Coated Abrasives Market Size, Advanced Materials Adoption, and Industrial Demand Acceleration

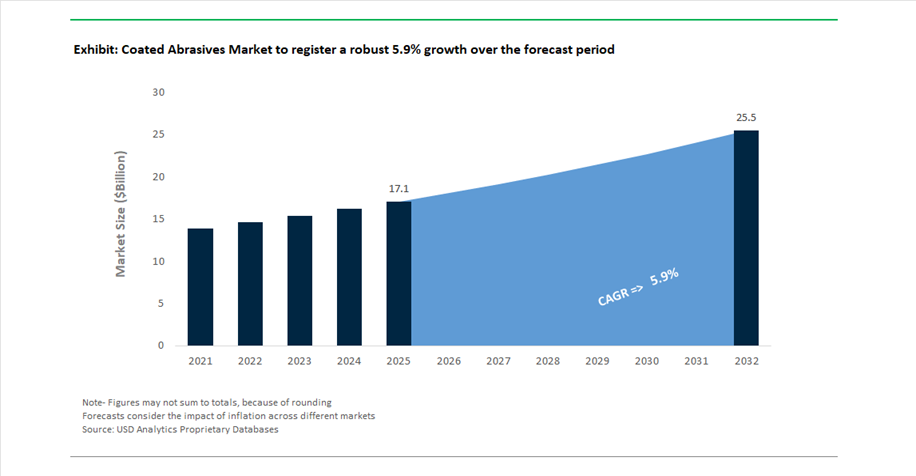

The global coated abrasives market was valued at $17.1 billion in 2025 and is projected to expand at a CAGR of 5.9% between 2025 and 2032, reaching $25.5 billion by 2032. This growth trajectory is underpinned by robust demand from metal fabrication, automotive manufacturing, aerospace, construction, woodworking, and precision engineering industries, where coated abrasives are essential for grinding, polishing, deburring, and surface finishing operations.

The market is experiencing a structural shift toward high-performance abrasive materials, particularly ceramic grains, precision-shaped abrasives, and engineered backing systems, which deliver superior cutting efficiency, durability, and heat resistance. As manufacturing processes become more automated and tolerance-sensitive, there is increasing adoption of abrasives optimized for robotic grinding cells and CNC-based finishing systems, ensuring consistent surface quality and reduced operator dependency.

A key growth catalyst is the rapid expansion of electric vehicle (EV) production and advanced industrial manufacturing, where coated abrasives are used in battery component finishing, e-motor polishing, and lightweight alloy processing. Additionally, industries such as medical devices and turbine manufacturing are demanding abrasives capable of handling superalloys and stainless steel without thermal damage, driving innovation in heat-reduction technologies and grain geometry.

Sustainability and operational efficiency are also reshaping the competitive landscape. Manufacturers are focusing on longer-lasting abrasive products, reduced material waste, and energy-efficient grinding solutions, aligning with broader industrial decarbonization goals. Furthermore, emerging economies in Asia-Pacific, particularly India and Southeast Asia, are becoming key demand centers due to rapid industrialization and infrastructure expansion, strengthening the global consumption base for coated abrasives.

Precision Grain Innovation, Capacity Expansion, and Automation-Driven Applications Transforming the Market

Recent developments in the coated abrasives market highlight a strong emphasis on next-generation grain technology, regional capacity expansion, and application-specific innovation. In March 2026, Saint-Gobain Abrasives expanded its Norton RazorStar® ceramic product line, introducing advanced fiber discs utilizing engineered shaped grain technology. These products are specifically designed for high-pressure grinding in aerospace and automotive applications, offering enhanced material removal rates and extended product life.

Capacity expansion is emerging as a strategic priority in high-growth regions. Carborundum Universal Limited (CUMI) announced the commencement of new commercial production capacity in March 2026, aimed at addressing rising demand across India and Southeast Asia’s manufacturing corridors. This move reflects a broader trend of localized production scaling to support industrial growth and reduce supply chain dependencies in APAC markets.

Technological innovation in grain structure is significantly improving performance benchmarks. 3M’s Cubitron™ 3 series, introduced in early 2024 and continuing its global rollout through 2025, incorporates precision-shaped grain with enhanced molecular bonding, delivering up to 50% faster cutting speeds compared to previous generations. Similarly, VSM Abrasives’ XELERION “dots” technology, unveiled at EuroBLECH 2024, represents a breakthrough in heat management, reducing heat input by up to 70%, making it highly suitable for stainless steel and superalloy finishing in medical and turbine applications.

