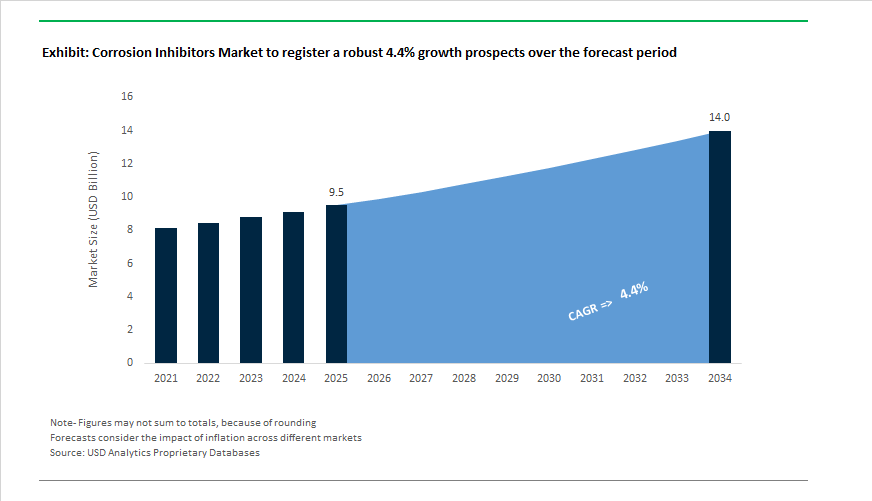

Corrosion Inhibitors Market Outlook 2025–2034: $9.5 Billion to $14 Billion at 4.4% CAGR Driven by Bio-Based Chemistries and Digital Formulation Platforms

The global Corrosion Inhibitors Market is projected to grow from $9.5 billion in 2025 to $14 billion by 2034, registering a CAGR of 4.4%. Demand is supported by infrastructure rehabilitation, refinery upgrades for high-acid crude processing, growth in waterborne industrial coatings, and stricter drinking water compliance standards. Corrosion inhibitors are widely deployed across cooling towers, boilers, oil refineries, municipal water systems, marine coatings, coil coatings, and aerospace primers. Market evolution is being shaped by low-phosphorus formulations, zero-VOC inhibitors, heavy-metal-free additives, and digital chemistry optimization tools aimed at improving lifecycle performance and environmental compliance.

Strategic consolidation and capacity expansion accelerated during 2024–2026. In February 2024, Nalco Water introduced the SCORPION™ High Temperature Corrosion Control Program for refineries processing high-acid crudes, utilizing low-phosphorus chemistry to minimize downstream catalyst contamination. In August 2024, PPG launched PRIMERON Optimal powder primer with optimized zinc levels to enhance corrosion resistance and durability in industrial outdoor environments. In March 2025, ICL introduced HALOX® 580 at the European Coatings Show, a 50% bio-based, ultra-low VOC corrosion inhibitor targeting eco-certified architectural and light industrial coatings. During the same event, HALOX® FLASH-X® 152 was launched as a zero-VOC dual-action inhibitor preventing both flash rust and galvanic weld corrosion. In November 2025, Solenis completed the acquisition of NCH Corporation, integrating localized onsite service models into its global corrosion protection network for industrial boilers and cooling systems.

Sustainability-led product reformulation intensified across coatings and packaging. In January 2025, Cortec launched EcoLine® 3860, a water-based acrylic anticorrosion coating containing 27% USDA-certified bio-based content, providing a renewable alternative for metal protection in high-humidity environments. In December 2025, ICL released HALOX® 650, a zero-VOC organic corrosion inhibitor engineered for high-temperature solvent-based and powder-coating applications such as aerospace primers and coil coatings. Cortec expanded its circular packaging strategy in January 2026, transitioning VpCI®-126 corrosion-inhibiting bags to a minimum of 20% recycled content. In February 2026, Cortec introduced a phosphate-free corrosion inhibitor specifically designed for hydro-testing of municipal drinking water storage systems, ensuring compliance without hazardous residues.

Digital innovation and regional manufacturing investments further strengthened competitive positioning. BASF showcased AI-driven corrosion inhibitor discovery at EUROCORR in September 2025, using machine learning to predict high-efficiency passivation chemistries and accelerate sustainable inhibitor development. In February 2026, BASF expanded dispersions production at its Mangalore, India facility to meet rising regional demand for construction coatings incorporating advanced corrosion protection technologies. BASF also announced the opening of a Global Digital Hub in Hyderabad in the first quarter of 2026, focusing on data-driven optimization of specialty additives and corrosion inhibitor formulations at scale. These developments illustrate a market increasingly defined by bio-based chemistry adoption, phosphate elimination, digital R&D acceleration, and integrated service models, supporting steady mid-single-digit growth through 2034.

