Cool Roof Coatings Market Size, Energy Efficiency Mandates, and High-Reflectivity Technology Adoption

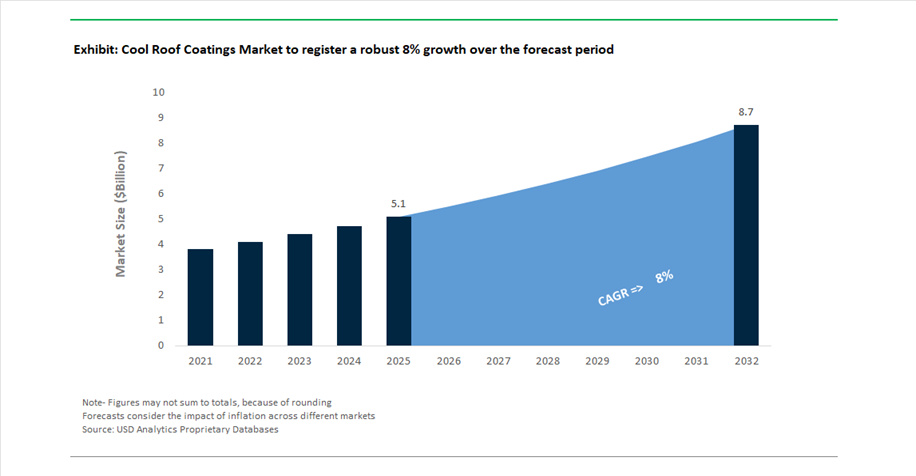

The global cool roof coatings market was valued at $5.1 billion in 2025 and is projected to grow at a CAGR of 8% between 2025 and 2032, reaching $8.7 billion by 2032. This strong growth trajectory is driven by increasing global emphasis on energy-efficient buildings, climate-resilient infrastructure, and urban heat island mitigation, where cool roof coatings play a critical role in reducing solar heat gain, lowering indoor temperatures, and minimizing energy consumption for cooling systems.

Cool roof coatings are engineered with high solar reflectance and thermal emittance properties, enabling buildings to reflect a significant portion of solar radiation. This capability is increasingly important in regions experiencing extreme heat conditions and rising energy costs, particularly across Asia-Pacific, the Middle East, and North America. Governments and regulatory bodies are also promoting cool roofing technologies through building codes and sustainability certifications, accelerating adoption in both new construction and retrofit projects.

Technological advancements are significantly enhancing product performance. Innovations in infrared (IR)-reflective pigments, advanced polymer resins, and nano-engineered materials are enabling coatings to maintain high reflectivity even in darker shades, expanding design flexibility for architects. Additionally, the integration of cool roof coatings with solar photovoltaic (PV) systems is improving overall building energy efficiency by reducing rooftop temperatures and enhancing solar panel performance.

The market is also witnessing a shift toward sustainable and low-carbon manufacturing processes, including waterborne coatings, solvent-free formulations, and renewable energy-based curing technologies. These developments align with global decarbonization goals and the construction sector’s transition toward Net Zero building standards, positioning cool roof coatings as a critical component of modern sustainable infrastructure.

High-Reflectivity Innovation, Sustainable Building Integration, and Strategic Expansion Driving Market Growth

The cool roof coatings market is rapidly evolving through strategic acquisitions, advanced material innovation, and sustainability-driven initiatives. A key development is RPM International’s acquisition of Kalzip GmbH (April 2026), integrating high-performance aluminum roofing and façade systems into its Construction Products Group. This move strengthens RPM’s ability to deliver fully integrated cool roofing and building envelope solutions, particularly in Europe, where energy efficiency standards are stringent.

Sustainable manufacturing technologies are gaining traction across the value chain. AkzoNobel’s IONOMY™ ecosystem (October 2025) enables the transition from traditional gas-fired curing to renewable energy-based and induction curing systems, significantly reducing the carbon footprint of cool roof coating production. By 2026, the initiative has gained industry momentum, supporting the broader push toward low-carbon construction materials.

Material innovation is enhancing both performance and design flexibility. PPG’s advancements in IR-reflective pigments (March 2025) have increased the solar reflectance of darker colors from approximately 5% to nearly 30%, enabling architects to achieve aesthetic goals without compromising energy efficiency. Similarly, NanoTech Materials’ next-generation thermal coatings (2024–2025) utilize proprietary particle technology to deliver superior heat-shielding performance, particularly in retrofitting projects aimed at reducing urban heat island effects.

Product development is increasingly aligned with sustainability certifications and lifecycle performance. GAF’s EnergyGuard™ NH Polyiso line (January 2026) offers Red List-free, high-reflectivity insulation solutions, while Sika Roofing’s award-winning projects (April 2026) highlight the integration of reflective membranes and waterproofing systems in large-scale commercial developments. These solutions extend roof lifespan while improving energy efficiency and resilience in extreme climates.

Design innovation is also influencing adoption. AkzoNobel’s “Rhythm of Blues” color collection (September 2025) demonstrates how solar-reflective technologies can be integrated into visually appealing coatings, ensuring that even deep hues maintain cooling performance. Additionally, Sherwin-Williams’ Emulate™ architectural metal coatings (October 2025) combine natural material aesthetics with high solar reflectance, catering to architects seeking sustainable yet visually distinctive building designs.

Strategic expansion and financial performance further reinforce market momentum. Holcim’s acquisition of Alkern (January 2026) supports its expansion into high-value building solutions, while RPM’s record fiscal 2026 performance, driven by strong demand in construction products, enables continued investment in R&D for energy-efficient coatings and sealants.

Policy-Driven Performance Thresholds Redefining Product Qualification

The cool roof coatings market is no longer driven by voluntary sustainability adoption; it is now governed by quantified, enforceable performance thresholds embedded within federal and state-level energy frameworks. The U.S. Department of Energy’s “Cool Roofs for All” initiative, combined with ENERGY STAR v7.0 enforcement, represents a structural inflection point where only high-performance formulations can access incentive-driven demand pools.

The most consequential shift lies in the transition from initial reflectance metrics to aged performance validation. ENERGY STAR v7.0 mandates a minimum 3-year aged solar reflectance of 0.63 for low-slope roofing systems—a 26% increase over previous standards. This effectively eliminates low-durability acrylic systems that cannot maintain reflectance stability under UV degradation and environmental exposure.

In parallel, financial mechanisms are reinforcing compliance. Coatings achieving aged SRI values of 88 or higher are now eligible for rebate structures averaging $0.30 per square foot, creating a direct economic incentive for high-reflectance technologies such as silicone and fluoropolymer-based systems. This transforms product selection from a cost-based decision into a performance-indexed financial optimization problem for contractors and building owners.

From a system-level perspective, DOE field data demonstrates that compliant coatings can reduce peak cooling demand by 11% to 16%, with some single-story commercial buildings achieving up to 80% of their theoretical energy conservation potential through roof reflectivity alone. This elevates cool roof coatings from an auxiliary upgrade to a primary lever in building energy optimization strategies.

California Title 24 Expanding the Regulatory Envelope for Cool Roof Adoption

California’s Title 24, Part 6 (2025–2026) represents the most aggressive regional enforcement of cool roof standards globally, effectively setting a benchmark that is likely to influence broader North American regulatory trajectories. The 2026 expansion removes historical exemptions, extending compliance requirements to all non-residential additions and major alterations across all climate zones.

The technical thresholds are stringent. Roofing systems must achieve either a minimum aged solar reflectance of 0.70 and thermal emittance of 0.85, or an SRI of at least 82, effectively mandating the use of high-performance coating chemistries. This is not a marginal upgrade—it redefines the baseline specification for commercial roofing materials.

Residential retrofit mandates further deepen market penetration. In high-temperature climate zones, reroofing projects exceeding 50% of roof area must comply with SRI thresholds ranging from 16 (steep slope) to 75 (low slope), ensuring that cool roof adoption is embedded not only in new construction but also in the existing building stock.

At the municipal level, cities such as Los Angeles are pushing even stricter requirements, mandating cool-granule technologies for asphalt shingles, effectively eliminating traditional dark roofing systems from new builds.

The macro-level impact is measurable: projected reductions exceeding 150,000 metric tons of CO₂ annually through decreased grid load. This positions cool roof coatings as a grid-level decarbonization instrument, not merely a building-level efficiency upgrade.

Data Center and Telecom Infrastructure Driving High-Value Demand

The rapid expansion of hyperscale data centers and 5G telecom infrastructure is creating a specialized, high-margin demand segment for advanced cool roof coatings. Unlike conventional commercial buildings, these facilities operate under extreme thermal loads, where even marginal reductions in heat ingress translate into significant operational savings.

High-reflectance silicone and fluoropolymer coatings are demonstrating the ability to reduce rooftop surface temperatures by up to 15°C. This reduction directly lowers conductive heat transfer into server environments, enabling more stable thermal management conditions.

The downstream effect is measurable in Power Usage Effectiveness (PUE) metrics. Data centers deploying high-SRI coatings report 5% to 8% improvements in cooling system efficiency, as chillers operate under reduced thermal stress and more consistent load profiles.

In telecom applications, particularly unconditioned equipment shelters, cool roof coatings can reduce internal temperatures by up to 30%, significantly lowering the risk of thermal-induced equipment failure and extending battery system life.

Durability is a critical differentiator in this segment. Advanced fluoropolymer-based systems now offer 20-year UV resistance guarantees, ensuring long-term performance stability under continuous solar exposure. This aligns with the lifecycle expectations of mission-critical infrastructure assets.

Cold Chain Logistics Creating High-ROI Thermal Barrier Applications

The expansion of global cold chain logistics—driven by e-commerce, pharmaceuticals, and perishable food supply chains—is unlocking a distinct opportunity for cool roof coatings as thermal barrier systems. In refrigerated environments, the economic value of heat reduction is amplified, as every unit of thermal ingress must be counteracted by energy-intensive cooling systems.

High-emittance, high-reflectance coatings with SRI values exceeding 90 are enabling up to 25% reductions in thermal conduction loads through roofing systems during peak daylight hours. For large-scale facilities, such as 100,000 sq. ft. warehouses, this translates into substantial reductions in energy consumption and operating costs.

The financial return profile is particularly compelling. Operators are achieving payback periods of less than 18 months, driven by rising electricity costs and the relatively low capital expenditure required for coating application. This positions cool roof coatings as one of the fastest-return energy efficiency investments within industrial infrastructure.

Beyond energy savings, structural benefits are emerging as a secondary value driver. By reducing thermal cycling, these coatings minimize expansion and contraction stresses on metal roofing systems by up to 50%, extending the lifespan of fasteners and reducing the risk of vapor barrier failure and ice formation.

Advanced formulations are also addressing condensation challenges in high-humidity environments. Anti-condensation coatings maintain high thermal emittance while preventing moisture accumulation, mitigating “roof sweat” issues that can compromise insulation and structural integrity.

White Reflective Cool Roof Coatings Dominate with 58% Share Driven by Maximum Solar Reflectance and Energy Savings

Reflective Technology Analysis: High-SRI Acrylic and Silicone Coatings Lead with Proven ROI and Regulatory Compliance

White reflective coatings account for a dominant 58.0% share of the cool roof coatings market in 2025, driven by their ability to deliver the highest total solar reflectance (0.80–0.90 TSR) and immediate, measurable energy savings. These coatings—primarily 100% acrylic elastomeric and silicone roof coatings—can reduce roof surface temperatures by 40–70°F (22–39°C), translating into 10–30% lower building cooling energy consumption. Their strong adoption is further supported by compliance with global energy efficiency standards such as California Title 24, ENERGY STAR®, and LEED v4.1, along with utility rebate programs covering up to 50% of installation costs. A major growth driver is the liquid-applied roof restoration market, where coatings extend roof life by 10–20 years at significantly lower cost than full replacement. This combination of high-performance thermal management, sustainability compliance, and cost efficiency firmly establishes white coatings as the leading segment in the global cool roof coatings market.

Commercial Sector Leads Cool Roof Coatings Market with 48% Share Driven by Large Roof Areas and ESG Initiatives

End-Use Sector Analysis: Big-Box Retail, Warehouses, and Offices Drive High-Volume Adoption

The commercial sector dominates the cool roof coatings market with a 48.0% share in 2025, driven by the prevalence of large, low-slope roof structures in buildings such as warehouses, retail stores, shopping malls, and office complexes. These structures have a high roof-to-volume ratio, making roofs the primary source of solar heat gain and a critical target for energy efficiency improvements. Cool roof coatings significantly reduce HVAC loads, delivering substantial operational cost savings for building owners. Additionally, increasing pressure from corporate ESG commitments, carbon reduction targets, and sustainability reporting frameworks (GRESB, CDP) is accelerating adoption across commercial real estate portfolios. While white coatings dominate, the emergence of pigmented “cool color” coatings using solar-reflective pigments (SRP) is expanding market potential by allowing architects to meet both aesthetic and energy performance requirements. These factors position the commercial sector as the key growth driver in the global cool roof coatings market.

Cool Roof Coatings Market Competitive Landscape Driven by Energy Efficiency, Reflective Technologies, and Sustainable Roofing Systems

The cool roof coatings market is driven by rising demand for energy-efficient buildings, high-SRI coatings, and sustainable roofing solutions. Key players compete through reflective technologies, liquid-applied membranes, and bio-based formulations, targeting commercial infrastructure, data centers, and urban heat island mitigation initiatives.

PPG Expands Cool Roof Coatings with Heat-Reflective Powder Technologies and Digital ESG Tools

PPG Industries, Inc. is strengthening its leadership in cool roof coatings through a $300 million investment in manufacturing and R&D modernization, supporting rising demand for energy-efficient coatings. Its ENVIROCRON™ Extreme Protection line delivers ultra-durable, heat-reflective performance for metal roofing systems, meeting IEEE and UL standards. PPG is advancing digital integration through its LINQ™ ecosystem, enabling real-time energy-saving simulations and ESG reporting for contractors. The company’s vertical integration in protective coatings supports its strong position in the non-residential segment, which is expected to dominate market demand. Its solutions are increasingly adopted in high-intensity applications such as data centers. PPG’s innovation strategy aligns with global decarbonization and building efficiency goals.

Sika Leads Liquid Applied Membranes with Long-Life Reflective Roofing Solutions

Sika AG maintains a dominant position in liquid-applied membrane (LAM) cool roof systems, with strong growth driven by Sikalastic® and Sarnafil® technologies. The company expanded its footprint in India and Southeast Asia, targeting large-scale infrastructure and logistics projects amid rising regional CAPEX. Its Sarnafil® G 410 SA membrane offers highly reflective surfaces and reduces VOC emissions by 40% through solvent-free application. Sika’s focus on bio-based polyurethane coatings supports its net-zero construction strategy, delivering roof systems with service lives exceeding 30 years. Its high-durability waterproofing solutions enhance lifecycle performance and energy efficiency. The company’s innovation and regional expansion reinforce its leadership in reflective roofing systems.

Sherwin-Williams Strengthens High-SRI Roofing Portfolio with Silicone-Based Solutions

The Sherwin-Williams Company is expanding its cool roof coatings portfolio with strong demand growth in North America’s Sunbelt region. Its Bowling Green facility expansion supports a 60% increase in production capacity for high-reflectivity roofing products. The Uniflex® Silicone44™ coating offers a Solar Reflectance Index above 110, making it a preferred solution for retrofitting aging commercial roofs to meet energy efficiency codes. The company is leveraging its recent acquisitions to integrate architectural aesthetics with industrial-grade reflective technologies. Sherwin-Williams continues to benefit from strong growth in its Performance Coatings segment. Its focus on silicone-based coatings and high-SRI performance strengthens its position in commercial roofing markets.

Dow Advances Acrylic Cool Roof Coatings with Bio-Based Formulations and Data Tools

Dow Inc. is driving innovation in cool roof coatings through advanced acrylic technologies and digital formulation tools. Its RHOPLEX™ EC-series defines industry standards for elastomeric roof coatings, offering durability, adhesion, and long-term reflectivity. The company introduced new adhesion technologies for challenging substrates like EPDM and asphalt, reducing reliance on costly primers. Dow’s Cool Roof Calculator 2.0 enables precise formulation tuning based on regional climate conditions, enhancing product performance. The expansion of its RHOPLEX™ RN-series with bio-based carbon content supports sustainability goals. Its focus on high-performance acrylic coatings positions it strongly in energy-efficient roofing solutions.

