Market Overview: Key Insights into Consumer Packaging Growth

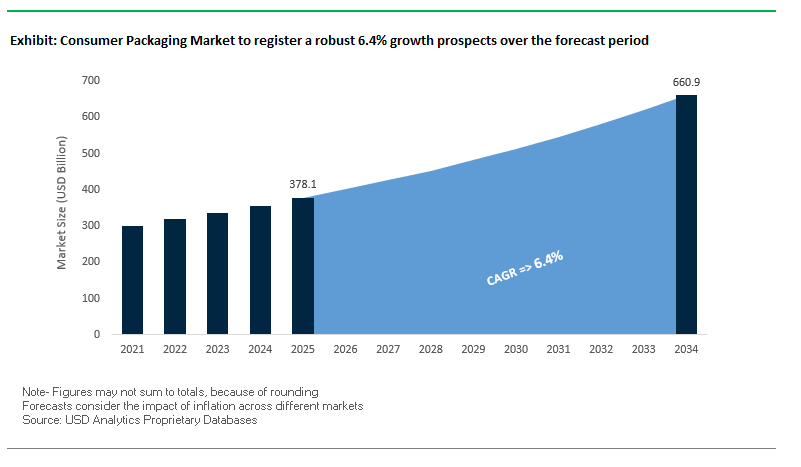

The Global Consumer Packaging Market is valued at USD 378.1 billion in 2025 and is projected to reach USD 660.8 billion by 2034, expanding at a healthy CAGR of 6.4%. Packaging has evolved from being a functional necessity to becoming a critical factor in consumer purchase decisions, with recyclability, sustainability, and convenience shaping the future of the sector. According to a recent Amcor report, 84% of consumers check on-pack recycling instructions before making a purchase, emphasizing that recyclability is now the single most influential driver of consumer choices in Europe.

The market is undergoing structural transformation led by regulatory frameworks like the EU’s Packaging and Packaging Waste Regulation (PPWR), which mandates recycled content inclusion and reduction of single-use plastics. Paper is emerging as a preferred alternative, with 72% of consumers expressing confidence in paper packaging claims, fueling rapid adoption across FMCG brands. At the same time, the rise of e-commerce has created demand for protective and branded solutions such as corrugated boxes, air cushions, and display-ready packaging to balance safety with consumer experience. Furthermore, circular economy strategies are gaining momentum, with major packaging producers scaling the use of PCR (post-consumer recycled) content to comply with upcoming 2030 targets.

Key Insights for Industry Professionals:

- Recyclability and on-pack disposal guidance now dominate purchase decisions.

- Paper-based packaging adoption is accelerated by regulations and consumer preference.

- E-commerce boom fuels corrugated and protective packaging innovation.

- Circular economy and PCR mandates are reshaping strategies across packaging majors.

Market Analysis: Recent Strategic Developments in Consumer Packaging

The consumer packaging industry has seen significant consolidation, innovation, and investments in sustainability. In August 2025, Graphic Packaging International introduced CleanClose™ child-resistant paperboard pods packaging, highlighting the dual focus on safety and fiber-based innovation. Around the same time, Amcor launched its lightweight Hector CRC closure, manufactured with up to 100% PCR plastic, reinforcing its commitment to eco-friendly solutions.

Strategic realignments have also been prominent. In July 2025, International Paper completed the divestiture of five European corrugated plants to meet regulatory conditions after acquiring DS Smith, reshaping its European footprint in fiber-based consumer packaging. Earlier, in April 2025, Amcor released findings underscoring that sustainability claims directly impact consumer purchasing behavior, giving packaging companies a roadmap for messaging.

Mergers and acquisitions are driving scale advantages. Ball Corporation made a minority investment in Swedish start-up Meadow in January 2025, targeting recyclable aluminum cans for home and personal care categories. In November 2024, Amcor acquired Berry Global, creating the largest resin purchaser globally, while in October 2024, Smurfit Kappa merged with WestRock to form Smurfit WestRock, establishing a new leader in fiber-based packaging. By December 2024, International Paper also finalized its acquisition of DS Smith, further consolidating the sector.

