properties, thereby reducing energy consumption and environmental impact. In addition, technological advancements have led to the development of innovative cladding systems that offer ease of installation, maintenance, and customization, catering to the evolving needs of architects, developers, and building owners.

Cladding Competitive Landscape

Avenere Cladding LLC, Carea Group S.A.S., CENTRIA, CGL Systems Ltd, Cladding Corp, GB Architectural Cladding Products Ltd, Kingspan Group plc, Middle East Insulation LLC, OmniMax International Inc, Rieger Architectural Products GmbH, SFS Group AG, Shildan Group, Trespa International B.V.

Cladding Market Dynamics

Market Trend: Rise of Innovative and Sustainable Materials in the Cladding Market

Architects, designers, and construction companies are increasingly incorporating materials such as fiber cement, metal composites, terracotta, and engineered wood in cladding systems. These materials offer a combination of aesthetic appeal, durability, weather resistance, and eco-friendly characteristics, aligning with the growing demand for sustainable building solutions. This trend reflects the industry's shift towards environmentally conscious practices and the desire for visually striking yet functional cladding options.

Market Driver: Urbanization and Modernization Projects Driving Cladding Demand

As cities expand and undergo redevelopment, there is a heightened demand for cladding materials that enhance building aesthetics, provide thermal insulation, and offer protection against environmental elements. The construction of commercial buildings, residential complexes, offices, and public facilities drives the need for diverse cladding solutions, ranging from traditional materials like brick and stone to contemporary options such as glass, metal, and composite panels.

Market Opportunity: Emphasis on Energy Efficiency and Architectural Design Spurs Cladding Market Opportunities

The Cladding market presents significant opportunities driven by the emphasis on energy efficiency and architectural design in construction projects. Energy-efficient cladding systems, including insulated panels and ventilated facades, are in demand to improve building performance and meet sustainability standards. In addition, the integration of advanced technologies such as photovoltaic cladding for solar energy generation and digital printing techniques for customized designs enhances the market's potential. With architects and developers prioritizing both functionality and aesthetics, the Cladding market offers diverse opportunities for manufacturers and suppliers of innovative cladding solutions.

Market Share Analysis: Composite Materials is the Largest Segment in the Cladding Market

The Composite Materials segment is the largest within the Cladding Market due to several key factors. Composite materials offer a combination of durability, versatility, and aesthetic appeal, making them a preferred choice for cladding applications in both residential and commercial buildings. Composite cladding typically consists of a blend of materials such as wood fibers, plastic resins, and additives, providing benefits such as weather resistance, low maintenance requirements, and design flexibility. In addition, composite materials can mimic the look of natural materials like wood or stone while offering enhanced durability and performance, making them popular among architects, builders, and property owners. The demand for sustainable and eco-friendly building materials also contributes to the dominance of composite materials in the Cladding Market as they often incorporate recycled content and have lower environmental impact compared to traditional cladding materials.

Market Share Analysis: Commercial and Office Applications is Poised to Register Fastest Growth in the Cladding Market

The Commercial and Office Applications segment is the fastest-growing within the Cladding Market due to several key factors. With rapid urbanization, infrastructure development, and commercial expansions globally, there is a significant demand for cladding solutions in commercial buildings, office complexes, and institutional facilities. Cladding plays a crucial role in enhancing the aesthetic appeal, functionality, and energy efficiency of commercial structures, contributing to a positive and modern architectural appearance. In addition, the trend towards sustainable and energy-efficient building designs drives the adoption of cladding materials that offer thermal insulation, weather protection, and environmental sustainability certifications. The growing focus on creating attractive and environmentally responsible commercial spaces fuels the rapid growth of the Commercial and Office Applications segment in the Cladding Market.

Market Ecosystem of Cladding industry

The cladding industry is characterized by a well-defined value chain encompassing material suppliers, panel fabrication, design and engineering, installation, and maintenance stages. Material suppliers like ArcelorMittal and Graniti Fiandre provide raw materials such as metal, stone, and glass for cladding panels, which are then transformed by companies like Kingspan Group and Cosentino Group into pre-fabricated cladding panels with desired finishes and properties, adding value by enhancing durability and aesthetics. Architectural design firms like Perkins+Will and engineering companies such as WSP play a crucial role in developing design and engineering specifications for cladding systems, ensuring functionality and structural integrity throughout the building envelope.

