Commercial Aerospace Coatings Market Size, MRO Demand Expansion, and High-Performance Coating Technologies

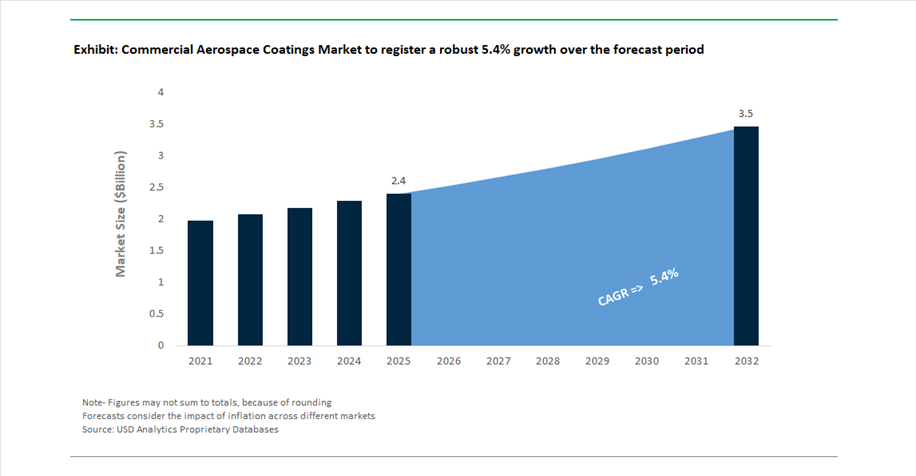

The global commercial aerospace coatings market was valued at $2.4 billion in 2025 and is projected to grow at a CAGR of 5.4% between 2025 and 2032, reaching $3.5 billion by 2032. This growth is driven by rising demand across aircraft OEM production, maintenance, repair and overhaul (MRO) activities, and fleet modernization programs, where coatings play a critical role in ensuring corrosion resistance, UV protection, weight optimization, and aerodynamic efficiency.

A key growth driver is the continued recovery and expansion of global aviation traffic, leading to increased aircraft utilization and higher demand for refinishing and maintenance coatings. Commercial airlines are prioritizing fuel efficiency and lifecycle cost reduction, which has intensified the adoption of lightweight, high-durability coatings that reduce drag and improve aircraft performance. Additionally, the shift toward next-generation aircraft platforms and composite airframes is creating demand for coatings with enhanced adhesion, flexibility, and environmental resistance.

The market is also undergoing a transition toward environmentally compliant coating technologies, including chrome-free primers, high-solids coatings, and low-VOC formulations, in response to stringent global aerospace regulations. Innovations in advanced resins, nanocoatings, and multifunctional surface treatments are enabling coatings that offer anti-icing, anti-microbial, and self-cleaning properties, further enhancing operational efficiency and passenger safety.

Regional Certification Expansion, Aerospace Production Scaling, and Sustainable Coating Innovation Driving Market Transformation

The commercial aerospace coatings market is evolving through regional certification expansion, production capacity scaling, and sustainability-driven innovation. In January 2026, AkzoNobel secured an extended CAAC approval, enabling it to supply a broader range of aerospace coatings and localized services within China. This certification significantly strengthens its position in the fast-growing Asia-Pacific aviation market, allowing closer collaboration with airlines and MRO providers while improving response times and service delivery.

Regional expansion strategies are also evident in the Middle East. AkzoNobel announced a major enhancement of its aerospace support network in January 2026, including improved logistics and on-site technical consultancy for major carriers. This move is designed to reduce lead times for specialized coatings and provide hands-on training for airline maintenance teams, reflecting the region’s growing importance as a global aviation hub.

Manufacturing capacity expansion is reinforcing supply capabilities. Sherwin-Williams’ March 2026 expansion of its Kentucky facility includes increased production capacity for aerospace coatings, supported by advanced automation to improve consistency and throughput. This investment aligns with rising global demand for high-performance topcoats such as SKYscapes® systems, widely used in commercial aircraft finishing.