Emerging Trends and Strategic Opportunities Shaping the Consumer Packaging Market

Corporate Investment in Advanced Recycling Technologies to Drive Circular Packaging

A significant trend in the consumer packaging market is the increasing corporate investment in advanced recycling technologies, including chemical recycling methods like pyrolysis and depolymerization. Traditional mechanical recycling cannot process complex multilayer films and flexible plastics, making advanced recycling essential for creating post-consumer recycled (PCR) content that meets high-performance standards. Major consumer goods and chemical companies are forming partnerships to de-risk investments and secure long-term agreements for the output of advanced recycling facilities. Industry reports indicate that scaling chemical recycling is critical for brands aiming to incorporate up to 50% recycled content into packaging, positioning this trend as a key growth driver. The move toward advanced recycling technologies creates a lucrative avenue for packaging material suppliers, technology developers, and consumer goods firms seeking sustainable, circular solutions while meeting regulatory and consumer expectations.

Integration of Smart Packaging for Supply Chain Visibility and Consumer Engagement

Another transformative trend in the consumer packaging market is the integration of smart packaging technologies such as QR codes, NFC tags, and RFID chips. This evolution is fueled by e-commerce growth, consumer demand for product transparency, and regulatory pressure for supply chain accountability. Regulations like the EU Corporate Sustainability Reporting Directive, along with anti-slavery acts in the UK and Australia, require brands to monitor and report on environmental and labor practices throughout their supply chains. Smart packaging allows real-time tracking, enhances anti-counterfeiting measures, and provides a platform for direct consumer engagement, including product origin, ingredient transparency, and sustainability data. Brands across sectors, from food to cosmetics, are leveraging smart packaging to boost consumer confidence and loyalty. This trend not only enhances supply chain efficiency but also opens a data-rich avenue for brand storytelling and market differentiation.

Development of Mono-Material Packaging Solutions for Enhanced Recyclability

The growing demand for mono-material packaging solutions represents a significant opportunity within the consumer packaging market. Multi-material laminates often cannot be recycled due to incompatible layers, creating a pressing need for high-performance, single-material alternatives. Companies like Mondi are developing mono-material stand-up pouches and barrier films that are certified recyclable while maintaining critical protection against oxygen, moisture, and light. R&D focuses on advanced coatings and thin-film technologies to achieve barrier performance comparable to multi-layer solutions. As consumer awareness of sustainable packaging rises and governments implement stricter regulations, mono-material solutions are poised for rapid adoption. This trend creates a growth avenue for packaging converters and material scientists who can deliver certified, aesthetically appealing, and environmentally responsible products.

Leveraging Government Incentives to Expand Domestic Recycling Infrastructure

A substantial opportunity in the consumer packaging market lies in leveraging government incentives for domestic recycling infrastructure. U.S. policies like the Inflation Reduction Act (IRA) and the Bipartisan Infrastructure Law (BIL) provide funding, grants, and tax credits to build or modernize recycling and material recovery facilities. With the U.S. historically exporting large volumes of plastic waste now restricted due to bans in importing countries there is an urgent need for domestic solutions. The BIL’s Advanced Energy Manufacturing and Recycling Grants Program and IRA tax credits lower capital costs and mitigate investment risks for companies establishing recycling operations. This opportunity enables packaging producers and waste management firms to create a robust, resilient domestic circular economy, reduce reliance on imports, and support the sustainability goals of consumer goods brands.

Competitive Landscape: Leading Companies in Consumer Packaging Industry

The consumer packaging industry is moderately consolidated with a mix of global packaging giants, fiber-specialists, and metal/aluminum leaders. Competitive advantages are built on sustainability credentials, global reach, and integration across the value chain.

Amcor PLC leads sustainability with Berry Global acquisition

Amcor is a global leader in flexible and rigid packaging across food, healthcare, and personal care. In late 2024, it announced its acquisition of Berry Global, creating the world’s largest resin buyer. With a strategy focused on making all packaging recyclable or reusable by 2025, Amcor continues to deliver mono-material films, flexible laminates, and innovative closures. Its strong global presence in over 40 countries gives it unmatched delivery capacity across industries.

