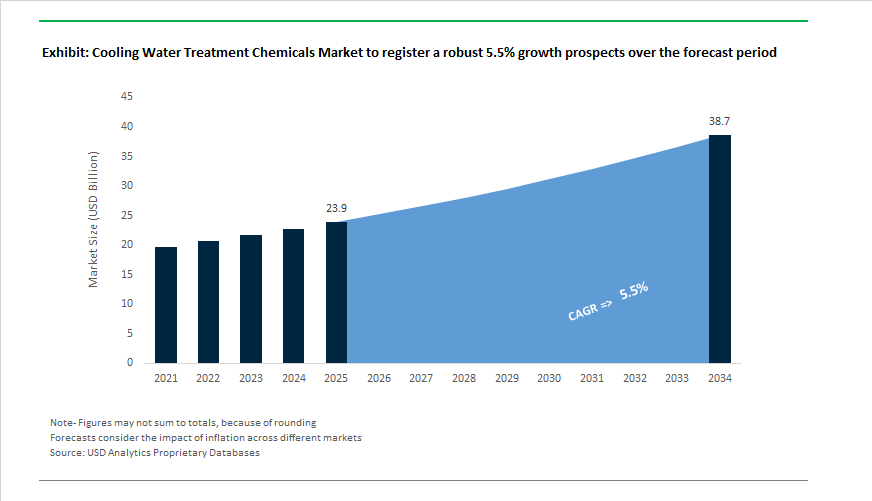

Cooling Water Treatment Chemicals Market Outlook 2025–2034: $23.9 Billion to $38.7 Billion at 5.5% CAGR Driven by Data Center Cooling, Industrial ZLD Mandates, and Digital Water Platforms

The global Cooling Water Treatment Chemicals Market is projected to expand from $23.9 billion in 2025 to $38.7 billion by 2034, registering a CAGR of 5.5%. Growth is being driven by rising industrialization, expansion of hyperscale data centers, zero-liquid-discharge regulations, and increasing adoption of automated water monitoring platforms. Cooling water treatment programs rely on corrosion inhibitors, scale inhibitors, dispersants, biocides, and pH control agents to maintain heat transfer efficiency and prevent fouling in power plants, chemical processing units, metal manufacturing facilities, refineries, and HVAC systems. As cooling loops become more complex and regulatory scrutiny intensifies, demand for integrated chemical-plus-digital service models is accelerating.

Strategic consolidation reshaped competitive positioning in 2024–2025. In February 2024, Kemira divested its Oil & Gas portfolio to focus capital on Water Solutions and Pulp & Paper, strengthening its commitment to industrial cooling water chemistries. In December 2024, Buckman opened a $10 million R&D pilot plant in Memphis to accelerate development of smart chemicals and digital monitoring tools for industrial water systems. In May 2025, Veolia achieved full ownership of Water Technologies & Solutions by acquiring CDPQ’s 30% stake, targeting €90 million in cost synergies in industrial cooling and energy markets. In June 2025, Solenis announced the acquisition of NCH Corporation, expanding into middle-market and light-industrial cooling segments. Kemira further strengthened its North American presence in September 2025 by acquiring Water Engineering for $150 million. In July 2025, Pritzker Private Capital completed the acquisition of Buckman, aiming to accelerate R&D and expand digital water management capabilities.

Digitalization and regulatory mandates are reshaping cooling water chemistry deployment. In April 2024, Nalco Water introduced its Premium Cooling Water Program focused on eco-efficient chemistry to improve heat transfer while reducing environmental footprint in power and chemical plants. China’s GB 50050-2024 standard, effective during 2024–2025, mandated real-time monitoring of conductivity and pH in high-volume cooling loops, accelerating adoption of automated dosing and monitoring systems across Jiangsu and Guangdong. In May 2025, Ecolab launched a specialized version of 3D TRASAR™ tailored for direct-to-chip liquid cooling in data centers, providing real-time coolant health analytics to support AI server thermal management while reducing water usage. In August 2025, Buckman and Atul formed a joint venture in India to address tightening zero-liquid-discharge regulations and rising demand for advanced cooling water chemistries in South Asia.

