Consumer Appliance Coatings Market Size, Premium Finish Demand, and High-Performance Functional Coatings

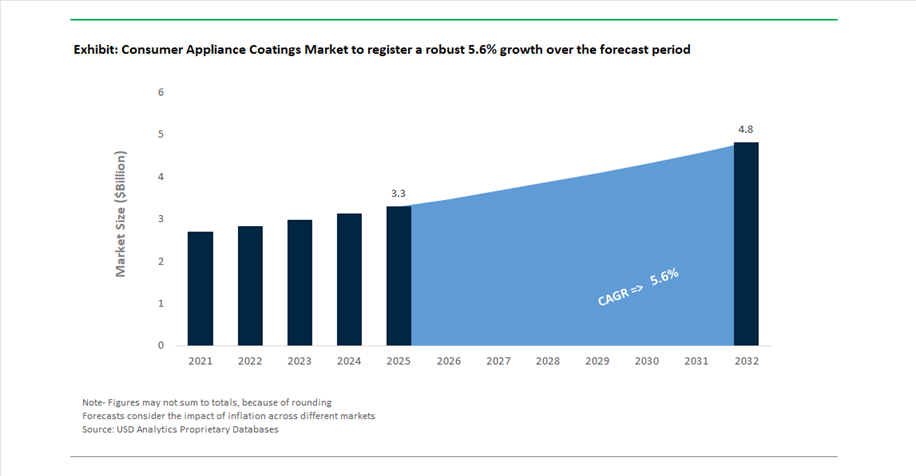

The global consumer appliance coatings market was valued at $3.3 billion in 2025 and is projected to grow at a CAGR of 5.6% between 2025 and 2032, reaching $4.8 billion by 2032. This growth is driven by increasing demand across home appliances such as refrigerators, washing machines, ovens, air conditioners, and small kitchen devices, where coatings are essential for corrosion resistance, heat stability, electrical insulation, and aesthetic appeal.

A major growth driver is the rising consumer preference for premium, design-oriented appliances, particularly in urban markets. Manufacturers are increasingly adopting coatings that deliver high-gloss finishes, fingerprint resistance, scratch durability, and color consistency, enabling differentiation in competitive retail environments. The shift toward “smart appliances” and integrated home ecosystems is further driving demand for coatings that combine functional performance with advanced visual effects, including metallic finishes, matte textures, and tactile surfaces.

The market is also undergoing a transformation toward sustainable and energy-efficient coating technologies, including powder coatings, waterborne formulations, and low-VOC systems. Powder coatings, in particular, are gaining traction due to their solvent-free nature, high transfer efficiency, and superior durability, making them ideal for appliance housings and components exposed to heat and moisture. Additionally, advancements in thermal management coatings and electrical insulation materials are supporting the development of appliances designed for energy storage and high-voltage applications.

Capacity Expansion, Advanced Powder Coatings, and Design-Led Innovation Driving Market Evolution

The consumer appliance coatings market is evolving through capacity expansion, advanced material innovation, and design-driven product differentiation. A key development is Sherwin-Williams’ completion of a 60% capacity expansion at its Bowling Green, Kentucky facility (March 2026), significantly increasing production of polyester coil coatings used in appliances and lighting fixtures. This investment strengthens supply chain resilience for North American OEMs while improving production efficiency and lead times.

Sustainability and high-performance materials are becoming central to product innovation. Jotun’s launch of next-generation powder coatings (June 2025), designed for energy storage systems and EV batteries, is also being adapted for home appliances requiring high-voltage insulation and thermal stability. These solvent-free coatings provide enhanced durability and environmental compliance, aligning with the industry’s transition toward low-emission manufacturing processes.

Design and aesthetics are playing an increasingly important role in market differentiation. PPG’s “Refresh & Sustain” showcase (January 2026) highlighted Master’s Mark™ and Tikkurila™ innovations, emphasizing color psychology and premium finishes for home environments. Similarly, Kansai Paint’s “GOING THROUGH” global trend concept (April 2026) introduces coatings with enhanced gloss, depth, and translucency, catering to the “minimalist-tech” aesthetic increasingly preferred in modern appliances.