Smurfit WestRock emerges as a fiber-based packaging powerhouse

The October 2024 merger of Smurfit Kappa and WestRock created Smurfit WestRock, one of the largest paper and corrugated packaging players worldwide. The company’s portfolio includes corrugated boxes, folding cartons, and bag-in-box systems, serving e-commerce and retail sectors. Its strategic focus on lightweighting and sustainable materials ensures alignment with global consumer brands seeking eco-friendly paper-based solutions.

Berry Global enhances circular plastic strategies before merger with Amcor

Berry Global, a specialist in rigid and flexible plastic packaging, has merged with Amcor in late 2024, enhancing their global scale. Berry’s portfolio includes bottles, closures, and films with strong barrier properties. Its strategy emphasizes circular economy practices, including the integration of recycled content into packaging, leveraging its vertically integrated manufacturing model.

Ball Corporation drives circular aluminum packaging innovation

Ball is a global leader in aluminum packaging, particularly beverage cans, bottles, and aerosols. In January 2025, it announced a minority investment in Meadow, signaling a push to expand recyclable aluminum into personal care and household products. With a goal of 90% aluminum recycling rates by 2030, Ball leverages low-carbon circular strategies as its key differentiation.

DS Smith expands via International Paper acquisition

DS Smith, known for its corrugated and retail-ready packaging, was acquired by International Paper in December 2024. Its focus is on recyclable paper-based packaging solutions, backed by an integrated model from paper collection to design and manufacturing. DS Smith’s role is pivotal in supplying e-commerce and FMCG brands with sustainable fiber packaging.

Sonoco Products strengthens position with Eviosys acquisition

Sonoco is a global supplier of value-added consumer packaging with expertise in rigid paper and flexible films. In late 2024, it acquired Eviosys, expanding into metal packaging for food cans and aerosols. Its EnviroSense™ product range focuses on sustainable packaging, while its global footprint ensures reliable supply to both small-scale brands and multinationals.

Consumer Packaging Market Share Insights

Flexible Packaging Dominates Market Share by Packaging Format in Consumer Packaging

Flexible packaging leads (58% share) on cost-to-protect ratio, lightweighting, and barrier performance that extends shelf life for everyday essentials. It is the format of choice for single-serve and portion-controlled products, aligning with on-the-go consumption and e-grocery fulfillment. The technology agenda is shifting rapidly from mixed laminates to mono-material PE/PP structures and recycle-ready paper laminates that meet retailer recyclability scorecards without sacrificing seal integrity, oxygen/moisture barrier, or machinability. Rigid packaging (42%) retains indispensable roles glass for beverages, rPET/rHDPE bottles and tubs where structure, hot-fill/retort tolerance, and premium shelf presence are non-negotiable benefiting from rising PCR content and refill/reuse models that defend share against flexibles.

Food & Beverages Continues to Anchor Market Share by End-Use in Consumer Packaging

With 55% share, food & beverages is the battleground for sustainability, convenience, and safety concentrating investment in recyclable/compostable materials, easy-open/reseal features, and high-barrier structures that cut food waste. Personal care & cosmetics punches above its volume weight by specifying premium, brand-defining packs (heavy-wall glass, airless pumps, PCR plastics) and piloting refill/reuse; e-commerce has matured into a distinct end-use, forcing right-sizing, curbside-recyclable mailers, and ISTA-certified ship-in-own-container designs that reduce DIM weight and returns. Homecare pivots to concentrates and refill pouches to shrink plastic per dose, while consumer healthcare evolves more slowly under tamper-evidence and child-resistance requirements that prioritize regulatory continuity.

United States Consumer Packaging Market Driven by EPR Regulations and Advanced Automation

The U.S. consumer packaging market is being shaped by a patchwork of state-level Extended Producer Responsibility (EPR) regulations, including California's SB 54, which mandates a 25% reduction in plastic packaging by 2032 and full recyclability or compostability for all packaging. These policies are compelling consumer packaged goods (CPG) companies to partner with co-packers and converters specializing in sustainable and recyclable materials. Technological advancements are transforming the sector, with automation and AI-enabled robotics addressing labor shortages, optimizing secondary packaging lines, and enabling predictive maintenance to reduce downtime and scrap.

