Conformal Coatings Market Size, Electronics Miniaturization, and High-Reliability Protection Demand

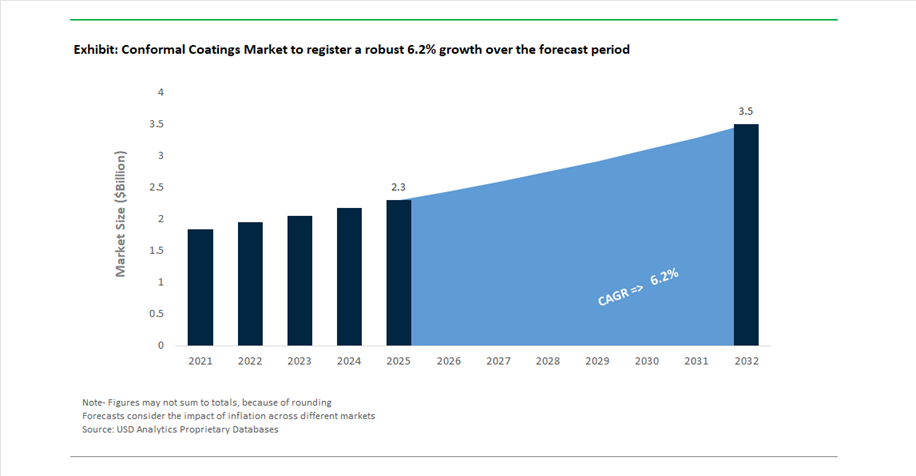

The global conformal coatings market was valued at $2.3 billion in 2025 and is projected to grow at a CAGR of 6.2% between 2025 and 2032, reaching $3.5 billion by 2032. This growth is driven by increasing demand across consumer electronics, automotive electronics, aerospace systems, industrial automation, and medical devices, where conformal coatings are critical for protecting printed circuit boards (PCBs) and sensitive components from moisture, dust, chemicals, thermal stress, and electrical interference.

A key structural driver is the rapid advancement of electronics miniaturization and high-density PCB design, which requires ultra-thin, uniform coatings capable of maintaining performance in compact and complex assemblies. The proliferation of electric vehicles (EVs), autonomous driving systems, 5G infrastructure, and IoT-enabled devices is significantly expanding the application scope for conformal coatings, particularly in environments exposed to extreme temperatures, humidity, and vibration.

Material innovation is reshaping the market, with increasing adoption of silicone, acrylic, urethane, and parylene-based coatings tailored for specific performance requirements such as thermal stability, flexibility, dielectric strength, and chemical resistance. Additionally, the shift toward UV-curable, low-VOC, and bio-based formulations is aligning with sustainability goals while improving processing efficiency and reducing curing times in high-volume electronics manufacturing.

Advanced Electronics Integration, AI-Driven Inspection, and Sustainable Coating Technologies Reshaping the Market

The conformal coatings market is evolving rapidly through strategic acquisitions, advanced material innovation, and automation-driven manufacturing improvements. In February 2026, Henkel announced its €2.1 billion acquisition of Stahl, strengthening its capabilities in specialty coatings for flexible substrates and electronics applications, particularly for sensors and flexible circuits used in automotive and advanced electronics systems.

Equipment integration and process optimization are becoming critical differentiators. Nordson Electronics Solutions expanded its North American partnership in March 2026, offering integrated solutions that combine precision dispensing systems, plasma treatment, and soldering technologies for PCB manufacturing. Additionally, Nordson’s AI-driven inspection systems unveiled at APEX EXPO 2026 enable real-time detection of coating defects such as voids, bubbles, and thickness inconsistencies, supporting the industry’s shift toward zero-defect manufacturing in high-reliability sectors like autonomous vehicles and medical electronics.

Material innovation is advancing into highly specialized and emerging applications. Dymax’s launch of low-outgassing conformal coatings (March 2026) addresses the stringent requirements of space electronics and low Earth orbit (LEO) satellites, ensuring reliability under vacuum and thermal stress conditions. The company also introduced IBOA-free formulations, reducing skin sensitization risks and making them suitable for wearable medical devices and consumer electronics.

