Market Analysis: Global Expansion, Sustainability Initiatives, and Premiumization Reshape the Cocoa and Chocolate Market

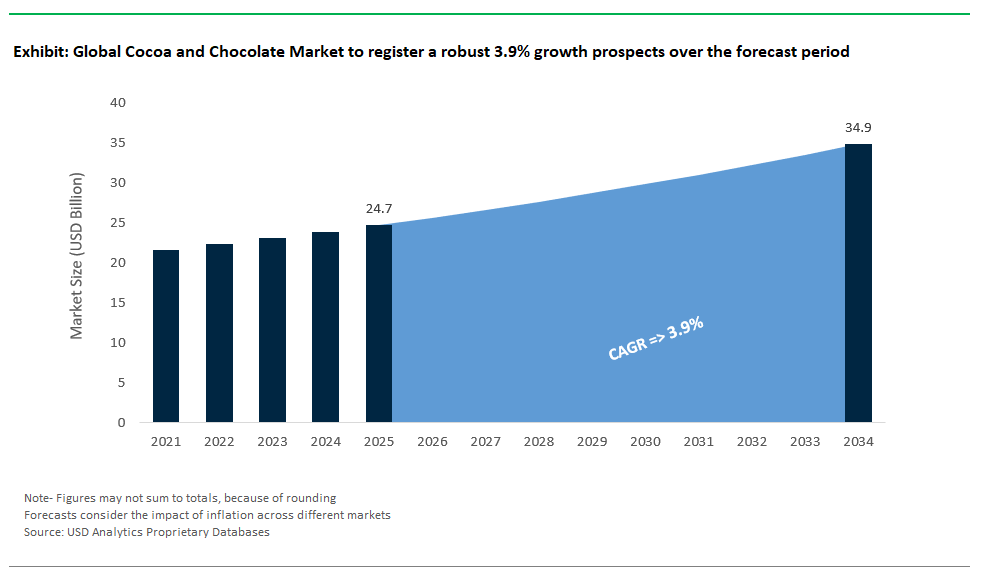

The Global Cocoa and Chocolate Market Size is estimated at $24.7 Billion in 2025 and is forecast to register an annual growth rate (CAGR) of 3.9% to reach $34.9 Billion by 2034.

The cocoa and chocolate market is experiencing a surge in global innovation and expansion, driven by product launches, strategic partnerships, and significant investments in manufacturing. In February 2025, Nestlé launched its new “KitKat Tablets” in Europe, Canada, and South Africa, with manufacturing centralized at the company’s newly upgraded Sofia, Bulgaria factory following a €44.2 million investment. Available in enticing flavors like Double Chocolate, Hazelnut, and Salted Caramel, these filled tablet bars are supported by robust marketing campaigns. Nestlé’s growth ambitions are also clear in its recent partnership with Formula 1 in Latin America, as the KitKat brand becomes the Official Chocolate Bar of Formula 1, unlocking a powerful global sports marketing platform through exclusive merchandise, in-store activations, and promotions set to expand globally into 2026.

Major players are investing heavily in infrastructure and sustainability to meet growing market demand and address changing consumer values. The Barry Callebaut Group a global chocolate and cocoa leader opened two new greenfield production facilities in Brantford, Canada, and Neemrana, India, underscoring its commitment to expanding its global supply capabilities. At the same time, Barry Callebaut is deepening its focus on circular economy principles by integrating upcycled cacaofruit products into its sustainability solutions portfolio, leveraging the entire cacaofruit for innovative new ingredients. The company’s participation as a 2025 Corporate Programme Partner with the EIT Food Accelerator Network further highlights its commitment to driving technological advancement and sustainable practices within the food and chocolate sector.

The market is also witnessing consolidation and a push toward premiumization. In November 2023, Mars Inc. made headlines by acquiring luxury chocolate retailer Hotel Chocolat Group plc for over $650 million, reinforcing its presence in the premium chocolate market. Meanwhile, Cargill continues to expand its sustainable cocoa sourcing programs worldwide, working directly with farmers and local communities to improve agricultural practices and support ethical chocolate production an increasingly important factor for both consumers and regulators. Collectively, these strategic moves and partnerships are redefining the cocoa and chocolate industry, fostering a wave of innovation, sustainability, and premium product experiences across global markets.

