Commercial Drinking Fountains Market Overview: Growth Outlook and Strategic Insights

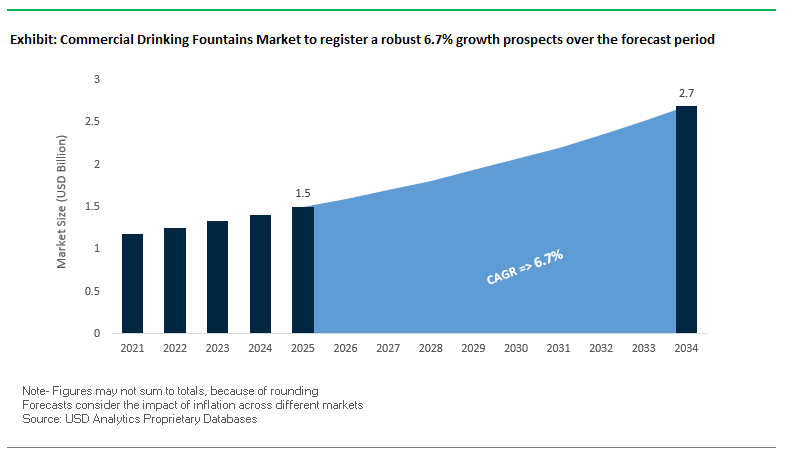

The global commercial drinking fountains market is projected to grow from USD 1.5 billion in 2025 to USD 2.7 billion by 2034, at a CAGR of 6.7%. This expansion is fueled by increasing investments in public health infrastructure, eco-friendly hydration solutions, and touchless technology. Demand is particularly strong in corporate offices, transportation hubs, schools, healthcare facilities, and public parks, with buyers prioritizing hygiene, durability, and compliance with environmental standards. Stainless steel remains the preferred material, offering long-term reliability in high-traffic environments, while solar-powered and off-grid models are becoming more prominent in sustainability-focused projects.

Key Insights for Industry Professionals

- Touchless Surge – Over 41% of new installations feature sensor-based, hands-free operation for improved hygiene.

- Material Preference – Stainless steel units hold 42% share, valued for corrosion resistance and ease of cleaning.

- Commercial Applications Dominate – Corporate, transport, and public sectors account for 55% of total demand.

- Sustainability Trend – 34% of recent urban parks now feature eco-friendly, solar-powered fountains.

- Installation Type Mix – Wall- and floor-mounted units make up 62% of the market, with wall-mounted popular in schools and hospitals.

Recent Developments and Industry Shifts

The commercial drinking fountains industry is evolving through filtration advancements, smart connectivity, and sustainability initiatives. In August 2025, Global Water Solutions introduced its Anti-Legionella Flow-Thru™ Valve, a breakthrough in preventing water stagnation in hospitals and commercial spaces. This reflects a wider industry trend toward health-protective water circulation technologies.

Zurn Elkay Water Solutions posted an 8% YoY sales increase in July 2025, underscoring strong non-residential demand, especially in education and healthcare. The same month, Haws Corporation earned its fourth Safety and Health Achievement Recognition Program (SHARP) award, highlighting excellence in manufacturing safety. Regulatory awareness is also shaping operations, as companies adapt to global trade compliance requirements to ensure uninterrupted supply chains.

Product innovation continues at pace Murdock Manufacturing launched a sensor-activated eco-friendly fountain in January 2025, directly addressing single-use plastic reduction goals. Also in January, Zurn Elkay released upgraded Elkay Filtered Bottle Filling Stations with a sleeker design and double filter lifespan (6,000 gallons), reducing operational costs for clients. The integration of hygiene-focused robotics as seen with YEEDI’s M14 PLUS cleaning robot signals how adjacent technology trends are influencing water station design and maintenance solutions.

