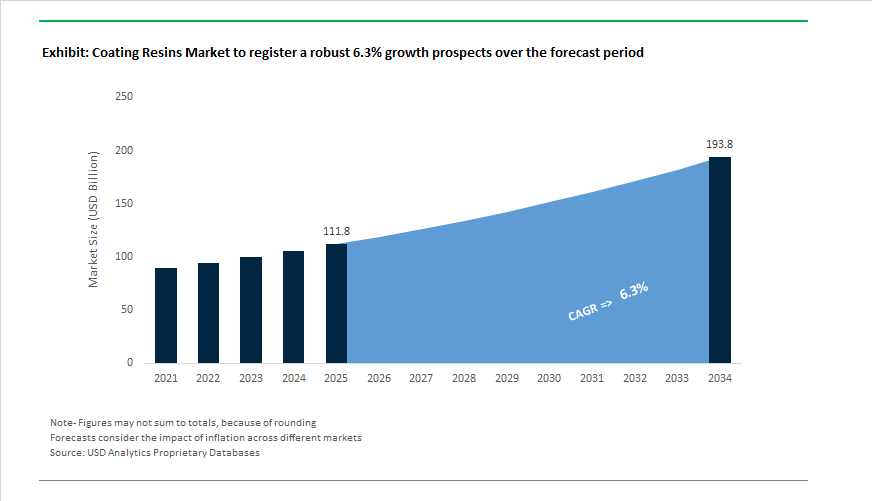

Coating Resins Market Outlook 2025–2034: $111.8 Billion to $193.7 Billion at 6.3% CAGR Driven by Consolidation, Renewable Feedstocks, and Powder Coating Innovation

The global Coating Resins Market is projected to expand from $111.8 billion in 2025 to $193.7 billion by 2034, registering a CAGR of 6.3%. Growth is supported by rising demand for acrylic resins, epoxy resins, polyurethane binders, alkyd resins, polyester resins, and powder coating systems across architectural, automotive, industrial, packaging, and electronics applications. Increasing regulatory pressure on VOC emissions, PFAS content, bisphenol-A usage, and carbon intensity is accelerating the shift toward waterborne, energy-curable, recycled-content, and bio-based resin chemistries. Simultaneously, large-scale M&A activity is reshaping competitive dynamics across upstream resin production and downstream coating formulation.

Industry consolidation intensified in 2025. In October 2025, AkzoNobel and Axalta announced an all-stock merger of equals valued at approximately $25 billion, creating a combined entity with 2024 revenues of $17 billion and projected cost synergies of $600 million. The transaction is expected to close in late 2026 or early 2027, forming one of the largest global coating platforms. In October 2025, BASF entered a binding agreement to sell its Automotive OEM, Refinish, and Surface Treatment businesses to Carlyle and the Qatar Investment Authority for €7.7 billion, marking a strategic shift away from finished automotive coatings toward upstream chemical precursors and resin technologies. In February 2025, Sherwin-Williams completed the acquisition of BASF’s Suvinil brand in Brazil, strengthening its position in South America’s architectural coatings and resin market. In June 2025, JSW Group signed an agreement to acquire the majority stake in AkzoNobel India Limited, significantly altering competitive intensity in India’s rapidly expanding architectural and industrial resin sector.

Sustainability-driven resin innovation accelerated during 2024–2026. In July 2024, Hexion introduced a lignin-based epoxy resin containing 40% renewable content, reducing dependence on petroleum-derived bisphenol-A in wood adhesives and composite coatings. In September 2024, BASF announced plans to integrate renewable propylene into its acrylic resin value chain by 2026, targeting a 20% bio-content threshold and a 25% reduction in carbon footprint versus fossil-based dispersions. Arkema confirmed in 2024 the successful incorporation of up to 40% post-consumer recycled PET into powder coating resins, lowering product carbon footprint by 20%. Covestro expanded production of PFAS-free Uralac® Premium P 8000 and P 9000 powder polyester resins into the Asia-Pacific region in September 2025, addressing tightening global restrictions on fluorinated chemicals. These developments indicate structural movement toward circular feedstocks, renewable monomers, and non-toxic resin platforms.