Emerging Growth Drivers in the Cocoa and Chocolate Market

Trend: Blockchain-Verified “Low-Cadmium” Cocoa for EU Compliance

The cocoa and chocolate market is witnessing a transformative trend toward blockchain-verified “low-cadmium” cocoa as regulatory compliance becomes a top priority, particularly in the European Union. With stringent cadmium limits set by EU authorities, producers capable of ensuring traceability and safety standards are gaining a competitive edge and commanding premium prices. Blockchain technology plays a pivotal role in this evolution, offering end-to-end transparency across the cocoa supply chain, reassuring both manufacturers and consumers of compliance with heavy metal regulations.

This shift is complemented by advancements in precision agriculture, where soil sensors and tailored agronomic practices help farmers reduce cadmium uptake in cocoa plants. Regions like Ecuador, known for their high-quality cocoa, are leveraging these technologies to meet international safety benchmarks and secure long-term supply contracts with leading global chocolate brands. As sustainability and food safety continue to influence consumer purchasing decisions, blockchain-enabled traceability coupled with “low-cadmium” certification is emerging as a key differentiator, setting a new standard for quality assurance in premium cocoa markets.

Opportunity: Upcycled Cocoa Pulp Beverages for Functional Markets

Upcycled cocoa pulp is unlocking a major growth opportunity in the functional beverage sector, transforming what was once a waste byproduct into a high-value ingredient. Traditionally discarded during cocoa processing, cocoa pulp is now being harnessed to create innovative, nutrient-rich beverages that cater to health-conscious consumers seeking natural and sustainable products. Its naturally sweet profile and high pectin content offer unique formulation benefits, enabling reduced-sugar recipes without compromising texture or flavor a critical advantage in the rapidly expanding market for low-sugar functional drinks.

Global beverage innovators are capitalizing on this potential, launching cocoa-fruit-based drinks that deliver both exotic flavors and functional health benefits, such as improved digestion and energy support. Beyond its nutritional attributes, the upcycling of cocoa pulp aligns with growing consumer demand for sustainability and circular economy practices, making these products highly marketable in premium wellness segments. As major chocolate manufacturers and beverage brands explore collaborative opportunities to integrate cocoa pulp into their portfolios, this niche is poised to evolve into a mainstream category, driving significant revenue growth and brand differentiation in the years ahead.

Competitive Landscape: Cocoa and Chocolate Market

The global cocoa and chocolate market is evolving rapidly, shaped by trends in premiumization, sustainability, functional benefits, and indulgent experiences. Rising demand for bean-to-bar transparency, single-origin cocoa, plant-based alternatives, and clean-label formulations is driving innovation among leading players. Brands are also responding to cocoa price volatility and consumer sustainability expectations by investing in ethical sourcing programs, alternative sweeteners, and future-ready product innovations.

Barry Callebaut – Leading B2B Innovator with WholeFruit & Ruby Chocolate

Barry Callebaut dominates the cocoa and chocolate industry as a B2B leader, supplying high-quality chocolate, cocoa ingredients, and custom formulations to global food manufacturers, artisan chocolatiers, and bakery brands. Their portfolio spans cocoa powder, butter, mass, specialty couvertures, and nutraceutical cocoa-based ingredients. Flagship innovations include Ruby chocolate a naturally pink chocolate with a fruity note and WholeFruit chocolate, utilizing 100% of the cacaofruit for a more sustainable, nutrient-rich product. The company introduced Second Generation Chocolate, focusing on “cocoa first, sugar last,” with simpler, cleaner labels. Recent initiatives like personalized 3D-printed chocolates through Mona Lisa and the Cacaofruit Experience range reflect its focus on premium, customizable, and functional chocolate solutions. Its Forever Chocolate program reinforces commitments to sustainability, zero child labor, and deforestation-free cocoa supply chains, ensuring leadership in ethical chocolate production.