Technological Trends and Growth Opportunities in the Commercial Drinking Fountains Market

Touchless Hydration Systems Driving Hygiene and User Confidence

The adoption of touchless drinking fountains and bottle filling stations has accelerated in response to heightened hygiene concerns post-pandemic. Infrared sensors, motion-activated bottle fillers, and hands-free spouts are now considered essential in public and commercial hydration infrastructure. This trend is not only enhancing user safety but also improving accessibility for high-traffic environments such as schools, offices, airports, and healthcare facilities. Additionally, manufacturers are integrating real-time usage counters and filter replacement alerts to ensure water quality and optimize maintenance schedules. The touchless technology movement has also gained regulatory momentum, with many public institutions mandating its use in newly installed hydration points.

Sustainable Design and Plastic Waste Reduction Initiatives

The push to reduce single-use plastic consumption is fueling the rapid expansion of bottle filling stations and hybrid units. These installations provide an eco-friendly alternative by enabling users to refill reusable bottles with filtered, chilled water. Sustainability-driven procurement policies especially in educational institutions, government buildings, and corporate campuses are prioritizing units with low energy consumption compressors, lead-free components, and eco-friendly refrigerants. The integration of refill counters displaying “plastic bottles saved” also plays a critical role in raising awareness and promoting environmental responsibility. This aligns closely with corporate ESG commitments and public policy targets for waste reduction.

Smart Drinking Fountains with IoT Integration

The emergence of IoT-enabled hydration stations presents a high-value growth opportunity. These units feature connected monitoring systems that track usage, water temperature, and filter status in real time. Facility managers benefit from predictive maintenance alerts, while users enjoy consistent water quality and availability. The integration of cashless payment options in public spaces and AI-powered consumption analytics can further optimize placement strategies and usage efficiency. This technological shift is expected to see strong adoption in smart city projects, premium commercial spaces, and large institutional campuses.

Advanced Filtration and Water Quality Assurance

Consumer expectations for water purity are driving the adoption of multi-stage filtration systems in commercial drinking fountains. These systems go beyond basic sediment and chlorine removal, incorporating UV sterilization, activated carbon blocks, and reverse osmosis for premium-grade hydration. Healthcare facilities, high-end corporate environments, and hospitality venues are particularly receptive to these premium filtration solutions, positioning them as a competitive differentiator. Additionally, antimicrobial surface materials and self-sanitizing nozzles are becoming strong selling points for buyers in infection-sensitive environments.

Commercial Drinking Fountains Market Share Insights

Market Share by Product Type: Bottle Filling Stations Lead, Hybrid Units Gain Momentum

Bottle Filling Stations hold the largest share at 38%, driven by sustainability goals and strong public demand for touchless hydration. Their presence in educational institutions, transit hubs, and corporate spaces is expanding rapidly due to their ability to reduce single-use plastic waste while offering a quick, hygienic refill experience. Hybrid Units, combining both fountain and bottle filler functions, account for 25% of the market and are the fastest-growing category, appealing to facilities that require flexibility for different user preferences. Water Coolers maintain relevance in office environments but are losing share in public installations due to their lower throughput and lack of touchless capability. Traditional Drinking Fountains are declining in standalone form but remain a legacy fixture in older infrastructure.

Market Share by Application: Educational Institutions Lead Adoption, Healthcare on the Rise

Educational Institutions dominate with 30% market share, supported by hydration access policies and sustainability programs that prioritize bottle filling stations in schools and universities. Commercial Offices follow at 25%, where installations align with corporate wellness initiatives and modern workplace amenities. Healthcare Facilities are an expanding segment, with demand for antimicrobial, touchless units that meet stringent sanitation standards. Public Spaces & Parks are seeing steady investment in ADA-compliant, vandal-resistant units, while Retail & Hospitality venues adopt premium designs to enhance guest experiences. Industrial & Manufacturing applications remain limited but are gradually incorporating hydration stations in employee break areas to improve workplace wellness.

