Construction Coatings Market Size, Infrastructure Expansion, and Integrated Building Solutions Demand

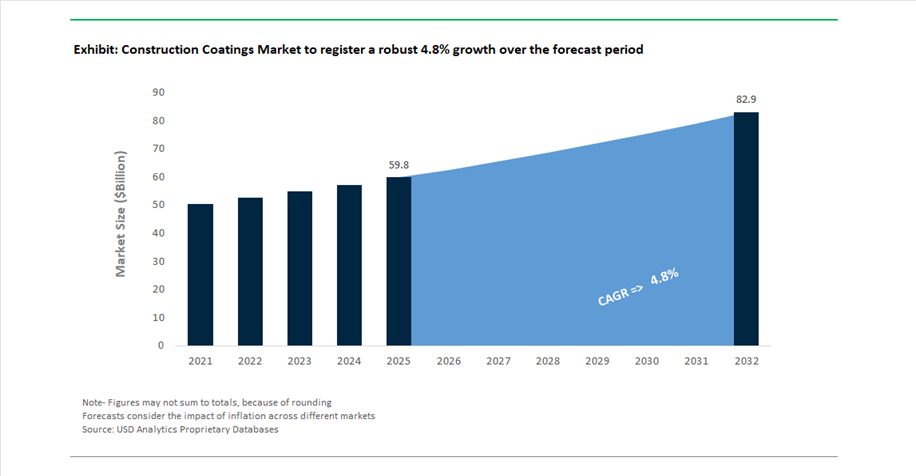

The global construction coatings market was valued at $59.8 billion in 2025 and is projected to grow at a CAGR of 4.8% between 2025 and 2032, reaching $83 billion by 2032. This growth is driven by increasing investments in commercial infrastructure, residential construction, industrial facilities, and urban redevelopment projects, where coatings are essential for surface protection, durability, weather resistance, and aesthetic enhancement.

A key market driver is the rising adoption of high-performance protective coatings for concrete, steel structures, roofing systems, and building facades, particularly in environments exposed to corrosion, moisture, UV radiation, and chemical stress. The growing emphasis on sustainable construction practices is accelerating demand for low-VOC, waterborne, and energy-efficient coating systems, aligning with global environmental regulations and green building standards.

The market is also shifting toward integrated construction solutions, where coatings are combined with waterproofing systems, insulation technologies, and building envelope materials to enhance overall building performance. Increasing demand for maintenance, repair, and operations (MRO) services is further supporting the adoption of advanced coatings designed to extend asset life and reduce lifecycle costs in aging infrastructure.

Strategic Acquisitions, Joint Ventures, and Regional Manufacturing Expansion Driving Market Consolidation

The construction coatings market is undergoing significant transformation through strategic acquisitions, long-term partnerships, and regional capacity expansion initiatives. A notable development is Sherwin-Williams’ integration of the Suvinil brand (January 2026), following its acquisition of BASF’s architectural coatings business in Brazil. The deal contributed $164.5 million to Q4 2025 net sales, significantly strengthening Sherwin-Williams’ position in the South American construction and decorative coatings market.

Strategic collaborations are reinforcing market presence in high-growth regions. In August 2025, PPG and Asian Paints extended their joint venture agreement through 2041, ensuring continued collaboration in protective, powder, and industrial coatings across India. This partnership enables both companies to leverage localized expertise and global technology platforms, addressing the growing demand for high-performance coatings in infrastructure and industrial construction projects.

Product innovation and branding strategies are targeting evolving construction requirements. PPG’s launch of MASTER’S MARK BALLARD™ Flat Interior Paint (January 2026) introduces an all-in-one solution with enhanced stain resistance, durability, and low-VOC performance, catering to modern architectural needs. This aligns with broader industry trends toward sustainably advantaged formulations that balance performance with environmental compliance.