Mondelez International – Iconic Brands Powering Global Snacking Trends

Mondelez continues to dominate the global chocolate market with household names like Cadbury, Milka, and Toblerone, positioned across mainstream and premium segments. Cadbury leads in indulgent milk chocolate and seasonal assortments, while Milka emphasizes Alpine milk quality and Toblerone is recognized for its premium triangular design and honey-almond nougat recipe. The company is responding to rising cocoa costs with strategic price adjustments and margin resilience while expanding in high-growth emerging markets like India. Mondelez is actively investing in ethical sourcing, aligning with consumer demand for sustainable cocoa supply chains. Snacking trends such as on-the-go packs, shareable formats, and comfort-driven indulgence remain core to Mondelez’s innovation pipeline, with strong emphasis on digital engagement and e-commerce expansion for enhanced accessibility.

Nestlé – Driving Sustainability and Cocoa Fruit Utilization

Nestlé leverages its powerhouse brands KitKat, Cailler, and Toll House to deliver diverse chocolate solutions from mass-market to premium indulgence. While KitKat dominates in wafer-based chocolate snacking, Cailler remains a hallmark of Swiss premium craftsmanship. Nestlé is also innovating within the baking category with Toll House, ensuring a strong foothold in at-home dessert preparation. A major differentiator for Nestlé is its commitment to sustainability, demonstrated through the Nestlé Cocoa Plan and recent launches under its "Nestlé Sustainably Sourced" range, certified by Rainforest Alliance. Innovative steps include using cocoa fruit pulp as a natural sweetener, reducing refined sugar while boosting farmer incomes. Additionally, Nestlé is capitalizing on travel retail growth through personalized packaging and premium assortments, while enhancing brand loyalty via digital activations and purpose-driven campaigns.

Hershey’s – Snacking Powerhouse with Functional Diversification

Hershey’s, anchored by iconic products like Reese’s and Hershey’s Kisses, commands significant market share in North America and is aggressively diversifying to mitigate cocoa price volatility. While Reese’s continues to lead with milk chocolate and peanut butter synergies, Hershey is expanding into on-trend ingredients and low-sugar chocolate through acquisitions like Lily’s, tapping into the better-for-you segment. Strategic diversification beyond chocolate into salty snacks (Dot’s Pretzels, SkinnyPop) and gummies positions Hershey as a holistic snacking leader, reducing dependency on cocoa-driven margins. Price adjustments and supply chain resilience strategies are central to its response to soaring cocoa costs. The company’s focus on functional indulgence, portfolio premiumization, and experiential marketing campaigns is reinforcing its competitive position.

Lindt & Sprüngli – Global Premium Chocolate Leader with Experiential Retail

Lindt & Sprüngli defines luxury in chocolate, driven by its flagship LINDOR truffles, Excellence dark bars, and seasonal icons like the Lindt Gold Bunny. Beyond Lindt, its portfolio includes Ghirardelli, specializing in baking and premium chocolate squares, and Russell Stover, offering boxed assortments with strong sugar-free options. Lindt reported 11.2% organic growth in H1 2025, driven by premiumization and retail expansion, opening flagship boutiques in key markets like London’s Piccadilly Circus and targeting high-potential markets like Saudi Arabia and India. Product innovation such as Lindt Dubai Style chocolate caters to regional tastes and premium gifting trends. Lindt’s sustainability roadmap includes responsible cocoa sourcing and exploration of cocoa-free chocolate alternatives, addressing both ethical and environmental concerns. Recognized as the world’s most valuable chocolate brand (Kantar BrandZ 2025), Lindt continues to elevate the premium segment through experiential retail and bespoke gifting.

Market Share and Segmentation Insights: Cocoa and Chocolate Market

By Product: Milk Chocolate Dominates, Dark Chocolate Grows Fastest

Milk and White Chocolate collectively hold the largest market share at 45.1% in 2025, driven by their widespread use in confectionery, snacks, and desserts. Their creamy texture and mass-market appeal make them a preferred choice among consumers globally. Industrial Chocolate maintains steady growth as it serves bakery, coating, and processed food applications, while Filled and Compound Chocolate cater to cost-sensitive segments and emerging markets. Dark Chocolate emerges as the fastest-growing category with a CAGR of 4.8%, fueled by health-conscious consumers seeking products rich in antioxidants, low sugar content, and clean-label formulations.

