Construction Paints and Coatings Market Size, Urbanization Demand, and Premium Architectural Solutions Expansion

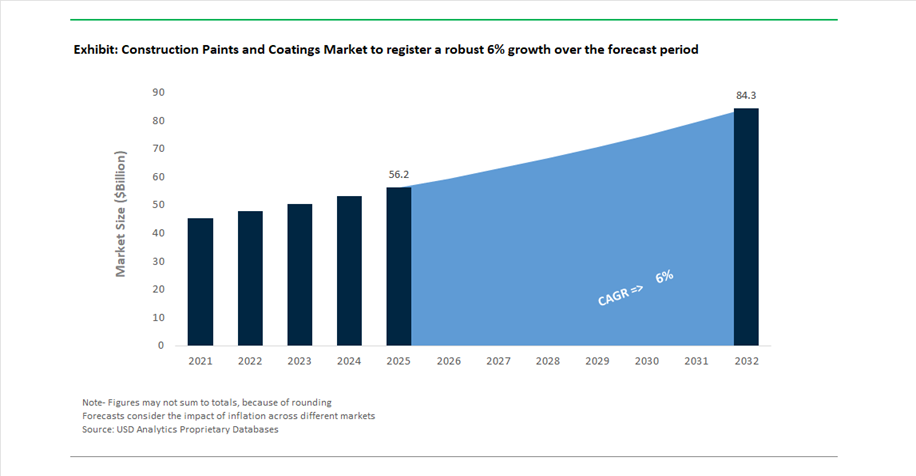

The global construction paints and coatings market was valued at $56.2 billion in 2025 and is projected to grow at a CAGR of 6% between 2025 and 2032, reaching $84.5 billion by 2032. This growth is supported by sustained demand across residential housing, commercial buildings, infrastructure projects, and renovation activities, where paints and coatings play a vital role in surface protection, durability, weather resistance, and aesthetic enhancement.

A major growth driver is the accelerating pace of urbanization and infrastructure development, particularly in emerging economies such as India, Southeast Asia, and Latin America. Increasing investments in smart cities, transportation infrastructure, and affordable housing projects are driving the adoption of high-performance architectural coatings that offer enhanced resistance to UV radiation, moisture, pollutants, and mechanical wear. At the same time, the rising importance of repainting and refurbishment cycles in mature markets is supporting consistent demand for premium decorative paints and protective coatings.

The market is also undergoing a shift toward sustainable and low-emission formulations, including waterborne paints, low-VOC coatings, and bio-based resins, in response to environmental regulations and green building standards. Innovations in anti-microbial coatings, heat-reflective paints, and self-cleaning surfaces are further enhancing product differentiation, particularly in high-value commercial and healthcare applications.

Additionally, manufacturers are increasingly focusing on integrated coating systems that combine paints with waterproofing, insulation, and fire protection solutions, offering end-to-end value for large-scale construction projects. The integration of digital color matching technologies and automated application systems is also improving efficiency and customization in both professional and DIY segments.

Market Consolidation, Strategic Acquisitions, and Product Innovation Driving Competitive Transformation

The construction paints and coatings market is experiencing significant consolidation and strategic repositioning through acquisitions, internal restructuring, and regional expansion initiatives. A major development is Sherwin-Williams’ integration of the Suvinil brand (February 2026), which contributed to its record $23.57 billion net sales in 2025. This acquisition has significantly expanded its footprint in Latin America’s architectural coatings market, particularly in the professional repaint and residential segments.

In the South Asian market, consolidation is accelerating. JSW Paints’ acquisition of a 61.2% stake in AkzoNobel India (December 2025) marks a pivotal shift, giving JSW control over the premium Dulux brand and strengthening its presence in both decorative and industrial coatings. This move positions JSW to aggressively expand its manufacturing capacity and distribution network across India, intensifying competition in one of the fastest-growing construction markets globally.

Strategic restructuring and leadership changes are also shaping the competitive landscape. BASF’s appointment of Jens Luehring as CEO of its standalone coatings business (March 2026) is a critical step in its broader spin-off strategy, allowing for a more focused approach toward automotive and industrial surface solutions. Meanwhile, Asian Paints’ amalgamation of its polymer subsidiary (March 2026) enhances vertical integration, improving control over raw material supply and cost efficiency in architectural paint production.

