Container and Packaging Market Overview: Rising Demand Across Food, Beverage, and E-Commerce Sectors

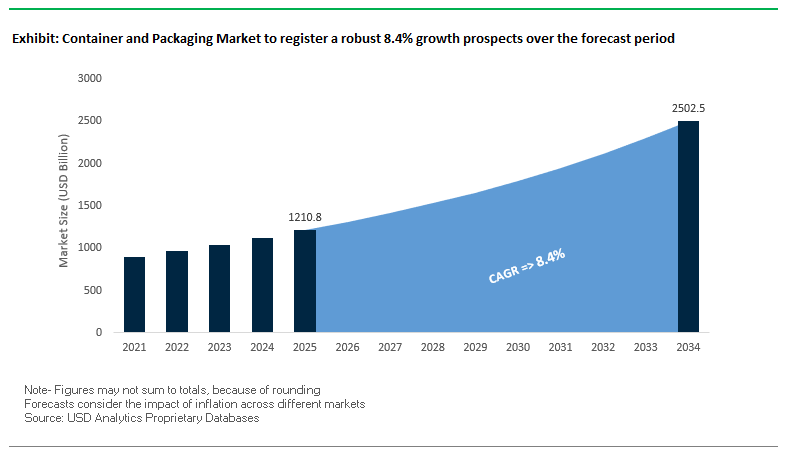

The Global Container and Packaging Market is valued at $1,210.8 billion in 2025 and is projected to reach $2,502.3 billion by 2034, expanding at a strong CAGR of 8.4%. Growth is being driven by the food and beverage industry, which accounts for the largest share of packaging consumption due to its crucial role in preserving freshness, extending shelf life, and ensuring safety during distribution. With rising global consumption of packaged food and beverages, packaging demand continues to expand across both developed and emerging economies.

The industry is also undergoing a rapid sustainability transition, as highlighted by a 2024 Jabil survey, where 68% of packaging decision-makers publicly committed to sustainable packaging, and 36% included measurable targets. The e-commerce boom further amplifies the need for durable yet lightweight packaging that can endure shipping conditions while delivering a premium “unboxing experience. At the same time, monomaterial packaging is gaining traction, simplifying recycling and enabling brands to move closer to a circular economy model.

Key Insights for Industry Professionals

- Food & beverage packaging dominates global demand, ensuring safety and extended shelf life.

- Sustainability commitments are accelerating, with clear targets for recycled, recyclable, and biodegradable packaging.

- E-commerce drives growth, pushing demand for durable, lightweight, and visually appealing packaging.

- Monomaterial solutions simplify recycling, positioning them as a cornerstone of future circular packaging systems.

Market Analysis: Strategic Shifts and Recent Developments in Container and Packaging

The global container and packaging industry has been reshaped by mergers, acquisitions, and sustainability-driven innovations in the last two years. In August 2025, Smurfit WestRock reported strong second-quarter results after its merger, reflecting the competitive strength of the newly formed entity in serving diversified packaging markets. During the same month, Mondi launched its Ad/Vantage Smooth Brown Semi Extensible paper-based line, emphasizing its commitment to high-performance, eco-friendly packaging.

In July 2025, UPM Adhesive Materials (formerly UPM Raflatac) announced an investment in a new coating line in Johor Bahru, Malaysia, strengthening its footprint in Southeast Asia. In April 2025, Amcor finalized its all-stock acquisition of Berry Global, forming a global giant in consumer and healthcare plastic packaging with anticipated synergies exceeding $650 million by 2028. Earlier, in March 2025, Constantia Flexibles and Aluflexpack AG announced their collaboration to enhance leadership in the premium flexible packaging segment.

Consolidation has been a recurring theme. International Paper completed its $7.2 billion acquisition of DS Smith in January 2025, expanding its sustainable packaging leadership across North America and Europe. Meanwhile, Veritiv acquired Orora Packaging Solutions in September 2024, boosting its distribution strength in specialty packaging. Earlier, in July 2024, Smurfit Kappa’s merger with WestRock officially created Smurfit WestRock, now a global paper-based packaging powerhouse. These moves underline a clear industry trajectory sustainability, consolidation, and innovation are defining the next phase of growth.