.png)

Competitive Landscape – Leading Innovators in Commercial Drinking Fountains

The market is shaped by global leaders delivering hygiene-focused, durable, and sustainable hydration solutions for public and commercial settings. Key players included are Zurn Elkay Water Solutions, Oasis International, Haws Corporation, Murdock Manufacturing, Cosmetal, Acorn Engineering Company, Sunroc Corporation, Elkay Manufacturing Company, Waterlogic Holdings Limited, Filtrine Manufacturing Company, Follett LLC, MasterFrost, Ebco Manufacturing Co., Watergen, OASE Living Water, Others.

Zurn Elkay Water Solutions – Comprehensive Hydration and Plumbing Systems

Zurn Elkay combines a wide portfolio of drinking fountains, filtered bottle fillers, sinks, and drainage systems. Its Elkay brand is well-known for advanced filtration, touchless operation, and sleek design. In May 2025, the company partnered with Erie's Public Schools to donate clean water solutions, reinforcing its ESG commitments. Products are increasingly connected-ready, enabling usage tracking and maintenance alerts. Zurn Elkay’s dual focus on sustainability and supply chain resilience positions it strongly in the retrofit and new construction segments.

Oasis International – Global Expertise in Clean Drinking Water Solutions

With over 115 years of history, Oasis is a leading manufacturer of drinking fountains, bottle fillers, and water coolers under brands such as Aqua Pointe®, Versacooler®, and Freshshield. The company emphasizes anti-bacterial, vandal-resistant, and outdoor-ready designs. Innovations like the Tilt 'N Tether filter change system improve maintenance efficiency. Serving over 80 countries, Oasis prioritizes public safety and water purity, with solutions for schools, healthcare, and municipal facilities.

Haws Corporation – Safety-Integrated Hydration Systems

Haws is a century-old leader in hydration stations, eyewash units, and safety showers. Its reputation rests on durability, safety compliance, and global service reach through 8,000+ distribution points. In July 2025, it renewed its SHARP recognition, affirming workplace safety excellence. Haws’ designs often integrate industrial safety with drinking water access, making them highly valued in manufacturing and public infrastructure projects.

Murdock Manufacturing – American-Made Durability and Sustainability

Murdock specializes in stainless steel fountains, bottle fillers, and outdoor hydrants, with customization options to fit specific project needs. In January 2025, it launched a sensor-activated model targeting sustainability and touch-free hygiene. Murdock’s products are widely used in parks, schools, and transit hubs, with a focus on long-lasting construction and compliance with NSF 42 and 53 filtration standards.

Global Water Solutions Ltd. – Technological Innovation in Water Hygiene

Global Water Solutions leads in pressure tanks, filtration systems, and anti-bacterial technology. Its Flow-Thru™ technology ensures constant water circulation, reducing Legionella risk a major concern for hospitals and high-traffic facilities. The August 2025 launch of the Anti-Legionella Flow-Thru™ Valve positions GWS as a technology-first innovator. The company caters to commercial buildings, off-grid sites, and recreational vehicle markets, combining safety, sustainability, and efficiency.

United States: Leadership in Touchless and Smart Drinking Fountain Solutions

The United States remains at the forefront of the commercial drinking fountains market, driven by rapid adoption of touchless hydration technology, advanced filtration, and IoT-enabled monitoring systems. Over 41% of new U.S. installations are now fully hands-free, a surge propelled by heightened hygiene awareness in commercial, educational, and public spaces. Additionally, 28% of these installations feature UV-C filtration systems, ensuring superior sanitation standards and appealing to institutional buyers prioritizing public health. The integration of smart sensors and IoT technology has increased by over 41%, enabling real-time water quality monitoring, usage analytics, and predictive maintenance capabilities that are becoming a competitive differentiator for manufacturers. Compliance with the Americans with Disabilities Act (ADA) continues to drive product innovation, with leading companies such as Elkay and Haws delivering a wide range of ADA-compliant models. Sustainability is another major market force, with U.S. buyers shifting toward bottle-filling stations to reduce plastic waste. Zurn Elkay Water Solutions’ “ezH2O” units are a notable example, receiving strong demand from corporations and municipalities alike. With companies like Oasis International exporting to over 80 countries, the U.S. has also established itself as a global manufacturing and distribution hub for commercial hydration solutions.