Product innovation is targeting performance-critical construction applications. Jotun’s launch of Hardtop XP II and expansion of its fire protection range (2025–2026) introduces coatings with enhanced durability, corrosion resistance, and fire safety performance, catering to large-scale infrastructure and industrial construction projects. Similarly, RPM International’s acquisition of Kalzip (April 2026) enables the integration of coatings with high-performance building envelope systems, offering comprehensive solutions for modern construction requirements.

Regional growth strategies are further intensifying competition. Nippon Paint India’s “India-first” roadmap (January 2026) focuses on expanding beyond its traditional markets, unifying business segments to improve operational efficiency and accelerate national expansion. Additionally, Protech Group’s acquisition of MF Paints (October 2025) strengthens its presence in the Canadian architectural coatings market, broadening its portfolio for residential and commercial construction applications.

EU Regulatory Framework Embedding Transparency into Market Access

The European construction paints and coatings market is undergoing a structural transformation under the revised Construction Products Regulation (CPR 2024/3010), which became fully applicable in January 2026. The regulation fundamentally redefines compliance by embedding environmental and safety performance directly into the CE marking process, making sustainability disclosure a prerequisite for market entry.

A key mechanism enabling this shift is the introduction of Digital Product Passports (DPPs). These machine-readable datasets provide real-time access to critical product information, including Global Warming Potential (GWP), VOC/SVOC emission profiles, and lifecycle environmental indicators. This level of transparency is transforming how coatings are specified, enabling contractors and regulators to make data-driven decisions at the point of application.

The harmonization of VOC emission classes across the EU further standardizes performance expectations. Coatings are now categorized based on 28-day chamber emission testing, similar to the French A+ labeling system but enforced uniformly across all Member States. This creates a competitive environment where manufacturers must optimize formulations to meet increasingly stringent emission thresholds.

Additionally, mandatory reporting of CO₂ emissions and energy consumption during production introduces a new layer of accountability. These indicators, now required in the Declaration of Performance, are pushing manufacturers to invest in low-energy production processes and renewable energy integration. The result is a data-driven, compliance-centric market structure, where environmental performance is inseparable from product competitiveness.

China’s Performance Standards Elevating Product Quality Thresholds

China’s implementation of the GB/T 9755—2024 standard represents a major recalibration of performance expectations in the construction paints sector. By consolidating previous interior and exterior standards into a unified framework, the regulation establishes higher durability and quality benchmarks across all application categories.

One of the most immediate impacts is the increase in scrub resistance requirements for interior wall coatings. The threshold for “qualified” products has been raised to 500 scrub cycles, effectively eliminating lower-performance formulations from premium commercial applications. This shift is driving innovation in binder chemistry and pigment dispersion to achieve higher durability without compromising finish quality.

The expansion of China Compulsory Certification (CCC) to include water-based interior paints further tightens market access controls. By 2026, all such products must carry CCC certification to be legally sold or used in large-scale construction projects, creating a formal barrier to entry for non-compliant manufacturers.

The regulatory framework is also moving toward harmonization of harmful substance limits, including VOCs, formaldehyde, and heavy metals. This eliminates inconsistencies between different coating categories and ensures a unified safety baseline across the industry. Additionally, new requirements for low-temperature film formation address performance challenges in cold-weather construction, ensuring coating integrity under variable climatic conditions.

Anti-Graffiti Coatings Enhancing Infrastructure Lifecycle Efficiency

Urban infrastructure maintenance is emerging as a key application area for advanced coatings, particularly through the adoption of non-sacrificial anti-graffiti systems. These coatings are designed to withstand repeated cleaning cycles without degradation, offering significant cost and operational advantages for municipalities and transit authorities.

From an economic perspective, the impact is substantial. Municipalities deploying these systems report up to 70% reductions in long-term cleaning costs, driven by the elimination of repeated recoating and the use of mild, biodegradable cleaning agents. This reduces both direct maintenance expenses and environmental impact.