.png)

By End User: Supermarkets Lead, Online Retail Surges

Supermarkets and Hypermarkets dominate distribution channels with the largest share of 34.8% in 2025, thanks to bulk availability and strong impulse buying patterns. Confectionery and Bakery manufacturers also represent a significant segment due to the integration of cocoa-based ingredients in pastries, biscuits, and premium desserts. Specialty stores maintain their niche appeal with artisanal and premium offerings. However, Online Retail is the fastest-growing channel, expanding at a CAGR of 5.1%, driven by the rise of direct-to-consumer (D2C) brands, subscription-based chocolate boxes, and digital convenience. Pharmaceutical and nutraceutical applications are also on the rise, leveraging cocoa’s functional properties for cardiovascular and cognitive health benefits.

United States: Premiumization, Ethical Sourcing, and Plant-Based Innovation Reshape the Cocoa and Chocolate Market

The U.S. cocoa and chocolate market is being fundamentally transformed by consumer demand for premium quality and ethical sourcing. In 2024, 28% of U.S. consumers researched the origins of their cacao, nearly doubling from 16% in 2018, signaling an increasing expectation for transparency and responsible supply chains among chocolate brands. Millennials and Gen Z are at the forefront of this movement, seeking assurances around fair labor practices, environmental stewardship, and certifications like Fairtrade and Rainforest Alliance. Premium chocolate, including craft, single-origin, and ethically sourced varieties, is seeing rapid growth, driving up both value and average unit prices across retail channels.

Innovation is thriving, particularly in the plant-based and functional chocolate segments. The U.S. leads globally in vegan and dairy-free chocolate launches, with brands like TCHO and Raaka introducing organic, allergen-friendly options that cater to flexitarians and those with dietary restrictions. The rise of functional chocolate infused with ingredients for stress relief, gut health, or cognitive support is reshaping the perception of chocolate as a permissible indulgence with added health benefits. Miniature, portion-controlled products and upcycled cacao pulp innovations further reflect U.S. consumers’ preferences for convenience, health, and sustainability, making the country a bellwether for global chocolate trends.

Germany: Sustainability, Regulation, and Premium Craftsmanship Drive Market Evolution

Germany’s cocoa and chocolate sector is renowned for its commitment to sustainability and high quality, exemplified by ongoing participation in the German Initiative on Sustainable Cocoa. This initiative brings together industry, government, and NGOs to improve living standards for cocoa farmers and encourage environmentally responsible cultivation. The EU’s stringent cadmium regulations are also shaping sourcing and production, with German manufacturers collaborating closely with suppliers to ensure compliance through soil management and the use of low-cadmium cocoa varieties.

Health and wellness trends are steering the German chocolate market towards reduced-sugar and sugar-free innovations, as consumers prioritize both taste and nutrition. The premium and craft chocolate segments are expanding, with a growing appetite for single-origin bars and artisanal products that emphasize provenance, flavor complexity, and authenticity. German consumers’ exacting standards, combined with regulatory requirements and sustainability priorities, continue to influence not just domestic trends but also set benchmarks across the broader European market.

United Kingdom: Responsible Sourcing, Sustainability, and Functional Innovation Lead Chocolate Market

The United Kingdom is at the forefront of the global movement for ethical and sustainable chocolate. UK consumers especially younger demographics are highly attuned to the social and environmental impacts of cocoa production, with strong demand for transparency, Fairtrade certification, and responsible sourcing. Retailers and manufacturers face increasing pressure to prove their ethical credentials, both in cocoa traceability and in broader environmental initiatives, positioning sustainability as a central brand differentiator.

Innovation in the UK chocolate market also extends to health and wellness, with functional chocolates fortified with probiotics, collagen, or adaptogens gaining traction among health-conscious consumers. The plant-based chocolate segment is rapidly growing, with companies investing in vegan and dairy-free alternatives that closely mimic traditional milk chocolate’s taste and texture. This blend of social responsibility, product innovation, and premium positioning is making the UK a trendsetter in the evolution of the cocoa and chocolate market.