Sustainability and bio-based solutions are gaining traction. Electrolube’s introduction of a bio-based conformal coating (2025–2026), specifically designed for EV battery management systems, represents a significant step toward reducing the environmental footprint of electronics manufacturing. This innovation combines thermal stability and chemical resistance with lower reliance on fossil-fuel-based materials.

Upstream investments in advanced materials are reinforcing supply capabilities. Shin-Etsu Chemical’s ¥83 billion investment in a new materials plant (January 2026) supports the production of high-purity silicone-based coatings and encapsulants, critical for semiconductor and automotive applications. Meanwhile, Arkema’s integration of Dow’s laminating adhesives unit enhances its polymer portfolio for thin-film and barrier coatings, while H.B. Fuller’s acquisition of ND Industries expands its footprint in functional coatings for electronics and aerospace applications.

Industry consolidation and strategic realignment are further shaping competitive dynamics. Chase Corporation’s integration under KKR (2024–2025) has enabled the company to streamline its global manufacturing network, accelerating delivery of acrylic and urethane conformal coatings to high-volume electronics markets.

Reliability Standards Tightening for Harsh Electronics Environments

The conformal coatings industry is undergoing a significant upgrade in qualification requirements following the release of IEC 61086-2024. This updated standard introduces a more rigorous testing framework designed to address the increasing failure rates of electronic assemblies operating in aggressive industrial, automotive, and outdoor environments.

A central component of the update is the mandatory adoption of Mixed Flowing Gas (MFG) testing, which exposes coated assemblies to corrosive gases such as H₂S, NO₂, SO₂, and Cl₂ over extended durations. Class 2 and Class 3 coatings must now withstand a minimum of 14 days of exposure without dendritic growth or catastrophic failure, significantly raising the qualification threshold compared to previous standards.

Humidity resistance requirements have also intensified. Coatings must maintain a surface insulation resistance exceeding 10⁸ ohms after prolonged exposure to 85°C and 85% relative humidity conditions for 21 days. This requirement is particularly challenging for legacy acrylic coatings, many of which require reformulation or increased film thickness to remain compliant.

Field validation data indicates that coatings meeting these updated protocols demonstrate up to 40% reduction in corrosion of fine-pitch components, directly improving reliability in high-density circuit boards. Additionally, adhesion performance standards now require coatings to retain a 5B rating even after extreme thermal cycling from −65°C to +125°C, reinforcing the shift toward high-performance materials such as silicones and parylenes.

Isocyanate Restrictions Accelerating Safer and Faster-Curing Chemistries

The enforcement of REACH Entry 74 restrictions on diisocyanates has reached a mature phase, triggering a broad reformulation wave across polyurethane-based conformal coatings. By 2026, a substantial portion of the European electronics manufacturing ecosystem has transitioned away from traditional isocyanate-containing systems to avoid regulatory complexity and occupational safety burdens.

The regulation targets formulations with ≥0.1% monomeric diisocyanate content, requiring mandatory worker training and certification for handling. To bypass these constraints, approximately 80% of Tier 1 manufacturers have adopted isocyanate-free or “safe-to-use” alternatives, fundamentally reshaping the competitive landscape.

This transition is delivering measurable environmental and operational benefits. VOC emissions have been reduced by 50% to 70% through the adoption of high-solids, solvent-free, and UV-curable systems. At the same time, occupational health outcomes have improved, with reported cases of polyurethane-related asthma declining by over 20% following full regulatory implementation.

One of the most impactful innovations is the adoption of UV-cure acrylated urethane systems, which drastically reduce processing time. Traditional thermal curing processes requiring hours in convection ovens are being replaced by LED-UV curing cycles completed in seconds, enabling high-throughput manufacturing and reduced energy consumption.

Ultra-Low-Viscosity Coatings Enabling Electronics Miniaturization

The rapid evolution of 5G infrastructure and IoT devices is driving demand for ultra-low-viscosity (ULV) conformal coatings, specifically engineered to protect increasingly compact and densely populated electronic assemblies. These coatings, with viscosities below 20 cPs, are enabling new levels of precision in electronic protection.

