Commercial Architectural Coatings Market Size, Sustainable Building Demand, and Premium Surface Solutions

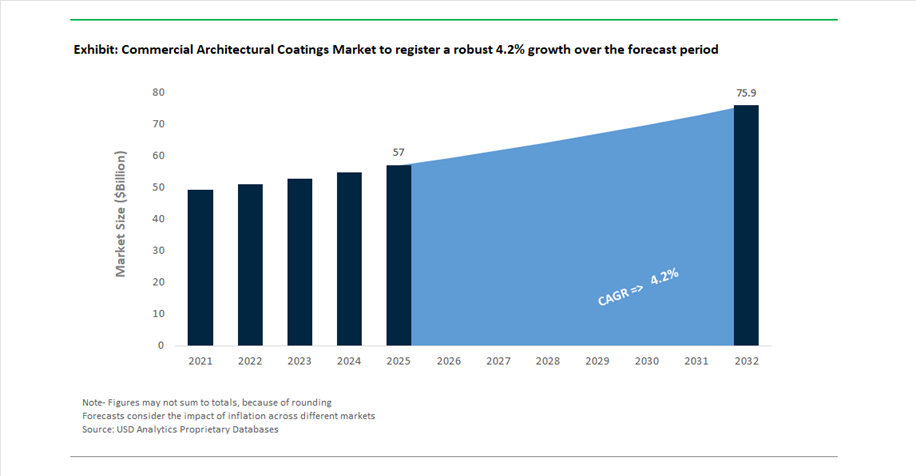

The global commercial architectural coatings market was valued at $57 billion in 2025 and is projected to grow at a CAGR of 4.2% between 2025 and 2032, reaching $76 billion by 2032. This steady growth is supported by rising demand from commercial construction, infrastructure development, hospitality, healthcare facilities, office spaces, and institutional buildings, where coatings provide protection, durability, aesthetic enhancement, and regulatory compliance.

A major growth catalyst is the increasing adoption of green building standards such as LEED and BREEAM, which is accelerating the shift toward low-VOC, waterborne, and sustainable coating solutions. Developers and architects are prioritizing coatings that deliver long lifecycle performance, energy efficiency, and reduced environmental impact, particularly for exterior facades, structural steel, and high-traffic interior environments. The growing use of powder coatings and high-performance primers is further enhancing corrosion resistance and reducing maintenance costs in large-scale commercial projects.

The market is also witnessing strong demand for premium and design-oriented coatings, driven by evolving architectural trends. Modern commercial spaces increasingly require coatings that offer advanced color depth, texture, and finish customization, enabling differentiation in competitive real estate and hospitality sectors. Additionally, the integration of functional coatings such as anti-microbial, anti-graffiti, and weather-resistant formulations is becoming critical in urban environments where durability and hygiene standards are paramount.

Strategic Acquisitions, Low-Carbon Coating Innovation, and Regional Expansion Driving Competitive Intensity

The commercial architectural coatings market is undergoing significant transformation through strategic acquisitions, sustainability-focused collaborations, and regional capacity expansion initiatives. A key development is Sherwin-Williams’ $1.15 billion acquisition of BASF’s Brazilian architectural coatings business (July 2025), including the premium Suvinil brand. This move, expected to finalize in early 2026, significantly strengthens Sherwin-Williams’ footprint in Latin America’s commercial and residential construction markets, enhancing its ability to serve large-scale infrastructure and decorative coating demand.

Sustainability-driven innovation is gaining strong momentum across the industry. In September 2025, AkzoNobel, Arkema, and BASF formed a strategic partnership to develop low-carbon architectural powder coatings, utilizing bio-based and mass-balanced resins to reduce CO₂ emissions. This collaboration reflects the growing emphasis on decarbonizing building materials while maintaining high durability and performance standards for exterior applications.

Product innovation is addressing evolving regulatory and performance requirements. In March 2026, PPG Industries launched AQUACRON® waterborne shop primers, specifically designed for structural steel in commercial architecture. These primers combine rapid curing, smooth finish, and low-VOC profiles, enabling contractors to meet environmental compliance while maintaining high throughput in construction projects. Additionally, PPG’s REDCert² certification (December 2025) for its European facilities reinforces the adoption of sustainable raw materials through biomass balance approaches, supporting developers pursuing green building certifications.

