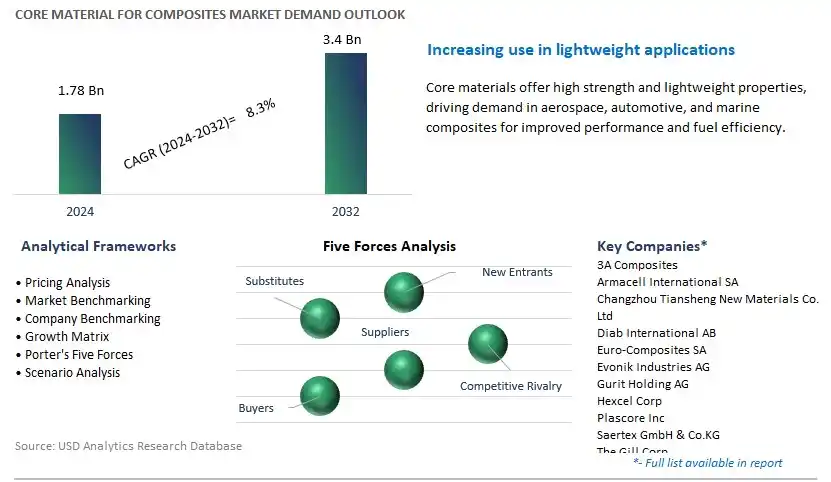

Global Core Material for Composites Market Size is valued at $1.78 Billion in 2024 and is forecast to register a growth rate (CAGR) of 8.3% to reach $3.4 Billion by 2032.

The global Core Material for Composites Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Type (Foam Core, Honeycomb, Wood), By End-User (Aerospace and Defense, Marine, Construction, Wind Energy, Automotive, Consumer Goods, Others).

An Introduction to Core Material for Composites Market in 2024

Core materials for composites are structural components used in sandwich panel construction to provide stiffness, strength, and support while minimizing weight in 2024. Sandwich panels consist of a lightweight core material sandwiched between two face sheets or skins, typically made of fiber-reinforced polymers (FRP), metal, or composite materials. The core material plays a critical role in determining the mechanical properties and performance of the sandwich panel, including bending stiffness, compression strength, and impact resistance. Common types of core materials used in composite sandwich panels include foams, honeycombs, and balsa wood. Foam cores, such as polyurethane, polystyrene, or PVC foam, offer excellent insulation properties and are lightweight, making them suitable for applications requiring thermal and acoustic insulation. Honeycomb cores, made from materials such as aluminum, Nomex, or fiberglass, provide high strength-to-weight ratios and are often used in aerospace, marine, and automotive applications where weight savings are critical. Balsa wood cores offer exceptional stiffness and strength-to-weight ratios and are commonly used in boat construction and wind turbine blades. The choice of core material depends on factors such as mechanical requirements, environmental conditions, and cost considerations. With advancements in material science and manufacturing technology, new lightweight and high-performance core materials are continually being developed, offering innovative solutions for a wide range of applications in industries such as aerospace, marine, transportation, and construction.

Core Material for Composites Market Competitive Landscape

The market report analyses the leading companies in the industry including 3A Composites, Armacell International SA, Changzhou Tiansheng New Materials Co. Ltd, Diab International AB, Euro-Composites SA, Evonik Industries AG, Gurit Holding AG, Hexcel Corp, Plascore Inc, Saertex GmbH & Co.KG, The Gill Corp, and others.

Core Material for Composites Market Dynamics

Market Trend: Increased Adoption of Lightweight Materials

A prominent trend in the market for core materials for composites is the increased adoption of lightweight materials in various industries, including aerospace, automotive, marine, and wind energy, driven by the need to reduce fuel consumption, improve performance, and enhance sustainability. Core materials play a crucial role in composite structures by providing stiffness, strength, and insulation while minimizing weight. As manufacturers and end-users seek to optimize the design and manufacturing of lightweight components and structures, there is a growing demand for core materials such as foams, honeycombs, and balsa wood that offer high strength-to-weight ratios, excellent mechanical properties, and compatibility with advanced composite manufacturing processes. This trend is driving market growth and innovation, with manufacturers investing in research and development of advanced core materials and production techniques to meet the evolving needs of industries transitioning towards lightweight and eco-friendly solutions.

Market Driver: Growth in Composites Manufacturing

The primary driver fueling the demand for core materials for composites is the growth in composites manufacturing across various industries, driven by increasing demand for high-performance, lightweight materials with superior mechanical properties and design flexibility. Composites offer advantages such as corrosion resistance, fatigue resistance, and tailored material properties, making them ideal for applications requiring strength, durability, and customization. As industries such as aerospace, automotive, construction, and renewable energy continue to adopt composites for structural and non-structural components, there is a significant need for core materials that provide structural support, impact resistance, and thermal insulation while enabling efficient manufacturing processes such as vacuum infusion, resin transfer molding, and sandwich panel construction. With the expanding use of composites in diverse applications, the demand for core materials is expected to grow, driving market expansion and investment in core material production capacity, technology innovation, and application development to meet industry requirements.