Corrosion Inhibitors Market Trends and Drivers

Global Mandate Toward Environmentally Acceptable (EAL) and Water-Based Corrosion Inhibitors

The corrosion inhibitors market is entering a mandatory transition cycle—not optional—driven by regulatory enforcement across North America, Europe, and offshore industrial zones.

A pivotal inflection point is REACH Annex XVII, which from September 1, 2025 restricts CMR Category 1B substances, including Diuron and phosphonium salts, effectively eliminating their use in consumer-facing supply chains and forcing industrial operators toward water-borne, phosphorus-free, and bio-derived inhibitors.

Simultaneously, the U.S. EPA is tightening restrictions on hexavalent chromium-based inhibitors, accelerating the commercialization of lignin-derived, chitosan-based, and amino-acid-modified corrosion formulations. These alternatives reduce VOC emissions, align with ISO environmental certification requirements, and support Scope 3 decarbonization targets.

High-Temperature / High-Salinity (HT/HS) Inhibitors Power the Energy Transition Landscape

Energy markets are expanding into extreme environments—deepwater oil, geothermal wells, and ultra-saline produced water systems—driving the need for thermally stable, salinity-resistant inhibitor chemistries.

According to the IEA Geothermal Outlook, geothermal capacity capable of supplying 15% of global electricity demand by 2050 will require inhibitors stable above 150°C. Correspondingly, academic validation (Southwest Jiaotong University, 2025) confirmed temperature-responsive gel-epoxy solid inhibitors that release protection only when temperatures spike, preventing premature breakdown and coating fatigue.

In parallel, mature wells in the Permian Basin report Total Dissolved Solids exceeding 200,000 ppm, catalyzing demand for high-molecular-weight quaternary ammonium compounds engineered to prevent precipitation and scaling when operators migrate to closed-loop produced-water reinjection systems.

Corrosion Inhibitors Purpose-Built for Green Hydrogen and CCUS Infrastructure

The decarbonization economy is reshaping corrosion engineering. As hydrogen transport pipelines expand, corrosion inhibitors are required to prevent hydrogen embrittlement, which can reduce pipeline ductility, posing catastrophic risk.

With the global hydrogen-to-energy economy projected to reach $6.8 trillion by 2050, the near-term commercial opportunity lies in Vapor-Phase Inhibitors (VPIs) for hydrogen-blended gas networks. August 2025 research demonstrated that surface-modifying inhibitors can raise resistive polarization (Rp) values above 300,000 ohm-cm², creating a persistent barrier that disrupts hydrogen penetration of metallic substrates.

The adjacent value pool is CO₂ corrosion protection within the rapidly expanding CCUS sector. Under India’s National Green Hydrogen Mission (US$2.4B funding), chemical innovation is targeting dense-phase CO₂ transport, where impurities such as SOx and NOx acidify condensate and accelerate corrosion—requiring specialized inhibitors that remain functional in dehydration-limited pipe environments.

Corrosion Inhibitors Market Share and Segmentation Insights

Type-Based Segmentation: Water-Based Inhibitors Dominate as VCI Technologies Expand

Water-based corrosion inhibitors command 48% market share in 2025, supported by favorable environmental profiles, cost efficiency, and compatibility with cooling water, closed-loop heating, and water injection systems. Their widespread adoption reflects tightening discharge regulations and increasing emphasis on sustainable water treatment programs. Oil-based inhibitors represent a substantial segment in hydrocarbon processing environments, including crude oil pipelines, refinery operations, and lubricant systems, where film-forming amines and petroleum sulfonates provide moisture-resistant surface protection. Volatile corrosion inhibitors (VCIs) are the fastest-growing category, offering vapor-phase protection for enclosed environments such as automotive component packaging, electronics storage, and aerospace assemblies. Across all types, manufacturers are advancing biodegradable, low-toxicity formulations aligned with green chemistry principles and stricter offshore and marine environmental compliance requirements.