Container and Packaging Market: Emerging Trends and Opportunities

Mandatory Recycled Content Legislation Driving Material Innovation

The container and packaging market is being reshaped by the introduction of mandatory recycled content legislation, which is forcing rapid innovation in materials and processes. Unlike voluntary sustainability initiatives, these laws impose binding compliance requirements that directly influence corporate strategies and investments. In the United States, states such as California, Washington, Maine, and New Jersey have introduced strict mandates requiring minimum levels of post-consumer recycled (PCR) content in plastic containers. Washington State, for example, has already mandated that plastic beverage bottles contain 15% PCR content by 2023, with targets rising incrementally to 50% by 2031. These laws are not only driving demand for recycled materials but also incentivizing companies to rethink sourcing and production processes.

India is also playing a pivotal role in accelerating the global shift through its Extended Producer Responsibility (EPR) regulations. These policies stipulate progressive recycling and recycled content use across plastic categories, with ambitious targets aiming for 80% recycling of plastic packaging by 2029–30. At the corporate level, brands like The Coca-Cola Company are adapting quickly, pledging to ensure at least 25% of their beverages are sold in reusable packaging by 2030. Coca-Cola’s investment in CuRe Technology, which produces rPET with a carbon footprint 65% lower than virgin PET, highlights how sustainability mandates are shaping corporate capital flows. The convergence of government enforcement and corporate action underscores the shift from optional sustainability to mandatory compliance, positioning recycled content innovation as a defining trend for the packaging industry.

Adoption of Digital Watermarking for Smart Sorting

Another key trend redefining the packaging sector is the integration of digital watermarking technologies, most notably through the HolyGrail 2.0 initiative. This breakthrough technology embeds imperceptible codes into packaging, enabling near-perfect sorting of materials at recycling facilities. Industrial trials conducted at a facility in Germany demonstrated the technology’s scalability, achieving an average of nearly 56,000 detections per day over a 100-day trial with detection efficiency surpassing 90%. Such precision significantly enhances the economic viability of recycling by reducing contamination rates and improving recovery of high-value recyclates.

Digital watermarks also enable more granular sorting, distinguishing between food-grade and non-food-grade packaging. This capability is essential for producing food-safe recycled streams, which are in growing demand due to recycled content mandates across global markets. Importantly, HolyGrail 2.0 is not a solo initiative it is backed by more than 130 companies under the European Brands Association (AIM), signaling strong industry alignment. With adoption programs already launched in Germany and Belgium, this technology is rapidly transitioning from pilot to commercial deployment. As a result, digital watermarking is becoming a cornerstone innovation in intelligent recycling, ensuring regulatory compliance while delivering high-quality materials for circular packaging systems.

Development of Reusable Packaging Systems and Infrastructure

One of the most significant opportunities lies in scaling reusable packaging systems from niche applications to mainstream adoption. While single-use packaging dominates today’s supply chains, growing consumer awareness, corporate pledges, and regulatory pushes are creating fertile ground for reusables. Coca-Cola has pledged that 25% of its global beverage volume will be delivered in reusable packaging by 2030, with initiatives underway across North America, Europe, and Latin America. Retail partnerships are also gaining traction Tesco, for instance, partnered with Loop to integrate reusable packaging into its product offerings, incentivizing participation through refundable deposits managed via digital apps.

However, the expansion of reuse models requires more than brand commitments it demands significant infrastructure development. This includes investments in reverse logistics networks, large-scale cleaning facilities, and standardized packaging formats that simplify the collection and refilling process. Coca-Cola Europacific Partners’ €327 million investment in expanding its refillable portfolio in Germany, including the rollout of a universal bottle, highlights the scale of resources required to build reusable ecosystems. As retailers, logistics providers, and brands align on shared infrastructure, reusable packaging systems present a long-term growth opportunity that aligns profitability with sustainability.