Sustainability certification and raw material innovation are strengthening competitive positioning. PPG’s REDCert² certification (December 2025) enables the supply of biomass-balanced, low-carbon coating solutions, supporting appliance manufacturers in meeting ESG targets. Additionally, BASF’s “DRIVING THE PROXY” collection (October 2025) demonstrates how advanced pigments and tactile surface technologies developed for automotive applications are being adopted in premium consumer appliances, enhancing both visual and functional performance.

Market consolidation and regional strategy shifts are also influencing competitive dynamics. AkzoNobel’s divestment of its India operations to JSW Group (February 2026) enables JSW to expand its manufacturing footprint in appliance coatings, while AkzoNobel focuses on higher-margin markets. Meanwhile, Nippon Paint’s strong 2025 revenue performance (April 2026) highlights growth in industrial coatings across Asia, driven by increased demand for high-value appliance coatings and price optimization strategies.

Financial strength and operational excellence remain critical enablers. Axalta’s record EBITDA performance in 2025, supported by its “2026 A Plan,” provides the capital required to invest in high-margin industrial coatings, including those for premium consumer appliances.

Energy Efficiency Mandates Driving Low-Cure Powder Coating Adoption

The consumer appliance coatings sector is undergoing a process-level transformation as U.S. Department of Energy (DOE) energy conservation standards increasingly target manufacturing emissions and energy consumption. Between 2024 and 2026, these regulations have placed direct pressure on appliance OEMs to reduce the energy intensity of production lines, particularly in powder coating curing operations.

A central innovation addressing this requirement is the development of low-cure powder coatings, capable of achieving full cross-linking at peak metal temperatures of 150°C to 160°C—significantly below the traditional 180°C to 200°C range. This reduction in curing temperature translates directly into measurable energy savings, with manufacturers reporting 15%–20% reductions in oven-related energy consumption.

Operational efficiency gains extend beyond energy use. Lower curing thresholds enable shorter dwell times, allowing coating lines to increase throughput by approximately 10% without compromising film performance. This is particularly valuable in high-volume appliance manufacturing environments where marginal efficiency gains translate into substantial cost savings.

Additionally, low-cure technologies are expanding substrate compatibility. The ability to coat heat-sensitive materials—including light-gauge metals and certain composites—supports the industry’s broader push toward lightweight appliance design, improving logistics efficiency and reducing material costs.

PFAS Phase-Out Reshaping Non-Stick Coating Technologies

The regulatory landscape in Europe is driving a fundamental shift in non-stick coating chemistry, as restrictions on per- and polyfluoroalkyl substances (PFAS) approach full implementation. The proposed limits—targeting concentrations as low as 25 parts per billion—effectively eliminate traditional fluoropolymer-based coatings such as PTFE from most consumer appliance applications.

This regulatory pressure has accelerated the transition toward ceramic-based sol-gel and silicone hybrid coatings, with more than 80% of European manufacturers already adopting or launching PFAS-free alternatives. These coatings are designed to deliver comparable release performance while addressing long-term environmental and health concerns associated with “forever chemicals.”

Performance improvements have been critical to adoption. Modern ceramic-hybrid coatings can withstand temperatures up to 450°C—nearly double the thermal tolerance of legacy fluoropolymer systems—while maintaining non-stick functionality. This enables their use across a broader range of appliances, including high-temperature cooking devices such as air fryers and grills.

The regulatory trajectory suggests that PFAS-free coatings will become the default standard rather than a premium alternative. Manufacturers that fail to transition risk both regulatory exclusion and reputational challenges, making this shift a structural realignment of coating chemistry across the appliance sector.

Anti-Fingerprint Coatings Enhancing Premium Appliance Aesthetics

Consumer preferences are increasingly influencing coating innovation, particularly in the premium appliance segment where aesthetics and ease of maintenance are key differentiators. Anti-fingerprint (AFP) clear coatings are emerging as a high-value solution for stainless steel and mixed-material surfaces.

These coatings utilize nano-engineered surface structures to achieve water contact angles exceeding 105°, enabling liquids and oils to bead and be easily removed. This significantly reduces visible smudging and simplifies cleaning, addressing a common consumer pain point in modern kitchens.