Sustainability and regulatory compliance are driving innovation in coating formulations. Hentzen Coatings’ centennial R&D initiative (2025–2026) focuses on chrome-free primers and high-solids technologies, enabling aerospace manufacturers and MRO providers to meet increasingly stringent environmental standards. In parallel, AkzoNobel’s AS7489-certified training program (October 2025) is enhancing industry-wide application standards, ensuring optimal coating performance in terms of durability, weight reduction, and aerodynamic efficiency.

Upstream material innovation is also strengthening the value chain. Arkema’s expansion of high-performance resin capacity in China (March 2026) supports the growing demand for aerospace-grade coating materials, particularly for OEM production by regional players such as COMAC and localized Airbus operations. Meanwhile, Axalta’s strong financial performance (February 2026) provides the capital required to expand its footprint in performance coatings, including aerospace applications, as it prepares for strategic consolidation initiatives.

Regulatory Elimination of Hexavalent Chromium Driving Material Substitution

The commercial aerospace coatings sector is undergoing a decisive material transition as hexavalent chromium (Cr(VI)) moves from controlled usage to effective elimination. Regulatory pressure is converging from multiple fronts, with European authorities shifting toward a full restriction model while U.S. enforcement continues through occupational exposure limits and environmental toxicity frameworks. This alignment has created a non-negotiable pathway toward chrome-free coating systems across OEM production and MRO operations.

From a technical standpoint, the transition has only recently become viable due to performance breakthroughs in alternative chemistries. Lithium-based and magnesium-rich primers are now achieving salt spray resistance exceeding 3,000 hours, matching or surpassing legacy strontium chromate systems. This removes the primary historical barrier—corrosion protection—allowing regulatory compliance without sacrificing durability.

Operational economics are also shifting. The elimination of Cr(VI) significantly reduces compliance overhead related to worker safety, including respiratory protection and medical surveillance programs. Industry benchmarks indicate a 35% reduction in these operational costs per hangar, making chrome-free systems not only compliant but economically advantageous.

Major OEMs have already advanced beyond early adoption. Aircraft manufacturers have eliminated over 90% of chromated substances in primary surface treatments, replacing them with sol-gel conversion coatings and advanced primer systems. This signals a structural shift where regulatory compliance is fully embedded into baseline material specifications, rather than treated as an optional upgrade.

Carbon Reduction Mandates Accelerating Low-VOC and Lightweight Coatings

The first implementation phase (2024–2026) of global aviation carbon reduction frameworks is reshaping coating formulations with a direct focus on emissions, weight, and lifecycle efficiency. Airlines and MRO operators are increasingly adopting high-solids and waterborne coating systems as part of broader decarbonization strategies.

A key driver is the reduction of solvent content in coating systems. High-solids basecoat/clearcoat technologies now operate below 420 g/L VOC thresholds, while waterborne systems deliver up to a 60% reduction in VOC emissions compared to traditional solvent-borne alternatives. These changes are critical for compliance with tightening regional air quality standards and international emissions frameworks.

Weight reduction has emerged as a secondary but equally impactful benefit. By minimizing solvent content and optimizing coating film density, airlines can reduce aircraft weight by up to 150 kg for wide-body aircraft, directly translating into lower fuel consumption over long-haul operations.

Surface performance improvements are also contributing to fuel efficiency. Advanced ultra-smooth topcoats reduce aerodynamic drag by approximately 0.5% to 1.0%, a seemingly marginal gain that compounds significantly over thousands of flight hours. Additionally, extended-life coatings capable of maintaining gloss and color for 7–10 years are reducing repaint frequency by around 20%, lowering both maintenance costs and lifecycle emissions.

Advanced Functional Coatings for Composite Airframes

The increasing use of carbon fiber reinforced polymers (CFRP) in modern aircraft is creating new technical requirements that traditional coating systems were not designed to address. One of the most critical challenges is lightning strike protection (LSP), historically achieved using metallic meshes embedded within composite structures.

The industry is now transitioning toward conductive hybrid coatings that integrate materials such as carbon nanotubes (CNTs) and graphene directly into primer or intermediate layers. These coatings provide the necessary electrical conductivity to dissipate lightning strikes while significantly reducing system weight. Current solutions achieve up to 50% weight reduction compared to traditional metal-based LSP systems, directly enhancing aircraft range and payload efficiency.