Advanced performance technologies and regional R&D investments further strengthened the coating resins ecosystem. Dow inaugurated its $100 million Texas Innovation Center in June 2024, focusing on waterborne resin development and digital color-matching technologies for low-VOC architectural and industrial coatings. PPG launched Envirocron® Extreme Protection Edge Plus in October 2025, a one-coat powder resin system engineered to enhance metal edge protection while reducing multi-layer application energy requirements. Asahi Kasei announced in February 2025 an absorption-type merger with Asahi Kasei Epoxy Corporation effective April 2026 to streamline epoxy resin and curing agent production for electronics and automotive sectors. Allnex introduced solvent-free, energy-curable resins for textile and leather coatings in 2024, targeting sustainable artificial leather production. These capital investments, renewable chemistry integrations, and mega-mergers underscore a structurally evolving coating resins market positioned for steady mid-single-digit expansion through 2034, anchored in performance differentiation and decarbonization-driven reformulation.

Coating Resins Market Trends and Drivers

Industrial-Scale Commercialization of Bio-Based and Mass-Balance Recycled Content Resins

What began as an R&D sustainability commitment is now becoming a full-scale transformation in resin feedstock sourcing, as global brands target Science Based Targets initiative (SBTi) pathway alignment, Scope 3 emissions reduction, and EU climate policies. Leading resin manufacturers are commercializing bio-circular resin chemistry at industrial scale, dramatically shifting the competitive structure of the coatings industry.

A key milestone was achieved in May 2025, when Arkema successfully scaled its Singapore Polyamide 11 (Rilsan®) complex—a €450 million investment, increasing castor-oil–derived resin capacity by ~50%. This investment marks a turning point in resin industrialization for high-performance automotive coatings, powder coatings, and 3D printing applications, proving that bio-based chemistry can match fossil-based alternatives in volume and durability.

Mass-balance certified supply chains are also gaining global traction. As of October 2025, Covestro’s CQ portfolio—defined by ≥25% bio-circular alternative raw material content—now includes TDI and MDI resin platforms, enabling downstream formulators to reduce Product Carbon Footprint (PCF) by up to 80% versus conventional petrochemical baselines. Concurrently, BASF has expanded its ISCC PLUS–certified mass-balance offerings, signaling a future where procurement teams specify traceability + PCF transparency as commercial contract requirements.

High-Performance Photopolymer and Electronics-Grade Resins Enabled by AI-Driven Material Development

The resin market is evolving beyond commodity architectural applications and expanding into high-value electronics, additive manufacturing (3D printing), and ultra-miniaturized components for 5G/6G systems.

From 2023 through 2024, Arkema (Sartomer) expanded UV/LED-cure photopolymer resin capacity in China to support vat polymerization platforms (SLA/DLP), delivering high mechanical toughness, thermal resistance, and snap-fit behavior essential for functional consumer electronics and lightweight automotive components.

At a structural innovation level, Material Informatics is emerging as a competitive accelerant. In September 2025, China-based Deep Material launched DM Agent, an AI-accelerated materials platform capable of compressing resin development cycles from multi-year R&D to months, using predictive molecular modeling for metal–polymer composite resins. This signals a new industry playbook where competitive advantage equals data + IP control over resin formulation speed.

Cool-Cure and Energy-Efficient Resin Systems to Support Decarbonized Manufacturing

The global shift toward low-energy industrial operations—particularly under decarbonization roadmaps in Europe and APAC—is creating a major market opportunity for low-temperature cure resin chemistries across OEM automotive, industrial wood, and metal finishing.

In November 2025, BASF Coatings commissioned a state-of-the-art resin facility in Münster, Germany, engineered for low-temperature curing, renewable energy integration, and automation. These resin systems enable coating curing at <80°C, reducing oven-related energy consumption by 15–20%, directly improving factory operating margins and sustainability scoring.

Additionally, the adoption of UV–LED curing resin formulations is accelerating in wood coatings and molded plastics. These new technologies eliminate oxygen inhibition issues, enabling instant room-temperature curing, effectively removing CO₂ emissions tied to gas-fired industrial drying tunnels. This repositioning of resins as productivity & carbon-efficiency enablers will redefine procurement KPIs across OEMs.

Advanced Resin Systems for Electrification – EV Battery Dielectrics and Thermal Potting

Electrification is fundamentally reshaping resin-material strategy. EV battery systems demand resins that deliver dielectric strength, thermal dissipation, vibration resistance, and high-throughput application compatibility.