Market Opportunity: Development of Sustainable Core Materials

An emerging opportunity within the market for core materials for composites lies in the development of sustainable core materials that offer enhanced environmental performance and recyclability, addressing growing concerns about carbon footprint and end-of-life disposal of composite structures. Manufacturers can capitalize on this opportunity by investing in the research and development of bio-based core materials derived from renewable resources, recycled materials, or natural fibers that offer comparable or superior performance to traditional core materials while reducing reliance on fossil fuels and minimizing environmental impact. Additionally, opportunities exist for developing innovative manufacturing processes and composite recycling technologies that enable the reuse or repurposing of core materials at the end of their service life, contributing to circular economy principles and reducing waste generation. By offering sustainable core material solutions, manufacturers can meet the sustainability goals of their customers, differentiate themselves in the marketplace, and capture market share in industries prioritizing environmental stewardship and resource efficiency.

Core Material for Composites Market Share Analysis: Foam Core segment generated the highest revenue in 2024

Within the core material for composites market segmented by type, foam core is the largest segment, driven by its versatility, lightweight properties, and wide-ranging applications across industries. Foam core materials offer an optimal balance of strength, weight, and cost-effectiveness, making them preferred choices for various composite manufacturing processes. Their cellular structure provides excellent insulation properties and enhances buoyancy, making them particularly suitable for applications in marine, aerospace, and automotive industries. Additionally, foam core materials offer superior impact resistance and dimensional stability compared to other core materials, ensuring durability and structural integrity in composite structures. As industries continue to demand lightweight, high-performance materials for advanced applications, the foam core segment maintains its stronghold as the leading choice in the core material for composites market.

Core Material for Composites Market Share Analysis: Wind Energy Sector is poised to register the fastest CAGR over the forecast period

Among the segments categorized by end-users in the core material for composites market, the wind energy sector is the fastest-growing segment, driven by the global shift towards renewable energy sources and the rapid expansion of wind power infrastructure. Core materials play a critical role in the fabrication of wind turbine blades, providing structural support, stiffness, and aerodynamic efficiency essential for harnessing wind energy effectively. With increasing investments in wind energy projects worldwide and advancements in turbine technology driving larger blade sizes, there is a surging demand for lightweight yet durable core materials to optimize blade performance and reliability. Additionally, the push towards sustainability and reduced environmental impact further accelerates the adoption of composite materials in wind turbine manufacturing. As the wind energy sector continues to soar, the demand for core materials for composites is expected to witness robust growth, solidifying the wind energy segment's position as a key driver of expansion in the market.

Core Material for Composites Market

By Type

Foam Core

-PVC Foam

-Polystyrene Foam

-Polyurethane Foam

-PMMA Foam

-SAN Co-polymer Foam

-Others

Honeycomb

-Aluminum Honeycomb

-Nomex Honeycomb

-Thermoplastic Honeycomb

Wood

-Balsa

-Others

By End-User

Aerospace and Defense

Marine

Construction

Wind Energy

Automotive

Consumer Goods

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Core Material for Composites Companies Profiled in the Study

3A Composites

Armacell International SA

Changzhou Tiansheng New Materials Co. Ltd

Diab International AB

Euro-Composites SA

Evonik Industries AG

Gurit Holding AG

Hexcel Corp

Plascore Inc

Saertex GmbH & Co.KG

The Gill Corp

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Core Material for Composites Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Core Material for Composites Market Size Outlook, $ Million, 2021 to 2032

3.2 Core Material for Composites Market Outlook by Type, $ Million, 2021 to 2032

3.3 Core Material for Composites Market Outlook by Product, $ Million, 2021 to 2032

3.4 Core Material for Composites Market Outlook by Application, $ Million, 2021 to 2032

3.5 Core Material for Composites Market Outlook by Key Countries, $ Million, 2021 to 2032

4 Market Dynamics

4.1 Key Driving Forces of Core Material for Composites Industry

4.2 Key Market Trends in Core Material for Composites Industry

4.3 Potential Opportunities in Core Material for Composites Industry

4.4 Key Challenges in Core Material for Composites Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Core Material for Composites Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Core Material for Composites Market Outlook by Segments