Performance metrics have reached critical thresholds for adoption. Conductive coatings now exhibit surface resistivity as low as 0.1 Ω/square, enabling effective dissipation of high-energy lightning currents (up to 200 kA). Additionally, eliminating metal-composite interfaces reduces galvanic corrosion risks, extending inspection intervals for structural components by approximately 15%.

Nano-Engineered Surfaces Enhancing Flight Safety and Efficiency

Ice-phobic nano-structured coatings are emerging as a high-impact innovation area, particularly for critical surfaces such as wing leading edges and engine nacelles. These coatings are designed to minimize ice adhesion, complementing existing thermal or pneumatic de-icing systems.

Recent advancements have demonstrated over 90% reduction in ice adhesion strength compared to conventional polyurethane coatings. This allows ice to shed more easily under aerodynamic forces, reducing reliance on energy-intensive active de-icing systems.

The operational benefits are significant. Aircraft equipped with these coatings can reduce the energy load of de-icing systems by up to 30%, which is particularly valuable for hybrid-electric and next-generation propulsion systems where energy efficiency is critical. Additionally, airlines report a 25% reduction in ground de-icing fluid usage, lowering both operational costs and environmental impact at major airports.

Polyurethane Topcoats Dominate Aerospace Coatings Market with 42% Share Driven by Extreme Durability and Brand Identity

Layer Analysis: High-Solids 2K Polyurethane Topcoats Lead with UV Resistance and MRO Demand

Topcoats command a leading 42.0% share of the commercial aerospace coatings market in 2025, driven by their critical role in delivering aesthetic appeal, environmental protection, and long-term durability. These coatings, primarily high-solids 2K aliphatic polyurethane systems, provide exceptional UV resistance, gloss retention (>90% over 5+ years), and chemical resistance against aggressive fluids such as Skydrol®, jet fuel, and de-icing agents. Designed to withstand extreme thermal cycling (-54°C to +60°C) and high-speed erosion from rain and debris, they are indispensable for aircraft operating at 35,000–40,000 feet. Increasingly complex airline liveries and multi-layer basecoat/clearcoat systems are boosting material consumption and value. Additionally, the MRO repaint cycle (every 5–8 years) accounts for over 60% of total topcoat demand, ensuring stable recurring revenue. These factors firmly establish polyurethane topcoats as the cornerstone of the global aerospace coatings market.

Narrow-Body Aircraft Lead Aerospace Coatings Market with 56% Share Driven by High Production Rates and Frequent Repaint Cycles

Aircraft Category Analysis: Short-Haul Fleet Expansion and High Utilization Drive Coating Demand

Narrow-body aircraft dominate the commercial aerospace coatings market with a 56.0% share in 2025, fueled by their role as the primary workhorses of global air travel. Platforms such as the Airbus A320neo and Boeing 737 MAX families account for over 70% of new aircraft deliveries, with production rates exceeding 120 units per month combined. Each aircraft requires coating coverage of approximately 400–500 square meters, but the real demand driver is their high utilization rate (5–8 flights per day), leading to faster coating degradation and repaint cycles every 5–6 years. Additionally, the widespread use of white fuselage coatings enhances thermal management by reflecting over 80% of solar radiation, reducing structural stress and improving fuel efficiency. With increasing fleet expansion, frequent maintenance cycles, and evolving airline branding requirements, narrow-body aircraft remain the primary growth engine in the global aerospace coatings market.

Commercial Aerospace Coatings Market Competitive Landscape Driven by Lightweight Coatings, MRO Demand, and Sustainable Aviation Solutions

The commercial aerospace coatings market is highly specialized, driven by OEM and MRO demand, lightweight coating technologies, and sustainable aviation solutions. Competition centers on high-performance primers, UV-resistant clearcoats, digital color systems, and PFAS-free innovations that enhance fuel efficiency, durability, and regulatory compliance.