Holcim Builds Integrated Cool Roof Systems with Circular Roofing and Global Reach

Holcim is transforming into a building solutions leader, expanding its cool roof portfolio through acquisitions such as Alkern and Firestone Building Products. The company offers integrated roofing systems combining insulation and reflective coatings, enhancing energy efficiency and performance. Its NextGen Growth 2030 strategy focuses on circular roofing, recycling old materials into new high-reflectivity coatings. Holcim’s global presence across 44 markets supports widespread adoption of cool roof technologies in urban infrastructure. Its ECOPlanet and ECOCycle® brands emphasize sustainability and carbon reduction. The company’s integrated approach strengthens its leadership in advanced roofing solutions.

RPM International Expands Restorative Cool Roof Solutions with High-Performance Systems

RPM International Inc., through its Tremco Construction Products Group, is strengthening its position in the cool roof coatings market with strong financial growth and strategic acquisitions. The integration of Kalzip GmbH enhances its building envelope capabilities, combining aluminum roofing with advanced liquid-applied systems like AlphaGuard™. RPM specializes in restorative roofing solutions that extend roof lifespans by 15–20 years while improving energy efficiency. Its MAP 2025 program has significantly improved operational efficiency and profitability. The company’s focus on restoration and maintenance aligns with growing demand for sustainable roofing upgrades. RPM’s integrated systems provide cost-effective and environmentally beneficial solutions for commercial roofing.

India Cool Roof Coatings Market: Mandatory Policies and Heat Mitigation Driving Explosive Growth

India is currently the fastest-expanding market for cool roof coatings, driven by extreme heat conditions and strong regulatory intervention. The Telangana Cool Roof Policy (2023–2028) has set a global benchmark, with Hyderabad linking Occupancy Certificates (OC) to mandatory cool roof compliance for large buildings.

National-level policy is also accelerating adoption. Updates to the Eco Niwas Samhita (ENS) 2024 mandate a minimum solar reflectance (SR) of 0.60 for affordable housing under PMAY-U. City-level initiatives such as the Ahmedabad Heat Action Plan are scaling retrofits, targeting 100,000 homes with white elastomeric coatings, reducing indoor temperatures by up to 5°C. Standardization through IS 16415 ensures long-term performance (≥80% reflectance retention after 3 years). Industrial demand is also rising, with logistics hubs in the Delhi-Mumbai Industrial Corridor (DMIC) deploying polyurethane-based reflective coatings across 15+ million sq. ft. of warehouses. Public-private partnerships have further trained 5,000+ applicators, addressing labor shortages and enabling large-scale deployment.

United States Cool Roof Coatings Market: Tax Incentives and Climate Resilience Driving Adoption

The U.S. market is driven by federal incentives and climate-focused building codes. Under the Inflation Reduction Act (IRA), cool roof coatings now qualify for 30% tax credits, significantly improving ROI for commercial and residential projects.

Regulatory frameworks are raising performance standards. The California Title 24 (2025) requires aged solar reflectance ≥0.65, the highest in North America, while NYC Local Law 97 is pushing adoption to meet carbon caps. Government initiatives such as the DOE “Cooler Communities” grant ($150 million) are scaling deployment across urban areas. Innovation is also strong, with domestic production of waterborne acrylic resins reducing supply chain risks. Additionally, LEED v5 has increased incentives for heat island reduction strategies, further embedding cool roofs into mainstream construction practices.

Australia Cool Roof Coatings Market: Extreme UV Innovation and Water-Harvesting Technology Leading Globally

Australia’s market is defined by cutting-edge innovation tailored to extreme climates. A major breakthrough is the commercialization of nano-engineered coatings that reflect 97% of sunlight and harvest water (≈390 mL/m²/day) through condensation.

Regulatory mandates are also strong. The Western Sydney Heat Resilience Plan requires coatings with SRI ≥78, while industrial solutions like multi-ceramic coatings can block over 96% of solar heat, extending roof lifespans by up to 20 years. Cool roof coatings are also enhancing renewable energy performance, increasing bifacial solar panel output by 8–11%. Insurance incentives—such as premium discounts for coated buildings—are further accelerating adoption, positioning Australia as a leader in multifunctional cool roof technologies.

Saudi Arabia Cool Roof Coatings Market: Vision 2030 and Thermochromic Innovation Driving Demand

Saudi Arabia is rapidly adopting high-performance cool roof coatings under Vision 2030 megaprojects like NEOM and The Line. Regulations now mandate coatings with thermal emittance ≥0.90, ensuring effective heat dissipation in extreme desert climates.