Advanced Bio-Based Materials for Performance Packaging

The development of advanced bio-based materials represents another transformative opportunity for the container and packaging market. Early biopolymers often lacked the barrier properties needed for high-performance packaging, but recent innovations are overcoming these challenges. Research in biopolymer composites shows that incorporating additives can significantly improve oxygen and water vapor barrier properties, making them viable alternatives for sensitive food packaging applications.

Academic studies and pilot-scale trials have demonstrated that bio-based films can achieve tensile strength and barrier metrics comparable to fossil-based plastics. Companies are now scaling up production of materials such as polylactic acid (PLA), derived from agricultural feedstocks and waste, while investments in polyhydroxyalkanoates (PHAs) are accelerating due to their biodegradability and biocompatibility. These new materials have the potential to serve as drop-in replacements for conventional plastics in high-barrier applications such as dairy products, frozen meals, and premium beverages. As regulatory pressures mount and consumers demand eco-friendly alternatives, bio-based packaging materials are moving beyond niche applications, positioning themselves as commercially viable, high-performance solutions that align with circular economy objectives.

Competitive Landscape: Leading Companies in the Global Container and Packaging Industry

The competitive environment is led by multinational corporations that are expanding their global reach, strengthening sustainability portfolios, and consolidating market positions through acquisitions.

Smurfit WestRock: A Global Paper-Based Packaging Powerhouse

Smurfit WestRock, created by the merger of Smurfit Kappa and WestRock in 2024, is now one of the largest providers of paper-based packaging solutions. Its portfolio spans corrugated containers, folding cartons, and specialty paper products. With vertical integration from forest management to recycling, Smurfit WestRock ensures superior quality control and sustainability. In April 2025, the company also invested $3.5 million in social sustainability initiatives, strengthening its leadership in responsible packaging.

Amcor plc: Expanding Global Leadership Through Berry Acquisition

Amcor remains a global leader in flexible and rigid plastic packaging. The April 2025 acquisition of Berry Global, following an $8.4 billion deal announced in November 2024, positioned Amcor as a packaging giant with strong healthcare and consumer portfolios. Its innovation-driven products, such as AmPrima™ Recycle Ready Solutions and AmFiber™ Performance Paper, are designed to replace traditional plastics while ensuring recyclability. Amcor’s strategy focuses on circular packaging systems and achieving 100% recyclable or reusable packaging by 2025.

International Paper Company: Strengthening Sustainable Fiber Packaging

International Paper is a leading player in fiber-based packaging. The January 2025 acquisition of DS Smith expanded its European footprint, cementing its position in sustainable paperboard and containerboard solutions. The company’s $250 million investment in 2024 to convert a mill for containerboard production demonstrates its commitment to scaling eco-friendly solutions. Its long-term focus remains on sustainable product innovation and high-performance paper packaging for global brands.

Mondi Group: Innovating with High-Barrier Sustainable Solutions

Mondi Group continues to lead in sustainable packaging and paper solutions. In August 2025, Mondi invested in a biomass power plant at its Slovakia mill, reducing fossil fuel dependency by 90%. The company’s FunctionalBarrier Paper Ultimate provides a recyclable, ultra-high-barrier alternative to plastics and aluminum, positioning Mondi as a pioneer in sustainable innovation. Its portfolio serves food, pet food, and home care sectors with recyclable, compostable, and reusable solutions.

Berry Global Group, Inc.: Integrated into Amcor’s Global Operations

Berry Global, now part of Amcor, was a major manufacturer of plastic containers, tubes, and packaging solutions prior to the April 2025 merger. Known for lightweight, durable packaging for food, beverage, personal care, and healthcare, Berry brought strong technical expertise and award-winning decoration capabilities. Its focus on high-performance plastics and recyclable designs made it a strategic acquisition for Amcor, strengthening its leadership in consumer and healthcare packaging.

