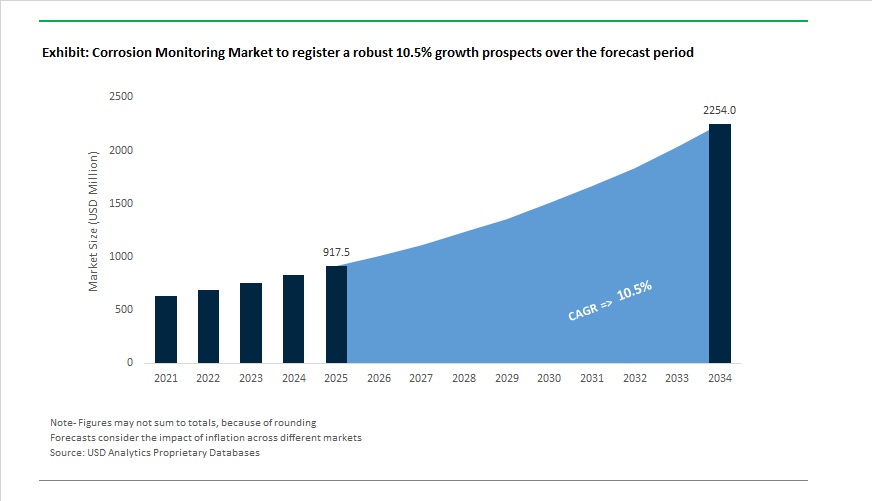

Corrosion Monitoring Market Outlook 2025–2034: $917.5 Million to $2,253.5 Million at 10.5% CAGR Driven by Digital Asset Integrity Platforms

The Corrosion Monitoring Market is projected to expand from $917.5 Million in 2025 to $2,253.5 Million by 2034, reflecting a robust 10.5% CAGR. Growth is being propelled by refinery digitalization, subsea asset integrity programs, regulatory mandates in municipal water infrastructure, and predictive analytics integration across oil, gas, power, and chemical processing industries. The market is transitioning from traditional coupon-based inspection models toward continuous, sensor-enabled corrosion detection systems integrated with AI-powered analytics platforms. Real-time wall thickness monitoring, corrosion under insulation detection, sand erosion correlation, and digital twin modeling are becoming core pillars of industrial asset management strategies.

Regulatory enforcement and municipal water infrastructure modernization accelerated early demand momentum. In November 2023–2024, the U.S. EPA proposed Lead and Copper Rule Improvements requiring utilities to implement enhanced Corrosion Control Treatment monitoring programs, triggering large-scale deployment of corrosion monitoring stations across municipal distribution networks. In February 2024, Corrosion Innovations acquired HoldTight Solutions to integrate soluble salt removal and surface testing technologies into broader corrosion lifecycle management portfolios, strengthening pre-coating inspection capabilities. During 2024, the Qatar Foundation introduced smart embedded corrosion coupons capable of transmitting integrity data digitally from inside pipelines, bridging the gap between manual inspection and real-time remote monitoring. In the same period, Emerson expanded its Plantweb Insight™ ecosystem by adding the Inline Corrosion Application, enabling real-time internal fluid corrosivity assessment through ER and LPR probe data aggregation.

Subsea and offshore asset integrity emerged as high-growth verticals. In February 2025, ClampOn secured a major subsea corrosion erosion monitoring contract for an offshore South American project, deploying tomography-based instruments to map deep-water pipe wall changes. In March 2025, Baker Hughes partnered with Petrobras to co-develop next-generation flexible pipe systems resistant to SCC-CO2 stress corrosion cracking, targeting 30-year lifespans in high-CO2 pre-salt fields. ClampOn expanded its Middle East operations in November 2024 by opening a Dubai branch to address rising demand for topside corrosion erosion monitors in large-scale energy projects across Saudi Arabia and the UAE. In January 2026, ClampOn launched Sand Monitor 4.0 integrated with its Corrosion-Erosion Monitor platform, enabling operators to correlate acoustic sand detection with real-time metal loss data for predictive failure modeling in pipeline bends.

Industrial digitalization and refinery optimization programs intensified during 2025–2026. Honeywell updated its Predict® Corrosion Suite in 2024–2025, introducing advanced what-if modeling capabilities that allow refiners to simulate corrosion rates for opportunity crudes without installing additional hardware. Emerson enhanced deployment flexibility in 2024–2025 with a Magnetic Vessel Mount solution for Rosemount™ Wireless Permasense transmitters, enabling weld-free installation on large vessels and tanks for continuous metal loss monitoring. In February 2026, Baker Hughes secured a landmark agreement with Marathon Petroleum to deploy TOPGUARD™ corrosion inhibitors integrated with digital monitoring platforms across 12 U.S. refineries and two renewable fuel facilities, aligning chemical treatment programs with predictive analytics. These developments underscore the accelerating convergence of corrosion chemistry, sensor hardware, regulatory compliance frameworks, and AI-driven digital twins, positioning corrosion monitoring as a central component of industrial reliability and environmental risk management strategies through 2034.