Design and aesthetic trends are also shaping product development strategies. Asian Paints’ “Moonlit Silk” (February 2026) and Behr’s “Hidden Gem” (July 2025) highlight a shift toward organic, calming, and texture-rich color palettes, influencing commercial interiors in sectors such as hospitality and office design. Meanwhile, Kansai Paint and Nippon Paint are expanding digital color matching and professional product portfolios, improving accessibility and customization for large-scale commercial projects.

Strategic expansion and integration efforts are further intensifying competition. RPM International’s acquisition of Kalzip (April 2026) strengthens its building envelope solutions portfolio, integrating aluminum roofing and façade systems with high-performance coatings. Similarly, Jotun’s new powder coatings facility in Malaysia (March 2026) is aimed at capturing growing demand in Southeast Asia’s commercial construction sector, particularly for metallic architectural finishes.

Corporate strategy and portfolio optimization are also playing a critical role. Hempel’s “Accelerate to Win” strategy (January 2026) focuses on expanding its presence in high-performance infrastructure and decorative coatings, supported by strong brand performance in premium and mid-market segments.

Low-Carbon Procurement Standards Redefining Product Competitiveness

The commercial architectural coatings market is being structurally reshaped by the integration of embodied carbon criteria into procurement frameworks, particularly through the U.S. General Services Administration (GSA) Buy Clean Initiative. As of 2026, coatings specified for federally funded projects must meet stringent Global Warming Potential (GWP) thresholds, effectively benchmarking products against the top 20%–40% of low-carbon alternatives in the market.

This shift has elevated Environmental Product Declarations (EPDs) from a supplementary disclosure tool to a mandatory competitive requirement. The surge in EPD submissions—up by over 350% since 2022—reflects a rapid industry-wide transition toward quantifiable carbon transparency. Manufacturers are now optimizing not only formulation chemistry but also production processes, energy sources, and supply chains to achieve lower embodied carbon scores.

The financial implications are direct and material. The GSA’s procurement model incorporates a 10%–15% scoring or price preference for coatings that demonstrate carbon-neutral or sub-zero manufacturing profiles. This effectively repositions sustainability performance as a pricing lever, disadvantaging legacy solvent-based systems that cannot meet these thresholds.

Additionally, coatings are increasingly recognized as a leverage point in overall building decarbonization strategies. Optimized coating systems can reduce lifecycle carbon emissions of a project by up to 8%, particularly when durability improvements reduce repaint cycles. This reframes coatings from a finishing material into a strategic contributor to whole-building carbon performance, aligning product development with broader sustainability targets.

EU Regulatory Framework Expanding Beyond VOC to Full Lifecycle Transparency

The European regulatory landscape is advancing beyond traditional VOC restrictions toward a comprehensive environmental and health disclosure model under the Construction Products Regulation (CPR) 2024. As of January 2026, coatings sold in the European Economic Area must comply with mandatory Environmental, Social, and Health (ESH) performance declarations, fundamentally altering market entry requirements.

A key regulatory innovation is the introduction of standardized limits for Semi-Volatile Organic Compounds (SVOCs), with coatings exceeding 0.1 mg/m³ emissions after 28 days restricted from high-occupancy environments such as offices, hospitals, and schools. This expands the regulatory focus from immediate emissions to long-term indoor air quality impacts, requiring advanced formulation strategies that address both VOC and SVOC profiles.

Carbon disclosure has also become mandatory through the Declaration of Performance and Conformity (DoPC), which now requires verified GWP data as a prerequisite for CE marking. This aligns closely with global trends toward lifecycle carbon accounting and ensures that environmental performance is consistently evaluated across all EU member states.

The introduction of Digital Product Passports (DPPs) further enhances transparency, enabling real-time access to data on chemical composition, recyclability, and compliance with REACH Substances of Very High Concern (SVHC) regulations. This digitalization of product data is streamlining specification processes while increasing scrutiny on material selection.

Functional Coatings Addressing Health-Centric Building Design

The growing emphasis on occupant health and safety is driving strong demand for antimicrobial and antiviral architectural coatings, particularly in high-traffic commercial and healthcare environments. These coatings are transitioning from niche applications to standard specifications in modern building design.

Technological advancements have significantly improved efficacy. Next-generation coatings utilizing photocatalytic or silver-ion technologies now achieve 99.99% pathogen reduction within 24 hours, outperforming conventional coatings by a wide margin. Importantly, these coatings provide sustained antimicrobial activity for 3 to 5 years, functioning as a continuous protective layer rather than a temporary treatment.