Raw material volatility and pricing adjustments influenced market dynamics through 2025–2026. BASF reported significant margin pressure in 2024–2025 following acrylic acid supply disruptions, impacting dispersant costs and prompting formulators to shift toward lower-phosphorus blends and bio-based starch polymer alternatives. In January 2026, major suppliers including Buckman implemented 5–12% price increases across cooling water product lines effective February 1, reflecting inflation in labor, logistics, and compliance costs. This trend toward value-based pricing is increasingly tied to bundled digital monitoring services rather than standalone chemical sales. These structural shifts in consolidation, regulatory compliance, smart monitoring integration, and feedstock optimization position the cooling water treatment chemicals market for steady mid-single-digit expansion through 2034.

Cooling Water Treatment Chemicals Market Trends and Drivers

AI-Optimized Cooling Water Treatment Drives Shift from Manual Testing to Automated Control

A foundational change is underway as chemical treatment becomes integrated with real-time IoT monitoring platforms—reducing operational risk, water waste, and chemical overconsumption.

In October 2025, Ecolab expanded 3D TRASAR™ Technology for Direct-to-Chip Liquid Cooling in Southeast Asia—a milestone signaling that cooling water treatment is converging with digital facility management. Using live monitoring of glycol concentration, pH, conductivity, and thermal stability, AI-based dosing ensures chemistry is continuously optimized rather than adjusted reactively.

With cooling systems accounting for up to 40% of a data center's total energy and water footprint, digital treatment systems are becoming a P&L lever, enabling:

- 10–20% chemical cost reduction via anti-overfeed algorithms

- Lower OPEX tied to water bills and blowdown penalties

- Reduced downtime risk, particularly in mission-critical cooling systems

A parallel development is the commercialization of smart-tagged polymers like Italmatch Chemicals’ Lumiclene, where embedded molecular markers allow operators to validate active polymer levels online—eliminating old practices of overdosing to play safe, unlocking scalable, compliant water savings across industrial campuses.

Global Regulatory Pressures Drive Transition Toward Stabilized Bromine & PAA Biocides

As environmental scrutiny intensifies, legacy chlorine systems are losing relevance in large-scale utilities, refineries, and power plants.

Key catalysts include:

- U.S. EPA 40 CFR 423.15 – Restricting residual chlorine discharge

- Rising litigation exposure and ESG penalties tied to halogenated byproducts

- Emergence of Legionella as a board-level safety risk

This regulatory shift is accelerating adoption of Peracetic Acid (PAA) as a biodegradable alternative—spotlighted in September 2025 by chemical distributor data confirming rapid PAA uptake due to its cleaner kill pathway.

Further, stabilized bromine is gaining share due to strong performance in alkaline programs enabling towers to run at higher Cycles of Concentration, saving 5 million gallons of water per facility annually.

High-Density Data Center Cooling Chemicals Emerge as a Premium Growth Segment

The hyperscale shift—driven by AI processing, 5G, and GPU-intensive loads—is reshaping cooling chemistry needs.

Rack densities are forecast to rise from 10 kW → nearly 20 kW per rack by late 2025, pushing demand for closed-loop glycol inhibitors, multi-metal corrosion protection, and low-foaming treatment chemistries capable of stabilizing copper cold plates and aluminum microchannel heat exchangers.

ChemTreat’s CTSolutions® D2C launch in August 2025 exemplifies commercial momentum: engineered specifically for Direct-to-Chip (D2C) cooling, where even chemical imbalance can trigger CPU throttling or full server shutdown.

The emerging competitive advantage for suppliers lies in delivering chemicals + AI monitoring platforms + compliance analytics, creating subscription revenue models instead of commodity-based chemical margins.

Wastewater Reuse and High-Recovery Cooling Open a Multi-Billion Circular Water Market

Water scarcity and regulatory mandates are reframing cooling towers from heat rejection assets into water recycling ecosystems.

Growth drivers include:

- IDE Tech’s MAXH2O Desalter, achieving up to 93.5% water recovery from cooling tower blowdown

- Industrial mandates in India, requiring use of secondary-treated municipal wastewater for industrial cooling—reducing water procurement costs by ~40%

Chemical suppliers face demand from Dispersants and antiscalants capable of preventing precipitation under supersaturation, Advanced biocides that neutralize high-organic-load effluent streams, Silica inhibitors supporting RO reject water reuse, and others.

Cooling Water Treatment Chemicals Market Share and Segmentation Insights

Chemical Type Segmentation: Corrosion Inhibitors Lead as Scale and Biocontrol Programs Intensify

Corrosion inhibitors account for 30% of cooling water treatment chemical demand in 2025, underscoring their critical role in protecting heat exchangers, cooling towers, condensers, and pipelines from rust and material degradation. Chemistries such as azoles, phosphonates, and molybdates are widely deployed, as the high capital cost of replacing industrial cooling assets makes corrosion prevention a top operational priority. Scale inhibitors, including polyacrylates and phosphonates, represent a substantial share, preventing calcium carbonate and calcium sulfate deposition that can severely impair heat transfer efficiency and increase energy consumption. Biocides also command significant demand, driven by regulatory pressure to control Legionella, algae, and biofilm formation using oxidizing agents like chlorine and bromine alongside non-oxidizing alternatives such as glutaraldehyde and isothiazolinones. pH adjusters, dispersants, antifoaming agents, and chelating agents complement core programs by maintaining chemical balance, suspending solids, controlling foam, and binding problematic metal ions.

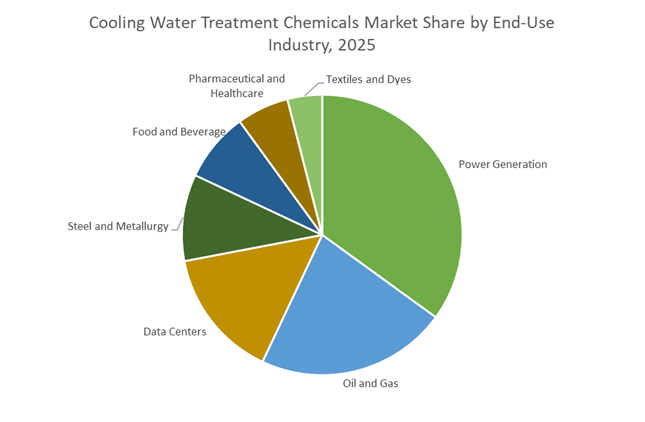

End-Use Industry Distribution: Power Generation Anchors Demand While Data Centers Accelerate Growth

Power generation leads cooling water treatment chemical consumption with 35% market share, reflecting the massive cooling volumes required in nuclear, thermal, and combined-cycle plants where condenser fouling or corrosion can trigger costly shutdowns. Oil and gas facilities represent a major secondary segment, operating complex high-temperature cooling networks in refineries and petrochemical plants that demand robust anti-corrosion and anti-scaling programs. Data centers are the fastest-growing end-use market, fueled by cloud computing and AI expansion, with efficient cooling tower treatment now mission-critical to prevent downtime and service disruption. Steel and metallurgy rely on specialized formulations to manage extreme scaling and corrosion in furnaces and rolling mills. Food and beverage producers prioritize food-grade, compliant chemistries to ensure hygiene, while pharmaceutical and healthcare facilities require validated, low-toxicity solutions for HVAC and process cooling. Textiles and dyes complete the landscape, increasingly adopting water-efficient treatment strategies amid conservation pressures.

Competitive Landscape of the Cooling Water Treatment Chemicals Market

The Cooling Water Treatment Chemicals Market is led by integrated water technology majors and specialty chemical innovators advancing digital monitoring, bio-based inhibitors, and circular water reuse. Competition centers on real-time cooling analytics, non-phosphorus formulations, PFAS mitigation, and sustainability-driven performance for data centers, heavy industry, and semiconductor manufacturing.

Ecolab sets the benchmark with 3D TRASAR platforms for AI data center cooling optimization

Ecolab, through Nalco Water, dominates high-tech and industrial cooling via its 3D TRASAR™ ecosystem. In May 2025, the company launched 3D TRASAR™ for Direct-to-Chip Liquid Cooling, enabling real-time monitoring of coolant health, pH, and flow rates for AI-driven data centers. Strategic momentum accelerated with the November 2025 acquisition of Ovivo’s Electronics Ultrapure Water business, strengthening Ecolab’s semiconductor cooling footprint. Its Water Quality IQ™ dashboard integrates lab diagnostics with onsite sensors, delivering prescriptive actions that cut water use by up to 20%. Under its Water Positive mission, Ecolab partnered with CDP in early 2026 to redefine operational water performance benchmarks globally.

Solenis expands middle-market dominance with ClearPoint biofilm control and onsite service scale

Solenis has emerged as a powerhouse in heavy industrial and middle-market cooling following its June 2025 merger with NCH Corporation, significantly expanding light-water service coverage. The company deploys ClearPoint™ biofilm detection and Biosperse™ biocides as industry standards for microbial control in large cooling towers. By 2026, Solenis operates 78 manufacturing facilities worldwide, executing a local-for-local strategy to reduce logistics risk. Its core strength lies in non-phosphorus corrosion and scale inhibitors, helping plants comply with tightening 2026 discharge regulations. Solenis’ specialized chemical delivery model supports rapid deployment and consistent performance across manufacturing, power generation, and processing industries.

Kurita advances CSV chemistry with bio-based inhibitors and online scale removal technologies

Kurita leads with its Creating Shared Value model, prioritizing energy-efficient cooling solutions. In late 2025, Kurita partnered with Solugen to introduce Kurita TowerNG, a bio-based scale and corrosion inhibitor line produced through enzymatic fermentation. Its patented DReeM Polymer™ removes existing scale while systems remain online, dramatically improving heat transfer without downtime. Under the PSV-27 Plan, Kurita targets over 150 CSV business models by 2027 focused on greenhouse gas reduction. The company also formed a Sustainability Corporate Strategy Division in April 2025, accelerating global adoption of Water Stewardship practices across industrial cooling operations.

Kemira pivots to full-service industrial water with AI-driven PFAS removal innovation

Kemira is steering the Green Transition in cooling water treatment by combining renewable raw materials with service-led delivery. In 2025, Kemira acquired Water Engineering, Inc., shifting from chemical supply to end-to-end industrial water management. A 2026 partnership with CuspAI applies advanced artificial intelligence to develop materials targeting PFAS and micropollutant removal from cooling cycles. Kemira aims to double water-related revenue by 2030 through Urban Water and circular economy expansion. As of early 2026, 55% of its raw materials are renewable or recycled, positioning Kemira at the forefront of petrochemical displacement in industrial cooling formulations.

Veolia integrates Hydrex chemistry with circular wastewater-to-cooling systems

Veolia combines Hydrex® cooling chemicals with a vast global operations and maintenance footprint. In May 2025, Veolia acquired CDPQ’s remaining stake in Water Technologies and Solutions, securing full ownership to accelerate industrial growth. Its Hydrex® 7000 series integrates chemicals with Hubgrade digital supervision for remote monitoring and leak detection. Veolia has also scaled OSG Hydrex salt electrolysis, enabling onsite, chemical-free biocide generation for cooling towers. A key differentiator is circularity, with wastewater-to-cooling systems allowing refineries and plants to reuse treated effluent as primary cooling water, significantly reducing freshwater dependence.

BASF enables green cooling formulations through dispersions scale-up and low-PCF chemistry

BASF acts as a foundational enabler in cooling water treatment, supplying high-purity intermediates and advanced dispersions for scale and corrosion inhibitor formulations. In February 2026, BASF commissioned a new dispersions line in Mangalore, India, addressing rising demand for industrial water treatment components. Guided by its Winning Ways strategy, BASF is positioning itself as a Green Transformation partner through low Product Carbon Footprint chemicals. The Innovation Campus Mumbai supports co-development of sustainable formulations tailored to regional water stress. BASF also committed to establishing Sustainable Water Management at all production sites in water-stressed regions by 2030, setting a benchmark for customers worldwide.

United States: Digital Cooling Systems and PFAS-Free Reformulation Accelerate Adoption

The United States cooling water treatment chemicals industry is being reshaped by the convergence of electric mobility, data center cooling demand, and tightening discharge regulations. In late 2025, ASTM International Committee D15 advanced specialized standards for low-conductivity thermal fluids, enabling rigorous evaluation of chemical additives used in dielectric immersion cooling for high-capacity EV batteries and hyperscale data centers. This standardization is accelerating the qualification of corrosion inhibitors, dispersants, and biocides designed for electrically sensitive cooling environments. Commercial innovation has followed quickly. Italmatch Chemicals expanded its Lumiclene portfolio in the U.S. during 2025, introducing smart-tagged polymers that allow real-time fluorometric tracking of active polymer concentration. Industrial operators report measurable reductions in overdosing, improving system efficiency while lowering total chemical consumption in open-recirculating cooling systems.

Technology adoption is extending into advanced cooling architectures. ChemTreat, a Danaher company, launched tailored chemical programs in 2025 for direct-to-chip liquid cooling, a rapidly growing application in AI server infrastructure. These formulations are engineered to prevent biofouling and localized corrosion in ultra-fine heat exchanger channels where traditional treatments fail. Regulatory pressure is reinforcing reformulation trends. Driven by upcoming updates to the Clean Water Act for 2026, U.S. facilities are transitioning toward PFAS-free and non-phosphorus antiscalants, with FlexPro-based technologies emerging as compliant alternatives for sensitive watersheds. Predictive analytics is also becoming integral. POLARIS Laboratories integrated its Aurora AI engine into coolant diagnostics in 2025, enabling early detection of liner pitting and scale formation months before mechanical failure. Infrastructure consolidation is strengthening validation capacity, following SGS acquiring Applied Technical Services in July 2025 to expand third-party verification for aerospace and defense cooling chemistries.

China: Mandatory Water Reuse and Digital Dosing Redefine Cooling Chemistry Demand

China’s cooling water treatment chemicals market is undergoing a structural shift driven by mandatory water reuse targets, industrial digitalization, and urban resilience programs. Under the 2025 roadmap issued by the National Development and Reform Commission, water-scarce cities are now required to achieve a 25% recycled water utilization rate. This mandate is forcing industrial facilities to operate cooling towers with high-conductivity gray water feedstocks, sharply increasing demand for robust dispersants and corrosion inhibitors capable of maintaining performance under elevated dissolved solids.

Process water recovery has become a parallel priority. In 2025, IDE Technologies deployed its MAXH2O Desalter in major petrochemical hubs, combining chemical precipitation and reverse osmosis to recover nearly all cooling tower blowdown. Regulatory pressure is extending into solids management. China’s 2025 sludge treatment implementation plan mandates a 95% treatment rate in county-level cities, stimulating adoption of high-efficiency flocculants and dewatering agents within wastewater-to-cooling-water loops. Urban infrastructure programs are opening additional applications. With Sponge City projects rolled out across dozens of municipalities by early 2026, demand is rising for bio-based algaecides and stabilizers used in large-scale urban cooling and flood-control water features. Supporting these transitions, the Ministry of Industry and Information Technology allocated substantial funding in 2025 to industrial digitalization, prioritizing IoT-enabled dosing pumps across the Yangtze River Delta manufacturing cluster.

India: ZLD Expansion and Desalination-Linked Cooling Systems Drive Chemical Innovation

India’s cooling water treatment chemicals industry is expanding rapidly in response to industrial water stress, renewable fuel programs, and stricter discharge norms. Under the PM JI-VAN Yojana, the government incentivized domestic production of scale and corrosion inhibitors in 2025 to support second-generation ethanol biorefineries, where cooling systems must handle complex organic loads. Zero Liquid Discharge adoption is reinforcing this demand. In late 2025, Thermax Limited reported growth in its water and waste management division, driven by turnkey ZLD projects for power plants that require high-performance anti-foulants and dispersants to maintain thermal efficiency.

Coastal industrialization is creating new synergies. VA Tech WABAG secured contracts in 2025 for integrated desalination and cooling water circuits using Pulse Flow RO technology, minimizing chemical scaling in high-salinity environments. Municipal-industrial water reuse is also accelerating. In early 2026, the Koyambedu Wastewater Treatment Plant in Chennai expanded tertiary-treated water supply to nearby industries, triggering increased use of oxidizing biocides to control microbial growth in recycled effluent cooling systems.

Germany: Low-Nutrient Treatments and Bio-Based Alternatives Under EU Water Policy

Germany’s cooling water treatment chemicals landscape is defined by regulatory rigor and rapid adoption of bio-based alternatives. Effective March 2025, amendments to EU water policy mandated continuous monitoring of thermal conditions and nutrient discharge in industrial effluents, compelling chemical producers and end users to shift toward low-nitrogen and low-phosphorus cooling treatments. Compliance requirements under updated Industrial Emissions Directive provisions now extend to advanced monitoring of microplastics and pharmaceutical residues in cooling blowdown, elevating analytical complexity and favoring high-purity, precisely dosed chemical programs.

Innovation is increasingly supported by public research funding. In 2025, Horizon Europe backed German-led projects focused on biomimetic membranes and corrosion inhibitors derived from agricultural waste, designed to replace conventional phosphonate-based chemistries. These initiatives align with Germany’s broader circular economy strategy and reduce dependency on persistent synthetic additives. As a result, the German market is becoming a proving ground for environmentally advanced cooling water treatment chemicals that meet both industrial performance and stringent ecological criteria.

Comparative Snapshot: Country-Level Direction in Cooling Water Treatment Chemicals

Cooling Water Treatment Chemicals Market County Level Snapshot

|

Country

|

Primary Regulatory or Market Driver

|

Key Application Focus

|

Direction of Chemical Innovation

|

|

United States

|

EV cooling standards and PFAS regulation

|

Data centers, EV batteries, defense

|

Smart-tagged, PFAS-free, AI-monitored treatments

|

|

China

|

Mandatory water reuse and digitalization

|

Industrial cooling and urban systems

|

High-conductivity tolerant, IoT-dosed chemistries

|

|

India

|

ZLD mandates and desalination growth

|

Power plants and biorefineries

|

Salinity-resistant, reuse-optimized chemicals

|

|

Germany

|

EU water policy and circular economy

|

Industrial manufacturing

|

Low-nutrient, bio-based cooling treatments

|

Cooling Water Treatment Chemicals Market Report Scope

Cooling Water Treatment Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$23.9 Billion

|

|

Market Size (2034)

|

$38.7 Billion

|

|

Market Growth Rate

|

5.5%

|

|

Segments

|

By Chemical Type (Corrosion Inhibitors, Scale Inhibitors, Biocides, Dispersants and Antifoaming Agents, pH Adjusters and Softeners, Chelating Agents), By System Type (Open Recirculating Systems, Closed Loop Systems, Once-Through Cooling Systems), By Technology (Smart-Tagged Polymer Systems, Low-Phosphorus Formulations, Bio-Based and Green Chemistry Solutions, Automated Dosing Systems), By End-Use Industry (Power Generation, Oil and Gas, Food and Beverage, Steel and Metallurgy, Data Centers, Textiles and Dyes, Pharmaceutical and Healthcare)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ecolab Inc., Solenis LLC, Veolia Environnement S.A., Kurita Water Industries Ltd., ChemTreat Inc., Thermax Limited, Italmatch Chemicals S.p.A., Kemira Oyj, Buckman Laboratories International Inc., BASF SE, VA Tech Wabag Limited, BWA Water Additives Ltd., DuPont de Nemours Inc., Ion Exchange India Limited, Nouryon Chemicals Holding B.V.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Cooling Water Treatment Chemicals Market Segmentation

By Chemical Type

- Corrosion Inhibitors

- Scale Inhibitors

- Biocides

- Dispersants and Antifoaming Agents

- pH Adjusters and Softeners

- Chelating Agents

By System Type

- Open Recirculating Systems

- Closed Loop Systems

- Once-Through Cooling Systems

By Technology

- Smart-Tagged Polymer Systems

- Low-Phosphorus Formulations

- Bio-Based and Green Chemistry Solutions

- Automated Dosing Systems

By End-Use Industry

- Power Generation

- Oil and Gas

- Food and Beverage

- Steel and Metallurgy

- Data Centers

- Textiles and Dyes

- Pharmaceutical and Healthcare

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Cooling Water Treatment Chemicals Industry

- Ecolab Inc.

- Solenis LLC

- Veolia Environnement S.A.

- Kurita Water Industries Ltd.

- ChemTreat Inc.

- Thermax Limited

- Italmatch Chemicals S.p.A.

- Kemira Oyj

- Buckman Laboratories International Inc.

- BASF SE

- VA Tech Wabag Limited

- BWA Water Additives Ltd.

- DuPont de Nemours Inc.

- Ion Exchange India Limited

- Nouryon Chemicals Holding B.V.

*- List not Exhaustive