A key advantage of ULV coatings is their ability to penetrate extremely tight geometries. They can flow into gaps as small as 25 microns beneath components such as BGAs and QFNs, providing comprehensive coverage where traditional coatings fail. This is critical for maintaining reliability in high-density circuit designs where even minor moisture ingress can lead to failure.

Material efficiency is another differentiator. ULV coatings achieve effective protection at film thicknesses of just 15–25 microns, reducing coating weight by approximately 35%. This is particularly valuable in applications such as aerospace electronics and portable IoT devices, where weight and space constraints are critical design parameters.

From a manufacturing perspective, advanced dispensing technologies enable transfer efficiencies of up to 98%, minimizing material waste and improving process control in automated production lines. Additionally, ULV coatings exhibit favorable dielectric properties, maintaining signal integrity at high frequencies such as millimeter-wave (mmWave) 5G applications.

Thermally Conductive Coatings Addressing Power Density Challenges

The increasing power density of modern electronics—particularly in electric vehicles (EVs), fast-charging systems, and GaN-based power devices—is creating a need for conformal coatings that actively manage heat dissipation. Thermally conductive conformal coatings are emerging as a solution that integrates protection with thermal management.

Unlike conventional coatings, which act as thermal insulators, these advanced materials incorporate ceramic fillers such as aluminum oxide or boron nitride to achieve thermal conductivities in the range of 0.5 to 1.5 W/m·K, significantly higher than the 0.15–0.2 W/m·K typical of standard coatings.

The performance impact is substantial. Application of thermally conductive coatings on power components such as MOSFETs can reduce junction temperatures by 10°C to 15°C. According to reliability models such as the Arrhenius equation, this reduction can potentially double component lifespan, making these coatings critical for long-life, high-reliability applications.

Importantly, these coatings maintain high dielectric strength (>15 kV/mm), ensuring electrical insulation even in high-voltage environments such as EV battery management systems. This dual functionality—thermal conduction and electrical insulation—is a key enabler for next-generation power electronics.

Advances in application techniques, including selective robotic coating, allow targeted deposition on thermal hotspots while preserving functionality in connectors and sensitive areas. This precision further enhances system-level performance.

Acrylic Conformal Coatings Lead Market with 34% Share Driven by Reworkability and High-Volume Electronics Manufacturing

Material Analysis: Acrylic (AR) Coatings Dominate with Fast Cure and Cost-Effective PCB Protection

Acrylic (AR) conformal coatings account for a leading 34.0% share of the conformal coatings market in 2025, driven by their unmatched ease of application, rapid curing, and reworkability in high-volume electronics production. These coatings, compliant with IPC-CC-830 and MIL-I-46058C standards, are widely used across consumer electronics, automotive control units, and industrial PCBs due to their ability to be easily removed using common solvents such as acetone or xylene—an essential feature for repairing high-value circuit boards. Acrylic coatings also support fast manufacturing throughput, with UV-curable systems achieving cure times of 2–10 seconds and solvent-borne variants drying within minutes, enabling efficient inline production. Additionally, they offer strong dielectric strength (>1200 V/mil) and moisture resistance, making them ideal for humid and corrosive environments. Despite limitations at high temperatures, acrylic coatings remain the default choice for cost-sensitive, high-volume conformal coating applications.

Consumer Electronics Segment Leads Conformal Coatings Market with 38% Share Driven by Smartphone and Wearable Device Demand

End-Use Industry Analysis: High-Volume Portable Electronics Drive Conformal Coating Adoption

The consumer electronics segment dominates the conformal coatings market with a 38.0% share in 2025, fueled by the massive production of smartphones, wearables, and smart home devices requiring advanced environmental protection. With global smartphone shipments reaching 1.2–1.4 billion units annually, conformal coatings are essential for achieving IP67/IP68 water resistance, protecting internal PCBs from moisture, corrosion, and electrical failure. Wearables such as smartwatches, earbuds, and fitness trackers further drive demand due to constant exposure to sweat, humidity, and temperature fluctuations, while smart appliances and home automation devices require coatings for durability in challenging environments. The market is evolving toward a combination of ultra-thin nano-coatings for splash resistance and traditional acrylic or parylene coatings for full immersion protection, depending on performance requirements. Increasing miniaturization and high-density PCB designs are also driving demand for precise, high-performance coatings, reinforcing consumer electronics as the largest segment in the global conformal coatings market.