Adoption trends reflect this shift. More than 65% of new commercial office tenders in major global cities now include requirements for antimicrobial surface protection, particularly in shared spaces such as lobbies, elevators, and restrooms. This indicates a structural integration of health-focused materials into building specifications rather than a reactive response to isolated events.

A critical innovation in this segment is the move toward non-leaching antimicrobial systems, where active agents are permanently bound within the coating matrix. This addresses environmental and toxicity concerns while aligning with green building standards such as LEED v5 and WELL v2.

Air-Purifying Coatings Emerging as a Key Enabler for Net-Zero Buildings

As commercial buildings become increasingly airtight to meet Net-Zero energy standards, indoor air quality (IAQ) is emerging as a critical challenge. VOC-capturing or air-purifying coatings are addressing this issue by actively removing pollutants from indoor environments.

These coatings incorporate chemical scavengers capable of neutralizing up to 70% of airborne formaldehyde and similar compounds within 48 hours, with sustained activity lasting up to six years. This provides a passive air purification mechanism that complements mechanical ventilation systems.

The impact on occupant health and productivity is measurable. Buildings utilizing these coatings report a 20% reduction in Sick Building Syndrome (SBS) symptoms, a metric increasingly leveraged by developers to justify premium leasing rates for high-performance office spaces.

From an energy perspective, these coatings reduce reliance on HVAC-based air filtration, lowering system loads by approximately 12%. This is particularly valuable in Net-Zero and Passive House designs, where minimizing energy consumption is a core objective.

Additionally, air-purifying coatings contribute to green building certification frameworks, offering measurable credits under indoor environmental quality categories. This enhances their value proposition in projects targeting high-level sustainability certifications.

Topcoats & Finish Paints Lead Commercial Architectural Coatings Market with 52% Share Driven by Aesthetic Value and High-Traffic Durability

Coating Layer Analysis: Premium Acrylic Finish Paints Dominate with Scrub Resistance and Design-Driven Demand

Topcoats and finish paints dominate the commercial architectural coatings market with a 52.0% share in 2025, as they directly influence visual appeal, tenant satisfaction, and commercial property valuation. These coatings—primarily 100% acrylic eggshell and satin finishes—are engineered for high scrub resistance (ASTM D2486 >1000 cycles), burnish resistance, and stain durability, making them ideal for high-traffic environments such as hospitals, hotels, offices, and educational facilities. Frequent cleaning using disinfectants and abrasive methods accelerates repaint cycles to 3–5 years, driving consistent demand. Additionally, evolving commercial interior design trends, including biophilic color palettes, accent walls, and branded finishes, are increasing the consumption of premium, high-hide, and specialty decorative coatings that command 2x–3x higher pricing. This combination of aesthetic importance, durability requirements, and recurring repaint demand firmly establishes topcoats as the leading segment in the global commercial coatings market.

High-Durability Coatings Lead Functional Segment with 41% Share Driven by Lifecycle Cost Savings and Facility Management Standards

Functional Specification Analysis: High-Performance Acrylic and Hybrid Coatings Optimize Maintenance Efficiency

High-durability coatings account for a leading 41.0% share of the commercial architectural coatings market in 2025, driven by the critical need to extend repaint cycles and reduce long-term maintenance costs. These coatings, typically based on advanced acrylics and waterborne alkyd-acrylic hybrids, deliver superior scrub resistance, stain repellency, block resistance, and gloss retention, making them essential for commercial interiors exposed to heavy wear and frequent cleaning. The economic advantage lies in reducing repaint frequency from 4 years to 7 years, saving up to $200,000–$400,000 in labor and operational disruption costs for large commercial properties. In 2025, compliance with Master Painters Institute (MPI) “Extreme” standards and VOC regulations (SCAQMD Rule 1113, OTC Phase II) ensures these coatings remain the default specification for facility managers. The transition from solvent-borne alkyds to waterborne alkyd-acrylic hybrids further enhances adoption by enabling low-odor, occupant-friendly applications, solidifying this segment’s dominance in the commercial high-performance coatings market.

Commercial Architectural Coatings Market Competitive Landscape Driven by Low-VOC Technologies, Digital Tools, and Remodeling Demand

The commercial architectural coatings market is led by global players leveraging low-VOC formulations, digital color technologies, and strong contractor networks. Growth is fueled by renovation demand, sustainable coatings, and high-performance acrylic and powder coatings for commercial buildings, healthcare, and hospitality sectors.