Container and Packaging Market Share Insights

Paper and Paperboard Lead Market Share by Material Type in the Container & Packaging Industry

Paper and paperboard account for 32% of the global container and packaging market, reflecting their role as the industry’s sustainability champion. The dominance of fiber-based formats is not just a function of regulation-driven plastic substitution, but also the ability of paperboard to deliver structural strength, printability, and recyclability at scale. Food and beverage companies are aggressively shifting to coated paperboard trays, cups, and cartons to meet single-use plastic bans in Europe and Asia, with bio-based barrier coatings extending applicability to moist and oily products. While limitations remain in terms of barrier performance, rapid advancements in water-based dispersions and compostable coatings are positioning paperboard as the preferred substrate for brands seeking packaging that aligns with circular economy mandates and resonates with environmentally conscious consumers.

Food and Beverages Dominate Market Share by End-Use Industry in the Container & Packaging Market

The food and beverages sector commands 55% of the container and packaging industry, making it the undisputed demand driver across all materials. Its dominance stems from the dual pressures of ensuring food safety and extending shelf life while minimizing environmental impact. Packaging formats in this segment from rigid PET bottles and aluminum cans to coated paperboard cartons are under relentless scrutiny for their carbon footprint and recyclability. Global food brands are leading investment into lightweighting, recycled content integration, and reusable delivery models, with packaging innovation directly tied to reducing both food waste and packaging waste. The scale of this sector ensures that its regulatory, consumer, and sustainability demands set the pace for material science and production innovation across the entire industry.

United States: Sustainability and Automation Redefine Container and Packaging

The U.S. container and packaging market is being reshaped by consumer demand for recyclable and compostable solutions, particularly in the food and beverage sector. Technological investments in automation-ready secondary packaging lines are helping companies manage labor shortages and SKU proliferation, with some firms reporting an 85% reduction in labor costs while maintaining production rates of 50–60 units per minute. The Department of Energy’s $52 million funding toward cellulose-based films highlights the focus on next-generation sustainable packaging materials.

E-commerce growth is fueling demand for small-parcel packaging solutions, while the pharmaceutical and healthcare sectors are investing in high-barrier materials and automation-ready lines. Corporate initiatives, such as SC Johnson’s refillable packaging systems, reflect the push for eco-friendly and reusable containers. Additionally, state-level Extended Producer Responsibility (EPR) regulations are encouraging manufacturers to rethink supply chains and integrate end-of-life product management into their packaging strategies.

Germany: Circular Economy Leadership and Regulatory-Driven Packaging Innovation

Germany’s container and packaging industry is anchored by a stringent regulatory framework, including the EU Packaging and Packaging Waste Regulation (PPWR 2025), which accelerates demand for eco-friendly, fully recyclable packaging. The country is a global leader in the circular economy, supported by the Packaging Act (Verpackungsgesetz) that enforces producer responsibility across the entire lifecycle of packaging.

Technological advancements such as robotics-enabled systems for short-run printing are helping companies maintain cost efficiency while meeting consumer-driven customization demands. Regulatory updates favoring fiber-based packaging over plastics have boosted the folding carton segment, particularly for pharmaceuticals and high-value products. Demand patterns also vary by sector: thin-wall plastic containers dominate dairy packaging due to cost efficiency, whereas smaller pack sizes are preferred for soft drinks for portion control and convenience.

China: E-Commerce and Carbon-Neutral Policies Fuel Sustainable Packaging

China’s container and packaging market is being propelled by the government’s dual carbon goals, driving the adoption of eco-friendly and reusable materials. Manufacturers are investing heavily in automation, AI, and “5G plus industrial internet” technologies to optimize production and enhance flexible manufacturing capacity. Policies restricting non-degradable plastics by the end of 2025 are further boosting demand for paper-based and sustainable packaging alternatives.

The rapid expansion of domestic e-commerce platforms has increased demand for secure, tamper-proof packaging. Companies like JDL Express have redesigned cardboard boxes to reduce material use by 5–25%, deploying over 860 million optimized boxes, which cut an estimated 12,164 metric tonnes of CO2 emissions. Additionally, intelligent labeling technologies such as QR codes are being increasingly integrated for traceability and anti-counterfeiting in e-commerce logistics.