Application diversification is accelerating, particularly in emerging high-tech sectors. Sia Abrasives, under the Bosch Power Tools cluster, announced a strategic pivot in March 2026 toward EV battery and e-motor finishing applications, targeting double-digit growth in North America and APAC. This reflects the increasing integration of coated abrasives into next-generation manufacturing ecosystems, where precision and consistency are critical.

Industry players are also strengthening product ecosystems and user engagement strategies. Klingspor’s centenary celebration of waterproof sandpaper in January 2026 was accompanied by technical seminars and product launches emphasizing wet-sanding advancements. The company has also invested in a training academy (January 2025) to address skilled labor shortages and ensure optimal product utilization in automated environments. Meanwhile, PFERD TOOLS’ rebranding and R&D expansion in Germany is focused on ergonomic abrasives, reducing vibration and noise in industrial applications, aligning with worker safety and productivity requirements.

Further innovation is visible in integrated system solutions. Saint-Gobain’s Norton vented paint cup system (July 2025) combines abrasives with finishing hardware, enabling streamlined paint preparation workflows for automotive OEMs. Additionally, Klingspor’s Supra generation grinding discs (August 2025) introduce a dual-layer structure balancing aggressiveness and durability, addressing the need for versatile solutions in metal fabrication.

EU REACH Restrictions on Antimony Trioxide Forcing Safer Abrasive Backing Formulations

The coated abrasives industry is undergoing a critical material transition as Antimony Trioxide (Sb₂O₃), widely used as a flame-retardant synergist in abrasive backings, faces phase-out under EU REACH regulations. Classified as a Category 1B carcinogen, Sb₂O₃ is now subject to strict concentration thresholds, with any abrasive product exceeding 0.1% by weight requiring mandatory hazard labeling and controlled disposal protocols as of 2026.

This regulatory pressure is driving a rapid shift toward safer flame-retardant alternatives. Approximately 80% of European abrasive cloth manufacturers have transitioned to halogen-free systems, utilizing materials such as aluminum trihydrate and ammonium polyphosphate. However, this transition has introduced formulation challenges, particularly in maintaining the mechanical integrity of abrasive backings. Current 2026 benchmarks indicate that optimized antimony-free systems retain approximately 95% of the original tensile strength required for high-pressure grinding applications, ensuring continued performance in demanding industrial use cases.

Beyond compliance, the shift is delivering measurable workplace safety benefits. Early 2026 audits indicate a 30% reduction in hazardous airborne particulates within abrasive manufacturing facilities following the removal of antimony-based compounds. This improvement aligns with broader occupational health initiatives and strengthens the case for adopting safer material systems.

Waterborne Phenolic Resins Replacing Solvent Systems to Meet VOC and Energy Targets

The coated abrasives manufacturing process is also being reshaped by the transition from solvent-borne to waterborne phenolic resins in the sizing and make-coat stages. This shift is driven by stringent VOC emission regulations under the EU Industrial Emissions Directive and U.S. EPA Title V standards, which are targeting substantial reductions in industrial air pollution.

Waterborne phenolic systems are delivering significant environmental and operational advantages. Manufacturers adopting these systems report VOC emission reductions ranging from 65% to 80%, effectively eliminating the need for costly emission control technologies such as regenerative thermal oxidizers. In addition, these resins enable lower-temperature processing, reducing drying oven energy consumption by approximately 15% compared to traditional solvent-based systems.

Performance parity has been achieved in modern formulations. Advanced waterborne phenolic resins now match the cross-link density of legacy solvent systems, ensuring minimal grain shedding—typically below 2% of total abrasive grain weight under operational load. This is critical for maintaining consistent cutting performance and product reliability in high-speed sanding and grinding applications.

Shelf-life improvements further enhance their practicality. Stabilization advancements have extended the usable life of waterborne phenolic resins to six months at standard storage conditions, representing a 50% improvement over earlier generations of aqueous systems.

Engineered Abrasive Grain Belts Enhancing Efficiency in Titanium Aerospace Grinding

The increasing use of titanium alloys, particularly Ti-6Al-4V, in aerospace applications is driving demand for high-performance coated abrasives featuring engineered abrasive grains. These advanced grains are designed with controlled shapes and microstructures that enable a self-sharpening effect, essential for managing the high thermal loads associated with titanium machining.