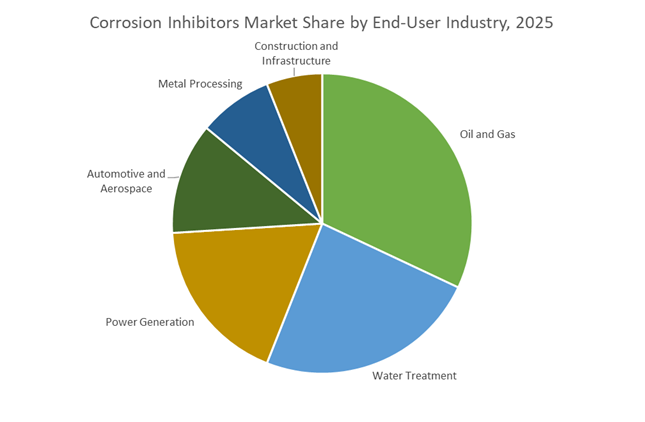

End-User Industry Breakdown: Oil and Gas Leads While Infrastructure Protection Expands

Oil and gas accounts for 32% of corrosion inhibitor consumption, reflecting persistent exposure to sour gas, saline water, and high-pressure environments from wellhead to refinery. Maintaining pipeline integrity and preventing asset failure remain critical safety and environmental imperatives. Water treatment and power generation follow closely, relying on inhibitors to preserve boilers, cooling towers, and steam systems that directly impact energy efficiency and plant reliability. Automotive and aerospace applications utilize inhibitors in engine coolants, hydraulic systems, and temporary protective coatings, with aerospace demanding exceptionally high reliability under extreme operating conditions. Metal processing industries depend on inhibitors in pickling baths and metalworking fluids to prevent premature surface degradation. Construction and infrastructure applications focus on extending the service life of reinforced concrete, bridges, and structural steel through corrosion control strategies that reduce lifecycle maintenance costs and protect public assets.

Competitive Landscape of the Corrosion Inhibitors Market

The Corrosion Inhibitors Market is shaped by digitally enabled water management leaders, material science innovators, and oilfield specialists delivering AI-driven dosing, bio-based chemistries, and high-performance protection for industrial, energy, and infrastructure assets.

Ecolab pioneers AI-powered corrosion management with closed-loop 3D TRASAR platforms

Ecolab remains the market leader in corrosion inhibitors for water-intensive industries, anchored by Nalco Water’s digitally integrated service model. Its flagship 3D TRASAR™ platform uses fluorescence technology to track inhibitor residuals and corrosion rates in real time. In early 2026, Ecolab expanded its partnership with Microsoft, embedding advanced AI predictive analytics to enable pre-emptive dosing based on weather patterns and incoming water quality. The OptiGuard™ Bio series, launched in 2025, introduced 100% biodegradable organic film-formers for marine and offshore environments. A key differentiator is vertical integration, combining proprietary chemistry, sensor hardware, and the LOAMS cloud platform into a closed-loop corrosion control ecosystem.

Solenis scales phosphorus-free corrosion programs for circular industrial water systems

Solenis has emerged as a dominant force in pulp, paper, and heavy industrial cooling following its 2025–2026 middle-market expansion. In February 2026, Solenis completed integration of NCH Corporation’s water treatment business, increasing its global onsite technician base by 20%. The company specializes in phosphorus-free corrosion inhibitors designed to meet tightening 2026 discharge regulations. At recent trade events, Solenis showcased HexEval™, an algorithm trained on thousands of heat exchangers that predicts corrosion risk with over 90% accuracy. Its core strength lies in circular economy enablement, supplying inhibitors that remain effective in high-cycle, high-impurity wastewater reuse systems across manufacturing and processing plants.

BASF advances smart-release inhibitors and ZeroPCF portfolios for electronics and EV protection

BASF operates both as an innovator of finished corrosion inhibitors and a major supplier of upstream chemical building blocks. On February 13, 2026, BASF opened a new dispersions production line in Mangalore, India, supporting fast-growing infrastructure and industrial demand across Asia-Pacific. Under its Winning Ways strategy, BASF is targeting Zero Product Carbon Footprint versions of its inhibitor portfolio by 2030 using biomass-balanced feedstocks. Recent R&D includes nanotechnology-enabled “smart capsule” inhibitors that release active agents only when pH shifts signal corrosion onset. BASF also leads in automotive and electronics, supplying high-purity VCIs for EV batteries and semiconductor manufacturing equipment.

Baker Hughes dominates oilfield corrosion protection and CCUS pipeline integrity

Baker Hughes is a global leader in oil and gas corrosion inhibitors, engineered for extreme temperature, pressure, and salinity conditions. Its TOLAD™ and SMARTGUARD™ product lines provide robust film-forming protection in high-CO2 sweet and H2S sour environments. During 2025–2026, Baker Hughes pivoted aggressively toward carbon capture, utilization, and storage, developing specialized inhibitors for CO2 transport pipelines. Oil and gas applications account for roughly 38% of global inhibitor revenues in 2026, with Baker Hughes holding a significant share. The company’s Intelligent Chemistry approach leverages automated systems such as Leucipa to remotely manage chemical injection rates via satellite, optimizing field-level corrosion control.

Dow integrates polymer science into boiler and infrastructure corrosion prevention

Dow focuses on material science-driven corrosion inhibition, supplying advanced polymers and chelants integrated into coatings and boiler treatment programs. Its ACUMER™ and VERSENE™ platforms are industry benchmarks for scale and corrosion control in high-pressure steam systems. In January 2026, Dow launched its Transform to Outperform initiative, deploying AI across operations to drive a USD 2 billion operational EBITDA uplift through productivity and customer experience modernization. With manufacturing in 29 countries, Dow обеспечивает localized supply for construction and metals processing markets. Strategically, Dow is simplifying its portfolio to concentrate on high-growth segments such as corrosion protection for 5G infrastructure and renewable energy installations.

Cortec leads bio-based VCI technologies for infrastructure preservation and green packaging

Cortec is the global authority in Volatile Corrosion Inhibitor technology, with strong leadership in bio-based and compostable formulations used by military and aerospace sectors for long-term asset preservation. A major innovation is Migrating Corrosion Inhibitor technology for concrete rehabilitation, allowing surface-applied inhibitors to penetrate concrete and protect embedded rebar in bridges and marine structures. In early 2026, Cortec launched its Material Bank framework, a digital platform designed to manage and preserve idle construction materials across large infrastructure projects. Cortec’s primary application focus is infrastructure rehabilitation, extending asset lifespans through non-invasive treatments aligned with sustainable construction practices.

United States: Aging Assets, PFAS-Free Chemistry, and Digital Corrosion Intelligence

The United States corrosion inhibitors industry is being reshaped by the convergence of aging infrastructure, environmental regulation, and data-driven asset integrity management. A 2025 status update from the U.S. Department of Transportation highlights that more than 60% of national pipeline and refinery assets have exceeded 30 years of service life. This structural reality is accelerating procurement of high-performance Organic Acid Technology inhibitors, which extend operational safety without introducing heavy metals. Environmental compliance is reinforcing this shift. In early 2025, the U.S. Environmental Protection Agency finalized strict PFAS discharge limits, forcing reformulation of cooling tower and industrial inhibitors toward amine-based and other sustainable alternatives that eliminate persistent fluorinated compounds.

Standards development and digitalization are further elevating technical requirements. Throughout 2025, ASTM International Committee D15 advanced WK76375 and WK83561 to define corrosion protection protocols for low-conductivity fluids used in EV battery plates, creating a new testing and qualification baseline for electrically sensitive systems. At the plant level, Honeywell scaled its Predict-RT digital corrosion twin, integrating real-time sensor data with inhibitor dosing algorithms to predict corrosion rates dramatically faster than manual sampling. Municipal and defense demand is also expanding. Cortec Corporation broadened its Migrating Corrosion Inhibitor portfolio in December 2025 to protect reinforced concrete in desalination and water infrastructure, while the U.S. Department of Defense expanded budgets for bio-based vapor phase corrosion inhibitors to safeguard maritime assets and stored equipment.

China: Trade Controls, Circular Packaging, and Smart Coastal Infrastructure

China’s corrosion inhibitors landscape is influenced by trade policy, circular economy mandates, and rapid digitalization of coastal infrastructure. On January 2, 2025, the U.S. Department of Commerce released preliminary administrative review results that maintained elevated cash deposit requirements on corrosion inhibitors imported from China. This action has sharpened pricing discipline in export markets while encouraging Chinese producers to move up the value chain.

Domestically, regulatory mandates are opening new application pathways. Regional requirements introduced in 2025 for industrial packaging to contain at least 20% recycled content have prompted chemical hubs in Shanghai and Zhejiang to develop VCI-integrated recycled resins, combining corrosion protection with circular materials compliance. High-purity chemistry is advancing alongside this shift. In early 2025, BASF inaugurated its loopamid facility in Shanghai. While centered on polyamide circularity, the site is serving as a pilot platform for extracting high-purity intermediates relevant to next-generation corrosion-inhibiting polymers. Infrastructure protection is becoming increasingly digital. Under the national Industrial Digitalization Roadmap, funding allocated in 2025 is supporting IoT-enabled dosing systems across more than 40 coastal cities to mitigate seawater-induced corrosion in ports, bridges, and municipal assets.

Germany: AI-Guided Chemistry and Hydrogen-Ready Inhibitor Systems

Germany continues to set the pace for high-technology, regulation-aligned corrosion inhibitor innovation, particularly at the intersection of artificial intelligence and the energy transition. In August 2025 at EUROCORR, BASF Coatings disclosed the use of machine learning models to identify effective inhibitor molecules, significantly accelerating discovery of non-toxic, chromium-free surface treatments. This approach is compressing R&D timelines while aligning formulations with EU sustainability expectations.