India: Regulatory Support and Consumer Trends Drive Packaging Innovation

India’s container and packaging industry is benefiting from initiatives such as Make in India and Zero Effect Zero Defect, promoting quality domestic production and sustainable packaging practices. The Production Linked Incentive (PLI) Scheme for food processing, with an outlay of INR 10,900 crore, is enhancing manufacturing capabilities and driving demand for standardized, high-quality packaging solutions.

Rising disposable income and urbanization are shifting consumer preferences toward convenient, single-serve, and packaged products, expanding demand for various container formats. While plastic packaging remains dominant due to affordability and versatility, increasing awareness of sustainability is encouraging manufacturers to explore paper and paperboard alternatives. Regulatory measures like the Plastic Waste Management (Amendment) Rules and Food Safety and Standards (Packaging and Labelling) Regulations are further reinforcing the shift toward eco-friendly packaging solutions across India.

Container and Packaging Market Report Scope

Container and Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1210.8 Billion

|

|

Market Size (2034)

|

$2502.3 Billion

|

|

Market Growth Rate

|

8.4%

|

|

Segments

|

By Material Type (Paper & Paperboard, Rigid Plastics, Flexible Plastics, Metal, Glass, Wood, Bioplastics), By Product Type (Boxes & Cartons, Jars & Containers, Bottles & Cans, Films & Wraps, Bags & Sacks, Closures & Lids, Drums & Barrels, Crates & Pallets), By Packaging Format (Primary Packaging, Secondary Packaging, Tertiary Packaging), By End-Use Industry (Food & Beverages, Pharmaceuticals & Healthcare, Personal Care & Cosmetics, Automotive, Electrical & Electronics, Chemicals, Household Products, Other Industries)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, WestRock Company, International Paper, Ball Corporation, Smurfit Kappa Group, O-I Glass, Inc., DS Smith plc, Mondi Group, Sonoco Products Company, Huhtamaki Oyj, Graphic Packaging International, Crown Holdings, Inc., Sealed Air Corporation, Silgan Holdings Inc., Greif, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Container and Packaging Market Segmentation

By Material Type

- Paper & Paperboard

- Rigid Plastics

- Flexible Plastics

- Metal

- Glass

- Wood

- Bioplastics

By Product Type

- Boxes & Cartons

- Jars & Containers

- Bottles & Cans

- Films & Wraps

- Bags & Sacks

- Closures & Lids

- Drums & Barrels

- Crates & Pallets

By Packaging Format

- Primary Packaging

- Secondary Packaging

- Tertiary Packaging

By End-Use Industry

- Food & Beverages

- Pharmaceuticals & Healthcare

- Personal Care & Cosmetics

- Automotive

- Electrical & Electronics

- Chemicals

- Household Products

- Other Industries

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Container and Packaging Market

- Amcor plc

- WestRock Company

- International Paper

- Ball Corporation

- Smurfit Kappa Group

- O-I Glass, Inc.

- DS Smith plc

- Mondi Group

- Sonoco Products Company

- Huhtamaki Oyj

- Graphic Packaging International

- Crown Holdings, Inc.

- Sealed Air Corporation

- Silgan Holdings Inc.

- Greif, Inc.

* List Not Exhaustive

Methodology

USDAnalytics employed a rigorous and multi-dimensional research methodology to provide a comprehensive analysis of the global Container and Packaging Market. Our approach combined extensive primary research, including interviews with packaging manufacturers, brand owners in food, beverage, personal care, pharmaceuticals, and e-commerce sectors, along with sustainability and supply chain experts, with secondary research from corporate filings, press releases, industry reports, regulatory publications, and trade events. Market sizing, CAGR estimates, and future forecasts were derived from historical consumption trends, emerging sustainability mandates such as Extended Producer Responsibility (EPR) and recycled content regulations, and innovations in reusable, bio-based, and monomaterial packaging. Segmentation covered material type, product type, packaging format, and end-use industry, while qualitative insights analyzed mergers, acquisitions, strategic collaborations, digital watermarking for recycling, and the adoption of high-performance bio-based materials. This methodology ensures USDAnalytics delivers data-driven, forward-looking insights tailored for industry professionals seeking actionable intelligence on market growth, sustainability transitions, and competitive dynamics shaping container and packaging globally.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.