Mergers and acquisitions are enabling vertical integration and expanded solution offerings. RPM International’s acquisition of Kalzip GmbH (April 2026) integrates high-performance aluminum roofing and façade systems into its Construction Products Group, allowing the company to deliver fully integrated coating and building envelope solutions for large-scale infrastructure projects. Additionally, RPM’s investment in a new manufacturing facility in Malaysia (January 2026) strengthens its footprint in Southeast Asia, enhancing supply capabilities for construction and performance coatings.

Strategic portfolio realignment is also reshaping competitive dynamics. AkzoNobel’s divestment of its Indian coatings operations to JSW Group (February 2026) reflects a focus on high-return core markets, while enabling JSW to expand its presence in India’s competitive construction coatings sector. Meanwhile, Nippon Paint’s updated “NIPSEA” strategy (February 2026) emphasizes a transition toward end-to-end construction solutions, including waterproofing, thermal insulation, and refurbishment systems, targeting both new construction and MRO segments.

Design trends continue to influence product development. Asian Paints’ “Moonlit Silk” (February 2026) highlights a shift toward organic textures and calming color palettes, shaping interior and exterior design preferences across commercial and residential projects.

Heightened Compliance Enforcement Reshaping Renovation Practices

The construction coatings segment is experiencing a regulatory tightening cycle in the United States, centered on stricter enforcement of the EPA’s Renovation, Repair, and Painting (RRP) program. While the regulatory framework itself is not new, the intensity of enforcement has increased significantly, particularly for projects involving pre-1978 residential buildings and child-occupied facilities.

A defining characteristic of the 2026 environment is the shift toward zero-tolerance enforcement, with over 50% of recent violations linked to certification lapses rather than technical non-compliance. This indicates that administrative oversight—rather than material performance—is now a primary risk factor for contractors and project managers.

Training and certification requirements have also become more structured. Contractors must complete an eight-hour training program, including hands-on modules, with mandatory recertification cycles every three to five years. This is increasing operational overhead while simultaneously raising the baseline competency level across the workforce.

Liability is extending beyond contractors to property managers and asset owners. Federal enforcement actions increasingly require real-time digital tracking of subcontractor certifications, effectively embedding compliance monitoring into project management systems. Failure to document lead-safe practices—such as containment and occupant notification—can trigger civil and criminal penalties under TSCA.

Structural Durability Standards Driving Waterproofing Innovation

China’s GB 55030-2022 regulation has emerged as a defining standard for construction coatings, particularly in the waterproofing segment. By consolidating previously fragmented codes into a unified framework, the regulation establishes significantly higher durability and performance benchmarks for building envelope systems.

One of the most impactful changes is the extension of required service life. Roofing waterproofing systems must now meet a minimum 20-year design life, while indoor waterproofing applications must achieve at least 25 years. This represents a substantial increase over legacy standards and is forcing manufacturers to shift toward high-performance liquid-applied membranes and advanced polymer-modified coatings.

Testing protocols have also become more stringent. Coatings must demonstrate resistance to prolonged water exposure—maintaining structural integrity after 14 days of immersion at controlled temperatures—while also meeting strict limits on water absorption (≤4%) in underground applications. These requirements are particularly relevant for infrastructure projects exposed to high moisture or hydrostatic pressure conditions.

The broader implication is a shift toward lifecycle-based performance metrics, where coatings are evaluated not just for initial application properties but for long-term durability under real-world environmental stress. This is driving innovation in formulation chemistry, particularly in elastomeric and hybrid waterproofing systems capable of maintaining flexibility and adhesion over extended periods.

Solar-Reflective Coatings Addressing Urban Heat and Energy Demand

Urban Heat Island (UHI) mitigation has become a central driver for construction coatings, particularly in densely populated metropolitan areas. Solar-reflective or “cool roof” coatings are emerging as a key solution, offering both environmental and economic benefits.

High-performance formulations are capable of reflecting more than 80% of incoming solar radiation, reducing rooftop surface temperatures by 30°C to 40°C compared to conventional materials. This temperature reduction directly translates into improved indoor thermal comfort and reduced strain on cooling systems.