Operational efficiency is another key benefit. Modern anti-graffiti coatings allow for rapid restoration of surfaces—often within 10 minutes—minimizing service disruptions in high-traffic areas such as metro stations and bus terminals. This is particularly valuable in urban environments where downtime carries significant economic and social costs.

Technologically, these coatings balance impermeability with breathability. They prevent paint and ink penetration while allowing moisture vapor to escape, preserving the integrity of substrates such as concrete and masonry. By reducing the need for aggressive chemical cleaning, they also extend the lifespan of structural surfaces by approximately 15%.

Intumescent Coatings Supporting the Rise of Mass Timber Construction

The increasing adoption of mass timber in commercial construction is creating a specialized growth segment for fire-retardant intumescent coatings. These coatings enable timber structures to meet stringent fire safety standards while preserving their natural aesthetic, a key requirement in modern architectural design.

Thin-film intumescent coatings are gaining dominance, accounting for more than half of the fire-retardant coatings used in wood applications. These systems provide fire resistance ratings ranging from 60 to 120 minutes, allowing timber structures to compete with traditional materials such as steel and concrete in mid- to high-rise buildings.

The underlying mechanism involves significant expansion upon heat exposure—up to 50 times the original coating thickness—forming a protective char layer that insulates the substrate and delays ignition. This is particularly important for cellulosic materials, where rapid heat buildup can lead to structural failure.

Alignment with global fire testing standards such as ASTM E119 and EN 13381-7 ensures compatibility across international markets, facilitating broader adoption in large-scale construction projects. Additionally, the shift toward halogen-free and low-VOC formulations aligns these coatings with green building certification systems, enhancing their appeal in sustainable construction.

Water-Borne Coatings Dominate Construction Paints Market with 63% Share Driven by Architectural Volume and Advanced Acrylic Systems

Technology Analysis: Water-Based Acrylic and Elastomeric Coatings Lead with High-Volume Demand and Performance Innovation

Water-borne coatings hold a dominant 63.0% share of the construction paints and coatings market in 2025, driven primarily by the massive global demand for architectural wall paints and exterior coatings. Water-based acrylic systems remain the industry standard due to their low VOC compliance, ease of application, and versatility across substrates. A key growth driver is the rapid adoption of water-borne Direct-to-Metal (DTM) coatings, which eliminate the need for primers while delivering corrosion resistance exceeding 500 hours in salt spray testing, significantly reducing labor and project timelines. Additionally, elastomeric wall coatings (EWC) are gaining traction in exterior applications, offering crack-bridging, waterproofing, and long-term durability for concrete, stucco, and EIFS surfaces. Importantly, these systems rely on coalescing solvents (3–8%) to ensure film formation, with increasing innovation in bio-based, zero-VOC coalescents, reinforcing sustainability trends and cementing water-borne dominance in the global construction coatings market.

Decorative Coatings Lead Market with 48% Share Driven by Aesthetic Trends and High-Performance Architectural Finishes

Functionality Analysis: Premium Decorative Finishes and Coil Coatings Drive Value Growth

Decorative coatings account for a leading 48.0% share of the construction paints and coatings market in 2025, driven by the combined demand for aesthetic appeal and basic environmental protection across residential and commercial structures. This segment includes both site-applied architectural paints and factory-applied finishes such as coil coatings for metal roofing and extrusion coatings for aluminum components, offering 20–40 year durability and weather resistance. A major value driver is the growing demand for premium and specialty finishes, including matte textures, metallic coatings, Venetian plaster, and suede finishes, particularly in commercial interiors designed for branding and visual impact. Additionally, innovations such as solar-reflective pigments for cool roofs are enhancing energy efficiency and sustainability. While protective coatings play a critical role in structural integrity, the sheer volume and premiumization of decorative applications position this segment as the primary growth engine in the global construction paints and coatings market.

Construction Paints and Coatings Market Competitive Landscape Driven by Low-VOC Innovation, Digital Tools, and Infrastructure Demand

The construction paints and coatings market is highly competitive, driven by architectural coatings demand, sustainable formulations, and contractor-focused distribution models. Key players compete on low-VOC technologies, digital color platforms, and large-scale infrastructure opportunities across commercial, residential, and renovation segments.