In 2025, Sartomer (Arkema) expanded its portfolio of UV-curable dielectric resins designed to replace PET foils in cell insulation, delivering ≥200 V/µm dielectric breakdown strength while enabling instant curing, compatible with gigafactory-scale automation lines.

Meanwhile, Henkel launched Loctite SI 5643 and SI 5637 (Nov 2025), fast-curing silicone potting resins developed for EV inverters, onboard chargers, and power modules, enabling heat transfer across microgaps and prolonging battery and electronics lifespan. These systems signal that advanced coating resins will function not as finishes—but as core EV reliability technologies.

Coating Resins Market Share and Segmentation Insights

Resin Type Landscape: Acrylic Resins Dominate While High-Performance Systems Expand

Acrylic resins lead the coating resins market with 38% share in 2025, supported by superior weatherability, UV stability, and color retention, making them the backbone of architectural paint systems. Their increasing adoption in waterborne formulations aligns with tightening VOC regulations worldwide. Alkyd resins maintain a strong presence in solvent-borne applications due to low cost, high gloss, and excellent flow, particularly in industrial enamels and primers, although reformulation toward higher solids continues. Polyurethane resins serve high-traffic and automotive applications requiring toughness and chemical resistance, while epoxy resins remain indispensable for protective primers and industrial flooring because of exceptional adhesion and corrosion protection. Polyester and vinyl-based resins support flexible packaging and general industrial uses. Specialty resins, including fluoropolymers, silicones, and polyaspartics, represent a smaller but rapidly growing segment, driven by demand for extreme durability in architectural façades, cookware coatings, and infrastructure projects.

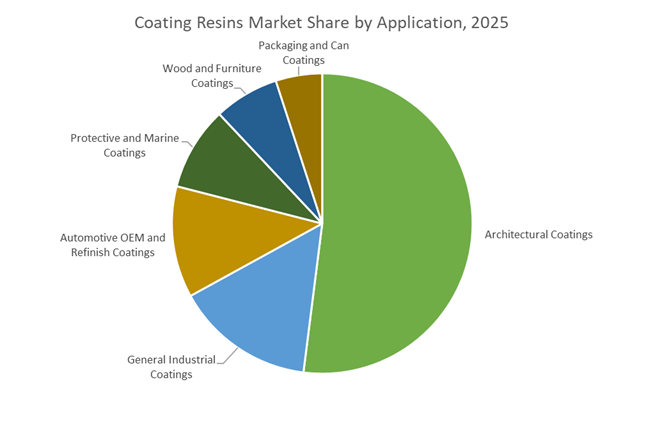

Application Segmentation: Architectural Coatings Drive Volume as Automotive and Marine Demand Advanced Resin Systems

Architectural coatings consume more than 52% of total coating resin output, fueled by continuous residential construction, urbanization, and refurbishment activity worldwide. Acrylic and vinyl resins dominate this high-volume segment, delivering cost-effective durability and aesthetic performance. General industrial coatings follow, relying on alkyd, epoxy, and polyester systems to protect machinery, appliances, and fabricated metal goods. Automotive OEM and refinish coatings demand multilayer resin architectures, where polyurethane and acrylic resins provide gloss depth, scratch resistance, and color stability. Protective and marine coatings depend heavily on epoxy chemistry for corrosion resistance in aggressive environments such as offshore platforms and ports. Wood and furniture coatings utilize tailored resin blends for grain clarity and abrasion resistance, while packaging and can coatings require specialized epoxy and polyester systems that balance flexibility with stringent food-contact compliance.

China: Automated Capacity Scale-Up Anchoring Low-Carbon Resin Manufacturing

China’s coating resins industry is entering a structurally transformative phase driven by capacity expansion, automation, and regulatory-led technology shifts. A major inflection point occurred in March 2025 when BASF Coatings completed the doubling of polyester and polyurethane resin production capacity at its Caojing site in Shanghai. The expansion lifted annual output to 18,800 metric tons and was strategically aligned with accelerating demand from Asian automotive OEMs seeking consistent, locally produced resin systems. Beyond volume, the Caojing facility has emerged as a benchmark for sustainable resin manufacturing. Operating entirely on renewable electricity and embedded with high-level automation, the site represents one of the most advanced low-carbon resin production platforms within the Shanghai Chemical Industry Park, reinforcing China’s push toward cleaner specialty chemical value chains.