France: Sustainability, Luxury, and Regulatory Compliance Shape French Cocoa and Chocolate Market

France’s cocoa and chocolate market is distinguished by a commitment to sustainability, luxury, and compliance with stringent EU regulations. The French Sustainable Cocoa Initiative is central to fostering responsible sourcing and improved conditions in the cocoa supply chain. The country’s storied culinary heritage drives demand for luxury and artisanal chocolates, with discerning consumers seeking out products that emphasize provenance, terroir, and fine craftsmanship. French chocolate makers are innovating with high-cocoa content, unique regional flavor profiles, and limited-edition lines that celebrate the artistry of chocolate-making.

Compliance with new EU regulations, such as the Deforestation-free Products Regulation (EUDR) and the Corporate Sustainability Due Diligence Directive (CSDDD), is a key priority for French manufacturers. These frameworks require rigorous transparency and sustainability reporting throughout the supply chain. France’s leadership in luxury chocolate, combined with its proactive approach to sustainability and regulatory adherence, positions it as a global influence in the premium chocolate segment.

Switzerland: Premium Chocolate Innovation and Sustainability Set Global Standards

Switzerland remains the gold standard for chocolate quality and innovation, with the highest per capita chocolate consumption globally at 11 kg per person in 2025. Swiss chocolatiers are renowned for continual product innovation in the premium segment, exemplified by unique flavors, advanced textures, and luxurious gifting formats. High-profile launches like Godiva’s “Belgian Heritage Collection” underscore the emphasis on heritage and exclusivity.

Swiss chocolate companies are also pioneers in sustainability and traceability, driving initiatives such as the Swiss Platform for Sustainable Cocoa, which promotes ethical sourcing and transparent supply chains. Investment in advanced food technology ensures Swiss chocolate maintains its reputation for precision, taste, and quality. These efforts collectively reinforce Switzerland’s role as a leader in setting quality and sustainability benchmarks for the global cocoa and chocolate industry.

Ivory Coast (Côte d'Ivoire): Cocoa Production Leadership and Social Sustainability Challenges

Ivory Coast stands as the world’s leading cocoa producer, with its output critical to global chocolate supply chains. However, 2024 brought considerable challenges, including a 22.4% decrease in cocoa production due to severe weather events, significantly impacting both local livelihoods and global prices. Efforts to improve sustainability and social responsibility are accelerating, highlighted by initiatives such as Nestlé’s income accelerator program which aims to reach 160,000 farming families by 2030 and projects led by the International Cocoa Initiative (ICI) to address child labor and pesticide exposure.

Meeting the EU’s new Deforestation-free Products Regulation is a pressing challenge for Ivorian farmers and cooperatives, who must increase transparency and adopt more sustainable practices to maintain access to the European market. Despite obstacles, Ivory Coast’s pivotal role in the global cocoa industry makes its progress in social and environmental sustainability a focal point for chocolate manufacturers and ethical consumers worldwide.

Ghana: Sustainability Leadership and Production Resilience in Cocoa Market

Ghana, as the second-largest cocoa producer globally, remains vital to the world’s chocolate supply. The sector faced notable setbacks in 2024 due to weather and disease but is set for a production rebound in the 2024/2025 season thanks to improved weather and disease management strategies. Ghana is a focal point for global sustainability initiatives, with efforts aimed at reducing child labor, improving farming practices, and aligning with international sustainability standards.

Compliance with the EU’s Deforestation-free Products Regulation is a top priority, driving the adoption of more transparent and environmentally conscious farming methods. With ongoing international support, Ghana is well-positioned to maintain its critical supply role while elevating the sustainability and social responsibility of its cocoa sector.

Brazil: Rising Demand, Premiumization, and Investment Fuel Cocoa and Chocolate Market Growth

Brazil’s cocoa and chocolate market is on a growth trajectory, buoyed by rising disposable incomes and an expanding middle class. Increased domestic demand for chocolate is driving greater production and innovation within the country. Foreign investment is flowing into Brazil’s chocolate sector, underlining confidence in the market’s long-term potential. The rise of premium and dark chocolate consumption is especially notable, as health-conscious Brazilian consumers seek higher-quality, more artisanal products.

Events celebrating chocolate culture such as local and regional chocolate expos are boosting consumer engagement and knowledge. Brazilian chocolate makers are responding to these trends with product launches that emphasize local flavors, sustainability, and quality, helping Brazil’s cocoa and chocolate industry achieve greater recognition both domestically and on the global stage.