From an energy perspective, buildings utilizing high-SRI coatings can achieve 10%–20% reductions in annual air conditioning energy consumption, depending on climatic conditions and building design. At a macro level, widespread adoption across urban areas can lower ambient air temperatures by up to 1.5°C, contributing to grid stability during peak demand periods.

These coatings are also gaining traction as part of ESG and green building strategies. Developers are leveraging solar-reflective coatings to secure certification points under frameworks such as LEED, enhancing asset value while demonstrating measurable sustainability outcomes.

Rapid-Cure Industrial Flooring Supporting Logistics Infrastructure Expansion

The rapid expansion of e-commerce and logistics infrastructure is driving demand for high-performance industrial floor coatings, particularly rapid-cure epoxy systems. These coatings are designed to meet the operational demands of high-throughput warehouses and distribution centers, where downtime directly impacts revenue.

A key performance attribute is accelerated return-to-service time. Modern rapid-cure epoxy systems enable full operational readiness within 24 hours, compared to several days for traditional flooring solutions. This allows developers to significantly compress project timelines and accelerate facility commissioning.

Durability is equally critical. These coatings are engineered to withstand continuous mechanical stress from automated guided vehicles (AGVs) and heavy equipment, offering abrasion resistance up to three times greater than standard concrete treatments. This ensures long-term performance in high-traffic industrial environments.

Chemical and thermal resistance further enhance their suitability for complex logistics environments, including facilities with adjacent cold storage and ambient zones. Additionally, the development of low-VOC and waterborne epoxy formulations allows application in partially occupied spaces without extensive ventilation requirements.

Water-Borne Construction Coatings Dominate with 62% Share Driven by VOC Compliance and Occupied-Space Applicability

Technology Analysis: Water-Based Acrylic Emulsions Lead with Regulatory Advantage and Application Efficiency

Water-borne coatings account for a dominant 62.0% share of the construction coatings market in 2025, driven by strict global VOC regulations and their suitability for on-site and occupied building applications. Regulations such as China GB 18582-2020, EU Deco Paint Directive, and US EPA AIM/SCAQMD Rule 1113 mandate ultra-low VOC levels (<50 g/L for flat coatings), effectively positioning waterborne acrylics, styrene-acrylics, and VAE emulsions as the industry standard. These coatings offer low odor, non-flammability, and fast drying, enabling renovation work in hospitals, schools, offices, and residential buildings without operational disruption—an essential advantage in modern construction projects. Technological advancements in 100% acrylic emulsion coatings have achieved full performance parity with solvent-based systems, delivering superior flexibility, block resistance, and dirt pick-up resistance. This combination of regulatory compliance, high-performance coatings, and application convenience firmly establishes water-borne systems as the backbone of the global construction coatings market.

Decorative Coatings Lead Construction Market with 47% Share Driven by Repaint Cycles and Interior Aesthetic Demand

Functionality Analysis: Interior Wall Paints and Exterior Finishes Drive High-Volume Consumption

Decorative coatings dominate the construction coatings market with a 47.0% share in 2025, driven by the vast surface area of interior walls, ceilings, and exterior facades across residential and commercial buildings. Every structure requires primer and multiple finish coats, making decorative paints the highest-volume segment globally. A key growth driver is the renovation and repaint cycle, which accounts for over 70% of demand in mature markets, with repaint frequencies of 3–5 years in commercial spaces and 5–7 years in residential buildings. Additionally, the segment is experiencing strong premiumization trends, with increasing demand for high-performance, deep-tint, and designer coatings aligned with evolving color trends such as biophilic greens, terracotta tones, and warm neutrals. These premium products, often priced 2x higher than standard paints, are boosting market value while maintaining steady volume demand, solidifying decorative coatings as the largest segment in the global construction coatings market.