Innovation infrastructure is evolving in parallel. In late 2025, Covestro inaugurated an automated Weighing and Mixing Workstation at its Asia-Pacific Innovation Center in Shanghai. This smart laboratory system integrates cloud-based data capture to accelerate AI-driven material insights, enabling faster iteration of coating resin formulations optimized for durability, flow, and environmental compliance. These investments are occurring against the backdrop of China’s 2025 Green Transformation directives, which are accelerating the shutdown of legacy solvent-based resin lines. The policy emphasis has shifted decisively toward waterborne acrylics and polyurethane dispersions, creating a structurally favorable environment for advanced, low-VOC coating resin technologies across construction, automotive, and industrial applications.

Competitive Landscape of the Coating Resins Market

The Coating Resins Market is shaped by vertically integrated chemical majors and specialty materials innovators focused on waterborne binders, ZeroPCF resin platforms, bio-attributed feedstocks, and high-performance polymers. Competitive differentiation increasingly centers on sustainable acrylic dispersions, polyurethane systems, fluoropolymers, and circular-economy resins for architectural, industrial metal, EV battery, and renewable energy coatings. Market leaders are accelerating capacity expansions in Asia, embedding AI into formulation workflows, and scaling biomass-balanced and PCR resin technologies. Strategic priorities include supply chain resilience, low-carbon resin portfolios, and next-generation performance materials for infrastructure, electronics, and aerospace applications.

BASF drives ZeroPCF architectural and industrial resins through Verbund integration

BASF remains a dominant force in coating resins, leveraging its Verbund integrated production model to supply one of the industry’s broadest portfolios, including Acronal® acrylic dispersions, Joncryl® water-based resins, and Basonat® aliphatic polyisocyanates. In 2025, BASF scaled its Joncryl® BRC bio-renewable line using biomass-balanced raw materials to achieve Zero Product Carbon Footprint performance parity with fossil-based grades. The company announced a major capacity expansion in Mangalore, India in February 2026 to meet South Asia’s rising demand for architectural and industrial metal coatings. Its Winning Ways strategy targets full ZeroPCF conversion, supported by internal production of key monomers such as acrylic acid and isocyanates.

Arkema accelerates specialty coating growth with ISCC PLUS and high-performance polymers

Arkema has evolved into a specialty materials pure player, emphasizing sustainable coating resins across electronics, eyewear, and industrial markets. Its portfolio spans Encor® emulsions, Crayvallac® additives, and Kynar® PVDF fluoropolymers. By early 2026, Arkema certified over 70% of global coating sites under ISCC PLUS, enabling mass-balanced bio-attributed materials for customers. The company tripled Rilsan® Clear transparent polyamide capacity in Singapore in January 2026 to serve fast-growing Asian consumer sectors. Innovation momentum continued with the late-2025 launch of Zenimid™, an ultra-high-performance polyimide range designed for extreme aerospace and industrial environments.

Dow scales PCR and waterborne acrylic resins through AI-driven formulation platforms

Dow leverages materials science scale to dominate high-volume architectural and packaging resin markets, anchored by MAINCOTE™ and RHOPLEX™ acrylic binders. In January 2026, Dow launched its Transform to Outperform initiative, targeting a USD 2 billion EBITDA uplift by 2028 through AI-enabled process simplification and customer modernization. The company introduced post-consumer recycled resin families in late 2025 for flexible packaging, cutting carbon and energy footprints by up to 30% versus virgin materials. Dow is also expanding specialized resin offerings for EV batteries and infrastructure, using real-time AI optimization to adapt formulations to regional regulatory requirements.

Covestro strengthens circular coating leadership after DSM RFM integration

Following its acquisition of DSM’s Resins and Functional Materials business, Covestro emerged as a major player in sustainable, high-tech coating resins. Its expanded portfolio includes Bayhydur® water-dispersible polyisocyanates alongside NeoCryl® and NeoPac® waterborne systems. In late 2025, Covestro showcased an automated AI-driven Weighing and Mixing Workstation at its Asia-Pacific Innovation Center to accelerate customized resin development. The company leads renewable energy applications with Desmodur® ultra N 31890 hardeners that dry three times faster, boosting photovoltaic manufacturing efficiency. Covestro’s core strength lies in circular economy materials, with a target of Scope 1 and 2 climate neutrality by 2035.