Sherwin-Williams Expands Architectural Coatings Dominance with Direct-to-Contractor Scale

The Sherwin-Williams Company continues to lead the construction paints and coatings market with over $23 billion in 2025 revenue and a projected 5% growth in 2026. Its expanded retail footprint, growing by 10% in early 2026, reinforces its direct-to-contractor distribution advantage across North America and EMEA. The integration of premium paint lines into its Professional Segment is driving consistent mid-single-digit growth in commercial construction coatings. Sherwin-Williams’ vertically integrated supply chain ensures full transparency and reliability for Tier-1 contractors and infrastructure projects. Its stronghold in architectural coatings is supported by scale, logistics efficiency, and high-performance product offerings. The company remains a dominant force in global construction coatings markets.

PPG Transitions to High-Tech Coatings with Digital Integration and Sustainability Leadership

PPG Industries, Inc. has strategically pivoted toward high-tech specialty coatings following the divestiture of its North American architectural business, strengthening its focus on performance-driven segments. Its SOLARON BLUE PROTECTION™ technology is being adapted for commercial glazing applications, offering advanced UV-blocking and thermal management for high-rise buildings. The company achieved a 15% reduction in carbon emissions by 2026, outperforming industry sustainability benchmarks. PPG LINQ™ digital ecosystem enhances project efficiency through AI-driven color visualization, reducing coating waste by up to 15%. This digital integration supports architects and contractors in large-scale commercial projects. PPG’s transformation positions it as a leader in advanced, sustainable construction coatings.

AkzoNobel Drives Sustainable Construction Coatings with Bio-Attributed Resin Innovation

AkzoNobel N.V. is advancing its leadership through a proposed merger with Axalta, aimed at creating the largest dedicated performance coatings company globally. Its 2026 Color of the Year, “Rhythm of Blues,” utilizes bio-attributed resin systems, reducing carbon footprint in architectural coatings. The company raised €1.1 billion in 2026 to fund efficiency improvements and strategic acquisitions under its transformation roadmap. AkzoNobel is also a key supplier of Calosol heat-absorbing technology, enabling energy-generating building facades. Its focus on sustainability, premium coatings, and innovation supports long-term growth in construction applications. The company’s strategic initiatives align with green building trends and carbon reduction goals.

Nippon Paint Expands APAC Leadership with Smart Surface and India-First Strategy

Nippon Paint Holdings (NIPSEA Group) is achieving steady growth with revenues exceeding $10 billion and a 6% annual growth trajectory in 2026. Its India-First strategy strengthens manufacturing and distribution capabilities across seven integrated plants, supporting rapid market expansion. The company’s smart surface coatings incorporate antimicrobial properties without toxic biocides, addressing hygiene requirements in public infrastructure. Nippon Paint is focusing on premiumization and brand building to capture rising middle-class demand in Southeast Asia. Its disciplined execution model supports sustained growth in architectural and infrastructure coatings. The company’s innovation and regional expansion reinforce its competitive position.

Asian Paints Strengthens Market Leadership with Pricing Strategy and Service Integration

Asian Paints Limited achieved strong growth with a 10% revenue increase in 2025 and expanded production capacity by 15% to meet infrastructure demand. The company implemented a 6%–8% price increase in 2026 to manage raw material volatility and maintain margins. Its transition beyond paints into home décor and professional painting services adds a high-margin service layer for commercial contracts. Asian Paints’ extensive distribution network across Tier-2 and Tier-3 cities ensures deep market penetration. The company benefits from strong brand recall and infrastructure-driven demand in South Asia. Its integrated approach strengthens its leadership in construction paints and coatings.