Construction Coatings Market Competitive Landscape Driven by Infrastructure Demand, Sustainable Materials, and Contractor Networks

The construction coatings market is highly competitive, led by global players focusing on high-durability coatings, infrastructure protection, and sustainable formulations. Growth is driven by urbanization, renovation demand, and government infrastructure spending, with emphasis on anti-corrosion, weather-resistant, and energy-efficient coating technologies.

Sherwin-Williams Strengthens Construction Coatings Leadership with Latin America Expansion and Pro-Contractor Model

The Sherwin-Williams Company reported $23.57 billion in 2025 sales and projects steady growth into 2026, supported by strong demand in premium architectural and commercial construction coatings. The integration of Suvinil strengthened its Latin American footprint, contributing over $164 million in a single quarter. Its vertically integrated direct-to-contractor model, powered by 5,000+ stores, ensures supply chain control during demand surges. The company introduced advanced exterior resins under the 2026 Colormix® Forecast, designed for extreme weather and UV resistance. Sherwin-Williams is targeting new account growth in commercial construction, leveraging its premium product portfolio. Its scale, distribution, and innovation reinforce leadership in global construction coatings.

PPG Refocuses on High-Performance Construction Coatings with Sustainability Leadership

PPG Industries, Inc. has strategically exited its North American architectural business to focus on high-performance coatings for infrastructure and industrial applications. The company reported strong Q1 2026 performance with adjusted EPS of $1.83, driven by organic growth in specialized segments. Its COLORFUL COMMUNITIES® initiative continues to embed PPG coatings into global urban development projects. PPG achieved a sustainability milestone by securing third-party certification for environmental impact tools, critical for green construction tenders. Its protective and marine coatings portfolio supports large-scale infrastructure such as bridges and energy plants. This repositioning strengthens PPG’s role in high-value construction coatings markets.

AkzoNobel Advances Energy-Positive Construction Coatings with Laser-Curing Innovation

AkzoNobel N.V. is reinforcing its leadership through a proposed merger with Axalta, aiming to create a dominant global performance coatings entity. The company achieved a 14.2% EBITDA margin in 2025 and targets 16% by 2026 through operational efficiency programs. Its partnership with IPG Photonics introduced laser-curing powder coatings, significantly reducing energy consumption in construction materials. AkzoNobel is also a key supplier for Calosol heat-absorbing façade technology, enabling energy-positive buildings. Capital reallocation from its India divestment supports high-spec projects in Europe and North America. Its focus on sustainable, energy-efficient coatings aligns with next-generation construction trends.

Nippon Paint Expands Infrastructure Coatings with R&M Focus and Energy-Saving Technologies

Nippon Paint Holdings (NIPSEA Group) continues to expand through its asset assembler model, supported by the $2.3 billion AOC acquisition, strengthening upstream integration in construction binders. The company shifted focus to renovation and maintenance, which now accounts for nearly 70% of its Asia-Pacific decorative coatings sales. It launched energy-saving coatings in 2026 designed to reduce cooling costs in urban environments. Nippon dominates structural coatings with anti-corrosion solutions for aging infrastructure using thick-film technology. Its decentralized pricing and strong local channels support consistent growth and brand loyalty. The company remains a key player in infrastructure coatings across Asia-Pacific markets.

RPM International Builds Global Leadership in Building Envelope and Roofing Solutions

RPM International Inc. reported strong fiscal 2026 performance with $1.61 billion in quarterly sales and significant EBIT growth driven by its MAP 2025 efficiency program. The acquisition of Kalzip GmbH strengthens its position in aluminum roofing and building envelope systems. Kalzip’s solutions have been deployed in major infrastructure projects such as Estadio Santiago Bernabéu and LAX Train Station. RPM is positioning itself as a one-stop solution provider for weatherproofing, sealants, and specialty coatings. Its focus on integrated building envelope systems enhances value for construction customers. Strategic leadership changes support continued expansion and operational efficiency.