Sherwin-Williams Expands Global Leadership with EMEA Integration and High-Performance Acrylics

The Sherwin-Williams Company maintains global leadership with $23.57 billion in 2025 sales and continued mid-single-digit growth projected for 2026. The integration of BASF’s decorative paints business significantly strengthens its EMEA footprint, while the Bowling Green expansion supports a 60% surge in North American exterior coatings demand. Its Colormix® 2026 Forecast introduces ultra-low-VOC, non-yellowing acrylic coatings tailored for high-traffic commercial environments such as healthcare and hospitality. The company’s vertically integrated network of 5,000+ stores enables a direct-to-contractor model, improving supply chain efficiency and project turnaround times. Sherwin-Williams continues to lead in high-performance architectural coatings, combining innovation with distribution scale. Its focus on premium, durable coatings supports demand across commercial construction and renovation projects.

PPG Refocuses Portfolio on High-Tech Coatings with Digital Color Ecosystem

PPG Industries, Inc. strategically exited its North American architectural coatings business, enabling a sharper focus on high-performance aerospace, automotive, and protective coatings segments. Its 2026 Color of the Year, “Secret Safari,” reflects a design-driven approach to modern commercial facades and architectural trends. PPG reported strong financial performance with record Q1 2026 adjusted EPS of $1.83, supported by synergies between architectural metal coatings and its aerospace and marine businesses. The expansion of the PPG LINQ™ digital ecosystem enhances project efficiency through AI-driven color visualization and reduces material waste by up to 15%. This digital integration supports architects and contractors in achieving precision in large-scale commercial projects. PPG’s repositioning strengthens its presence in specialized, high-margin coatings markets.

AkzoNobel Strengthens Architectural Powder Coatings with Long-Life UV Resistance

AkzoNobel N.V. continues to enhance profitability with a 27% increase in operating profit in 2025, driven by disciplined pricing strategies amid raw material volatility. Its Interpon D architectural powder coatings line now includes superdurable finishes offering over 25 years of UV resistance, making it ideal for commercial skyscrapers and infrastructure projects. The proposed merger with Axalta aims to create a leading global performance coatings entity with expanded capabilities. AkzoNobel has achieved a 47% reduction in Scope 1 and 2 emissions through adoption of bio-attributed resins and sustainable manufacturing practices. Its focus on powder coatings aligns with increasing demand for solvent-free, durable architectural solutions. The company’s innovation and sustainability initiatives reinforce its leadership in commercial coatings.

Nippon Paint Drives Growth Through R&M Dominance and Antimicrobial Coatings

Nippon Paint Holdings (NIPSEA Group) is expanding its global presence through the $2.3 billion AOC acquisition and a strategic push into India and Southeast Asia. The company is trending toward ¥1.6 trillion in revenue for 2026, supported by its asset assembler model and aggressive M&A strategy. Its dominance in the renovation and maintenance segment, which accounts for 70% of regional sales, provides resilience amid slowing new construction in China. Nippon’s smart surface coatings incorporate antimicrobial properties without toxic biocides, addressing hygiene requirements in public and commercial spaces. The company’s focus on specialty formulations and sustainable coatings supports long-term growth. Its regional diversification and innovation strengthen its competitive position in architectural coatings.

Masco (Behr) Targets Professional Segment with One-Coat Technologies

Masco Corporation’s Behr Paint is transitioning toward a pro-first strategy, with 2026 EPS guidance of $4.10–$4.30 reflecting recovery in remodeling activity. The expansion of BEHR DYNASTY® and MARQUEE® coatings introduces one-coat hide technology, reducing labor costs and improving efficiency for commercial painting contractors. Its exclusive partnership with The Home Depot ensures strong distribution in the residential repair and remodel segment, which offers stable demand and higher margins. Masco is investing in bio-based formulations and faster drying technologies, reducing project timelines by 20%. The company’s focus on contractor efficiency and sustainability aligns with evolving market needs. Its innovation supports growth in commercial repainting and renovation projects.

Asian Paints Expands Market Leadership with Digital Services and Affordable Low-VOC Solutions

Asian Paints Limited dominates the South Asian architectural coatings market with over half of India’s organized sector and consistent 10–12% volume growth entering 2026. The company is evolving beyond paints into integrated home décor and services, leveraging digital visualization tools and Safe Painting Services to secure commercial contracts. Investments exceeding $250 million in capacity expansion focus on waterborne VAM production, ensuring supply chain resilience. Its Neo-Bharat latex paints target semi-urban commercial infrastructure with affordable, low-VOC alternatives to traditional coatings. Asian Paints’ strong distribution network and service-led model enhance customer engagement. Its strategic focus on sustainability, affordability, and digitalization strengthens its leadership in emerging markets.