Following design and engineering, cladding installation contractors and specialist subcontractors carry out the installation of cladding systems, ensuring adherence to design specifications and regulatory standards. This stage is pivotal in bringing the design concepts to life and ensuring the cladding system's proper integration with the building structure. Finally, maintenance and inspection companies like WSP and Bureau Veritas conduct periodic inspections and provide maintenance services to preserve the cladding system's performance and integrity over time, contributing to long-term sustainability and functionality.

Geographical Analysis: The US Cladding Market Size to generate $105 Billion in 2030

The US Cladding Market offers a variety of products including steel, aluminum, composite materials, fiber cement, terracotta, ceramic, and others, catering to applications in residential, industrial, commercial, office, and institutional buildings. Cladding serves both aesthetic and functional purposes, providing weather protection, thermal insulation, and architectural enhancement. With a focus on sustainability and design versatility, materials like composite and fiber cement cladding are gaining popularity. The market's growth is driven by construction activities, renovation projects, and the emphasis on energy-efficient building envelopes in the US construction industry.

TABLE OF CONTENTS

1 Introduction to 2024 Cladding Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Cladding Market Size Outlook, $ Million, 2021 to 2030

3.2 Cladding Market Outlook by Type, $ Million, 2021 to 2030

3.3 Cladding Market Outlook by Product, $ Million, 2021 to 2030

3.4 Cladding Market Outlook by Application, $ Million, 2021 to 2030

3.5 Cladding Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Cladding Industry

4.2 Key Market Trends in Cladding Industry

4.3 Potential Opportunities in Cladding Industry

4.4 Key Challenges in Cladding Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Cladding Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Cladding Market Outlook by Segments

7.1 Cladding Market Outlook by Segments, $ Million, 2021- 2030

By Product

Steel

Aluminum

Composite Materials

Fiber Cement

Terracotta

Ceramic

Others

By Application

Residential

Industrial

Commercial

Office

Institutional

8 North America Cladding Market Analysis and Outlook To 2030

8.1 Introduction to North America Cladding Markets in 2024

8.2 North America Cladding Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Cladding Market size Outlook by Segments, 2021-2030

By Product

Steel

Aluminum

Composite Materials

Fiber Cement

Terracotta

Ceramic

Others

By Application

Residential

Industrial

Commercial

Office

Institutional

9 Europe Cladding Market Analysis and Outlook To 2030

9.1 Introduction to Europe Cladding Markets in 2024

9.2 Europe Cladding Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Cladding Market Size Outlook by Segments, 2021-2030

By Product

Steel

Aluminum

Composite Materials

Fiber Cement

Terracotta

Ceramic

Others

By Application

Residential

Industrial

Commercial

Office

Institutional

10 Asia Pacific Cladding Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Cladding Markets in 2024

10.2 Asia Pacific Cladding Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Cladding Market size Outlook by Segments, 2021-2030

By Product

Steel

Aluminum

Composite Materials

Fiber Cement

Terracotta

Ceramic

Others

By Application

Residential

Industrial

Commercial

Office

Institutional

11 South America Cladding Market Analysis and Outlook To 2030

11.1 Introduction to South America Cladding Markets in 2024

11.2 South America Cladding Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Cladding Market size Outlook by Segments, 2021-2030

By Product

Steel

Aluminum

Composite Materials

Fiber Cement

Terracotta

Ceramic

Others

By Application

Residential

Industrial

Commercial

Office

Institutional

12 Middle East and Africa Cladding Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Cladding Markets in 2024

12.2 Middle East and Africa Cladding Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Cladding Market size Outlook by Segments, 2021-2030

By Product

Steel

Aluminum

Composite Materials

Fiber Cement

Terracotta

Ceramic

Others

By Application

Residential

Industrial

Commercial

Office

Institutional

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

List of Companies

Avenere Cladding LLC

Carea Group S.A.S.

CENTRIA

CGL Systems Ltd

Cladding Corp

GB Architectural Cladding Products Ltd

Kingspan Group plc

Middle East Insulation LLC

OmniMax International Inc

Rieger Architectural Products GmbH

SFS Group AG

Shildan Group

Trespa International B.V.

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise