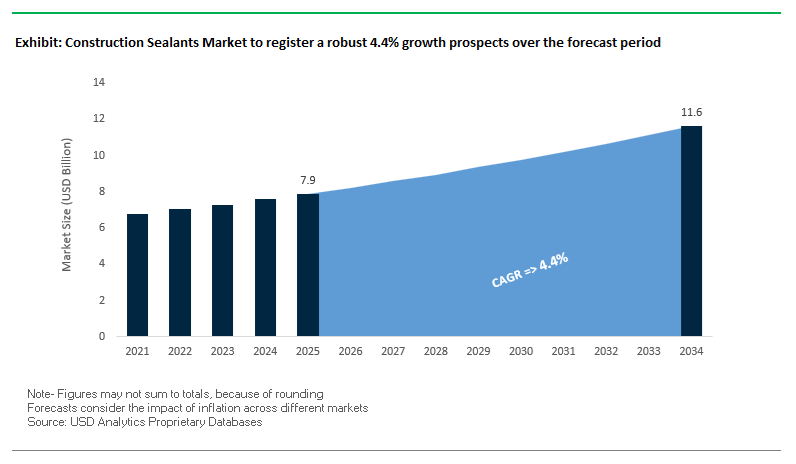

The Global Construction Adhesives and Sealants Market is projected to grow from $23.6 billion in 2025 to $56.6 billion by 2034, registering an CAGR of 10.2%. This robust expansion is underpinned by surging investments in infrastructure modernization, smart urbanization, and sustainable construction materials across developed and emerging economies. The market’s evolution highlights the accelerated shift toward high-performance, low-VOC, and elastic bonding technologies, replacing mechanical fixings and traditional fasteners with next-generation polymer-based adhesive systems.

High-performance elastic adhesives such as polyurethane (PU), silyl-modified polymers (SMP), and hybrid silane formulations are transforming façade engineering and flooring applications by ensuring stronger, lighter, and more flexible structures. Meanwhile, silicone-based sealants continue to dominate the global revenue share due to their unmatched UV resistance, thermal stability, and movement capability, particularly in glazing, structural façade joints, and curtain wall systems. As climate variability and energy efficiency demands intensify, construction projects increasingly rely on multi-functional sealants that combine weatherproofing, fire protection, and aesthetic flexibility.

Sustainability remains the defining force in product innovation. The rise of bio-based structural adhesives, derived from soy, lignin, and other renewable polymers, is revolutionizing the use of Cross-Laminated Timber (CLT) and engineered wood. These formulations offer structural-grade strength with lower embodied carbon, aligning with global initiatives like the EU Green Deal and LEED Platinum certification goals. Simultaneously, low-VOC and bitumen-free adhesives are becoming mandatory across public procurement projects in Europe and North America, ensuring compliance with GREENGUARD, EMICODE, and EN ISO 16000 air quality benchmarks.

Key Industry Insights

- Low-VOC Innovation Surge: Major brands are developing water-based, solvent-free adhesives to meet green building regulations and indoor air quality standards.

- Silicone Sealant Dominance: Silicone-based systems remain the preferred choice for facade sealing and high-rise glazing due to UV, weather, and thermal resistance.

- Elastic Bonding Trend: One-component polyurethane and hybrid systems are replacing mechanical fixings, providing safer, faster, and more flexible bonding in modern infrastructure.

- Bio-Based Breakthrough: Soy and lignin-based structural adhesives are gaining ground in engineered wood (CLT, LVL) applications for sustainable construction.

- Fire-Protection Growth: Increasing integration of fire-rated and elastomeric sealants in public infrastructure and commercial projects is redefining product standards.

The global construction adhesives and sealants industry is experiencing a convergence of sustainability mandates, large-scale infrastructure investments, and breakthrough polymer innovations. The period between July and October 2025 saw a surge of strategic product launches and acquisitions, marking a decisive shift toward low-monomer, fire-safe, and energy-efficient adhesive systems.

In August 2025, Henkel reported strong performance in its Adhesive Technologies division, highlighting strategic focus on global megatrends such as urbanization, sustainability, and digitalization. Its continuous investment in smart adhesive chemistry reinforces its leadership across both DIY construction and industrial-grade bonding applications. Similarly, Sika AG completed the acquisition of a major fire protection and sealing solutions firm in September 2025, strengthening its capabilities in fire-rated joint sealing, structural fire-stopping, and building envelope durability—a move that strategically positions it within the high-demand commercial and infrastructure construction sectors.

October 2025 was a landmark month for technological innovation. H.B. Fuller introduced a new generation of polyurethane (PUR) hot-melt adhesives designed for commercial roofing and weatherproofing, enabling rapid curing, superior bonding strength, and improved performance under UV exposure. The same month, Dow launched a next-generation silicone structural glazing sealant for high-rise buildings, featuring up to ±50% movement capability and compatibility with energy-efficient glass systems—a vital innovation for net-zero building projects. Meanwhile, Arkema (Bostik) unveiled low-monomer polyurethane flooring adhesives to comply with upcoming EU REACH safety regulations, underscoring the industry's pivot toward health-conscious formulations.

Regional expansion has also been pivotal. Wacker Chemie AG’s announcement in October 2025 to expand silicone sealant production in Asia signals growing demand for durable and UV-resistant silicone materials in emerging markets. Likewise, Mapei’s August 2025 involvement in a major European rail infrastructure project illustrates how advanced cement additives and structural adhesives are becoming integral to tunneling, concrete repair, and waterproofing systems.

From a policy standpoint, the September 2025 U.S. Department of Transportation (DOT) report emphasized the growing requirement for elastomeric sealants in infrastructure projects, driven by new federal longevity standards for bridges and road repairs. Additionally, Sika’s July 2025 launch of Purform® technology for ultra-low monomer polyurethane systems ensures compliance with future regulatory exemptions under the REACH framework, positioning the company as a pioneer in occupational safety and formulation efficiency.

The industry is experiencing an accelerated migration toward low-VOC and solvent-free construction adhesives and sealants, a trend rooted in increasingly stringent regulatory frameworks and sustainability goals. The shift is catalyzed by the demand for healthier indoor environments, energy-efficient buildings, and green certification compliance under programs like LEED, BREEAM, and WELL.

According to the European Chemicals Agency (ECHA), regulatory targets aim for a 40% further reduction in VOC emissions between 2020 and 2030, following prior decade-wide cuts. The forces adhesive formulators to replace traditional solvent-based polymers with waterborne, reactive hot-melt, and high-solids alternatives that comply with emerging air quality thresholds. Major corporations are responding decisively—one global leader in adhesive technologies has committed over $500 million in R&D investment to scale the production of next-generation eco-friendly formulations, including high-performance, water-based adhesives tailored for building and infrastructure applications.

Similarly, bio-based innovation is becoming a competitive differentiator. A major multinational recently unveiled a construction-grade adhesive line containing up to 90% renewable raw materials, enabling contractors to meet green procurement requirements while maintaining performance parity with petroleum-derived products. The expansion of environmentally certified products is also directly linked to end-user adoption, as architects and developers increasingly specify low-VOC sealants to achieve maximum Indoor Environmental Quality (IEQ) credits in LEED-certified projects.

Hybrid polymer sealants—particularly MS Polymer (Modified Silane) and SPUR (Silyl-Terminated Polyurethane) chemistries—are redefining performance standards across the construction sector. Combining the mechanical resilience of polyurethane with the weatherability and UV resistance of silicones, these hybrid systems are the go-to materials for facade sealing, expansion joints, and interior finishing applications that demand durability, aesthetic compatibility, and safety.

Laboratory testing consistently demonstrates that premium hybrid polymer sealants exhibit elastic recovery exceeding 70% and movement capability up to ±25%, placing them in the “high-performance” classification under ISO 11600 and ASTM C920. The ensures long-term flexibility in high-movement joints—such as curtain walls and precast facades—where conventional silicones or polyurethanes often fail due to cracking or adhesion loss. Case studies further confirm that hybrid sealants achieve primer-less adhesion across substrates like concrete, aluminum, wood, and glass, with tensile strength values of ≥1 MPa, substantially reducing application time and labor costs.

From an environmental and health standpoint, MS Polymer-based sealants are solvent- and isocyanate-free, offering enhanced on-site safety for applicators while supporting global sustainability objectives. The elimination of harmful monomers also simplifies compliance with emerging safety regulations, making hybrid sealants the preferred option for international high-rise, infrastructure, and institutional projects where safety certifications are mandatory. The proliferation of high-performance hybrid sealants not only elevates construction productivity but also solidifies their dominance in the modern building materials ecosystem.

The worldwide commitment to energy-efficient renovation and decarbonization represents a multi-decade growth driver for the construction adhesives and sealants sector. Aging building infrastructure—especially in developed regions—is the focal point of government-funded retrofitting programs aimed at reducing carbon emissions and improving airtightness through superior sealing materials.

In the United States, the Department of Energy’s Weatherization Assistance Program (WAP) and related clean energy initiatives have allocated billions in funding to promote air sealing, caulking, and insulation—activities that can cut residential energy losses by 25–40%. These programs directly increase demand for high-performance air barrier sealants and foam-based adhesives, which are essential for weatherproofing and energy conservation in both residential and commercial buildings. Similarly, in Europe, the EU’s Renovation Wave Strategy aims to double annual building renovation rates by 2030, creating an enormous demand for airtight, flexible, and thermally resilient sealants capable of sustaining long-term performance.

Industry data indicates that energy losses through poorly sealed joints, interfaces, and penetrations remain one of the primary causes of building inefficiency, underscoring the value of elastomeric, low-permeance sealants engineered to maintain airtightness over decades. Manufacturers responding to the retrofit surge are developing multi-functional sealant systems that combine adhesion, flexibility, and moisture resistance, allowing them to meet both energy efficiency and durability benchmarks. The segment is poised to be a key revenue pillar as governments and private sector stakeholders scale up renovation and weatherization initiatives globally.

The rise of Modern Methods of Construction (MMC)—including modular, prefabricated, and mass timber (CLT and Glulam) building systems—is reshaping how adhesives and sealants are designed, applied, and tested. These advanced construction techniques demand materials that support fast curing, structural integrity, and factory-optimized performance, opening up new growth avenues for manufacturers of high-performance bonding systems.

In modular production facilities, the efficiency imperative is paramount. Next-generation polyurethane (PUR) adhesives have been optimized for cold-press curing cycles of just 30–120 minutes, achieving demolding strength rapidly to enable continuous production flow. For Cross-Laminated Timber (CLT) and engineered wood applications, manufacturers are developing PUR adhesive systems that not only offer structural bonding but also enhance fire performance, achieving a charring rate of approximately 0.65 mm/min—nearly equivalent to unbonded solid wood—while maintaining integrity under load.

In addition, with national governments such as the UK and Canada mandating a significant share of public housing and infrastructure projects to use off-site modular methods, adhesive and sealant suppliers are strategically positioned to serve the expanding market. Factory-controlled MMC processes require high-consistency, pre-tested bonding materials that can guarantee dimensional stability, thermal resistance, and long-term joint performance under varying environmental loads. As MMC adoption accelerates globally, construction adhesives and sealants engineered for modular and mass timber applications are expected to become indispensable in sustainable and rapid-build systems, reinforcing the industry’s role in shaping the future of next-generation construction.

Construction Adhesives & Sealants Market Share Insights, 2025-2034

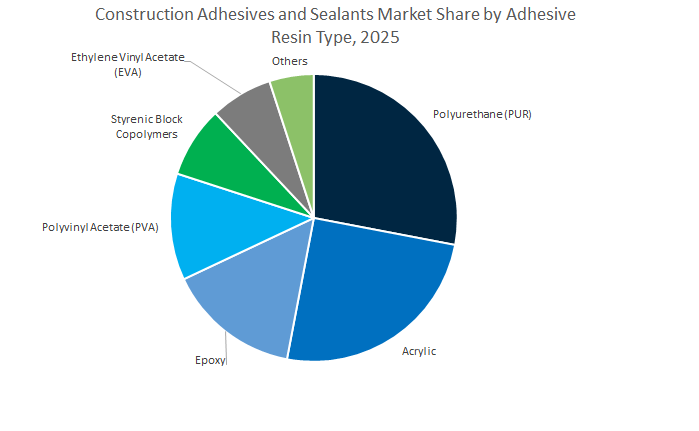

Polyurethane (PUR) adhesives dominate the global construction adhesives and sealants industry, accounting for an estimated 27.8% market share in 2025. Their supremacy stems from their unique balance of strength, elasticity, and chemical resistance, making them suitable for both structural and flexible bonding applications. Polyurethane formulations are extensively used in structural glazing, panel bonding, expansion joints, and waterproofing systems, offering superior adhesion to diverse substrates such as concrete, metal, glass, and plastics. Their ability to perform under dynamic load and environmental stress—without cracking or delaminating—has cemented their leadership in high-performance façade and roofing systems. In addition, advancements in hybrid polyurethane technologies (such as silyl-modified PUR systems) are enabling low-VOC, moisture-curing solutions with enhanced weatherability, supporting sustainability goals in modern construction. The broad adoption of polyurethane adhesives and sealants in both residential and infrastructure projects highlights their indispensable role in achieving durability, efficiency, and energy performance across the built environment.

Residential construction remains the largest and most influential end-use segment, accounting for 38.9% of total market share in 2025. The demand is powered by rapid urbanization, population growth, and sustained investment in new housing and renovation projects worldwide. Adhesives and sealants are used in nearly every stage of residential construction—from foundation waterproofing and flooring to panel bonding, tile fixing, insulation, and window sealing. Water-based acrylic and polyurethane formulations dominate this space due to their combination of performance, safety, and affordability. Moreover, the rise of green building materials and energy-efficient housing has increased demand for low-VOC and durable products that support airtightness and thermal performance. The growing popularity of DIY home renovation further contributes to volume growth, making the residential segment both the largest and most diverse market for construction adhesives and sealants.

Non-residential construction—including commercial buildings, hospitals, and institutional facilities—commands a substantial share of the market and serves as a key pillar of high-performance adhesive and sealant demand. These projects require materials that withstand heavy usage, temperature fluctuations, and environmental exposure. Silicone and polyurethane sealants are heavily used for facade sealing, glazing, and curtain wall bonding, while epoxy and hybrid adhesives are favored in structural and flooring applications. The Repair & Renovation (R&R) segment represents a large, stable, and counter-cyclical market, sustaining adhesive demand during downturns in new construction. This sector benefits from retrofitting trends, sustainability upgrades, and routine maintenance—particularly in mature markets like Europe and North America.

The construction adhesives and sealants market is led by globally diversified companies with deep expertise in material science, formulation chemistry, and systems integration. These players are prioritizing low-emission, fire-safe, and long-life adhesive technologies to align with global construction sustainability mandates and industrial safety regulations.

Sika AG stands as a global benchmark in construction specialty chemicals, with industry-defining brands such as Sikaflex® and SikaBond® leading the polyurethane and hybrid sealant markets. Its Purform® polyurethane technology represents a breakthrough in low-monomer chemistry, ensuring compliance with future EU occupational safety standards while maintaining top-tier performance in roofing, flooring, and façade applications. With a growing footprint in fire-rated and waterproofing solutions, Sika continues to dominate structural bonding, reinforcement, and concrete repair systems across global infrastructure megaprojects.

Henkel, the world’s largest adhesives producer, brings unmatched application diversity and R&D capabilities, serving more than 800 end-use sectors. Through its Loctite and Teroson brands, Henkel delivers advanced adhesives and sealants optimized for laminated wood, flooring, and structural assemblies. Its Inspiration Center Düsseldorf (ICD) acts as a collaborative innovation hub, driving smart adhesive solutions, sustainable formulations, and digitally optimized production. Henkel’s integrated ecosystem—spanning formulation to dispensing equipment—sets a new standard in industrial-scale adhesive deployment.

H.B. Fuller is a global leader in energy-efficient construction adhesives and sealants, particularly in fenestration (window systems) and roofing. Its One Step Foamable Adhesive® portfolio is UL and FM-certified for commercial buildings, supporting thermal efficiency and structural durability. The company’s PUR hot-melt adhesives launched in October 2025 underscore its focus on fast-curing, weather-resistant solutions tailored for roofing and waterproofing systems. With over 30 private-label roofing brands, H.B. Fuller continues to advance performance standards in commercial and prefabricated construction.

Through its Bostik division, Arkema combines polymer innovation and sustainability to offer advanced adhesives for flooring, tiling, and interior bonding systems. The company’s low-monomer polyurethane adhesives, launched in September 2025, ensure REACH compliance and address health and safety concerns in commercial installations. Bostik’s commitment to low-VOC, bio-based, and waterborne technologies strengthens its position as a pioneer in sustainable indoor construction materials. Its synergy with Arkema’s specialty polymer segment enables rapid adaptation to new construction chemistry demands.

Mapei delivers complete construction solutions, including cement additives, structural adhesives, waterproofing systems, and marine flooring materials. With operations across 40+ countries and over 100 plants, it emphasizes localized production and on-site technical assistance. The company’s participation in Europe’s high-speed rail infrastructure project (August 2025) showcases its capabilities in complex underground tunneling and waterproofing. Mapei’s deployment of advanced demand forecasting and supply chain systems reflects its industry-leading efficiency in managing a portfolio of 8,100+ products.

Wacker Chemie AG is synonymous with silicone sealant excellence, focusing on durability, UV stability, and superior elasticity. Its August 2025 expansion in Asia enhances its global supply of high-consistency rubber (HCR) and liquid silicone rubber (LSR), supporting booming construction activity across the region. Wacker’s pure silicone formulations deliver long-term performance in glazing, facade sealing, and structural joints, making it a trusted supplier for high-rise, coastal, and desert-climate projects.

China continues to dominate the global construction adhesives and sealants market as the largest consumer and producer, supported by its vast infrastructure ecosystem, high-rise developments, and evolving environmental mandates. The country’s 14th Five-Year Plan prioritizes green building materials, accelerating the transition to low-VOC construction adhesives and water-based sealant formulations in compliance with sustainability standards. With $4.2 trillion allocated for infrastructure development, demand for polyurethane sealants, epoxy structural adhesives, and silicone glazing materials is rapidly expanding, particularly in bridge, rail, and high-rise commercial construction projects.

China’s prefabricated and modular construction sector—driven by government policy—is increasingly reliant on reactive hot-melt and MS Polymer-based adhesives to streamline assembly processes and reduce labor intensity. Coastal megaprojects, including large marine bridges and offshore ports, are fueling consumption of saltwater-resistant hybrid sealants with exceptional UV stability. Furthermore, the enforcement of new formaldehyde emission regulations in wood-based building materials is catalyzing the adoption of polyvinyl acetate (PVA) and bio-based adhesive formulations, aligning with the country’s broader carbon-neutrality agenda. The shifts make China a central hub for both mass-volume manufacturing and advanced product innovation in the construction adhesives sector.

The U.S. construction adhesives and sealants market is being reshaped by massive public infrastructure investments, the LEED green building movement, and the shift toward eco-conscious materials. The Bipartisan Infrastructure Law has directed billions toward bridge and road rehabilitation, significantly increasing demand for polymer-modified cementitious adhesives and expansion joint sealants capable of long-term performance under dynamic loading. Henkel’s new technology center in New Jersey (2024) exemplifies the market’s innovation trajectory, emphasizing low-emission, recyclable, and water-based construction adhesives to meet evolving EPA and state VOC standards.

The rising adoption of Mass Timber in commercial construction is another major trend, where fire-rated polyurethane adhesives are essential for structural wood bonding. State governments across California, New York, and Washington have introduced stricter VOC content regulations, compelling reformulation of traditional solvent-based products. Meanwhile, the private equity sector is consolidating niche players focusing on air barrier sealants, insulation panel adhesives, and moisture-cure hybrid polymers, expanding domestic capacity. Additionally, as climate resilience gains importance, demand for high-flexibility and weather-resistant sealants for high-rise and coastal structures continues to rise, reinforcing the U.S.’s position as a center for performance-driven adhesive innovation.

Germany remains the European powerhouse for advanced construction adhesives and sealants, shaped by the EU Green Deal, REACH compliance, and an unwavering commitment to sustainable construction materials. The enforcement of energy-efficient renovation programs under the Energy Performance of Buildings Directive (EPBD) has spurred demand for adhesives and sealants used in ETICS/EIFS thermal insulation systems. Concurrently, German chemical leaders such as Henkel AG and BASF SE are pioneering bio-based polyurethane systems to replace petrochemical feedstocks, supporting carbon neutrality and circular economy objectives.

With Germany’s booming logistics and industrial real estate sector, the market for fast-curing, self-leveling flooring adhesives is expanding rapidly to facilitate quick installation cycles. Companies are also deploying digitalized supply chain platforms for full material traceability and REACH-compliance monitoring, reflecting growing transparency expectations. Furthermore, government-supported R&D grants are backing smart adhesive technologies with embedded curing sensors for structural health monitoring in infrastructure applications. The integration of sustainability, precision engineering, and digital compliance cements Germany’s role as Europe’s benchmark market for innovation in construction sealants.

India’s construction adhesives and sealants industry is experiencing exponential growth, powered by the National Infrastructure Pipeline (NIP) and extensive public housing schemes such as Pradhan Mantri Awas Yojana. The rapid expansion of urban infrastructure, including metro networks and industrial corridors, has created surging demand for silicone weatherproofing sealants, tile adhesives, and structural epoxy systems for large-scale concrete bonding. The Make in India initiative continues to attract global manufacturers like H.B. Fuller and Pidilite Industries, who are investing in local production facilities for high-performance polymer adhesives and sealants tailored to India’s climate and cost dynamics.

Prefabrication is emerging as a strong trend in metropolitan cities such as Mumbai, Bengaluru, and Delhi, necessitating high-strength reactive adhesives for joining steel and precast concrete modules. The government is tightening BIS performance standards for low-VOC and low-formaldehyde materials in public sector projects, pushing domestic producers toward more eco-compliant solutions. Simultaneously, the rise of luxury and premium interior construction is boosting demand for non-staining, high-clarity adhesives for decorative surfaces and LVT flooring applications. With escalating infrastructure investments and green building certification requirements, India is positioning itself as one of the fastest-growing and most diversified markets for construction adhesives in Asia.

Japan’s construction adhesives and sealants sector is characterized by precision engineering, seismic safety, and long-term durability standards. The nation’s frequent earthquake activity drives high demand for high-modulus silicone sealants and MS Polymer-based formulations that maintain elasticity under extreme joint movement. Japanese R&D efforts are increasingly focused on long-life-span repair adhesives for existing infrastructure—bridges, tunnels, and railways—where polyurethane and epoxy composites offer superior adhesion and crack resistance.

Moreover, fire and safety regulations have accelerated innovation in intumescent and flame-retardant sealants for passive fire protection, particularly in high-rise and industrial facilities. Local manufacturers are deploying fully automated robotic application technologies for façade glazing and waterproofing to counteract labor shortages while ensuring precision. Japan’s rising exposure to typhoon and humidity extremes has also heightened demand for butyl and acrylic weatherproof sealants in roofing and exterior systems. The integration of automation and performance-driven product innovation underscores Japan’s role as a technology-intensive leader in specialized construction sealants.

The UAE’s construction adhesives and sealants market is strongly influenced by mega-projects and iconic architectural designs, demanding extreme-performance bonding solutions. Developments such as The Line (NEOM) and Dubai Creek Tower require structural glazing silicones and epoxy adhesives capable of withstanding high UV exposure, heat, and sand abrasion. The Estidama Pearl Rating System enforces stringent sustainability standards, mandating low-VOC and thermally efficient sealant formulations for all new commercial and residential projects.

Massive investments in utility-scale solar energy projects are creating a new demand vertical for photovoltaic (PV) module adhesives and high-temperature sealants engineered to resist thermal cycling. The hospitality and luxury residential markets are increasingly specifying aesthetic, color-matched sealants for marble and pool construction. Additionally, fire and life safety code enforcement is accelerating the adoption of certified fire-stopping sealants across high-rise and mixed-use developments. The UAE’s combination of extreme climate conditions, high design complexity, and stringent regulatory standards ensures a sustained demand for premium-grade construction adhesives and sealants.

Construction Adhesives & Sealants Market Report Scope

Construction Adhesives & Sealants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$23.6 Billion

|

|

Market Size (2034)

|

$56.6 Billion

|

|

Market Growth Rate

|

10.2%

|

|

Segments

|

By Product Type (Adhesives, Sealants), By Adhesive Resin Type (Polyurethane, Epoxy, Acrylic, Polyvinyl Acetate, Ethylene Vinyl Acetate, Styrenic Block Copolymers, Cyanoacrylate, Other High-Performance Resins), By Sealant Resin Type (Silicone, Polyurethane, Hybrid, Polysulfide, Acrylic, Butyl, Other Elastomers), By Technology (Water-based, Solvent-based, Hot Melt, Reactive, Pressure-Sensitive Adhesives), By End-User (Residential Construction, Non-Residential Construction, Infrastructure, Repair & Renovation, Modular & Prefabricated Construction

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, Sika AG, H.B. Fuller Company, The Sherwin-Williams Company, Arkema Group, Wacker Chemie AG, Dow Inc., 3M Company, RPM International Inc., Huntsman Corporation, DuPont de Nemours, Inc., Mapei S.p.A., Pidilite Industries Ltd., BASF SE, Illinois Tool Works

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Product Type

By Adhesive Resin Type

- Polyurethane

- Epoxy

- Acrylic

- Polyvinyl Acetate

- Ethylene Vinyl Acetate

- Styrenic Block Copolymers

- Cyanoacrylate

- Other High-Performance Resins

By Sealant Resin Type

- Silicone

- Polyurethane

- Hybrid

- Polysulfide

- Acrylic

- Butyl

- Other Elastomers

By Technology

- Water-based

- Solvent-based

- Hot Melt

- Reactive

- Pressure-Sensitive Adhesives

By End-Use Industry

- Residential Construction

- Non-Residential Construction

- Infrastructure

- Repair & Renovation

- Modular & Prefabricated Construction

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- Sika AG

- H.B. Fuller Company

- The Sherwin-Williams Company

- Arkema Group

- Wacker Chemie AG

- Dow Inc.

- 3M Company

- RPM International Inc.

- Huntsman Corporation

- DuPont de Nemours, Inc.

- Mapei S.p.A.

- Pidilite Industries Ltd.

- BASF SE

- Illinois Tool Works

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Construction Adhesives and Sealants Market as structural bonding, silicone leadership, and sustainable chemistry reshape global building envelopes and interiors. It delivers analysis reviews of demand drivers, regulatory inflection points, and installation productivity gains; highlights performance breakthroughs in elastic bonding, structural glazing, and fire-rated joint sealing; and benchmarks low-VOC and bio-based innovation that is displacing mechanical fixings and solvented chemistries. With clear connections between durability, movement capability, weatherability, and lifecycle carbon, this report is an essential resource for architects, specifiers, contractors, OEM fabricators, and procurement leaders seeking evidence-based guidance on product selection, code compliance, and value engineering across residential, non-residential, infrastructure, and retrofit programs.

Scope Highlights

Segmentation:

- By Product Type: Adhesives; Sealants.

- By Adhesive Resin Type: Polyurethane; Epoxy; Acrylic; Polyvinyl Acetate; Ethylene Vinyl Acetate; Styrenic Block Copolymers; Cyanoacrylate; Other High-Performance Resins.

- By Sealant Resin Type: Silicone; Polyurethane; Hybrid; Polysulfide; Acrylic; Butyl; Other Elastomers.

- By Technology: Water-based; Solvent-based; Hot Melt; Reactive; Pressure-Sensitive Adhesives.

- By End-Use Industry: Residential Construction; Non-Residential Construction; Infrastructure; Repair & Renovation; Modular & Prefabricated Construction.

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Frame: Historic data 2021–2024 and forecast 2025–2034.

Companies: Analysis / profiles of 15+ companies covering strategies, portfolios, capacity moves, and innovation pipelines.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.