PPG Dominates Aerospace Coatings with E-Coat Innovation and Digital Integration

PPG Industries, Inc. leads the commercial aerospace coatings market with a strong market share in 2026, supported by strong presence in both OEM coatings and MRO applications. The company’s $300 million modernization program enhances global capacity for transparencies, sealants, and advanced aerospace coatings amid rising aircraft production. Its Aerocron™ electrocoat primer delivers uniform coverage on complex geometries while reducing weight, improving aircraft fuel efficiency. PPG SOLARON BLUE PROTECTION™ provides advanced UV-blocking for aircraft windows without compromising optical clarity, enhancing crew safety. The PPG LINQ™ digital ecosystem leverages AI-driven 3D visualization and precision color matching, reducing refinishing waste by 15%. PPG’s integrated innovation and scale position it as a dominant force in high-performance aerospace coatings.

AkzoNobel Expands Global Aerospace Coatings Network with Sustainable Technologies

AkzoNobel N.V. is strengthening its aerospace coatings leadership through a €50 million upgrade of its Waukegan facility and the development of a regional warehouse to improve supply chain efficiency. The planned Dubai Aerospace Coatings Hub in 2026 will support the rapidly expanding Middle East MRO and airline market. Its Aerodur® 3001 system enables faster drying and simplified application, reducing aircraft-on-ground (AOG) time during repainting cycles. AkzoNobel has achieved a 47% reduction in Scope 1 and 2 emissions through bio-based resins and waterborne coatings, reinforcing its sustainability leadership. The company’s Industrial Excellence program enhances operational efficiency through optimized global production networks. Its focus on sustainable, high-performance coatings strengthens its competitive position in aviation coatings.

Sherwin-Williams Targets High-Gloss Aerospace Finishes with Digital Visualization Tools

The Sherwin-Williams Company is expanding its aerospace coatings portfolio with a focus on high-gloss, UV-resistant finishes for commercial and business aviation segments. Its SKYscapes® basecoat-clearcoat system reduces application time by up to 30%, improving operational efficiency for airlines and MRO providers. The introduction of conductive coating CM0485115 enhances lightning strike protection for composite and aluminum aircraft structures. Sherwin-Williams’ Aircraft Color Visualizer tool enables precise 3D simulation of aircraft liveries, improving design accuracy and customer engagement. Its spec-driven sales model ensures deep integration into airline procurement standards. The company’s strong technical support and performance-driven coatings reinforce its presence in premium aerospace finishes.

Mankiewicz Leads Interior Aerospace Coatings with FST-Compliant Technologies

Mankiewicz Gebr. & Co. dominates the interior aerospace coatings segment, specializing in fire-safe, low-smoke, and low-toxicity (FST) coating systems for aircraft cabins. Its ALEXIT® coatings set industry benchmarks for durability, chemical resistance, and soft-touch aesthetics in cabin interiors. The expansion of its ALEXSEAL® brand into aerospace delivers high-end exterior finishes for private and executive jets. The company is advancing sustainable innovations, including glare-reduction coatings for cockpits and thermal management solutions for electronic housings. With over 1,800 specialists worldwide, Mankiewicz emphasizes localized R&D for customized solutions across Airbus, Boeing, and Embraer platforms. Its niche expertise in interior and specialty coatings strengthens its competitive differentiation in aerospace applications.

Hentzen Coatings Strengthens Position with Chromate-Free and High-Durability Solutions

Hentzen Coatings, Inc. is recognized for its highly engineered aerospace coatings, particularly in defense and commercial applications requiring rapid customization and compliance. The company leads in environmentally friendly coatings, offering high-solids and water-reducible formulations that meet stringent AS9100 standards. Its chromate-free primers and chemical agent resistant coatings (CARC) provide superior corrosion protection without environmental hazards. Hentzen’s coatings are designed for extreme thermal cycling conditions, maintaining performance from -55°C to 80°C. Investments in automated processing enable just-in-time delivery, reducing inventory burdens for MRO providers. Its focus on durability, sustainability, and responsiveness enhances its role in specialized aerospace coatings markets.

Henkel Expands Aerospace Coatings with PFAS-Free Technologies and Adhesive Integration

Henkel AG & Co. KGaA is advancing its aerospace coatings strategy by focusing on PFAS-free and fluorine-free surface technologies aligned with evolving environmental regulations. The company introduced anti-fingerprint coatings for cockpit and in-vehicle displays, improving durability and user experience. Its Loctite® AF 8812 coating delivers 9H hardness, protecting avionics and touchscreen surfaces from wear and light exposure. The acquisition of ATP strengthens Henkel’s capabilities in composite bonding and coatings integration. Its sustainability roadmap targets a fully renewable-powered production footprint by 2030. Henkel’s “Total Airframe Solution” combines adhesives and functional coatings, simplifying assembly and enhancing performance in modern composite aircraft structures.

