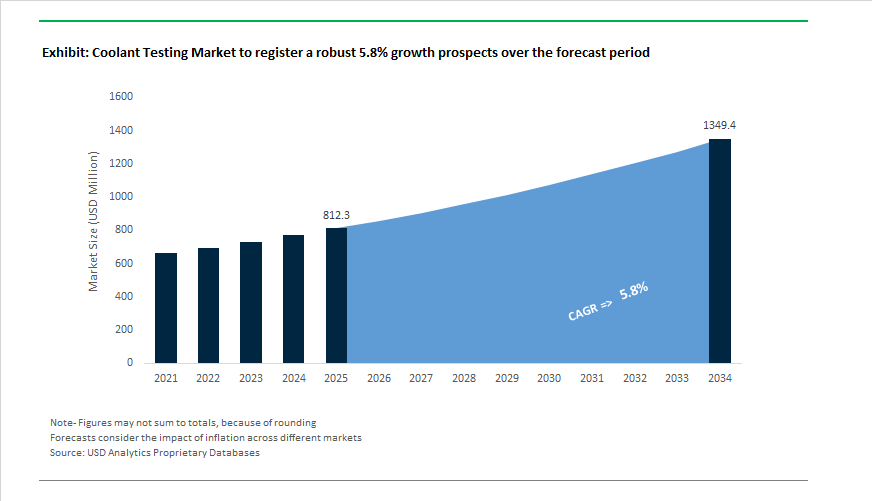

Coolant Testing Market Outlook 2025–2034: $812.3 Million to $1,349.2 Million at 5.8% CAGR Driven by EV Thermal Management and Predictive Fluid Analytics

The global Coolant Testing Market is projected to expand from $812.3 Million in 2025 to $1,349.2 Million by 2034, registering a CAGR of 5.8%. Growth is supported by increasing vehicle parc complexity, the transition toward electric vehicle thermal management systems, stricter environmental compliance requirements, and the adoption of condition-based maintenance models. Coolant testing services now extend beyond traditional pH and freeze-point analysis to include glycol degradation monitoring, cavitation erosion detection, dielectric stability measurement, corrosion inhibition depletion analysis, and renewable content verification. Rising deployment of Organic Acid Technology (OAT) coolants and long-life extended drain interval formulations is further increasing the demand for high-precision analytical testing.

Industry consolidation and facility expansion accelerated in 2024. In May 2024, Lumax Auto Technologies introduced a new aftermarket coolant range in India, supported by technician training programs focused on radiator pressure diagnostics and coolant acidity testing, targeting commercial fleet reliability. In June 2024, Recochem completed the acquisition of KIK Consumer Products' Auto Care business, including the Prestone brand, strengthening North American and UK quality control and laboratory testing infrastructure for advanced OAT coolants. In August 2024, Shell Lubricants India expanded its Taloja testing facility with a new laboratory dedicated to e-thermal fluid evaluation, addressing the growing South Asian EV market’s need for specialized thermal management validation. These investments reflect regional scaling of coolant analysis capacity aligned with evolving powertrain architectures.

Digital transformation and predictive analytics reshaped coolant monitoring in 2025. In October 2025, a coalition of diagnostic firms launched commercially viable Smart Coolant Monitoring systems utilizing IoT-enabled sensors for real-time pH shifts, glycol oxidation tracking, and metal contamination alerts, enabling fleet operators to shift from scheduled to condition-based maintenance. During the same month, LTIMindtree introduced a Fluid Digital Twins framework capable of simulating coolant degradation in heavy-duty engines and predicting system failures up to 500 operating hours in advance. In November 2025, BASF partnered with major European OEMs to conduct high-fidelity field testing of long-life coolants using proprietary analytical techniques to detect early-stage cavitation erosion in high-heat, downsized engines. These developments underscore the integration of AI, digital twins, and sensor-based diagnostics into mainstream coolant lifecycle management.

Regulatory compliance, EV dielectric testing, and sustainability verification emerged as structural growth drivers in 2026. In January 2026, leading laboratories including Intertek and SGS expanded dielectric stability testing services for immersion-cooled EV batteries and data center fluids, focusing on electrical conductivity and moisture ingress detection. During the same month, testing bodies introduced standardized Non-PFAS coolant certification protocols to support eco-label claims for new aliphatic additive formulations. Carbon-14 dating methods were introduced in 2025 to verify renewable bio-based propylene glycol content, strengthening sustainability claim validation. Curtiss-Wright reported in February 2026 increased integration of fluid status sensors into aerospace and defense systems, embedding autonomous coolant monitoring into hardware platforms. Additionally, the validation of 15-year or 350,000-mile extended drain interval coolants in 2025 created demand for advanced inhibitor depletion analysis beyond traditional silicate testing. These converging trends indicate sustained mid-single-digit growth through 2034, anchored in predictive diagnostics, EV thermal stability requirements, extended lifecycle validation, and environmentally compliant coolant formulations.

Coolant Testing Market Trends and Drivers

Real-Time Condition Monitoring Replaces Periodic Laboratory Testing

A structural transition is underway—from historical manual sampling and laboratory-based diagnostics to Industry 4.0 coolant testing systems powered by real-time, in-line sensors. This shift is reshaping value creation across manufacturing, HVAC/R, automotive, energy storage and utilities.

In January 2025, industrial OEMs including Danfoss embedded Condition-Based Monitoring (CBM) sensors directly into variable-speed HVAC/R drives, enabling 24/7 real-time thermal and flow condition analysis. Alongside this, in-line sensing platforms such as Eaton’s WSPS 05 now allow detection of water saturation and coolant contamination at ppm-level sensitivity, extending coolant lifecycles by ~30% and eliminating catastrophic failures caused by waxing, scaling, or pump cavitation.

EV Thermal Systems Trigger a New Global Standardization Wave

Electrification introduces a fundamental challenge: coolants must now provide dielectric safety, preventing electrical arcing inside battery packs and high-voltage drivetrains. Historically, coolant testing was never designed for high-voltage environments—however, from late-2024 to 2025, new regulatory frameworks have rewritten compliance expectations globally.

ASTM D8485 (Dec-2024) establishes a new corrosion test protocol specifically for EV coolants, eliminating legacy water-based assumptions and instead replicating real EV system materials using copper, stainless steel, and aluminum.

China GB 29743.2-2025 (effective Oct-1, 2025) mandates: Initial conductivity ≤100 µS/cm and Post-test conductivity ≤300 µS/cm after 1,064-hour circulation

Because conductivity is now the benchmark safety metric for EV coolant testing, OEMs and laboratories must adopt new dielectric test instrumentation, reshaping global coolant testing infrastructure and procurement cycles.

Certification and Performance Validation for Immersion Cooling in Data Centers

Hyperscale cloud, AI compute, and HPC workloads are forcing a shift toward direct-to-chip (DLC) and immersion cooling, creating a new high-margin need for coolant testing laboratories, certification platforms, and validation-as-a-service business models.

In May 2025, Shell Lubricants obtained the first ever Intel Data Center Certification for immersion cooling fluids—validating compatibility with 4th and 5th Gen Xeon processors. Operators adopting immersion cooling report up to 48% reduction in data center energy consumption, creating board-level ROI arguments tied to ESG, decarbonization and power-cost risk.

Simultaneously, UL Solutions expanded UL 2417 safety certification to include auto-ignition temperature, flash-point testing, and dielectric breakdown metrics, now required for hyperscalers such as NVIDIA (Blackwell platform) and Vertiv, which standardized PG-25 propylene glycol blends and dielectric esters. This has opened a new revenue tier: coolant compliance and certification for multi-megawatt AI factories.

Ultra-High-Purity Analytical Testing for Gen-IV Nuclear Reactors and CSP

Next-generation nuclear reactor cooling systems operate at >700°C and require purity controls at parts-per-billion (ppb)—levels far beyond conventional coolant analysis capabilities. This is catalyzing investment in AI-enabled automated coolant analytics, isotopic measurement platforms, and remote lab-as-a-service models.

Argonne National Laboratory (2024-2025) demonstrated the need for continuous in-situ oxygen and moisture testing for molten-salt coolants to protect nuclear graphite structures.

Liquid metal coolant systems for Gen-IV reactors (e.g., TerraPower Natrium) demand testing that can monitor chloride and sulfur contamination at isotope-level precision (37Cl vs. 35Cl) to minimize neutron absorption and enable 60–80-year lifecycle reactor uptime.

The coolant testing market therefore expands beyond industrial manufacturing into national-infrastructure-critical segments each requiring highly specialized analytical instruments.

Coolant Testing Market Share and Segmentation Insights

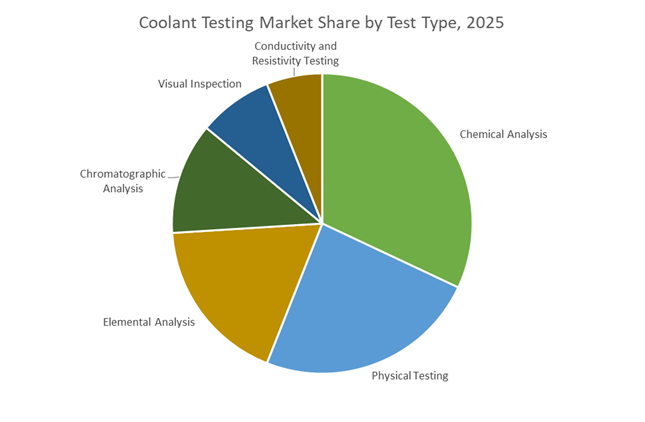

Test Type Distribution: Chemical Analysis Leads Preventive Maintenance Strategies

Chemical analysis holds 32% market share in 2025, forming the backbone of coolant condition monitoring programs. Measurement of pH, reserve alkalinity, glycol concentration, and corrosion inhibitor levels determines whether engine coolants continue to provide freeze protection, boil-over resistance, and anti-corrosion performance. Physical testing represents a significant portion of the market, utilizing refractometers and hydrometers to assess specific gravity, freeze point, and boiling point as rapid field diagnostics. Elemental analysis via ICP spectroscopy plays a critical predictive maintenance role by detecting wear metals such as iron, copper, lead, and aluminum, signaling internal engine component degradation before catastrophic failure. Chromatographic analysis, particularly ion chromatography, supports detailed assessment of organic acid technology additive depletion and contamination. Visual inspection remains universally practiced for initial assessment of discoloration or debris, while conductivity and resistivity testing represent a growing niche for identifying ionic contamination and preventing galvanic corrosion in advanced cooling systems.

Automotive Leads Volume While Heavy-Duty and Industrial Users Drive Predictive Maintenance Adoption

Automotive applications account for 38% of the Coolant Testing Market in 2025, driven by the massive global population of passenger cars and light commercial vehicles undergoing routine service intervals. Regular coolant analysis helps detect pH drift, glycol degradation, and inhibitor depletion, preventing overheating and extending engine lifespan for everyday drivers. Heavy-duty transport represents a substantial secondary segment, where commercial trucks, buses, and construction fleets depend on scheduled coolant testing to avoid costly roadside breakdowns and maximize asset utilization. Industrial machinery follows closely, integrating coolant testing into predictive maintenance programs for compressors, HVAC systems, and manufacturing equipment, where unplanned downtime can translate into significant financial losses. Marine and agricultural equipment form a resilient niche, operating in saltwater, dusty, and high-load environments that accelerate coolant degradation, making corrosion monitoring essential. Aerospace and defense remain specialized, governed by stringent military and aviation standards requiring advanced coolant diagnostics to guarantee mission-critical reliability.

Competitive Landscape of the Coolant Testing Market

The Coolant Testing Market is dominated by global inspection majors and data-driven fluid analysis specialists delivering oil condition monitoring, EV coolant validation, and predictive maintenance analytics. Competition increasingly centers on same-day laboratory turnaround, digital dashboards, dielectric coolant testing, and integration with enterprise asset management systems for high-uptime industrial, automotive, and data center operations.

Bureau Veritas sets the benchmark for same-day coolant diagnostics and fleet-wide OCM visibility

Bureau Veritas leads the coolant testing market through its advanced Oil Condition Monitoring services across industrial and maritime assets. Its comprehensive coolant analysis packages measure more than 25 parameters, including glycol percentage, SCA levels, and metal contaminants. A core differentiator is LOAMS, which provides fleet managers with a unified dashboard for trend analysis and automated maintenance alerts. In 2026, Bureau Veritas strengthened market visibility with a major presence at CONEXPO, highlighting fluid monitoring for renewable energy and data center reliability. Its specialized OCM laboratories deliver same-day results, a critical advantage for high-uptime operations seeking rapid fault detection and proactive equipment protection.

SGS expands digital trust and mining coolant analysis with unmatched global laboratory reach

SGS dominates automotive and heavy machinery coolant testing through its network of more than 2,500 laboratories across 115 countries. In February 2026, SGS acquired MsMin in Chile, strengthening asset reliability and industrial coolant analysis in South America’s mining sector. Strategically, SGS is advancing its Digital Trust journey, targeting CHF 200 million in incremental revenue by 2027 through cybersecurity-enabled testing reports. The company is a major quality assurance partner for coolant manufacturers, validating bio-based and non-conductive EV formulations against ASTM and ISO standards. Its unmatched geographic coverage supports global logistics, maritime fleets, and multinational equipment operators.

Intertek accelerates EV coolant validation with machine-learning condition monitoring

Intertek delivers Total Quality Assurance for both ICE coolants and next-generation dielectric fluids. In early 2026, the company expanded automotive electrification services with specialized protocols for battery thermal management coolants. Its upgraded Condition Monitoring platform applies machine learning to predict coolant degradation using historical metal-wear data, enabling earlier intervention. Intertek’s regulatory expertise is a major draw for OEMs navigating updated REACH and GHS requirements for coolant additives. The company also provides high-purity chemical analysis for long-life OAT and HOAT coolants increasingly specified in heavy-duty commercial vehicles, reinforcing its role in compliance-driven performance validation.

POLARIS integrates coolant analytics directly into enterprise maintenance ecosystems

POLARIS Laboratories operates as a pure-play fluid analysis specialist with a strong focus on data-driven reliability. In 2026, POLARIS launched Practical Oil and Coolant Analysis Training alongside its Zero Tolerance for Downtime webinar series, targeting predictive maintenance skills for critical power operators. The company specializes in diagnostics for data centers and hospitals, where monitoring coolant conductivity and pH prevents catastrophic equipment failure. A key differentiator is direct integration of test results into EAM platforms such as IBM Maximo and SAP, allowing maintenance teams to automate work orders and asset decisions from coolant health data.

ALS scales tribology-driven coolant services for mining and renewable diesel platforms

ALS brings deep tribology expertise to complex coolant systems across mining and heavy industry. The company reported 13.3% underlying revenue growth to USD 1.7 billion in H1 FY26, driven by strong industrial testing demand. ALS delivers custom contract laboratories, including on-site facilities for remote operations, and is executing a disciplined 2026 capital plan to expand high-end analytical capacity across APAC and EMEA. Recent innovation includes specialized test packages for HVO and renewable diesel engines, addressing unique fuel-coolant interactions. This capability positions ALS strongly in emerging low-carbon powertrain maintenance ecosystems.

Eurofins advances PFAS-free coolant certification with high-precision analytical platforms

Eurofins Scientific is rapidly expanding beyond food testing into industrial coolant analysis, supported by projected 2026 revenue of €7.66 billion. The company is prioritizing Green Transformation services, focusing on certification of bio-based and non-toxic coolants for consumer and industrial markets. In 2026, Eurofins announced a global initiative to standardize PFAS-free certification across coolant additive supply chains, aligning with new European environmental mandates. Its core strength lies in analytical precision, leveraging advanced chromatography and mass spectrometry to detect trace impurities that drive corrosion in high-performance engines and electrified mobility platforms.

United States: EV Standardization and AI-Led Laboratory Scale-Up

The United States coolant testing industry is undergoing a structural upgrade driven by electric vehicle thermal management requirements, artificial intelligence integration, and consolidation within testing infrastructure. A major inflection point emerged in late 2025 when ASTM International Committee D15 advanced proposed standards WK76375 and WK83561. These standards are specifically designed to evaluate corrosion protection, material compatibility, and low-conductivity performance of coolants used in EV battery plates and fuel cell stacks. Their progression reflects a broader shift in coolant testing away from internal combustion benchmarks toward electrochemical stability and electrical insulation metrics critical for high-voltage platforms.

Digital transformation is reshaping laboratory operations. In December 2024, POLARIS Laboratories launched Aurora, an AI-powered analysis engine that by 2025 significantly automated coolant data interpretation. The platform has enabled faster detection of liner pitting, scale formation, and additive depletion for heavy-duty fleet operators, improving predictive maintenance outcomes. Capacity expansion is reinforcing this capability. POLARIS completed a major expansion of its Houston facility in early 2024, increasing throughput for specialized coolant analysis to serve marine, petrochemical, and heavy industrial customers along the Gulf Coast through 2026. At the frontier of extreme-environment testing, Idaho National Laboratory achieved a milestone in 2025 with its Primary Coolant Apparatus Test, validating liquid metal coolant performance for the MARVEL microreactor. This work sets new benchmarks for coolant testing under high-temperature, non-conventional operating conditions.

Industry consolidation is further shaping service capabilities. In July 2025, SGS announced a definitive agreement to acquire Applied Technical Services, strengthening its North American footprint in automotive and aerospace thermal system testing. Knowledge exchange platforms are also accelerating best practices. The 2025 Reliability Summit in Indianapolis highlighted the transition to Extended Life Coolants, with laboratories showcasing new protocols for detecting organic acid depletion in hybrid cooling systems. Collectively, these developments position the U.S. as a reference market for advanced, data-driven coolant testing aligned with EV and next-generation energy systems.

Germany: Regulatory Rigor and Secure Data Handling for OEM-Centric Testing

Germany’s coolant testing ecosystem is being reshaped by stringent regulatory alignment, data security requirements, and sustainability-led testing frameworks. In December 2025, Intertek achieved TISAX Assessment Level 3 certification in Germany, enabling the secure handling of sensitive coolant performance data for major automotive OEMs. This accreditation is increasingly critical as coolant formulations become proprietary and tightly integrated with vehicle platform design, especially for EV thermal management systems.

Regulatory developments at the European level are driving deeper analytical scrutiny. Following Commission Implementing Regulation (EU) 2025/58, German laboratories intensified purity testing for monoethylene glycol and additive packages sourced from outside the bloc, responding to heightened anti-dumping enforcement. At the same time, laboratories accelerated accreditation toward compliance with the Machinery Regulation (EU) 2023/1230, which mandates rigorous fluid safety and thermal stability testing for industrial cooling systems used in high-precision manufacturing. Sustainability considerations are reinforcing Germany’s leadership position. SGS was ranked the top sustainability-focused TIC company in 2025 by TIME and Statista, driven in part by its IMPACT NOW platform that standardizes testing protocols for biodegradable and eco-friendly coolants. These dynamics collectively elevate Germany as a compliance-intensive, OEM-centric hub for advanced coolant testing in Europe.

China: Battery Thermal Management and Fleet Reliability Mandates

China’s coolant testing industry is increasingly aligned with electric mobility scale-up and commercial fleet reliability objectives. Throughout 2025, the China Rubber Industry Association coordinated with European counterparts to harmonize testing protocols for dielectric coolants used in high-capacity EV batteries. This alignment reflects the growing importance of cross-border standards convergence as Chinese battery platforms and vehicles expand into global markets that require validated thermal and electrical safety performance.

Commercial transport regulations are reinforcing routine testing demand. Regulatory reviews in 2025 targeting heavy-duty vehicle systems increased the requirement for periodic coolant analysis in buses and logistics fleets. The objective is to minimize roadside breakdowns, improve thermal efficiency, and extend service intervals under high-load operating conditions. As a result, demand is rising for standardized coolant testing services that can assess additive depletion, corrosion risk, and heat transfer efficiency in large fleet environments. These trends position China’s coolant testing market at the intersection of EV battery innovation and large-scale commercial vehicle reliability management.

India: Power Infrastructure Focus and Localization of ASTM-Grade Testing

India’s coolant testing industry is expanding in response to power generation needs and the localization of EV manufacturing. At the 2025 India Power Stations O&M Conference, Intertek and other industry leaders presented new testing protocols for large-scale industrial coolants used in power plant heat exchangers. These protocols focus on preventing mineral scaling, controlling corrosion, and optimizing thermal transfer efficiency, addressing critical reliability challenges in India’s growing power infrastructure.

Localization is emerging as a strategic priority. During 2025, there was a marked shift toward establishing ASTM-grade coolant testing laboratories in industrial hubs such as Pune and Chennai. This expansion supports the Make in India initiative by enabling domestic EV component manufacturers to access compliant coolant testing services without reliance on overseas laboratories. The result is shorter validation cycles, improved regulatory alignment, and stronger integration between testing services and localized manufacturing ecosystems.

Comparative Snapshot: Country-Level Direction in the Coolant Testing Industry

Coolant Testing Market County Level Snapshot

|

Country

|

Primary Regulatory or Market Driver

|

Key Application Focus

|

Direction of Coolant Testing Evolution

|

|

United States

|

EV standards and AI-driven diagnostics

|

EV batteries, fleets, advanced reactors

|

Data-automated, extreme-condition testing

|

|

Germany

|

EU regulation and OEM data security

|

Automotive and industrial systems

|

High-purity, secure, sustainability-aligned testing

|

|

China

|

EV battery scale-up and fleet mandates

|

Battery thermal management, logistics

|

Harmonized standards and periodic analysis

|

|

India

|

Power O&M and manufacturing localization

|

Power plants and EV components

|

ASTM-grade, localized testing capacity

|

Coolant Testing Market Report Scope

Coolant Testing Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$812.3 Million

|

|

Market Size (2034)

|

$1349.2 Million

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Test Type (Visual Inspection, Physical Testing, Chemical Analysis, Elemental Analysis, Conductivity and Resistivity Testing, Chromatographic Analysis), By Coolant Technology (Inorganic Additive Technology, Organic Additive Technology, Hybrid Organic Additive Technology, Nitrite-Free and Phosphate-Free Coolants, Dielectric and Immersion Coolants), By Application (Automotive, Heavy-Duty Transport, Industrial Machinery, Aerospace and Defense, Marine and Agricultural Equipment), By Service Provider (In-House Laboratory Testing, Third-Party Testing Services, On-Site and Portable Testing)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

SGS S.A., Bureau Veritas S.A., Intertek Group plc, POLARIS Laboratories LLC, Eurofins Scientific SE, ALS Limited, TÜV SÜD AG, TÜV Rheinland AG, AMSOIL Inc., Valvoline Global Operations, Exxon Mobil Corporation, Chevron Corporation, Castrol Limited, FUCHS SE, Element Materials Technology Group Limited, Applus Services S.A.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Coolant Testing Market Segmentation

By Test Type

- Visual Inspection

- Physical Testing

- Chemical Analysis

- Elemental Analysis

- Conductivity and Resistivity Testing

- Chromatographic Analysis

By Coolant Technology

- Inorganic Additive Technology

- Organic Additive Technology

- Hybrid Organic Additive Technology

- Nitrite-Free and Phosphate-Free Coolants

- Dielectric and Immersion Coolants

By Application

- Automotive

- Heavy-Duty Transport

- Industrial Machinery

- Aerospace and Defense

- Marine and Agricultural Equipment

By Service Provider

- In-House Laboratory Testing

- Third-Party Testing Services

- On-Site and Portable Testing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Coolant Testing Industry

- SGS S.A.

- Bureau Veritas S.A.

- Intertek Group plc

- POLARIS Laboratories LLC

- Eurofins Scientific SE

- ALS Limited

- TÜV SÜD AG

- TÜV Rheinland AG

- AMSOIL Inc.

- Valvoline Global Operations

- Exxon Mobil Corporation

- Chevron Corporation

- Castrol Limited

- FUCHS SE

- Element Materials Technology Group Limited

- Applus Services S.A.

*- List not Exhaustive