Masco (Behr) Focuses on Remodeling Market with Sustainable and Value-Based Coatings

Masco Corporation’s Behr Paint reported $7.6 billion in 2025 sales, with a strong focus on the repair and remodel segment, which offers stable demand compared to new construction. The company is targeting margin expansion in 2026 through operational efficiency improvements following tariff-related challenges. Its ECOMIX™ recycled paint line supports eco-friendly commercial interior projects, aligning with sustainability trends. Behr’s Color of the Year “Smoky Jade” reflects design-driven demand in commercial spaces. Its exclusive partnership with The Home Depot ensures strong positioning in DIY and pro-sumer markets. Masco’s value-driven coatings and sustainability focus enhance its competitiveness in construction coatings.

India Construction Paints & Coatings Market: Capacity Expansion and Housing Boom Driving Rapid Growth

India is currently one of the fastest-growing markets for construction paints and coatings, driven by large-scale capacity additions and strong policy support. The commissioning of Birla Opus facilities (2025) added 1,332 million liters of capacity, increasing national production potential by over 40% and intensifying competition in premium segments.

Government initiatives are a major catalyst. Under PMAY Urban 2.0, approximately $120 billion has been allocated for affordable housing, with hundreds of thousands of new units already approved—directly boosting demand for decorative emulsions and architectural coatings. Environmental compliance is also tightening, with 100% adoption of Zero-Liquid-Discharge (ZLD) processes in major plants. Additionally, smart city investments (~$27.6 billion) are driving adoption of anti-carbonation and photocatalytic coatings, while rising incomes in Tier-2 cities are increasing demand for low-VOC and antimicrobial interior paints.

United States Construction Paints & Coatings Market: Infrastructure Funding and AI-Driven Efficiency Driving Innovation

The United States market is shaped by federal infrastructure investment and advanced coating technologies. The Infrastructure Investment and Jobs Act (IIJA) has directed over $45 billion toward bridge rehabilitation, boosting demand for high-performance epoxy and intumescent coatings for steel structures.

Technological innovation is a key differentiator. AI-designed reflective coatings are capable of reducing surface temperatures by 5–20°C, improving energy efficiency and lowering operational costs. Regulatory changes under TSCA have completed the phase-out of methylene chloride, driving a 22% increase in bio-based solvent adoption. Additionally, the semiconductor cleanroom boom is increasing demand for ESD and chemical-resistant coatings, while waterborne coatings now dominate with ~67% market share, driven by green building certifications.

China Construction Paints & Coatings Market: Green Mandates and Repainting Economy Driving Structural Shift

China’s market is transitioning toward sustainable, high-performance coatings, supported by regulatory enforcement and changing demand patterns. The implementation of GB 4806.10-2026 is expanding approved materials while mandating ultra-low levels of hazardous compounds, particularly for public and food-contact surfaces.

With new construction slowing, the market is shifting toward a “repainting economy”, with up to 70% of marketing efforts focused on maintenance and refurbishment. Environmental inspections have driven a 45% increase in powder and water-based coating adoption, especially in coastal provinces. Additionally, the expansion of Building-Integrated Photovoltaics (BIPV) is increasing demand for transparent conductive coatings, while investments in high-purity NMP production are supporting advanced resin systems for both construction and energy applications.

Germany Construction Paints & Coatings Market: Bio-Circular Innovation and Regulatory Leadership Driving Sustainability

Germany remains the global benchmark for sustainable construction coatings, driven by strict environmental policies and advanced material innovation. The introduction of an anti-greenwashing bill (2025) ensures that all sustainability claims are independently verified, increasing transparency across the market.

The industry has achieved a ~90% phase-out of PFAS-based surfactants, while scaling bio-circular resins that reduce CO₂ emissions by up to 50%. Germany is also leading in Digital Product Passports (DPP), enabling full traceability of coating materials. Energy-efficient curing technologies—such as IR and UV-LED systems—are reducing operational energy consumption by ~22%. Additionally, R&D into permeation-resistant coatings for hydrogen infrastructure is positioning Germany at the forefront of next-generation construction materials.

Saudi Arabia Construction Paints & Coatings Market: Vision 2030 and Green Building Mandates Driving Demand

Saudi Arabia’s market is expanding rapidly under Vision 2030, with large-scale megaprojects such as NEOM and The Line driving demand for heat-reflective and sand-resistant coatings tailored for extreme desert environments.