Performance gains are substantial. Engineered abrasive grain belts reduce surface burn on titanium components by approximately 40%, significantly lowering scrap rates in high-value aerospace manufacturing processes. At the same time, these abrasives achieve material removal rates up to three times higher than conventional aluminum oxide systems, enabling manufacturers to reduce grinding cycle times by approximately 25%.

Consistency is another key advantage. Engineered grain technology maintains a stable surface finish throughout the life of the abrasive, with roughness variation limited to ±10% over extended operational cycles. This consistency is critical for meeting the stringent quality requirements of aerospace components.

Energy efficiency improvements further enhance their value. By reducing specific grinding energy by approximately 15%, these systems minimize the risk of metallurgical damage, such as alpha-case formation, which can compromise the structural integrity of titanium components.

Dust-Extraction Abrasives Supporting Safe Processing of Automotive Composite Materials

The automotive industry’s shift toward lightweight composite materials such as carbon fiber and glass fiber reinforced polymers is creating a strong demand for dust-extraction coated abrasives. Sanding these materials generates fine, hazardous dust that poses both health and process risks, necessitating advanced solutions for dust management.

Net-backed and multi-hole film abrasives are delivering high-efficiency dust extraction capabilities, achieving capture rates exceeding 98% when used with vacuum-assisted systems. This represents a significant improvement over traditional paper-backed abrasives, which typically capture only around 60% of airborne dust.

Operational benefits extend to tool longevity and surface quality. By preventing clogging and material buildup, dust-extraction abrasives can last up to four times longer than conventional products. Additionally, the elimination of trapped dust particles between the abrasive and the work surface reduces defects such as “pig-tail” scratches, improving first-pass yield in automotive paint preparation processes by approximately 20%.

From a regulatory perspective, these technologies support compliance with tightening occupational exposure limits for composite and silica dust, which have been reduced by approximately 10% as of 2026. This makes dust-extraction abrasives a critical component of modern health, safety, and environmental strategies in automotive manufacturing.

Aluminum Oxide Dominates Coated Abrasives Market with 46% Share Driven by Versatility and Cost-Performance Efficiency

Grain Type Analysis: Aluminum Oxide Abrasives Lead Across Metal, Wood, and Industrial Applications

Aluminum oxide holds a leading 46.0% share of the coated abrasives market in 2025, driven by its optimal balance of hardness, toughness, durability, and cost efficiency across a wide range of industrial applications. Available in fused (brown) and advanced ceramic variants, aluminum oxide abrasives are the industry standard for metal grinding, woodworking, paint removal, and general-purpose sanding. With a hardness rating of 9 on the Mohs scale, these grains exhibit a self-sharpening fracture mechanism, continuously exposing fresh cutting edges and maintaining consistent performance over time. This makes them highly effective for ferrous metal fabrication, automotive refinishing, and construction surface preparation. Additionally, aluminum oxide remains 30–50% more cost-effective than ceramic alumina and significantly cheaper than silicon carbide, making it the preferred choice for high-volume sanding operations. The growing adoption of engineered ceramic alumina subtypes further enhances performance in advanced manufacturing environments, reinforcing its dominance in the global coated abrasives market.

Metal Fabrication Sector Leads Coated Abrasives Market with 32% Share Driven by Industrial Processing Demand

End-Use Industry Analysis: Automated Grinding and Surface Finishing Drive Market Growth

The metal fabrication segment accounts for 32.0% of the coated abrasives market in 2025, making it the largest end-use industry due to the essential role of abrasives in metal processing, finishing, and surface preparation. Applications include weld seam grinding, deburring, edge radiusing, and surface finishing, all critical for ensuring product quality and coating adhesion in industries such as construction, automotive, aerospace, and heavy equipment manufacturing. A key trend shaping the market is the shift toward automated and robotic grinding systems, where coated abrasive belts serve as precision tools for consistent, high-speed material removal. These systems demand abrasives with long life, predictable cut rates, and heat-resistant performance, driving increased adoption of ceramic-enhanced aluminum oxide abrasives. Additionally, the need for high-quality surface finishes and efficient production workflows is accelerating demand for advanced abrasives, positioning metal fabrication as a major growth driver in the industrial abrasives market.