Asian Paints Captures Infrastructure Growth with Strong Distribution and Capacity Expansion

Asian Paints Limited is leveraging India’s infrastructure boom, supported by ₹12.2 lakh crore government capital expenditure, to expand its construction coatings business. The company implemented strategic price increases to manage raw material volatility while maintaining margins. Investments exceeding $250 million in capacity expansion target Tier 2 and Tier 3 cities, key growth areas for construction activity. Asian Paints’ strong dealer and contractor network enhances market penetration across decorative and industrial coatings. It leads in hospitality and tourism projects with specialized antimicrobial and luxury finishes. Its distribution strength and localized strategy position it strongly in emerging construction coatings markets.

India Construction Coatings Market: Consolidation and Infrastructure Boom Driving High Growth

India has emerged as one of the most dynamic markets for construction coatings, driven by strong policy support, infrastructure expansion, and major industry consolidation. A key development is JSW Paints’ acquisition of a 60.76% stake in AkzoNobel India (2025), which has reshaped the competitive landscape and elevated JSW into a leading position across industrial and decorative coatings.

Government initiatives are a major growth catalyst. The $130 billion infrastructure allocation (2025–26 Union Budget) is accelerating demand for polyurethane (PU) and epoxy coatings in metro systems, airports, and urban transit hubs. Additionally, GST reductions on construction materials (cement, tiles) have triggered a housing surge, indirectly boosting architectural coating consumption. The expansion of Vande Bharat trains and railway modernization projects is further increasing demand for anti-carbonation and fire-retardant coatings, while competitive pressures from entrants like Birla Opus are driving innovation in quick-drying, low-odor emulsions.

China Construction Coatings Market: Dual Carbon Strategy and Urban Redevelopment Driving High-Value Shift

China’s construction coatings market is undergoing a strategic transition toward high-performance and sustainable solutions, aligned with its “Dual Carbon” goals. The enforcement of GB 4806.10-2026 standards is tightening requirements for safety and purity, especially in public and commercial interiors.

Despite a slowdown in new construction, growth is driven by urban redevelopment and infrastructure investment, including a RMB 400 billion PPP initiative targeting major projects like airports. Environmental enforcement has led to a 45% increase in waterborne and powder coating adoption, particularly in Fujian and Zhejiang provinces. Additionally, the rise of Building-Integrated Photovoltaics (BIPV) is increasing demand for transparent conductive coatings, while expanded production of high-purity NMP is supporting advanced resin systems.

United States Construction Coatings Market: Infrastructure Modernization and Energy-Efficient Coatings Driving Demand

The United States market is driven by large-scale infrastructure upgrades and sustainability mandates. Under the Infrastructure Investment and Jobs Act (IIJA), over $40 billion is being allocated to bridge and road rehabilitation, increasing demand for high-performance duplex coating systems on steel structures.

Energy efficiency is a major trend. State-level regulations in California and Texas are accelerating adoption of “cool roof” coatings, which reduce solar heat gain by up to 25%. Regulatory pressure under TSCA Section 6 is also driving a 22% increase in bio-based and oxygenated solvent usage, replacing hazardous chemicals. Additionally, the semiconductor boom is fueling demand for ESD coatings and chemical-resistant wall systems in cleanroom environments, while antimicrobial coatings are now standard in ~85% of new commercial projects.

Germany Construction Coatings Market: Bio-Circular Resins and Hydrogen Infrastructure Driving Sustainability Leadership

Germany remains the global benchmark for sustainable construction coatings, driven by strict environmental regulations and advanced material innovation. The industry has achieved a ~90% phase-out of PFAS-based surfactants, positioning German manufacturers as leaders in toxin-free coatings.

Innovation is centered on decarbonization and traceability. The commercialization of bio-circular resins is reducing CO₂ emissions by up to 50%, while Digital Product Passports (DPP) provide full lifecycle transparency. Germany is also advancing permeation-resistant coatings for hydrogen infrastructure, supporting the country’s energy transition. Additionally, the adoption of electric IR and UV-LED curing systems is reducing energy consumption by ~22%, while government subsidies (€2.1 billion) for building renovations are driving demand for high-build facade coatings.