Innovation is focused on durability and efficiency. The expansion of nano-ceramic reflective coatings is improving resistance to sand abrasion, while zero-VOC mandates are pushing the market toward silicone and waterborne systems. Government housing programs (Sakani) require reflective coatings for subsidized homes, and integration with cool pavements (2.5 million m²) is targeting city-wide temperature reductions (~2°C). Industrial applications—such as reflective coatings on oil storage tanks—are also reducing energy losses and emissions.

South Africa Cool Roof Coatings Market: Low-Cost Solutions and Social Impact Driving Adoption

South Africa is leveraging cool roof coatings as a low-cost solution to energy poverty, particularly in informal housing. Programs such as the SANEDI initiative have coated 25,000 m² of homes, while pilot projects under the Million Cool Roofs Challenge 2.0 demonstrated 7–10°C indoor temperature reductions without energy consumption.

Regulatory recognition is also growing. Updates to SANS 10400-XA now formally recognize cool roofs as an energy-efficiency solution. Applications are expanding beyond housing, with grain silos and agribusiness infrastructure adopting reflective coatings to prevent heat-related spoilage. Innovations in bio-based solvents (lignin-derived) further support sustainability, while municipal incentives—such as property tax rebates—are encouraging commercial adoption.

Germany Cool Roof Coatings Market: EU Green Deal and Circular Chemistry Driving Sustainability Leadership

Germany leads Europe in cool roof coating innovation, driven by strict regulatory frameworks and circular economy principles. Under the EU Energy Performance of Buildings Directive (EPBD) 2025, passive cooling solutions—such as reflective coatings—are now mandatory in major renovation projects.

Technological advancements are centered on sustainability. The scale-up of infrared-reflective pigments enables even dark-colored roofs to maintain high reflectivity, while bio-circular resins reduce CO₂ footprints by up to 45%. Germany is also pioneering Digital Product Passports (DPP), ensuring transparency in VOC levels, reflectance, and recyclability. Government subsidies under the BEG program cover up to 20% of installation costs, accelerating adoption. Additionally, coatings are being tailored for hydrogen infrastructure, ensuring durability under thermal stress.

Cool Roof Coatings Market Report Scope

Cool Roof Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.1 Billion

|

|

Market Size (2032)

|

$8.7 Billion

|

|

Market Growth Rate

|

8%

|

|

Segments

|

By Material (Elastomeric Coatings, Acrylic, Silicone, Polyurethane, Bituminous, Specialty Hybrids and Nano-coatings), By Reflective Technology (White Reflective Coatings, Pigmented, Thermal Barrier, Radiative Cooling Coatings), By Technology (Water-borne, Solvent-borne), By Roof Type (Low-Slope Roofs, Steep-Slope Roofs, Specialty Structures), By End-Use Sector (Commercial, Industrial, Residential, Institutional)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sherwin-Williams Company, PPG Industries, Inc., AkzoNobel N.V., RPM International Inc., BASF SE, The Dow Chemical Company, Sika AG, Holcim Ltd., GAF Materials Corporation, Hempel A/S, Henry Company LLC, Kansai Paint Co., Ltd., Nippon Paint Holdings Co., Ltd., 3M Company, Huntsman International LLC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Cool Roof Coatings Market Segmentation

By Material

- Elastomeric Coatings

- Acrylic

- Silicone

- Polyurethane

- Bituminous

- Specialty Hybrids and Nano-coatings

By Reflective Technology

- White Reflective Coatings

- Pigmented

- Thermal Barrier

- Radiative Cooling Coatings

By Technology

- Water-borne

- Solvent-borne

By Roof Type

- Low-Slope Roofs

- Steep-Slope Roofs

- Specialty Structures

By End-Use Sector

- Commercial

- Industrial

- Residential

- Institutional

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Cool Roof Coatings Market

- Sherwin-Williams Company

- PPG Industries, Inc.

- AkzoNobel N.V.

- RPM International Inc.

- BASF SE

- The Dow Chemical Company

- Sika AG

- Holcim Ltd.

- GAF Materials Corporation

- Hempel A/S

- Henry Company LLC

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

- 3M Company

- Huntsman International LLC

*- List not Exhaustive