7.1 Core Material for Composites Market Outlook by Segments, $ Million, 2021- 2032

By Type

Foam Core

-PVC Foam

-Polystyrene Foam

-Polyurethane Foam

-PMMA Foam

-SAN Co-polymer Foam

-Others

Honeycomb

-Aluminum Honeycomb

-Nomex Honeycomb

-Thermoplastic Honeycomb

Wood

-Balsa

-Others

By End-User

Aerospace and Defense

Marine

Construction

Wind Energy

Automotive

Consumer Goods

Others

8 North America Core Material for Composites Market Analysis and Outlook To 2032

8.1 Introduction to North America Core Material for Composites Markets in 2024

8.2 North America Core Material for Composites Market Size Outlook by Country, 2021-2032

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Core Material for Composites Market size Outlook by Segments, 2021-2032

By Type

Foam Core

-PVC Foam

-Polystyrene Foam

-Polyurethane Foam

-PMMA Foam

-SAN Co-polymer Foam

-Others

Honeycomb

-Aluminum Honeycomb

-Nomex Honeycomb

-Thermoplastic Honeycomb

Wood

-Balsa

-Others

By End-User

Aerospace and Defense

Marine

Construction

Wind Energy

Automotive

Consumer Goods

Others

9 Europe Core Material for Composites Market Analysis and Outlook To 2032

9.1 Introduction to Europe Core Material for Composites Markets in 2024

9.2 Europe Core Material for Composites Market Size Outlook by Country, 2021-2032

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Core Material for Composites Market Size Outlook by Segments, 2021-2032

By Type

Foam Core

-PVC Foam

-Polystyrene Foam

-Polyurethane Foam

-PMMA Foam

-SAN Co-polymer Foam

-Others

Honeycomb

-Aluminum Honeycomb

-Nomex Honeycomb

-Thermoplastic Honeycomb

Wood

-Balsa

-Others

By End-User

Aerospace and Defense

Marine

Construction

Wind Energy

Automotive

Consumer Goods

Others

10 Asia Pacific Core Material for Composites Market Analysis and Outlook To 2032

10.1 Introduction to Asia Pacific Core Material for Composites Markets in 2024

10.2 Asia Pacific Core Material for Composites Market Size Outlook by Country, 2021-2032

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Core Material for Composites Market size Outlook by Segments, 2021-2032

By Type

Foam Core

-PVC Foam

-Polystyrene Foam

-Polyurethane Foam

-PMMA Foam

-SAN Co-polymer Foam

-Others

Honeycomb

-Aluminum Honeycomb

-Nomex Honeycomb

-Thermoplastic Honeycomb

Wood

-Balsa

-Others

By End-User

Aerospace and Defense

Marine

Construction

Wind Energy

Automotive

Consumer Goods

Others

11 South America Core Material for Composites Market Analysis and Outlook To 2032

11.1 Introduction to South America Core Material for Composites Markets in 2024

11.2 South America Core Material for Composites Market Size Outlook by Country, 2021-2032

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Core Material for Composites Market size Outlook by Segments, 2021-2032

By Type

Foam Core

-PVC Foam

-Polystyrene Foam

-Polyurethane Foam

-PMMA Foam

-SAN Co-polymer Foam

-Others

Honeycomb

-Aluminum Honeycomb

-Nomex Honeycomb

-Thermoplastic Honeycomb

Wood

-Balsa

-Others

By End-User

Aerospace and Defense

Marine

Construction

Wind Energy

Automotive

Consumer Goods

Others

12 Middle East and Africa Core Material for Composites Market Analysis and Outlook To 2032

12.1 Introduction to Middle East and Africa Core Material for Composites Markets in 2024

12.2 Middle East and Africa Core Material for Composites Market Size Outlook by Country, 2021-2032

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Core Material for Composites Market size Outlook by Segments, 2021-2032

By Type

Foam Core

-PVC Foam

-Polystyrene Foam

-Polyurethane Foam

-PMMA Foam

-SAN Co-polymer Foam

-Others

Honeycomb

-Aluminum Honeycomb

-Nomex Honeycomb

-Thermoplastic Honeycomb

Wood

-Balsa

-Others

By End-User

Aerospace and Defense

Marine

Construction

Wind Energy

Automotive

Consumer Goods

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

3A Composites

Armacell International SA

Changzhou Tiansheng New Materials Co. Ltd

Diab International AB

Euro-Composites SA

Evonik Industries AG

Gurit Holding AG

Hexcel Corp

Plascore Inc

Saertex GmbH & Co.KG

The Gill Corp

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Type

Foam Core

-PVC Foam

-Polystyrene Foam

-Polyurethane Foam

-PMMA Foam

-SAN Co-polymer Foam

-Others

Honeycomb

-Aluminum Honeycomb

-Nomex Honeycomb

-Thermoplastic Honeycomb

Wood

-Balsa

-Others

By End-User

Aerospace and Defense

Marine

Construction

Wind Energy

Automotive

Consumer Goods

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)