Trends and Opportunities Shaping the Global Corrosion Monitoring Market

Wireless Sensor Networks Integrated with Predictive Analytics Platforms

Industrial operators are rapidly replacing manual corrosion measurement and spreadsheet-based inspection logs with wireless sensor networks connected to cloud-based analytics platforms. Field deployments in 2025 demonstrated that battery-powered corrosion and environmental sensors using LoRaWAN and NB-IoT connectivity can operate for up to 10 years without replacement, transmitting hourly humidity and temperature data from under insulation layers. Solutions such as CUI-focused sensor systems allow operators to detect Corrosion Under Insulation without removing cladding, cutting scaffolding requirements and inspection labor costs by a significant margin while improving inspection frequency.

The strategic value extends beyond automation. Cloud platforms are now applying machine learning algorithms to electrochemical noise data, linear polarization resistance measurements, and ultrasonic wall thickness readings. When integrated with digital twin models of piping networks and pressure vessels, these platforms can forecast remaining useful life with a level of precision that supports data-driven Risk-Based Inspection programs aligned with API 570 requirements. This transition from reactive maintenance to predictive integrity management is becoming a core differentiator for corrosion monitoring vendors competing for large-scale multi-site contracts.

NDT Robotics Adoption for Hazardous, Confined, and Inaccessible Assets

Robotics-enabled non-destructive testing is moving from pilot projects into standard inspection workflows for high-risk assets. By late 2025, omnidirectional aerial drones capable of stable contact-based ultrasonic testing had proven their ability to measure wall thickness on vertical and overhead structures such as flare stacks and storage tanks. These systems eliminate the need for rope access or human climbers, directly supporting compliance with ISO 45001 occupational safety standards while reducing inspection downtime.

At the same time, magnetic crawler robots equipped with phased array ultrasonics and eddy current probes are becoming standard for internal pipeline, tank floor, and coated surface inspections. These crawlers can penetrate coatings and insulation to detect subsurface pitting and corrosion with centimeter-level accuracy. The inspection data is increasingly integrated into geographic information systems and centralized asset integrity dashboards, enabling corrosion engineers to prioritize interventions based on quantified risk rather than visual indicators alone. This trend is strengthening demand for vendors that can deliver both hardware reliability and seamless data integration.

Corrosion Monitoring for CCUS and High-Pressure CO₂ Transport Networks

The global expansion of Carbon Capture, Utilization, and Storage infrastructure is creating a specialized and high-margin opportunity for corrosion monitoring suppliers. Studies conducted in early 2025 on large-scale CCUS projects such as the Changqing Oilfield demonstrated that trace impurities including sulfur oxides and nitrogen oxides can drive localized corrosion rates as high as 3.5 mm per year when moisture is present in CO₂ streams. These findings are reshaping material selection and monitoring strategies for CO₂ pipelines and injection wells.

As a result, operators are investing in high-pressure linear polarization resistance probes, corrosion coupons, and electrochemical sensors specifically engineered for dense-phase and supercritical CO₂ environments. In parallel, wellbore integrity programs are increasingly deploying fiber optic distributed acoustic sensing and electrochemical monitoring systems at depths exceeding 2,000 meters to track changes in redox conditions and casing integrity. Vendors that can validate sensor survivability under extreme pressure and temperature conditions are well positioned to secure long-term contracts tied to national decarbonization initiatives.

Real-Time Monitoring of Reinforced Concrete Infrastructure

Aging civil infrastructure in North America and Europe is driving strong demand for corrosion monitoring solutions tailored to reinforced concrete structures. Regulatory agencies report that nearly 30% of residential and civil buildings already exhibit corrosion-related degradation, with bridge maintenance alone accounting for approximately 15% of total operating budgets for major facilities. In response, infrastructure owners are shifting toward embedded IoT sensors that continuously monitor concrete resistivity, chloride ingress, and rebar corrosion activity.

Corrosion Monitoring Market Share and Segmentation Insights

Monitoring Type Landscape: Non-Intrusive Technologies Lead as Predictive Maintenance Accelerates

Non-intrusive corrosion monitoring accounts for 58% of market share in 2025, driven by widespread adoption of ultrasonic testing, guided wave inspection, magnetic flux leakage, and acoustic emission systems that enable asset integrity assessment without operational shutdowns. These techniques eliminate production losses and significantly reduce safety risks associated with opening pressurized equipment, making them the preferred choice across oil and gas, power generation, and infrastructure networks. Intrusive monitoring methods, including electrical resistance probes, linear polarization resistance sensors, and corrosion coupons, continue to hold a meaningful share by delivering direct electrochemical data and real-time corrosion rate measurements inside pipelines and process vessels. The market is rapidly shifting toward continuous condition monitoring, with wireless non-intrusive sensors feeding digital platforms to support predictive maintenance strategies. In practice, operators increasingly deploy both approaches together, combining intrusive probes for corrosion kinetics with non-intrusive inspection to validate wall loss, pitting, and crack propagation.