Saudi Arabia Construction Coatings Market: Vision 2030 Megaprojects Driving Extreme-Performance Demand

Saudi Arabia’s construction coatings market is defined by large-scale Vision 2030 megaprojects, including NEOM and The Line, which are driving demand for heat-reflective and sand-abrasion-resistant coatings tailored for desert environments.

Rapid urbanization is another key driver, with plans to build 700,000+ new homes to increase homeownership to 70% by 2030. The tourism sector is also fueling demand for high-durability interior coatings in luxury hotels. Additionally, the oil & gas industry is increasing adoption of thermal insulation coatings to combat corrosion under insulation (CUI). Regulatory mandates are accelerating the shift toward low-VOC acrylic systems, while innovations in nano-coatings are enhancing durability and sustainability.

Brazil Construction Coatings Market: Infrastructure Programs and Agribusiness Driving Growth

Brazil’s market is expanding through infrastructure investment and strong agribusiness demand. The government’s Growth Acceleration Program (PAC) is boosting adoption of corrosion-resistant coatings in transportation and sanitation infrastructure.

Housing initiatives such as Minha Casa Minha Vida are driving steady demand for decorative coatings, while updated building codes mandate liquid-applied polyurethane waterproofing systems for commercial rooftops. The agricultural sector is also a major driver, with a 15% increase in demand for ZM-coated steel in grain storage facilities. Additionally, investments of $19.5 billion in clean-tech are accelerating adoption of UV-stabilized coatings for renewable energy infrastructure, positioning Brazil as a key regional growth market.

Construction Coatings Market Report Scope

Construction Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$59.8 Billion

|

|

Market Size (2032)

|

$83 Billion

|

|

Market Growth Rate

|

4.8%

|

|

Segments

|

By Resin Chemistry (Acrylic, Polyurethane (PU), Epoxy, Alkyd and Polyester, Fluoropolymer and Silicone, Specialty Bio-based Resins), By Technology (Water-borne, Solvent-borne, Powder Coatings, High-Solids), By Functionality (Decorative, Protective and Anti-Corrosive, Waterproofing and Damp-proofing, Intumescent and Fire-Retardant, Smart Coatings), By End-Use Sector (Residential, Commercial and Institutional, Industrial, Infrastructure)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, PPG Industries, Inc., AkzoNobel N.V., Nippon Paint Holdings Co., Ltd., RPM International Inc., Asian Paints Limited, BASF SE, Axalta Coating Systems Ltd., Kansai Paint Co., Ltd., Jotun A/S, Sika AG, Hempel A/S, Masco Corporation, DAW SE, Berger Paints India Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Construction Coatings Market Segmentation

By Resin Chemistry

- Acrylic

- Polyurethane (PU)

- Epoxy

- Alkyd and Polyester

- Fluoropolymer and Silicone

- Specialty Bio-based Resins

By Technology

- Water-borne

- Solvent-borne

- Powder Coatings

- High-Solids

By Functionality

- Decorative

- Protective and Anti-Corrosive

- Waterproofing and Damp-proofing

- Intumescent and Fire-Retardant

- Smart Coatings

By End-Use Sector

- Residential

- Commercial and Institutional

- Industrial

- Infrastructure

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Construction Coatings Market

- The Sherwin-Williams Company

- PPG Industries, Inc.

- AkzoNobel N.V.

- Nippon Paint Holdings Co., Ltd.

- RPM International Inc.

- Asian Paints Limited

- BASF SE

- Axalta Coating Systems Ltd.

- Kansai Paint Co., Ltd.

- Jotun A/S

- Sika AG

- Hempel A/S

- Masco Corporation

- DAW SE

- Berger Paints India Limited

*- List not Exhaustive