Durability is a critical performance metric in this category. Advanced UV-cured AFP coatings maintain over 95% of their initial gloss after extensive abrasion testing, ensuring long-term retention of a “showroom-quality” finish. This is particularly important for high-touch surfaces such as refrigerator doors and oven panels.

Additionally, these coatings contribute to design consistency across appliances by providing uniform matte or satin finishes, enabling seamless integration of different materials within a single product line. The integration of antimicrobial additives in approximately 40% of new formulations further enhances their functionality, particularly in shared or high-use environments.

Waterborne Epoxy Liners Advancing Food Safety and Emission Reduction

The shift toward safer and more sustainable coating systems is also evident in the adoption of waterborne epoxy coatings for appliance interiors, particularly in refrigerators and freezers. These coatings must meet stringent performance requirements, including moisture resistance, chemical stability, and compliance with food-contact safety standards.

One of the most significant advantages of waterborne systems is their ability to reduce VOC emissions by up to 90% compared to solvent-based alternatives, allowing manufacturers to meet environmental regulations without investing in costly emission control technologies such as regenerative thermal oxidizers.

Performance parity with traditional systems has been largely achieved. Modern waterborne epoxy coatings exhibit moisture vapor transmission rates comparable to high-solids solvent systems, ensuring effective corrosion protection in high-humidity environments such as evaporator compartments.

These coatings also offer greater curing flexibility, with formulations designed for ambient or low-temperature curing processes. This reduces the risk of thermal deformation in thin substrates and aligns with broader energy efficiency goals in appliance manufacturing.

Water-Borne Coatings Lead Consumer Appliance Market with 42% Share Driven by VOC Compliance and High-Speed Manufacturing

Technology Analysis: Water-Based Polyurethane and Polyester Systems Dominate with Wet-on-Wet Efficiency

Water-borne coatings hold a leading 42.0% share of the consumer appliance coatings market in 2025, driven by their ability to meet stringent VOC regulations such as EPA NESHAP 6H and EU IED standards while supporting high-speed, automated production lines. Modern formulations—including water-borne acrylics, polyurethane dispersions (PUDs), and polyester-melamine systems—enable wet-on-wet application processes, where primer and topcoat are applied sequentially without intermediate curing, reducing energy consumption and production footprint. These coatings now deliver full performance parity with solvent-borne systems, offering excellent chemical resistance to household cleaners, high gloss retention, and durability required for appliances such as refrigerators, washing machines, and dishwashers. Additionally, their superior ability to coat complex geometries—including deep-drawn components and intricate assemblies—ensures uniform coverage and corrosion protection, reinforcing water-borne dominance in the global appliance coatings market.

Aesthetic & Decorative Coatings Lead with 46% Share Driven by Premium Finishes and Consumer Design Trends

Functional Specification Analysis: Stainless Steel Look and Matte Finishes Drive High-Value Coating Demand

Aesthetic and decorative coatings account for a dominant 46.0% share of the consumer appliance coatings market in 2025, as visual appeal remains the primary purchasing factor for consumers. A key trend is the widespread adoption of “stainless steel look” coatings, achieved through multi-layer systems combining metallic basecoats, printed grain patterns, and protective clearcoats, delivering premium aesthetics at 40–60% lower cost than real stainless steel. Additionally, evolving consumer preferences are driving demand for matte black, black stainless, and warm neutral finishes, replacing traditional high-gloss white coatings. These finishes require advanced technologies such as self-matting polyurethane and UV-cured coatings, which provide scratch resistance, anti-fingerprint properties, and easy-clean performance. The rise of custom colors and designer finishes further enhances product differentiation, making aesthetic coatings a key value driver in the consumer appliance coatings market.

Consumer Appliance Coatings Market Competitive Landscape Driven by Powder Coatings, Functional Surfaces, and Smart Appliance Integration

The consumer appliance coatings market is driven by demand for durable, low-VOC coatings, anti-fingerprint surfaces, and smart functional coatings. Competition focuses on powder coatings, sustainability, and advanced surface aesthetics tailored for premium appliances, electronics, and connected home devices.