United States Commercial Aerospace Coatings Market: Advanced Polymer R&D and Efficiency-Driven Innovation Leading Global Benchmark

The United States remains the global leader in commercial aerospace coatings, supported by a massive installed base of over 6,000 aircraft and continuous innovation in high-performance materials. The integration of AI-driven robotic spray systems across major facilities has improved coating precision while reducing material waste by approximately 15%, enhancing both efficiency and cost control.

Regulatory and technological advancements are reshaping the market. Updates under EPA NESHAP (2025) are accelerating the transition away from hexavalent chromium toward lithium-based and magnesium-rich primers, improving environmental compliance. Innovation in UV-curable clear coats is significantly reducing aircraft downtime for repainting—from 12 days to about 8 days—while riblet-textured coatings inspired by sharkskin are improving fuel efficiency by reducing drag by ~2%. Additionally, federal investments in MRO infrastructure are expanding environmentally controlled paint hangars, reinforcing the U.S. as the global benchmark for aerospace coatings.

China Commercial Aerospace Coatings Market: Self-Reliance Strategy and Sustainable Cabin Materials Driving Growth

China is rapidly advancing in the aerospace coatings market through its “Made in China 2025” initiative, focusing on domestic production and sustainability. A key milestone is the commercialization of 100% domestically produced polyurethane topcoats for the COMAC C919 program, ensuring high-altitude UV resistance and reducing reliance on imports.

Sustainability is also a major focus. By 2026, regulations mandate that 60% of aircraft synthetic leather interiors use waterborne PU coatings, aligning with global ESG standards. China is also investing in transparent conductive coatings (TCO) for aircraft windows, enabling integrated de-icing and anti-fogging systems. Expansion of MRO hubs in the Greater Bay Area is driving demand for abrasion-resistant exterior coatings, while VOC caps (250 g/L) are accelerating the shift toward high-solids formulations. These developments position China as a fast-rising aerospace coatings powerhouse.

France Commercial Aerospace Coatings Market: Chrome-Free Technology and Bio-Based Resin Innovation Leading Europe

France is at the forefront of European aerospace coatings innovation, particularly in sustainable and regulatory-compliant technologies. French manufacturers have achieved full hexavalent chromium-free certification for structural primers used in aircraft such as the A321XLR, aligning with REACH 2.0 requirements.

Innovation is strong in advanced materials. The adoption of graphene-enhanced primers is extending the service life of aluminum-lithium alloys by up to 30% in harsh environments. Additionally, the commercialization of lignin-derived polyurethane coatings is reducing carbon footprints by up to 40%. Investments in MRO infrastructure, including closed-loop solvent recovery systems (85% recycling), are improving sustainability. France is also pioneering Digital Product Passports (DPP) for aerospace coatings, ensuring full lifecycle traceability.

India Commercial Aerospace Coatings Market: Manufacturing Expansion and Cost Advantage Driving Emerging Leadership

India is rapidly emerging as a key aerospace coatings hub, supported by government incentives and growing domestic manufacturing capabilities. The PLI scheme for technical textiles has directed over $800 million into production of coated aerospace fabrics, strengthening local supply chains.

The market is also benefiting from cross-sector synergies. Expansion of Vande Bharat trains has driven adoption of fire, smoke, and toxicity (FST)-compliant coatings, now being applied in aviation interiors. Policy reforms, such as removal of import duties on specialized coating resins, are positioning India as a cost-effective global MRO destination for aircraft repainting. Additionally, airlines are implementing silver-ion antimicrobial coatings across cabin surfaces, while domestic production of waterborne PU dispersions is reducing costs for interior coatings. These factors position India as a fast-growing aerospace coatings market.