Coated Abrasives Market Competitive Landscape Driven by Ceramic Grain Innovation, Automation, and Precision Surface Finishing

The coated abrasives market is characterized by advanced ceramic abrasives, precision surface finishing solutions, and automated sanding technologies. Key players are focusing on high-performance grains, dust-free sanding systems, and ESG-compliant manufacturing to enhance productivity, durability, and efficiency across automotive, aerospace, metal fabrication, and woodworking industries.

Saint-Gobain leads coated abrasives with ceramic grain innovation and global industrial footprint

Saint-Gobain Abrasives dominates the coated abrasives market with the largest global footprint and strong revenue base of €47.9 billion in 2025. Its Norton Quantum Prime line utilizes ceramic alumina micro-fracturing technology, reducing grinding pressure by 25% and extending abrasive life by 50%. The company continues to expand geographically, strengthening its presence in Europe and Latin America. Its Norton A275OP and Blaze portfolios remain industry benchmarks in automotive refinishing and aerospace applications. The “Grow & Impact” strategy prioritizes ESG-compliant manufacturing and high-margin industrial segments. Product innovation focuses on durability, efficiency, and sustainable abrasives.

3M advances coated abrasives through precision-shaped grain technology and digital manufacturing integration

3M is a technology leader in coated abrasives, driven by its Cubitron II precision-shaped grain innovation. The company exited its precision grinding segment in 2026 to focus on high-growth areas such as EV manufacturing and electronics. Its digital twin modeling capabilities allow simulation of abrasive wear, improving process optimization for OEMs. ESG initiatives include biodegradable backing materials and solvent-free adhesive systems. 3M’s robotic sanding systems provide real-time monitoring of abrasive performance, enabling predictive maintenance. Product strategy focuses on automation, sustainability, and high-precision abrasives for aerospace and defense.

Mirka drives dust-free sanding systems with smart abrasives and automation-ready solutions

Mirka is a global leader in net abrasives and dust-free sanding technologies, particularly through its Abranet Galaxy series. Its self-sharpening ceramic grains deliver consistent cut rates without clogging, improving productivity in high-end finishing applications. The launch of DEROS II and DEOS II sanders enhances performance in marine and aerospace sectors. Mirka’s ecosystem integrates smart tools with Bluetooth connectivity to monitor efficiency and vibration exposure. Expansion into robotics supports automated manufacturing environments. Product development focuses on smart sanding systems, dust-free solutions, and precision finishing.

Sia Abrasives leverages Bosch integration for high-precision finishing and AI-driven production control

Sia Abrasives benefits from Bosch’s global R&D capabilities, enabling advanced coated abrasive solutions for automotive and industrial applications. Its Sianet and Siachrome lines address ultra-fine finishing requirements for EV battery systems and high-performance coatings. Integration with Bosch AIoT systems enables predictive surface finishing and adaptive process control. X-Lock compatibility allows rapid tool changes, improving operational efficiency in metal fabrication. Expansion of Siacarbon backing enhances durability in heavy-duty sanding. Product innovation focuses on automation, precision finishing, and high-performance abrasives.

Klingspor expands coated abrasives portfolio with ceramic technology and heavy-duty metalworking solutions

Klingspor is a key player in coated abrasives, offering a broad portfolio of over 50,000 SKUs for industrial and retail applications. Its CEVOLUTION ceramic abrasive technology optimizes grain density for extended service life in stainless steel processing. The company is expanding into DIY and small-scale markets with professional-grade products in compact packaging. Its TITAN flap discs and WSM flapwheels are engineered for aggressive grinding and high stock removal. Investment in automated production ensures cost competitiveness. Product strategy focuses on versatility, durability, and metalworking efficiency.

Hermes Schleifmittel specializes in precision abrasives with advanced grain structures and localized expertise

Hermes Schleifmittel focuses on high-precision coated abrasives for automotive, aerospace, and furniture industries. Its HERMESIT abrasives feature a three-dimensional grain structure that ensures consistent surface quality throughout tool life. The company has restructured operations to strengthen its position in European and Asian markets. Divestment of North American manufacturing supports a focus on premium engineering applications. Its long-belt abrasives are widely used in precision finishing where uniformity is critical. Product development emphasizes surface consistency, supply chain resilience, and high-performance abrasive solutions.