Energy infrastructure transformation is another critical driver. The German Federal Ministry of Research funded multi-year projects during 2025–2026 focused on methane pyrolysis and hydrogen transport, creating demand for specialized inhibitors that prevent hydrogen embrittlement in repurposed gas pipelines. Offshore compliance has also reached a tipping point. By mid-2025, German chemical suppliers transitioned all North Sea offshore formulations to OSPAR-compliant biodegradable chemistries, fully replacing legacy phosphate-based inhibitors. These developments reinforce Germany’s role as a proving ground for corrosion inhibitors designed for future energy systems and strict environmental governance.

India: Long-Life Infrastructure and Localization of Specialty Chemistry

India’s corrosion inhibitors industry is expanding on the back of large-scale infrastructure programs and targeted localization policy. Under the PM Gatishakti National Master Plan 2025 update, government agencies prioritized advanced Migrating Corrosion Inhibitors for high-speed rail corridors and coastal bridge projects, with the explicit objective of achieving century-long service life in aggressive environments. This focus is driving adoption of inhibitors that protect embedded steel and concrete simultaneously, reducing lifetime maintenance costs.

Industrial policy is reinforcing domestic capacity. The Department for Promotion of Industry and Internal Trade identified corrosion protection as a Vocal for Local priority in its 2024–2025 report, enabling 100% foreign direct investment under the automatic route for specialty chemical manufacturing. This framework is attracting global technology while building indigenous production of corrosion inhibitors tailored for India’s climatic and infrastructural conditions.

Comparative Snapshot: Country-Level Strategic Direction in the Corrosion Inhibitors Industry

Corrosion Inhibitors Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

Key Application Focus

|

Direction of Inhibitor Innovation

|

|

United States

|

Aging infrastructure and PFAS regulation

|

Pipelines, EV cooling, defense assets

|

OAT-based, PFAS-free, digital twin enabled

|

|

China

|

Trade controls and circular economy mandates

|

Packaging, coastal infrastructure

|

VCI-integrated recycled materials, IoT dosing

|

|

Germany

|

AI-driven R&D and hydrogen transition

|

Automotive, offshore, hydrogen pipelines

|

Non-toxic, biodegradable, hydrogen-resistant

|

|

India

|

Infrastructure longevity and localization

|

Rail, bridges, coastal assets

|

MCI-focused, locally manufactured systems

|

Corrosion Inhibitors Market Report Scope

Corrosion Inhibitors Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$9.5 Billion

|

|

Market Size (2034)

|

$14 Billion

|

|

Market Growth Rate

|

4.4%

|

|

Segments

|

By Compound (Organic Inhibitors, Inorganic Inhibitors, Hybrid and Green Inhibitors), By Type (Water-Based Inhibitors, Oil-Based Inhibitors, Volatile Corrosion Inhibitors), By Mechanism (Anodic Inhibitors, Cathodic Inhibitors, Mixed and Film-Forming Inhibitors), By End-User Industry (Oil and Gas, Water Treatment, Power Generation, Automotive and Aerospace, Construction and Infrastructure, Metal Processing)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ecolab Inc., BASF SE, Cortec Corporation, Ashland Global Holdings Inc., Baker Hughes Company, The Lubrizol Corporation, Solenis LLC, Dow Inc., Henkel AG & Co. KGaA, DuPont de Nemours Inc., AkzoNobel N.V., Syensqo SA, Clariant AG, Suez SA, Italmatch Chemicals S.p.A.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Corrosion Inhibitors Market Segmentation

By Compound

- Organic Inhibitors

- Inorganic Inhibitors

- Hybrid and Green Inhibitors

By Type

- Water-Based Inhibitors

- Oil-Based Inhibitors

- Volatile Corrosion Inhibitors

By Mechanism

- Anodic Inhibitors

- Cathodic Inhibitors

- Mixed and Film-Forming Inhibitors

By End-User Industry

- Oil and Gas

- Water Treatment

- Power Generation

- Automotive and Aerospace

- Construction and Infrastructure

- Metal Processing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Corrosion Inhibitors Industry

- Ecolab Inc.

- BASF SE

- Cortec Corporation

- Ashland Global Holdings Inc.

- Baker Hughes Company

- The Lubrizol Corporation

- Solenis LLC

- Dow Inc.

- Henkel AG & Co. KGaA

- DuPont de Nemours Inc.

- AkzoNobel N.V.

- Syensqo SA

- Clariant AG

- Suez SA

- Italmatch Chemicals S.p.A.

*- List not Exhaustive