Germany: Regulatory-Driven Growth and Sustainable Public Infrastructure Expansion

Germany’s commercial drinking fountains industry is undergoing significant expansion, propelled by legislative mandates requiring municipalities to provide free public drinking water. This policy, aligned with the EU Drinking Water Directive, will result in at least 1,000 new public installations, reflecting the country’s commitment to climate adaptation and sustainability. Compliance with the updated EU quality standards addressing contaminants such as endocrine disruptors and microplastics has driven manufacturers to adopt materials engineered to inhibit microbial growth and prevent harmful substance leaching. The country’s environmental strategy actively supports reducing bottled water dependence, positioning drinking fountains as a core element of public health infrastructure. In urban environments, there is a notable demand for vandalism-resistant designs to ensure durability and functionality in high-traffic public spaces. German manufacturers, benefiting from a reputation for engineering excellence, are integrating compliance, sustainability, and robust design into their competitive strategies, making them influential players in the European market.

Japan: Pioneering Water Conservation and Disaster-Resilient Hydration Systems

Japan’s commercial drinking fountains market is defined by innovation in water conservation technology and disaster preparedness solutions. Companies like DG TAKANO have introduced the “Bubble90” nozzle, which delivers equivalent cleaning performance with just one-tenth of the water used by standard faucets a breakthrough for sustainability-conscious buyers. Japan is also a leader in atmospheric water generation, with the UNIDO-endorsed “POTORI” air-to-water technology enabling safe drinking water production in disaster zones and water-scarce regions. The country’s disaster-resilient infrastructure strategy has driven demand for off-grid drinking fountain systems capable of operating with minimal resources essential for emergency preparedness in earthquake-prone areas. These innovations position Japan as a high-value market for advanced, sustainable, and technically sophisticated drinking fountain solutions.

India: Government-Led Water Infrastructure Expansion Fueling Market Demand

India’s commercial drinking fountains sector is rapidly expanding under large-scale governmental initiatives like the Jal Jeevan Mission, which aims to provide safe, piped drinking water to all rural households by 2024. Complementing this, the “Drink from Tap” project in cities such as Puri is transforming urban hydration infrastructure. These programs, aligned with the ‘Viksit Bharat @2047’ vision, are accelerating the adoption of IoT-based smart water management systems for real-time monitoring, leak detection, and water quality control. Public-private partnerships are playing a significant role, exemplified by Desire Energy Pvt Ltd’s $19 million “Jal Prabal” project. Such collaborations not only expand infrastructure but also open opportunities for commercial-grade drinking fountains in public, corporate, and institutional settings. The market’s growth trajectory is strengthened by rising urbanization, increasing public health awareness, and a strong government focus on long-term water sustainability.

Australia: Large-Scale Investments in Water Security and Regional Accessibility

Australia’s commercial drinking fountains market is supported by substantial government funding through programs like the National Water Grid Fund, aimed at securing long-term water access and sustainability. The Queensland government has allocated A$1.14 billion in a single fiscal year for water infrastructure, with a decade-long plan totaling A$47.8 billion. These investments fund projects such as dams, pipelines, and water recycling plants, creating opportunities for public and commercial drinking fountain deployment across cities and remote areas. Regional and rural communities are a strategic focus, driving demand for off-grid, durable, and low-maintenance hydration solutions capable of operating under challenging environmental conditions. Australia’s market growth is thus anchored in government-backed infrastructure expansion and a strong emphasis on water conservation.