Key applications span food and beverage, personal care, and e-commerce sectors, where right-sized, protective, and data-rich packaging solutions are increasingly essential for last-mile delivery efficiency. Sustainability remains a core focus, with reformulated grease-resistant papers, plant-based coatings, and DOE-backed cellulose-based films gaining traction. Premium brands are also innovating functionality with multilayer high-barrier films, resealable pouches, and transparent windows that extend shelf life while supporting clean-label formulas. Academic research, such as Georgia Tech’s development of chitin-cellulose films with superior oxygen barrier properties, is driving further material science innovations in packaging.

Germany Consumer Packaging Market Strengthened by Circular Economy Leadership and Industry 4.0 Integration

Germany’s consumer packaging market operates under a rigorous regulatory framework, including the EU Packaging and Packaging Waste Regulation (PPWR) and the Packaging Act (VerpackG), which mandates full recyclability or reuse of packaging by 2030. The German Supply Chain Act (LkSG) ensures compliance with human rights and environmental standards, increasing scrutiny on suppliers and packaging producers. Circular economy leadership is evident through modulated fees incentivizing recyclable design, and strong collaboration between manufacturers and regulators is fostering sustainable packaging innovation.

Technological innovation is advancing rapidly, with increased orders for machinery capable of handling bio-based materials and development of digital product passports and watermarks to enhance material transparency. Digitalization and automation under Germany’s Plattform Industrie 4.0 initiative are improving productivity and efficiency through IoT integration and cyber-physical systems. Key applications focus on food, beverage, and retail sectors, particularly premium and artisanal products, where consumers demand high-end, visually appealing packaging that aligns with environmental standards.

China Consumer Packaging Market Accelerated by Dual Carbon Goals and Domestic Manufacturing Expansion

China’s consumer packaging industry is being driven by governmental “dual carbon” initiatives and the March 2024 Action Plan for Large-Scale Equipment Updates, promoting sustainable materials and recycling practices. Regulatory reforms, including restrictions on packaging layers and void ratios, directly impact packaging suppliers across food, cosmetics, and e-commerce sectors, while express delivery regulations mandate reduced and reusable packaging.

Technological advancements in automation, AI, and integration of “5G plus industrial internet” are optimizing production efficiency and flexible manufacturing capacity. Domestic manufacturing is being prioritized to reduce reliance on imported technology, while the rapid growth of e-commerce, fresh food, and food delivery sectors continues to fuel packaging demand. China is a global hub of innovation, with extensive patents resulting from research into new materials, high-performance films, and automated packaging solutions that support sustainability and cost-effectiveness.

India Consumer Packaging Market Expanding Through Government Initiatives and Recycling Investments

India’s consumer packaging market is growing due to government initiatives such as the Swachh Bharat Abhiyan and plastic waste management rules, including bans on certain single-use plastics and EPR mandates requiring 30% recycled content in rigid plastics by 2025. Corporate investments exceeding INR 10,000 crore are upgrading recycling infrastructure, with key players like Indorama Ventures, Dhunseri, and Varun Beverages expanding capacity to meet rising demand.

Technological adoption includes automated systems and innovative plastic-free laminate films suitable for paper and foil lamination. Rapid growth in domestic e-commerce, food and beverage, and pharmaceutical sectors is driving demand for flexible and cost-effective consumer packaging solutions. Strategic partnerships, such as the CIRCLE Alliance launched by Unilever, USAID, and EY with a USD 21 million commitment, promote packaging circularity and plastic waste reduction. Key applications include ready-to-drink beverages and processed foods, where sustainable, high-performance packaging is increasingly critical.

Brazil Consumer Packaging Market Accelerating with Sustainable Policies and Major Investments

Brazil’s consumer packaging industry is benefiting from the National Solid Waste Policy and 2024 legislation banning single-use disposable items, with a 2030 deadline for fully compostable or recyclable packaging. Technological advancements, including robotics and AI, are enhancing efficiency and quality control, while biodegradable films using carboxymethyl cellulose (CMC) from sugarcane bagasse exemplify innovation in sustainable materials.