Regulatory changes are also shaping the market. The Green Building Code (2025) mandates low-VOC coatings in all new commercial and government buildings, accelerating the shift toward waterborne formulations. Industrial expansion—such as Lucid Motors’ Jeddah facility—is increasing demand for high-durability OEM coatings, while petrochemical investments are boosting adoption of heavy-duty protective and intumescent coatings. Additionally, government incentives under the IKTVA program are encouraging local production, strengthening the domestic supply chain.

Brazil Construction Paints & Coatings Market: Trade Synergy and Industrial Expansion Driving Regional Leadership

Brazil is a major player in the global construction coatings market, producing over 2 billion liters annually, ranking among the top global producers. The Mercosur–EU trade agreement (2026) is expected to further boost exports and integration into global supply chains.

The market is heavily dominated by architectural coatings, accounting for nearly 75% of production volume, driven by residential and commercial construction. Infrastructure investments and offshore oil exploration are increasing demand for epoxy and seawater-resistant coatings, while high import tariffs (10–35%) are encouraging multinational companies to expand local manufacturing. Additionally, the strong performance of acrylic coatings (≈37% share) reflects their suitability for tropical climates, reinforcing Brazil’s regional leadership.

Vietnam Construction Paints & Coatings Market: Urbanization and Manufacturing Expansion Driving High Growth

Vietnam is emerging as a high-growth market for construction paints and coatings, supported by rapid urbanization and strong industrial expansion. Government targets to build 100,000 social housing units by 2025 are driving demand for weather-resistant and waterproof coatings.

Industrialization is another key driver. Growth in automotive and electronics manufacturing is increasing demand for durable industrial coatings, while rising disposable income is boosting adoption of premium, low-odor architectural products. Additionally, the expansion of domestic automotive production (up 27% YoY) is driving consumption of OEM and refinish coatings. Manufacturers are also focusing on climate-specific innovations, such as hydrophobic and anti-fungal coatings tailored for tropical environments, positioning Vietnam as a key emerging market.

Construction Paints and Coatings Market Report Scope

Construction Paints and Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$56.2 Billion

|

|

Market Size (2032)

|

$84.5 Billion

|

|

Market Growth Rate

|

6%

|

|

Segments

|

By Technology (Water-borne Coatings, Solvent-borne Coatings, Powder Coatings, Radiation-Curable (UV), By Resin Chemistry (Acrylic, Polyurethane (PU), Epoxy, Alkyd, Specialty Hybrids), By Application Sector (Residential, Commercial and Institutional, Industrial, Infrastructure), By Functionality (Decorative, Protective and Anti-Corrosive, Waterproofing and Damp-proofing, Intumescent and Fire-Retardant, Smart)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sherwin-Williams Company, PPG Industries, Inc., AkzoNobel N.V., Nippon Paint Holdings Co., Ltd., RPM International Inc., Asian Paints Limited, Kansai Paint Co., Ltd., Jotun A/S, Axalta Coating Systems Ltd., BASF SE, Masco Corporation, Hempel A/S, Sika AG, Berger Paints India Limited, DAW SE

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Construction Paints and Coatings Market Segmentation

By Technology

- Water-borne Coatings

- Solvent-borne Coatings

- Powder Coatings

- Radiation-Curable (UV

By Resin Chemistry

- Acrylic

- Polyurethane (PU)

- Epoxy

- Alkyd

- Specialty Hybrids

By Application Sector

- Residential

- Commercial and Institutional

- Industrial

- Infrastructure

By Functionality

- Decorative

- Protective and Anti-Corrosive

- Waterproofing and Damp-proofing

- Intumescent and Fire-Retardant

- Smart

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Construction Paints and Coatings Market

- Sherwin-Williams Company

- PPG Industries, Inc.

- AkzoNobel N.V.

- Nippon Paint Holdings Co., Ltd.

- RPM International Inc.

- Asian Paints Limited

- Kansai Paint Co., Ltd.

- Jotun A/S

- Axalta Coating Systems Ltd.

- BASF SE

- Masco Corporation

- Hempel A/S

- Sika AG

- Berger Paints India Limited

- DAW SE

*- List not Exhaustive