Conformal Coatings Market Competitive Landscape Driven by Silicone Chemistry, UV-Curable Technologies, and Electronics Reliability

The conformal coatings market is highly innovation-driven, led by players focusing on silicone coatings, UV-curable systems, and low-VOC formulations. Growth is fueled by EV electronics, 5G infrastructure, and consumer devices, with emphasis on dielectric protection, thermal stability, and compliance with stringent environmental regulations.

Henkel Advances VOC-Free Conformal Coatings with High-Performance Loctite Portfolio

Henkel AG & Co. KGaA is setting benchmarks in sustainable conformal coatings with the launch of Loctite Stycast UV 7998 in 2026, a solvent-free, UL 94 V-0 rated coating delivering 40% lower CO2 emissions. Its Loctite portfolio features self-leveling and superior wetting properties, reducing material usage by up to four times while maintaining dielectric performance. The company is expanding its footprint in EV electronics and home appliances, where reliability under thermal shock is critical. Henkel’s strong R&D network emphasizes REACH and RoHS compliance, ensuring regulatory alignment across global markets. Its focus on environmentally friendly coatings and advanced electronics protection enhances its competitive positioning. The company continues to lead in high-performance, low-VOC conformal coating solutions.

Dow Strengthens Silicone Conformal Coatings Leadership for 5G and Automotive Electronics

Dow Inc. remains a global leader in silicone conformal coatings, leveraging vertical integration to stabilize supply and pricing amid raw material volatility. Its coatings are engineered for 5G telecom infrastructure, offering protection against extreme humidity and corrosive pollutants, extending equipment lifespan up to 100,000 hours MTBF. The company is expanding silicone monomer production capacity across key regions to support demand in Asia-Pacific and North America. Its DOWSIL™ series is widely used in automotive electronics, providing stress relief for sensitive solder joints in both ICE and EV platforms. Dow’s focus on high-reliability coatings supports applications in telecommunications, automotive, and industrial electronics. Its integrated supply chain and material expertise reinforce its leadership in silicone-based coatings.

Shin-Etsu Expands High-Purity Silicone Coatings for ADAS and Renewable Energy Systems

Shin-Etsu Chemical Co., Ltd. is investing $700 million to expand silicone production capacity by 15–20%, targeting demand from ADAS and autonomous vehicle electronics. The company leads in high-purity silicone chemistry, offering advanced moisture barrier coatings that prevent electrochemical migration in dense PCB assemblies. Its development of low-viscosity, fast-curing silicone resins enables high-speed robotic dispensing without thermal curing ovens, improving manufacturing efficiency. Shin-Etsu is also a key supplier to the renewable energy sector, protecting power electronics from harsh environmental conditions such as salt mist and industrial corrosion. Its focus on advanced materials innovation supports high-reliability electronics applications. The company’s specialization in silicone chemistry strengthens its competitive edge in conformal coatings.

Dymax Enhances UV-Curable Coatings with Dual-Cure Technology and Safety Innovations

Dymax Corporation is advancing UV/LED light-curable conformal coatings with new formulations demonstrated at APEX EXPO 2026, eliminating IBOA to improve operator safety. Its Total Process approach integrates SpeedMask® resins with BlueWave® LED curing systems, enabling rapid masking, coating, and curing within seconds. Dymax specializes in dual-cure technology, ensuring full polymerization in shadow areas of complex PCB designs. Its 9482 series coatings offer fluorescing properties and UL 94 V-0 ratings, supporting inspection and high-level circuit protection in aerospace and medical electronics. The company’s focus on speed, safety, and precision enhances manufacturing efficiency. Dymax continues to lead in advanced UV-curable conformal coating technologies.