United States Coated Abrasives Market: Precision Manufacturing, Robotics Integration, and EV Supply Chain Expansion

The United States coated abrasives market continues to dominate the global high-performance segment, supported by strong demand from semiconductor manufacturing, aerospace finishing, and precision engineering applications. In January 2026, the Semiconductor Industry Association reported global semiconductor sales reaching $82.5 billion, reflecting a 46.1% YoY increase. This surge has significantly elevated the demand for coated abrasive films for wafer thinning, lapping, and polishing, positioning the U.S. as a critical hub for microelectronics-grade abrasives. Concurrently, 3M announced Expanded Beam Optical (EBO) production capacity investments in April 2026, reinforcing the need for precision finishing abrasives in fiber optics and data center infrastructure.

Automation is reshaping abrasive consumption patterns, with Saint-Gobain Surface Solutions collaborating with AV&R to deploy the BF-X 200-c robotic finishing system. This AI-enabled system optimizes coated abrasive belt life cycles in aerospace turbine manufacturing, aligning with Industry 4.0 standards. Additionally, the shift toward silicon carbide (SiC) coated abrasives is accelerating due to EV production, where high hardness materials are essential for finishing advanced composites and alloys. Sustainability mandates, including a 27% reduction in non-recovered waste by 2025, are pushing manufacturers toward recycled polymer-backed abrasives and circular manufacturing models, while defense sector expansion is driving demand for ceramic alumina belts in armored vehicle fabrication.

Germany Coated Abrasives Market: Green Engineering, Industry 4.0, and High-Precision Metalworking Leadership

The Germany coated abrasives market is characterized by its leadership in eco-friendly abrasive solutions, advanced grinding technologies, and regulatory-driven innovation. Saint-Gobain reported in early 2026 that its abrasive solutions reduced the carbon footprint of residential building finishes by up to 23%, highlighting Germany’s strong alignment with sustainable manufacturing and low-carbon abrasive technologies. The enforcement of REACH regulations is accelerating the transition away from phenol-formaldehyde resins, promoting environmentally compliant bonding agents in coated abrasives production.

Technological innovation is equally critical. In September 2025, ANCA introduced InsertsPRO, enabling automated grinding of indexable inserts that rely heavily on high-performance coated abrasive discs for precision sharpening. German Mittelstand companies are adopting Digital Twin technology to monitor abrasive belt wear, reducing downtime by approximately 15% in automotive production lines. With global car sales reaching 74.6 million units in 2024, German OEMs have intensified procurement of high-grit finishing films for premium automotive coatings. Additionally, advancements in cryogenic grinding for medical implants are expanding the application scope of coated abrasives into high-value healthcare manufacturing.

China Coated Abrasives Market: Green Manufacturing Policies and High-Volume Industrial Demand

The China coated abrasives market is undergoing a structural shift from volume-driven production to high-value, environmentally regulated abrasive manufacturing. Under the Made in China 2025 initiative, manufacturers are increasingly adopting green coated abrasive technologies, supported by tax incentives and environmental compliance frameworks. Regulatory tightening is evident with the GB 4806.10-2025 standard issued by China’s National Health Commission, expanding permitted coating materials from 105 to 346 substances while enforcing strict limits on primary aromatic amines migration, significantly impacting raw material selection in abrasive coatings.

China’s dominance in the global steel industry, processing nearly 2 billion metric tons annually, sustains massive demand for zirconium alumina coated belts used in descaling and surface preparation. The country also leads in synthetic silicon carbide (SiC) production, integrating it into abrasives for electronics and ceramics manufacturing. VOC emission control policies are accelerating the shift toward water-based bonding systems, aligning with environmental targets. Furthermore, the rapid growth of domestic smartphone production is fostering localization of super-finish lapping films, reducing reliance on imported abrasive technologies and strengthening China’s position in electronics-grade coated abrasives.

India Coated Abrasives Market: PLI-Driven Manufacturing Growth and Export-Oriented Expansion

The India coated abrasives market is emerging as a high-growth region, fueled by government incentives, domestic manufacturing expansion, and rising automotive and electronics demand. The ₹1.91 lakh crore Production Linked Incentive (PLI) scheme has catalyzed over ₹9,200 crore in investments as of December 2025, significantly boosting coated abrasives demand in electronics assembly and automotive component manufacturing. A 77% decline in mobile phone imports since 2021 reflects strong import substitution trends, increasing reliance on domestically produced precision abrasive materials.