Allnex expands powder coating and cobalt-free resin systems across India

Allnex, backed by PTT Global Chemical, is a specialized leader in industrial coating resins and additives, operating 35 manufacturing sites worldwide with over €2.2 billion in annual revenue. At Paint India 2026, the company introduced ADDITOL® Dry CF cobalt-free additives, addressing tightening regulations around oxidative curing. Allnex dominates powder coating resins through CRYLCOAT® low-temperature cure systems, ideal for heat-sensitive substrates such as MDF and wood. In 2026, it upgraded its Mumbai laboratory and expanded its Mahad manufacturing facility, strengthening localized technical support and high-performance resin supply for the rapidly growing Indian coatings market.

Sherwin-Williams advances self-healing and IR-reflective resin platforms for urban infrastructure

Sherwin-Williams is among the world’s largest resin producers, supplying both internal paint brands and external customers through its Engineered Polymer Solutions division. Its EPS 2400 series waterborne acrylic resins are widely adopted in cabinetry, furniture, and industrial wood finishes. During 2025 to 2026, Sherwin-Williams launched self-healing and infrared-reflective coating technologies for Cool City infrastructure projects. The company’s consumer-centric R&D model focuses on durability, energy efficiency, and surface protection. Strategic vertical integration allows Sherwin-Williams to manufacture a significant share of its own resins, insulating margins from global feedstock volatility.

India: Certification-Led Market Access and Policy-Backed Resin Value Chain Upgrading

India’s coating resins industry is being reshaped by sustainability certification, localized application development, and targeted industrial policy. In July 2025, Arkema secured ISCC PLUS certification for its Navi Mumbai facility, enabling the production of bio-attributed acrylic, alkyd, and polyester resins using a mass-balance approach. This certification significantly strengthens India’s role as a manufacturing and export hub for sustainable specialty resins serving Middle Eastern and Southeast Asian markets, where traceable low-carbon materials are increasingly mandated.

Application-driven innovation is also gaining traction. In early 2024, DIC Corporation established a dedicated application laboratory in India focused on evaluating coating resin performance for large-scale infrastructure and automotive projects. This move localized technical validation, shortened qualification cycles, and improved collaboration with domestic OEMs and EPC contractors. On the policy front, the NITI Aayog 2025 chemical industry report highlighted the expansion of the Production-Linked Incentive Scheme to include downstream high-value specialty resins, signaling strong governmental intent to deepen India’s participation in global coating resin value chains. Regulatory standardization is reinforcing this trajectory. The Department for Promotion of Industry and Internal Trade issued new Quality Control Orders in 2025 for resin-treated laminates and coatings, enforcing mandatory BIS compliance to improve safety, durability, and environmental performance across domestic resin applications.

United States: Functional Realignment Toward PFAS-Free and Energy-Efficient Resin Systems

The United States coating resins market is undergoing strategic realignment driven by regulatory pressure, infrastructure recovery, and energy efficiency imperatives. In November 2024, Allnex announced a major restructuring of its U.S. footprint, investing in East St. Louis as its primary solvent-borne resin manufacturing hub while repositioning its Louisville facility as a specialized R&D center by 2025. This consolidation reflects a targeted approach to maintain solvent-borne capabilities where necessary, while accelerating innovation in next-generation resin technologies.

Regulatory developments are strongly influencing formulation strategies. State-level PFAS restrictions in regions such as California and Maine have pushed U.S. manufacturers to fast-track PFAS-free barrier coatings for food-contact packaging. In this context, Covestro introduced NeoCryl A, a recyclable acrylic resin positioned as an alternative to polyethylene films. Demand dynamics have also been shaped by infrastructure renewal programs. Following Florida’s 2025 citrus and infrastructure recovery initiatives, there has been increased use of epoxy-polyester hybrid resins and weatherable high-performance systems for heavy-duty construction equipment. At the same time, North American wood and flooring manufacturers are rapidly adopting UV, LED, and electron-beam curable resins to eliminate energy-intensive thermal curing, reducing Scope 2 emissions and reinforcing the shift toward energy-efficient coating resin technologies.