H.B. Fuller Expands Global Electronics Coatings Presence with HumiSeal® Portfolio

H.B. Fuller Company, strengthened by the integration of Chase Corporation, commands a strong position in the conformal coatings market through its HumiSeal® brand. The company focuses on acrylic and urethane coatings, which together account for over 50% of the material market share in electronics protection. Its reworkable acrylic coatings are widely used in consumer electronics, supporting repairability requirements in smartphones and wearable devices. H.B. Fuller is expanding technical support capabilities in India and Vietnam, aligning with global OEM strategies to diversify manufacturing beyond China. The company is well-positioned to capture growth in the expanding $2.42 billion conformal coatings market. Its focus on localized support and high-performance materials strengthens its competitive presence.

Nordson Drives Precision Coating with Advanced Selective Coating Equipment and Digital Traceability

Nordson Corporation leads in selective conformal coating equipment, enabling precise material application and reducing waste by up to 30% compared to manual processes. Its ASYMTEK Select Coat® SL-1040 system introduces advanced flow control for green chemistries and particle-filled coatings. Nordson’s systems integrate real-time data logging, meeting traceability requirements for aerospace and medical device manufacturing. Its ultrasonic sensor technology ensures consistent coating thickness across high-volume production runs with minimal maintenance. The company’s focus on automation, precision, and digital integration enhances manufacturing reliability. Nordson’s equipment-driven approach plays a critical role in advancing conformal coating application technologies.

China Conformal Coatings Market: High-Volume Electronics Manufacturing and Green Transition Driving Dominance

China remains the global epicenter for conformal coatings, supported by its massive electronics manufacturing base and aggressive environmental policies. By late 2025, the country achieved a 40% increase in adoption of waterborne and solvent-free UV coatings, particularly across major hubs like the Pearl River Delta, aligning with stricter VOC regulations.

Demand is being driven by multiple high-growth sectors. The rapid rollout of 5G infrastructure is boosting consumption of silicone-based coatings for base stations, while the New Energy Vehicle (NEV) boom is accelerating use of polyurethane and hybrid coatings for battery management systems (BMS), ensuring long-term durability under thermal stress. Additionally, breakthroughs in nanocomposite coatings are improving heat dissipation in high-power electronics, and the integration of automated selective coating robots is enhancing consistency and reducing VOC exposure.

United States Conformal Coatings Market: Semiconductor Expansion and High-Reliability Applications Driving Innovation

The United States market is defined by high-performance applications in aerospace, defense, and medical electronics. The expansion of semiconductor mega-fabs under the CHIPS Act is significantly increasing demand for parylene conformal coatings, particularly for cleanroom-grade equipment and advanced chip packaging.

Innovation is also driven by miniaturization and reliability requirements. The adoption of Atomic Layer Deposition (ALD) coatings in wearable medical devices enables moisture-proof protection at extremely small scales (≈5 mm devices). Defense and aerospace sectors are specifying coatings that meet MIL-I-46058C and IPC-CC-830 standards, ensuring performance in extreme environments. Additionally, the reshoring of EV supply chains is driving demand for silicone coatings in power inverters, while regulatory pressure from CARB is accelerating the transition toward UV-LED curable, low-VOC systems.

South Korea Conformal Coatings Market: UV-Curing Leadership and Battery Innovation Driving Efficiency

South Korea is a global leader in high-speed conformal coating technologies, particularly in EV batteries and display electronics. Nearly 80% of display-related coating lines have transitioned to UV-LED curing, reducing production cycles from minutes to seconds.

The EV sector is a major growth driver. The widespread adoption of fire-retardant silicone coatings is enhancing safety in high-density battery modules by mitigating thermal runaway risks. Advanced manufacturing technologies—such as vision-guided robotic coating systems—are achieving near zero-defect rates for OLED driver boards. Additionally, strong growth in 5G RF components and medical device exports is increasing demand for ultra-thin, high-precision conformal coatings, positioning South Korea as a leader in efficiency and innovation.

Germany Conformal Coatings Market: REACH Compliance and Automotive Reliability Driving Sustainability Leadership

Germany sets the benchmark for eco-compliant and high-reliability conformal coatings, particularly in industrial and automotive applications. The industry has achieved a ~90% phase-out of PFAS-based additives, ahead of EU regulatory deadlines.