Commercial Drinking Fountains Market Report Scope

Commercial Drinking Fountains Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.5 Billion

|

|

Market Size (2034)

|

$2.7 Billion

|

|

Market Growth Rate

|

6.7%

|

|

Segments

|

By Product Type (Water Coolers (Pressure-Type, Bottled), Drinking Fountains (Wall-Mounted, Freestanding), Bottle Filling Stations, Hybrid Units), By Application (Educational Institutions, Commercial Offices, Healthcare Facilities, Public Spaces & Parks, Retail & Hospitality, Industrial & Manufacturing), By Material (Stainless Steel, Plastic, Concrete, Ceramic), By Distribution Channel (Offline (Direct Sales, Distributors), Online (E-commerce Platforms))

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Zurn Elkay Water Solutions, Oasis International, Haws Corporation, Murdock Manufacturing, Cosmetal, Acorn Engineering Company, Sunroc Corporation, Elkay Manufacturing Company, Waterlogic Holdings Limited, Filtrine Manufacturing Company, Follett LLC, MasterFrost, Ebco Manufacturing Co., Watergen, OASE Living Water, Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Commercial Drinking Fountains Market Segmentation

By Product

- Water Coolers

- Drinking Fountains

- Wall-Mounted

- Freestanding

- Bottle Filling Stations

- Hybrid Units

By Application

- Educational Institutions

- Commercial Offices

- Healthcare Facilities

- Public Spaces & Parks

- Retail & Hospitality

- Industrial & Manufacturing

By Material

- Stainless Steel

- Plastic

- Concrete

- Ceramic

By Distribution Channel

- Direct Sales

- Distributors

- E-commerce Platforms

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Commercial Drinking Fountains Market

- Zurn Elkay Water Solutions

- Oasis International

- Haws Corporation

- Murdock Manufacturing

- Cosmetal

- Acorn Engineering Company

- Sunroc Corporation

- Elkay Manufacturing Company

- Waterlogic Holdings Limited

- Filtrine Manufacturing Company

- Follett LLC

- MasterFrost

- Ebco Manufacturing Co.

- Watergen

- OASE Living Water

* List Not Exhaustive

Research Coverage

This report investigates the global Commercial Drinking Fountains Market, delivering breakthrough insights, analytical reviews, and strategic evaluations to support informed decision-making. It highlights innovations in touchless hydration, IoT integration, sustainable design, and advanced filtration that are reshaping the industry. The study by USDAnalytics examines leading manufacturers, competitive positioning, and key market drivers such as hygiene-focused infrastructure, plastic waste reduction policies, and large-scale public health initiatives. Covering over 25 countries, the analysis explores opportunities in educational, healthcare, corporate, and public infrastructure applications. It also assesses emerging revenue streams from hybrid units, smart city deployments, and disaster-resilient hydration systems. Featuring both historical data (2021–2024) and forecasts (2025–2034), the report is an essential resource for industry professionals aiming to navigate evolving regulations, sustainability mandates, and technology adoption trends. Scope includes- :

- Segmentation:

- By Product: Water Coolers, Drinking Fountains, Bottle Filling Stations, Hybrid Units

- By Application: Educational Institutions, Commercial Offices, Healthcare Facilities, Public Spaces & Parks, Retail & Hospitality, Industrial & Manufacturing

- By Material: Stainless Steel, Plastic, Concrete, Ceramic

- By Distribution Channel: Direct Sales, Distributors, E-commerce Platforms

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

- Historic Data: 2021–2024, with forecast data from 2025–2034.

- Companies: Analysis and profiles of 15+ global and regional market leaders.

Methodology

This report is based on a robust research framework combining primary and secondary sources to ensure accuracy, depth, and relevance. Primary research involved interviews with manufacturers, municipal planners, procurement managers, and sustainability officers, alongside field surveys in key markets. Secondary data was sourced from government publications, trade association reports, environmental compliance documents, and verified corporate disclosures. Data validation followed a triangulation process, cross-checking statistical models, expert insights, and observed adoption patterns. Forecasting (2025–2034) applied time-series analysis, market diffusion modeling for touchless and hybrid systems, and scenario planning for regulatory changes and technological adoption rates. This methodology ensures a data-rich, actionable resource for market participants.