Germany: Bio-Based Leadership and Circular Resin Integration

Germany continues to act as a technology and sustainability bellwether for the global coating resins industry, with 2025 marking notable progress in bio-based and circular material deployment. Early in the year, Arkema commercialized its Synaqua bio-based waterborne resins, offering up to 97% renewable content. These resins are engineered to replace fossil-derived alkyds in architectural decorative coatings, supporting both carbon reduction targets and stringent European environmental standards.

Circular economy initiatives are also advancing resin innovation. German-led projects launched powder coating resins incorporating 40% post-consumer recycled PET in 2024, achieving a meaningful reduction in product carbon footprint without compromising mechanical or thermal performance. Strategic M&A activity further strengthened Germany’s position in high-performance polyurethane chemistry. In August 2025, Covestro acquired the specialty isocyanate assets of Vencorex, enhancing supply security for aliphatic isocyanates used in aerospace-grade and automotive polyurethane coatings. These developments collectively reinforce Germany’s leadership in compliant, circular, and high-durability coating resin systems.

Comparative Snapshot: Country-Level Strategic Direction in the Coating Resins Industry

Coating Resins Market County Level Snapshot

|

Country

|

Strategic Focus Area

|

Key Industrial Driver

|

Direction of Resin Innovation

|

|

China

|

Automated low-carbon capacity

|

Automotive OEM demand and green regulation

|

Waterborne acrylics and PUDs

|

|

India

|

Certification and policy stimulus

|

Export access and infrastructure growth

|

Bio-attributed specialty resins

|

|

United States

|

Regulatory compliance and efficiency

|

PFAS bans and infrastructure recovery

|

PFAS-free, UV and EB curable resins

|

|

Germany

|

Bio-based and circular materials

|

EU sustainability mandates

|

High-renewable and recycled-content resins

|

Coating Resins Market Report Scope

Coating Resins Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$111.8 Billion

|

|

Market Size (2034)

|

$193.7 Billion

|

|

Market Growth Rate

|

6.3%

|

|

Segments

|

By Resin Type (Acrylic Resins, Alkyd Resins, Polyurethane Resins, Epoxy Resins, Polyester Resins, Vinyl and Vinyl Acetate Resins, Specialty Resins), By Technology (Waterborne Technology, Solvent-borne Technology, Powder Coating Technology, Radiation-Curable Technology), By Application (Architectural Coatings, Automotive OEM and Refinish Coatings, General Industrial Coatings, Protective and Marine Coatings, Wood and Furniture Coatings, Packaging and Can Coatings)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Arkema S.A., Covestro AG, Allnex GmbH, Dow Inc., The Sherwin-Williams Company, DSM-Firmenich AG, DIC Corporation, Evonik Industries AG, Wacker Chemie AG, Huntsman Corporation, Nippon Paint Holdings Co., Ltd., Eternal Materials Co., Ltd., Wanhua Chemical Group Co., Ltd., Jiangsu Sanmu Group Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Coating Resins Market Segmentation

By Resin Type

- Acrylic Resins

- Alkyd Resins

- Polyurethane Resins

- Epoxy Resins

- Polyester Resins

- Vinyl and Vinyl Acetate Resins

- Specialty Resins

By Technology

- Waterborne Technology

- Solvent-borne Technology

- Powder Coating Technology

- Radiation-Curable Technology

By Application

- Architectural Coatings

- Automotive OEM and Refinish Coatings

- General Industrial Coatings

- Protective and Marine Coatings

- Wood and Furniture Coatings

- Packaging and Can Coatings

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Coating Resins Industry

- BASF SE

- Arkema S.A.

- Covestro AG

- Allnex GmbH

- Dow Inc.

- The Sherwin-Williams Company

- DSM-Firmenich AG

- DIC Corporation

- Evonik Industries AG

- Wacker Chemie AG

- Huntsman Corporation

- Nippon Paint Holdings Co., Ltd.

- Eternal Materials Co., Ltd.

- Wanhua Chemical Group Co., Ltd.

- Jiangsu Sanmu Group Co., Ltd.

*- List not Exhaustive