The automotive sector is a key driver, with demand for polycarbonate-based polyurethane coatings ensuring up to 15-year durability for engine control units (ECUs) under extreme conditions. Germany is also pioneering Digital Product Passports (DPP), enabling full traceability of coating materials. Advanced manufacturing practices, including IoT-enabled spray systems, are optimizing resin viscosity in real time and reducing waste by ~18%. Additionally, growth in renewable energy is driving demand for epoxy coatings in offshore wind and industrial automation systems.

Japan Conformal Coatings Market: Nanotechnology Precision and Semiconductor Integration Driving Advanced Applications

Japan’s conformal coatings market is defined by nanoscale precision and semiconductor innovation. The commercialization of nanostructured Parylene-N films provides superior gas barrier properties for advanced lithography equipment, supporting next-generation chip manufacturing.

Technological advancements are also focused on multifunctionality. The use of viscoelastic silicone hybrid coatings in automotive sensors provides both environmental protection and vibration damping. Additionally, the growth of remote healthcare devices is driving demand for antimicrobial conformal coatings, while government-backed semiconductor investments are increasing demand for ultra-high-purity coating systems with impurity levels below 1 ppb. These developments reinforce Japan’s leadership in high-precision conformal coating technologies.

India Conformal Coatings Market: Electronics Manufacturing Expansion and PLI Support Driving High Growth

India is emerging as a key growth market for conformal coatings, supported by strong government incentives and expanding electronics manufacturing. Under the PLI 2.0 scheme, significant investments are being directed toward domestic production of coating materials and electronics assembly.

The market is driven by diverse applications. Rapid growth in smartphone manufacturing is increasing demand for quick-dry acrylic coatings, while the expansion of Vande Bharat trains is boosting adoption of fire-retardant coatings for onboard electronics. Renewable energy projects are also contributing, with demand for UV-stable coatings in solar inverter circuits. Additionally, domestic production of waterborne PU dispersions (PUDs) is reducing reliance on imports, while applications in agritech—such as coatings for smart irrigation sensors—are expanding the market’s scope.

Conformal Coatings Market Report Scope

Conformal Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.3 Billion

|

|

Market Size (2032)

|

$3.5 Billion

|

|

Market Growth Rate

|

6.2%

|

|

Segments

|

By Material (Acrylic (AR), Polyurethane, Silicone (SR), Epoxy (ER), Parylene (XY), Specialty and Hybrids), By Technology (UV-Curable, Solvent-Borne, Water-Borne, Secondary Cure Mechanisms), By Operation (Automated, Manual Spraying, Dipping, Brushing, Chemical Vapor Deposition (CVD)), By End-Use Industry Vertical (Automotive, Consumer Electronics, Aerospace and Defense, Medical Devices, Telecommunications and Industrial)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, The Dow Chemical Company, H.B. Fuller Company, Chase Corporation, Shin-Etsu Chemical Co., Ltd., Electrolube, Dymax Corporation, Altana AG, 3M Company, Illinois Tool Works Inc., MG Chemicals, KISCO Ltd., CHT Group, Panacol-Elosol GmbH, Sika AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Conformal Coatings Market Segmentation

By Material

- Acrylic (AR)

- Polyurethane

- Silicone (SR)

- Epoxy (ER)

- Parylene (XY)

- Specialty and Hybrids

By Technology

- UV-Curable

- Solvent-Borne

- Water-Borne

- Secondary Cure Mechanisms

By Operation

- Automated

- Manual Spraying

- Dipping

- Brushing

- Chemical Vapor Deposition (CVD)

By End-Use Industry Vertical

- Automotive

- Consumer Electronics

- Aerospace and Defense

- Medical Devices

- Telecommunications and Industrial

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Conformal Coatings Market

- Henkel AG & Co. KGaA

- The Dow Chemical Company

- H.B. Fuller Company

- Chase Corporation

- Shin-Etsu Chemical Co., Ltd.

- Electrolube

- Dymax Corporation

- Altana AG

- 3M Company

- Illinois Tool Works Inc.

- MG Chemicals

- KISCO Ltd.

- CHT Group

- Panacol-Elosol GmbH

- Sika AG

*- List not Exhaustive