AkzoNobel Advances Powder Coatings Leadership with Laser-Curing and Strategic Merger

AkzoNobel N.V. is strengthening its leadership in consumer appliance coatings through its proposed merger with Axalta, creating a $17 billion coatings powerhouse with extensive global manufacturing capabilities. The company reported €10.15 billion in 2025 revenue with EBITDA margins rising to 14.2%, supported by €200 million in cost savings. Its 2026 “Rhythm of Blues” collection introduces appliance-specific finishes aligned with evolving consumer design trends. AkzoNobel is pioneering laser-curing technology in partnership with IPG Photonics, significantly reducing carbon emissions in appliance coating lines. Its continued investment in industrial excellence and facility modernization enhances operational efficiency. The company’s leadership in powder coatings and sustainable chemistry reinforces its dominance in appliance coatings.

PPG Expands Functional Appliance Coatings with Soft-Touch and Smart Surface Technologies

PPG Industries, Inc. remains a top-tier player with over $18 billion in revenue, delivering integrated coating solutions for consumer appliances and electronics. Its Velvecron® stain-resistant coating provides premium soft-touch finishes while maintaining high durability and chemical resistance. PPG is expanding transparent and conductive coatings to support touchscreen-enabled smart appliances and control panels. The company achieved a 15% reduction in carbon emissions by early 2026, reflecting strong sustainability progress. Its robust financial performance, including record Q1 2026 EPS, is driven by growth in high-margin specialty coatings. PPG’s innovation in functional coatings positions it strongly in next-generation smart appliance markets.

Sherwin-Williams Strengthens Appliance Coatings Portfolio with Integrated Supply Chain and Expansion

The Sherwin-Williams Company reported $23.57 billion in 2025 sales and continues to expand its appliance coatings footprint through strategic acquisitions such as Suvinil. Its vertically integrated distribution model enables efficient supply chain management and supports continuous reinvestment in automated coating systems. The company’s Performance Coatings Group is achieving strong account growth despite fluctuating demand conditions. Sherwin-Williams leverages its packaging and performance segments to deliver food-safe, corrosion-resistant coatings for appliance interiors. Its strong cash flow generation supports ongoing innovation and capacity expansion. The company’s integrated capabilities strengthen its position in global appliance coatings markets.

Axalta Enhances Premium Appliance Coatings with High-Durability and Anti-Fingerprint Technologies

Axalta Coating Systems is executing its 2026 strategic plan with strong financial performance, achieving a 22.0% EBITDA margin and $5.11 billion in sales. Its upcoming merger with AkzoNobel will significantly expand its global reach and R&D capabilities. Axalta specializes in high-durability coatings designed to withstand thermal cycling in appliance applications. The company is developing advanced anti-fingerprint and easy-clean coatings for stainless-look appliances, addressing consumer demand for aesthetics and functionality. Strong free cash flow supports ongoing innovation and operational improvements. Axalta’s focus on premium finishes and functional coatings enhances its competitiveness in appliance coatings.

Nippon Paint Expands Specialty Coatings with Strong APAC Presence and Green Chemistry Focus

Nippon Paint Holdings (NIPSEA Group) is accelerating growth through its asset assembler model and the $2.3 billion AOC acquisition, strengthening its specialty resins portfolio. The company is trending toward ¥1.6 trillion in revenue for 2026, supported by strong performance in China and Southeast Asia. Its focus on green chemistry and low-VOC coatings aligns with growing demand for sustainable appliance finishes. Nippon Paint leverages its dominance in decorative and OEM markets to cross-sell advanced coatings to appliance manufacturers. Its decentralized structure enables rapid market responsiveness and innovation. The company’s regional strength and sustainability focus reinforce its competitive positioning.

TIGER Coatings Leads in Premium Powder Coatings with Advanced Surface Aesthetics

TIGER Coatings is a specialist in powder coatings, focusing on high-end surface finishes for premium appliances and lighting applications. Its 2026 Trend Colors collection introduces innovative finishes such as Aurum Ascendic and Quantum Silver, catering to luxury appliance markets. The company’s powder coatings eliminate VOC emissions, making them ideal for environmentally conscious manufacturers. TIGER’s expertise in custom surface aesthetics allows OEMs to differentiate their products in competitive premium segments. Its innovations in texture and durability enhance both functionality and visual appeal. The company’s focus on sustainable, design-driven coatings strengthens its niche leadership in appliance coatings.