India Commercial Architectural Coatings Market: Capacity Disruption and Premiumization Driving Rapid Transformation

India is currently the most dynamic market for commercial architectural coatings, undergoing a major structural shift driven by capacity expansion and rising premium demand. The launch of Birla Opus by Grasim Industries added 1,332 million liters of annual capacity, representing a ~40% increase in national production, fundamentally reshaping competition in the premium segment.

Regulatory and demand-side factors are accelerating transformation. Stricter Zero-Liquid-Discharge (ZLD) mandates in key states are pushing manufacturers toward sustainable production, while waterborne coatings now account for over 72% of market share, driven by green building certifications such as LEED. Premiumization is evident in Tier-1 cities, where self-cleaning and heat-reflective coatings command ~20% price premiums, and repaint cycles have shortened significantly (from ~7 years to ~3–4 years). Additionally, large-scale infrastructure investments (~$130 billion) are fueling demand for anti-carbonation coatings in airports, metros, and commercial hubs.

China Commercial Architectural Coatings Market: Consolidation and Smart Coatings Driving High-Value Shift

China’s market is transitioning from volume-driven growth to a high-value, technology-focused model, despite a slowdown in new construction. The implementation of GB 4806.10-2025 standards is tightening safety requirements, mandating ultra-low levels of hazardous substances in commercial interiors.

A key structural shift is the “repainting economy”, with major players redirecting up to 70% of marketing efforts toward maintenance and refurbishment. Innovation is also accelerating, with the introduction of color-changing coatings that respond to light exposure, reducing HVAC energy consumption in glass-heavy buildings. Growth is increasingly concentrated in Tier 3–6 cities, while government policies are forcing consolidation by phasing out small solvent-based producers. Additionally, the rise of building-integrated photovoltaics (BIPV) is driving demand for transparent conductive coatings in commercial facades.

United States Commercial Architectural Coatings Market: Federal Stimulus and AI-Driven Customization Leading Innovation

The United States market is evolving through infrastructure funding and advanced digital technologies. Investments under the Infrastructure Investment and Jobs Act (IIJA) are driving strong demand for corrosion-resistant coatings in public infrastructure such as transit hubs and commercial buildings.

Technological innovation is a major differentiator. The deployment of AI-enabled color-matching kiosks across 15,000+ retail locations enables near-perfect customization (99.9% accuracy), transforming contractor workflows. Regulatory changes are also shaping the market, with EPA rules driving a 22% increase in adoption of bio-based and oxygenated solvents. Additionally, the semiconductor boom is creating niche demand for ESD and chemical-resistant coatings in cleanroom environments, while antimicrobial coatings have become standard in ~85% of new commercial projects, particularly in healthcare and education sectors.

Germany Commercial Architectural Coatings Market: REACH 2.0 Compliance and Bio-Circular Innovation Driving Sustainability

Germany remains the global benchmark for sustainable architectural coatings, driven by strict environmental regulations and circular economy practices. The industry has already achieved a ~90% phase-out of PFAS-based surfactants, ahead of broader EU restrictions.

Innovation is centered on energy efficiency and traceability. The rollout of Digital Product Passports (DPP) provides full lifecycle transparency for coatings, while bio-circular resins are reducing CO₂ emissions by up to 50%. Demand for IR-reflective “cool” coatings is rising sharply under energy efficiency laws, and strict indoor air quality regulations (≤300 µg/m³ TVOC) are pushing the market toward fully waterborne systems. Additionally, Germany is developing permeation-resistant coatings for hydrogen infrastructure, reinforcing its leadership in sustainable and high-performance coatings.

Japan Commercial Architectural Coatings Market: Disaster-Resistant Formulations and Healthcare-Focused Innovation

Japan’s market is uniquely shaped by seismic resilience and aging population needs, driving specialized coating innovations. New building codes mandate flexible, crack-bridging coatings that maintain structural integrity and moisture protection after earthquakes.