Brazil Commercial Aerospace Coatings Market: Biofuel Compatibility and Lightweight Coatings Driving Regional Innovation

Brazil is leveraging its strong aerospace and biofuel ecosystem to lead in sustainable aerospace coatings. Embraer has transitioned to 100% chrome-free coating systems, reducing aircraft paint weight by approximately 120 kg, improving fuel efficiency.

The country is also innovating in fuel compatibility. New biofuel-resistant sealants and coatings are designed to withstand high blends of sustainable aviation fuel (SAF), including synthetic kerosene. Additionally, solar-reflective coatings are being deployed to reduce cabin temperatures by up to 5°C, lowering auxiliary power unit (APU) fuel consumption. Investments in airport infrastructure and coating facilities are further supporting large-scale applications, while local sourcing of pigments is reducing environmental impact.

Japan Commercial Aerospace Coatings Market: Nanotechnology and Smart Coatings Driving High-Precision Performance

Japan’s aerospace coatings market is defined by cutting-edge nanotechnology and reliability-focused innovation. The commercialization of self-healing nanocoatings enables automatic repair of micro-cracks, preventing moisture ingress and extending coating life.

Advanced functionalities are a key differentiator. Japan is leading in ice-phobic hydrophobic coatings, reducing de-icing energy requirements by up to 20%. Additionally, development of optical-grade coatings for HUD systems ensures glare-free performance in advanced cockpits. Research into permeation-resistant coatings for hydrogen storage supports next-generation green aviation initiatives. Integration of IoT-enabled monitoring systems in coating processes ensures zero-defect manufacturing, reinforcing Japan’s leadership in precision aerospace coatings.

Commercial Aerospace Coatings Market Report Scope

Commercial Aerospace Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.4 Billion

|

|

Market Size (2032)

|

$3.5 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Resin Chemistry (Polyurethane (PU), Epoxy, Acrylic, Specialty Resins, Fluoropolymers, Silicone and Ceramic Hybrids), By Technology (Solvent-borne Coatings, Water-borne Coatings, Powder Coatings, Radiation-Curable), By Layer (Primers, Topcoats, Functional Specialty Coatings, Icephobic Nano-coatings, Conductive Coatings, Erosion-Resistant Coatings), By Application Area (Exterior Coatings, Interior Coatings, Engine and Specialized Parts), By End-User (OEM (Original Equipment Manufacturer), MRO (Maintenance, Repair, and Overhaul)), By Aircraft Category (Narrow-body Aircraft, Wide-body Aircraft, Regional Jets and Turboprops)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

PPG Industries, Inc., AkzoNobel N.V., The Sherwin-Williams Company, Mankiewicz Gebr. & Co., Axalta Coating Systems Ltd., Hentzen Coatings, Inc., BASF SE, Jotun A/S, Hempel A/S, Socomore, Henkel AG & Co. KGaA, International Aerospace Coatings, Indestructible Paint Ltd., Argosy International Inc., Mapaero

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Commercial Aerospace Coatings Market Segmentation

By Resin Chemistry

- Polyurethane (PU)

- Epoxy

- Acrylic

- Specialty Resins

- Fluoropolymers

- Silicone and Ceramic Hybrids

By Technology

- Solvent-borne Coatings

- Water-borne Coatings

- Powder Coatings

- Radiation-Curable

By Layer

- Primers

- Topcoats

- Functional Specialty Coatings

- Icephobic Nano-coatings

- Conductive Coatings

- Erosion-Resistant Coatings

By Application Area

- Exterior Coatings

- Interior Coatings

- Engine and Specialized Parts

By End-User

- OEM (Original Equipment Manufacturer)

- MRO (Maintenance, Repair, and Overhaul)

By Aircraft Category

- Narrow-body Aircraft

- Wide-body Aircraft

- Regional Jets and Turboprops

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Commercial Aerospace Coatings Market

- PPG Industries, Inc.

- AkzoNobel N.V.

- The Sherwin-Williams Company

- Mankiewicz Gebr. & Co.

- Axalta Coating Systems Ltd.

- Hentzen Coatings, Inc.

- BASF SE

- Jotun A/S

- Hempel A/S

- Socomore

- Henkel AG & Co. KGaA

- International Aerospace Coatings

- Indestructible Paint Ltd.

- Argosy International Inc.

- Mapaero

*- List not Exhaustive