India Consumer Appliance Coatings Market: Regulatory Enforcement and Localization Driving Rapid Growth

India has emerged as a high-growth hub for consumer appliance coatings, transitioning toward a regulated, premium-quality market under the “Make in India” initiative. A major inflection point is the Quality Control Order (QCO) 2025, effective March 2026, which mandates 100% BIS compliance for household appliances—forcing manufacturers to adopt high-purity, flame-retardant coating systems.

Policy-driven manufacturing expansion is a key driver. The PLI scheme for white goods, with investments of ₹1.46 lakh crore, is accelerating domestic production of corrosion-resistant epoxy-polyester hybrid coatings for refrigerators and air conditioners. Additionally, the $1.4 trillion National Infrastructure Pipeline (NIP) and rapid urbanization are expected to significantly increase appliance penetration, boosting coating demand. Smart city initiatives are also promoting antimicrobial silver-ion coatings in healthcare and commercial kitchen appliances. Sustainability trends are evident, with waterborne and low-VOC powder coatings growing at ~5.2% annually, aligning with export requirements.

China Consumer Appliance Coatings Market: AI Integration and Green Manufacturing Driving Scale Leadership

China remains the global leader in appliance coatings, leveraging its manufacturing scale and AI-driven innovation. Under “Dual Carbon” targets, manufacturers are transitioning toward zero-emission powder coating systems, particularly for high-volume appliance production.

Technological innovation is a key differentiator. The rise of smart cleaning appliances has driven adoption of nano-ceramic anti-scratch coatings, while expanded capacity at sites like Jiaxing is boosting production of UV-curable and waterborne resins. Regulatory updates under GB 4806.10 are tightening food-contact safety requirements, favoring silicone-based, BPA-free coatings. Additionally, demographic trends are shaping product design, with younger consumers driving demand for compact appliances with textured finishes, while premium segments focus on energy-efficient, high-durability coatings.

United States Consumer Appliance Coatings Market: Nearshoring and Functional Coatings Driving Premium Growth

The United States market is evolving through nearshoring strategies and high-value coating innovations. Growth under USMCA is driving investment in automated powder coating lines across North American appliance assembly plants.

Advanced coating technologies are shaping demand. The transition to cationic electrocoat (e-coat) systems ensures uniform coverage for complex appliance components, while the CHIPS Act is improving availability of conductive additives for IoT-enabled smart appliances. Regulatory pressure has triggered a 20% shift toward zero-VOC and ultra-high-solid coatings, enhancing sustainability. Additionally, premiumization trends are driving adoption of fingerprint-resistant nano-coatings for stainless steel surfaces, while EPA-led recycling initiatives are encouraging easy-to-strip coatings to improve end-of-life recyclability.

Germany Consumer Appliance Coatings Market: Bio-Circular Innovation and Precision Engineering Driving Sustainability

Germany leads in high-performance and sustainable appliance coatings, driven by strict REACH compliance and advanced R&D. The country has achieved a ~90% phase-out of PFAS-based surfactants, transitioning toward environmentally safe alternatives.

Innovation is centered on advanced materials. Developments include self-healing polyurethane coatings that repair surface scratches automatically, and the adoption of UV-LED and electron beam (EB) curing technologies, reducing energy consumption by ~22%. Germany is also pioneering Digital Product Passports (DPP), enabling full traceability of coating materials. Additionally, the trend toward miniaturization is increasing demand for thin-film conformal coatings in appliance electronics, reinforcing Germany’s leadership in precision coating technologies.

Japan Consumer Appliance Coatings Market: High-Performance Specifications and Antibacterial Innovation Driving Leadership

Japan’s market is defined by stringent quality standards and high-performance coating requirements. The country invests over $2.1 billion annually in R&D, focusing on advanced materials such as thermally conductive coatings for heating elements in appliances.