Advanced material technologies are also gaining traction. The widespread adoption of photocatalytic self-cleaning coatings reduces maintenance costs for high-rise buildings, while zwitterionic antimicrobial surfaces prevent bacterial biofilm formation in hospitals. Regulatory reforms are accelerating the adoption of biocompatible coatings in healthcare infrastructure. Additionally, government incentives are shifting demand toward retrofitting projects (≈65% of market volume), reflecting Japan’s focus on upgrading existing commercial buildings.

Brazil Commercial Architectural Coatings Market: Waterproofing Standards and Agribusiness Demand Driving Growth

Brazil’s market is expanding through infrastructure upgrades and agribusiness-driven demand. Updated building codes now mandate liquid-applied polyurethane waterproofing systems for high-rise commercial rooftops, significantly increasing demand for durable coatings.

Agriculture is a major growth driver, with a 15% increase in demand for ZM-coated steel used in grain storage infrastructure. Additionally, the country’s “Fuel of the Future” legislation is boosting demand for chemical-resistant coatings in fuel-handling facilities. Investments in public-private infrastructure projects (~$14 billion) are further driving adoption of high-visibility and anti-skid coatings in transport hubs. Coastal developments are also benefiting from the adaptation of marine-grade coatings to combat corrosion, positioning Brazil as a key regional market.

UAE Commercial Architectural Coatings Market: Net-Zero Mandates and Hospitality Boom Driving Premium Demand

The UAE market is defined by strict sustainability regulations and rapid hospitality expansion. VOC limits of 30–100 g/L for commercial interiors are accelerating the dominance of waterborne acrylic coatings, which already account for over 58% market share.

A major demand driver is the hospitality refurbishment wave, with over 35,000 hotel rooms under development requiring fast-curing, high-durability coatings that allow turnaround within 24 hours. Smart city initiatives under the Dubai 2040 Urban Master Plan are boosting adoption of heat-reflective coatings to combat urban heat islands. Additionally, stringent indoor air quality standards (≤0.08 ppm formaldehyde) are driving demand for air-purifying coatings, while the shift toward design-build contracts is increasing specification of premium finishes.

Commercial Architectural Coatings Market Report Scope

Commercial Architectural Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$57 Billion

|

|

Market Size (2032)

|

$76 Billion

|

|

Market Growth Rate

|

4.2%

|

|

Segments

|

By Technology (Water-borne, Solvent-borne, Powder Coatings, Bio-based Formulation), By Resin Chemistry (Acrylic, Polyurethane (PU), Epoxy, Alkyd, Specialty Resins), By Coating Layer (Topcoats and Finish Paints, Primers and Undercoats, Sealers and Waterproofers, Stains and Varnishes), By Functional Specification (Antimicrobial and Hygiene Coatings, High-Durability, Solar-Reflective, Anti-Graffiti and Chemical-Resistant), By Commercial Application (Office and Corporate Buildings, Healthcare Facilities, Educational Institutions, Retail and Hospitality, Infrastructure and Public Works)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sherwin-Williams Company, PPG Industries, Inc., AkzoNobel N.V., Nippon Paint Holdings Co., Ltd., RPM International Inc., Asian Paints Limited, Kansai Paint Co., Ltd., Jotun A/S, Axalta Coating Systems Ltd., BASF SE, Masco Corporation, Hempel A/S, Benjamin Moore & Co., DAW SE, Berger Paints India Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Commercial Architectural Coatings Market Segmentation

By Technology

- Water-borne

- Solvent-borne

- Powder Coatings

- Bio-based Formulation

By Resin Chemistry

- Acrylic

- Polyurethane (PU)

- Epoxy

- Alkyd

- Specialty Resins

By Coating Layer

- Topcoats and Finish Paints

- Primers and Undercoats

- Sealers and Waterproofers

- Stains and Varnishes

By Functional Specification

- Antimicrobial and Hygiene Coatings

- High-Durability

- Solar-Reflective

- Anti-Graffiti and Chemical-Resistant

By Commercial Application

- Office and Corporate Buildings

- Healthcare Facilities

- Educational Institutions

- Retail and Hospitality

- Infrastructure and Public Works

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Commercial Architectural Coatings Market

- Sherwin-Williams Company

- PPG Industries, Inc.

- AkzoNobel N.V.

- Nippon Paint Holdings Co., Ltd.

- RPM International Inc.

- Asian Paints Limited

- Kansai Paint Co., Ltd.

- Jotun A/S

- Axalta Coating Systems Ltd.

- BASF SE

- Masco Corporation

- Hempel A/S

- Benjamin Moore & Co.

- DAW SE

- Berger Paints India Limited

*- List not Exhaustive