Leading players such as Carborundum Universal are establishing advanced R&D centers to develop humidity-resistant abrasive grains, tailored for India’s tropical climate. The automotive sector, reporting ₹32,879 crore in FY 2025-26, is driving consumption of waterproof abrasive papers for refinishing and body repair applications. Additionally, infrastructure expansion through PM MITRA Parks and industrial corridors is increasing bulk demand for coated abrasives in machinery maintenance. India’s ambitious renewable energy target of 48 GW solar PV manufacturing capacity is also creating new opportunities for abrasives used in silicon wafer slicing and polishing, positioning the country as a strategic export hub in the global coated abrasives market.

Japan Coated Abrasives Market: Ultra-Precision Manufacturing, Super-Abrasives, and Smart Factory Leadership

The Japan coated abrasives market leads globally in ultra-precision finishing, nano-scale abrasives, and advanced electronics applications. With a market valuation of $2.3 billion in 2025, Japan’s growth is driven by the demand for miniaturized electronic components requiring nano-finishing technologies. The country is at the forefront of developing coated abrasives for carbon fiber composites, supporting aerospace lightweighting initiatives and fuel-efficient structural designs.

Japan’s adoption of Digital Twin and smart factory systems enables real-time monitoring of abrasive tool wear, optimizing belt tension and operational efficiency. The increasing use of cubic boron nitride (CBN) coated abrasives in high-speed rail component finishing highlights Japan’s focus on advanced material compatibility. Sustainability is also a priority, with the development of bio-based resin backings aligned with strict ESG requirements in electronics manufacturing. Moreover, Japan’s leadership in lights-out manufacturing reflects a high degree of automation, where coated abrasives must deliver exceptional consistency, durability, and performance reliability in fully autonomous production environments.

Coated Abrasives Market Report Scope

Coated Abrasives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$17.1 Billion

|

|

Market Size (2032)

|

$25.5 Billion

|

|

Market Growth Rate

|

5.9%

|

|

Segments

|

By Grains (Aluminum Oxide, Silicon Carbide, Ceramic Alumina, Zirconia Alumina, Garnet and Emery, Super Abrasives), By Backing Material (Paper, Cloth, Vulcanized Fiber, Polyester Film, Hybrid Backing), By Product Form (Belts, Discs, Sheets and Rolls, Flap Discs and Wheels, Specialty Shapes), By Coating Density (Open Coat, Closed Coat, Semi-Open Coat), By End-Use Industry (Metal Fabrication, Automotive, Woodworking and Furniture, Aerospace and Defense, Electrical and Electronics, Building and Construction)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M Company, Saint-Gobain S.A., Robert Bosch Power Tools GmbH, Hermes Schleifmittel GmbH, Klingspor AG, Mirka Ltd., sia Abrasives Industries AG, Tyrolit Group, Carborundum Universal Limited, Fujimi Incorporated, Sankyo-Rikagaku Co., Ltd., Deerfos Co., Ltd., Indasa S.A., VSM Abrasives Corporation, Awuko Abrasives Wandmacher GmbH & Co. KG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Coated Abrasives Market Segmentation

By Grains

- Aluminum Oxide

- Silicon Carbide

- Ceramic Alumina

- Zirconia Alumina

- Garnet and Emery

- Super Abrasives

By Backing Material

- Paper

- Cloth

- Vulcanized Fiber

- Polyester Film

- Hybrid Backing

By Product Form

- Belts

- Discs

- Sheets and Rolls

- Flap Discs and Wheels

- Specialty Shapes

By Coating Density

- Open Coat

- Closed Coat

- Semi-Open Coat

By End-Use Industry

- Metal Fabrication

- Automotive

- Woodworking and Furniture

- Aerospace and Defense

- Electrical and Electronics

- Building and Construction

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Coated Abrasives Market

- 3M Company

- Saint-Gobain S.A.

- Robert Bosch Power Tools GmbH

- Hermes Schleifmittel GmbH

- Klingspor AG

- Mirka Ltd.

- sia Abrasives Industries AG

- Tyrolit Group

- Carborundum Universal Limited

- Fujimi Incorporated

- Sankyo-Rikagaku Co., Ltd.

- Deerfos Co., Ltd.

- Indasa S.A.

- VSM Abrasives Corporation

- Awuko Abrasives Wandmacher GmbH & Co. KG

*- List not Exhaustive