Corporate investments highlight market momentum, with Smurfit Westrock committing R$840 million to expand production capacity in Santa Catarina for domestic and export markets. The food, beverage, and cosmetics sectors are major drivers, supported by Brazil’s expanding food processing industry. Government support through FINEP, including Melhoramentos’ R$40 million investment in sustainable cellulose fiber packaging, further accelerates growth. Sustainability remains a central focus, positioning Brazil as a key player in the global consumer packaging market.

Japan Consumer Packaging Market Shaping Through Advanced Materials and Innovative Design

Japan’s consumer packaging industry is distinguished by advanced manufacturing capabilities and precision technology, blending traditional aesthetics with modern design principles. Regulatory guidance, such as the Plastic Resource Circulation Act effective since April 2022, promotes eco-friendly “design for the environment” packaging and reduces single-use plastics.

The market is focused on high-performance films with superior barrier properties and IoT-enabled tracking, catering to specialty applications requiring dimensional stability and deformation resistance. Corporate collaborations with firms like Nestlé and Meiji drive the development of innovative packaging solutions, as seen with Nestlé’s 2025 launch of KitKat flavors packaged in individual boxes for local and international markets. Academic research is supporting sustainable innovation, using biopolymers and natural agents to produce environmentally friendly packaging with high functionality, reflecting Japan’s leadership in next-generation consumer packaging solutions.

Consumer Packaging Market Report Scope

Consumer Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$378.1 Billion

|

|

Market Size (2034)

|

$660.8 Billion

|

|

Market Growth Rate

|

6.4%

|

|

Segments

|

By Packaging Material (Paper & Paperboard, Plastic, Glass, Metal, Wood, Other Materials), By Packaging Format (Flexible Packaging, Rigid Packaging), By End-Use Industry (Food & Beverages, Personal Care & Cosmetics, Healthcare, E-commerce, Homecare, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, Smurfit Kappa Group plc, Huhtamaki Oyj, Constantia Flexibles, Sonoco Products Company, DS Smith plc, WestRock Company, Sealed Air Corporation, Silgan Holdings Inc., Berry Global Group, Inc., Ball Corporation, Crown Holdings, Inc., Uflex Ltd., Graphic Packaging Holding Company

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Consumer Packaging Market Segmentation

By Packaging Material

- Paper & Paperboard

- Plastic

- Glass

- Metal

- Wood

- Other Materials

By Packaging Format

- Flexible Packaging

- Rigid Packaging

By End-Use Industry

- Food & Beverages

- Personal Care & Cosmetics

- Healthcare

- E-commerce

- Homecare

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Consumer Packaging Market

- Amcor plc

- Mondi Group

- Smurfit Kappa Group plc

- Huhtamaki Oyj

- Constantia Flexibles

- Sonoco Products Company

- DS Smith plc

- WestRock Company

- Sealed Air Corporation

- Silgan Holdings Inc.

- Berry Global Group, Inc.

- Ball Corporation

- Crown Holdings, Inc.

- Uflex Ltd.

- Graphic Packaging Holding Company

* List Not Exhaustive

Methodology

The Consumer Packaging Market analysis has been conducted by USDAnalytics through a comprehensive methodology integrating both primary and secondary research tailored for industry professionals. Primary research involved interviews with key stakeholders, including packaging manufacturers, brand owners, recyclers, and regulatory authorities, to gather real-time insights on market trends, technological adoption, sustainability initiatives, and consumer preferences. Secondary research encompassed corporate press releases, annual reports, patent filings, government regulations, academic publications, and trade journals to validate trends and track recent strategic developments. USDAnalytics applied quantitative modeling to forecast market size, growth, and segmentation by packaging material, format, and end-use industry, while qualitative analysis focused on sustainability adoption, circular economy practices, smart packaging integration, and regional regulatory impacts such as the EU Packaging and Packaging Waste Regulation, U.S. EPR mandates, and India’s plastic waste rules. This approach ensures a detailed understanding of innovations in mono-material solutions, advanced recycling technologies, automation, e-commerce packaging, and consumer-driven sustainability, providing actionable insights for decision-makers in the global consumer packaging landscape.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.