Cocoa and Chocolate Market Report Scope

Cocoa and Chocolate Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$24.7 Billion

|

|

Market Size (2034)

|

$34.9 Billion

|

|

Market Growth Rate

|

3.9%

|

|

Segments

|

By Product (Dark Chocolate, Milk/White Chocolate, Industrial Chocolate, Filled/Compound Chocolate), By End User (Supermarkets/Hypermarkets, Specialty Stores, Confectionery and Bakery, Dairy & Beverages, Pharmaceuticals & Nutraceuticals, Foodservice, Online Retail Stores), By Nature (Conventional, Organic), By Processing Stage (Cocoa Beans, Cocoa Derivatives)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Barry Callebaut AG, Mars, Incorporated, Mondelez International, Nestlé S.A., The Hershey Company, Ferrero Group, Lindt & Sprüngli AG, Cargill, Inc., Olam Food Ingredients, Blommer Chocolate Company, Cémoi Group, ECOM Agroindustrial Corp. Limited, Godiva Chocolatier, Inc., Guylian, Meiji Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Cocoa and Chocolate Market Segmentation

By Product

- Dark Chocolate

- Milk/White Chocolate

- Industrial Chocolate

- Cocoa Butter

- Cocoa Powder

- Cocoa Liquor (Mass)

- Cocoa Nibs

- Filled/Compound Chocolate

By End User

- Supermarkets/Hypermarkets

- Specialty Stores

- Confectionery and Bakery

- Dairy & Beverages

- Pharmaceuticals & Nutraceuticals

- Foodservice

- Online Retail Stores

By Nature

By Processing Stage

- Cocoa Beans

- Cocoa Derivatives

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Cocoa and Chocolate Market

- Barry Callebaut AG

- Mars, Incorporated

- Mondelez International

- Nestlé S.A.

- The Hershey Company

- Ferrero Group

- Lindt & Sprüngli AG

- Cargill, Inc.

- Olam Food Ingredients

- Blommer Chocolate Company

- Cémoi Group

- ECOM Agroindustrial Corp. Limited

- Godiva Chocolatier, Inc.

- Guylian

- Meiji Co., Ltd.

* List Not Exhaustive

Research Coverage

The Cocoa and Chocolate Market report by USDAnalytics delivers an in-depth analysis of market sizing, CAGR, and value projections, offering critical insights into market dynamics, trends, and recent developments. The study details pivotal industry moves, such as Nestlé’s KitKat Tablets launch and Formula 1 partnership, Barry Callebaut’s expansion in Canada and India, and Mars’ acquisition of Hotel Chocolat. Leading trends include blockchain-verified “low-cadmium” cocoa for EU compliance, upcycled cocoa pulp beverages, and sustainability initiatives transforming the industry.

Comprehensive segmentation covers product types (dark, milk, and white chocolate, industrial chocolate, filled/compound chocolate), end users (supermarkets/hypermarkets, specialty stores, bakery, dairy, pharmaceuticals, foodservice, online retail), nature (conventional, organic), and processing stage (cocoa beans, cocoa derivatives liquor, butter, powder, nibs). The report highlights the evolving competitive landscape, profiling major companies such as Barry Callebaut, Mars, Mondelez, Nestlé, Hershey, Ferrero, Lindt & Sprüngli, Cargill, Olam, Blommer, Cémoi, ECOM, Godiva, Guylian, Meiji, and others.

Time frame includes historic data from 2021–2024 and forecasts through 2025–2034, supporting actionable planning and strategy. Geographic coverage spans North America (US, Canada, Mexico), Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia), South America (Brazil, Argentina, Rest of South America), and Middle East & Africa (Saudi Arabia, UAE, South Africa, Egypt, Rest of Africa).

The report is designed for industry professionals, providing clear analysis on growth drivers, regulatory shifts, sustainability strategies, and future opportunities within the global cocoa and chocolate industry.

Deliverables:

- Full Market Research Report (PDF, Excel): Complete data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis.

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis.

- Recent Developments & News Tracker

- Executive Summary & Analyst Insights.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.