Post-pandemic hygiene standards continue to shape demand. The widespread adoption of photocatalytic antibacterial coatings is now a standard feature in appliances like washing machines. Additionally, Japan is advancing anti-static and anti-reflective coatings for smart appliance displays, supported by significant public-sector funding. Automation is also improving efficiency, with robotic spray systems using laser-guided sensors ensuring precision coating thickness. These innovations position Japan as a leader in high-specification appliance coatings.

Brazil Consumer Appliance Coatings Market: Capacity Expansion and Bio-Based Innovation Driving Regional Growth

Brazil is strengthening its position in the appliance coatings market through capacity expansion and local manufacturing incentives. Investments such as WEG’s R$70 million expansion are increasing production of industrial liquid coatings for domestic white goods.

The market is also benefiting from infrastructure and electrification. Expansion of logistics and grid networks is driving demand for anti-corrosive coatings in appliances used in coastal and rural regions. Brazil is also leveraging its agricultural strength to develop bio-based polyurethane coatings from castor oil, supporting sustainability goals. Additionally, the adoption of automotive-grade clear coatings in premium appliances is enhancing aesthetic quality, while import substitution policies are strengthening domestic supply chains.

South Korea Consumer Appliance Coatings Market: UV-Curing Leadership and Aesthetic Innovation Driving Global Competitiveness

South Korea is a leader in fast-curing and design-focused appliance coatings, leveraging its strengths in electronics and material science. The adoption of high-speed UV-cured coatings has reduced production times by approximately 25%, significantly improving manufacturing efficiency.

Innovation is centered on smart and aesthetic applications. The development of ultra-thin protective coatings for OLED-integrated appliance surfaces ensures durability while maintaining high clarity. Government support for “K-Appliance” initiatives is driving advancements in textured and gradient coatings, enhancing product design appeal. Additionally, strict eco-label standards—such as zero-formaldehyde emission mandates—are pushing a full transition toward solvent-free powder coatings. South Korea’s expertise in marine coatings is also being leveraged to create ultra-durable finishes for appliances in coastal environments.

Consumer Appliance Coatings Market Report Scope

Consumer Appliance Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.3 Billion

|

|

Market Size (2032)

|

$4.8 Billion

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Resin Chemistry (Epoxy, Epoxy-Polyester Hybrid, Polyester, Polyurethane (PU), Acrylic, Specialty), By Technology (Water-borne, Solvent-borne, UV-Cured and Radiation Curable), By Application (Refrigeration and Freezers, Cooking Appliances, Home Laundry, Dishwashers, Small and Smart Appliances), By Functional Specification (Aesthetic and Decorative, Antimicrobial and Sanitized, Anti-Fingerprint and Easy-Clean, Scratch and Impact Resistant, Heat Stable)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sherwin-Williams Company, PPG Industries, Inc., AkzoNobel N.V., Axalta Coating Systems Ltd., Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd., Jotun A/S, Tiger Coatings GmbH & Co. KG, Beckers Group, RPM International Inc., Hempel A/S, Henkel AG & Co. KGaA, Asian Paints Limited, KCC Corporation, Meijia New Material Technology Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Consumer Appliance Coatings Market Segmentation

By Resin Chemistry

- Epoxy

- Epoxy-Polyester Hybrid

- Polyester

- Polyurethane (PU)

- Acrylic

- Specialty

By Technology

- Water-borne

- Solvent-borne

- UV-Cured and Radiation Curable

By Application

- Refrigeration and Freezers

- Cooking Appliances

- Home Laundry

- Dishwashers

- Small and Smart Appliances

By Functional Specification

- Aesthetic and Decorative

- Antimicrobial and Sanitized

- Anti-Fingerprint and Easy-Clean

- Scratch and Impact Resistant

- Heat Stable

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Consumer Appliance Coatings Market

- Sherwin-Williams Company

- PPG Industries, Inc.

- AkzoNobel N.V.

- Axalta Coating Systems Ltd.

- Nippon Paint Holdings Co., Ltd.

- Kansai Paint Co., Ltd.

- Jotun A/S

- Tiger Coatings GmbH & Co. KG

- Beckers Group

- RPM International Inc.

- Hempel A/S

- Henkel AG & Co. KGaA

- Asian Paints Limited

- KCC Corporation

- Meijia New Material Technology Co., Ltd.

*- List not Exhaustive