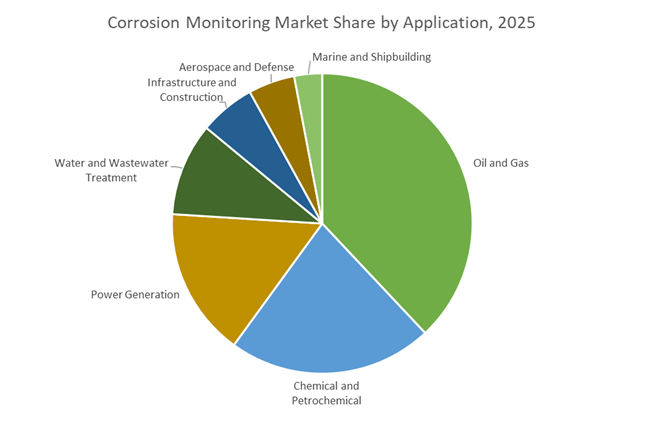

Application Breakdown: Oil and Gas Dominates While Utilities and Infrastructure Expand Adoption

Oil and gas represents 38% of corrosion monitoring demand, reflecting extreme operating environments across upstream production, long-distance pipelines, and high-temperature refining units exposed to CO2, H2S, and aggressive process fluids. Chemical and petrochemical facilities follow closely, where monitoring is essential to prevent catastrophic releases and unplanned shutdowns in high-pressure systems handling corrosive compounds. Power generation relies on corrosion monitoring to protect boilers, condensers, and cooling circuits, with nuclear plants integrating monitoring tightly into regulatory safety frameworks. Water and wastewater utilities deploy monitoring to manage internal corrosion from aggressive water chemistry and external degradation of buried assets. Infrastructure and construction applications focus on bridges, storage tanks, and reinforced concrete, prioritizing long-term structural health. Aerospace, defense, marine, and shipbuilding represent specialized segments, demanding high-reliability monitoring for aircraft structures, naval vessels, and offshore assets operating in highly corrosive environments.

Competitive Landscape of the Corrosion Monitoring Market

The Corrosion Monitoring Market is driven by digital sensing, predictive analytics, and asset integrity platforms, with leaders combining wireless infrastructure, AI-enabled software, and field-proven probes to minimize unplanned downtime across oil & gas, refining, power generation, and heavy industry.

Emerson leads non-intrusive wireless corrosion monitoring with Plantweb analytics

Emerson dominates non-intrusive corrosion monitoring by combining Rosemount™ Wireless Permasense ultrasonic transmitters with Plantweb™ Insight software for continuous metal-loss detection without pipe penetration. In 2025, Emerson launched the Plantweb™ Insight Inline Corrosion Application, leveraging WirelessHART to deliver actionable corrosion insights directly to refinery dashboards. Its Connected Services strategy now includes quarterly Remote Data Enhancement reports, where Emerson specialists analyze asset data to optimize inspection and maintenance timing. A core competitive advantage is Emerson’s pervasive wireless infrastructure, enabling large-scale deployment in remote or hazardous environments where hardwiring is cost-prohibitive, making it a preferred partner for digital corrosion monitoring in energy, chemicals, and process industries.

Baker Hughes integrates corrosion sensing with automated chemical control for oil and CCUS

Baker Hughes is a powerhouse in corrosion monitoring for oil, gas, and emerging CCUS infrastructure, blending mechanical integrity with intelligent chemistry. In February 2026, Baker Hughes became the preferred digital monitoring provider for Marathon Petroleum, rolling out solutions across 12 refineries and two renewable fuel facilities. The company is also expanding aggressively into CO2 transport monitoring, developing sensors tailored to CCUS corrosion profiles. Its Leucipa™ automated field production platform uses AI to adjust inhibitor injection based on live corrosion data. Vertical integration through Waygate Technologies (NDT) and Bently Nevada enables a holistic asset integrity model spanning inspection, monitoring, and predictive maintenance.

Honeywell pioneers model-based corrosion prediction with soft-sensor APM platforms

Honeywell differentiates itself through software-led corrosion monitoring, reducing reliance on physical sensors via advanced predictive models. Its Predict® Corrosion Suite, including Predict-Crude and Predict-Pipe, quantifies corrosion rates for specific metallurgy and operating conditions. During 2025–2026, Honeywell scaled Forge Performance+ for Industrials, embedding soft sensors into its Asset Performance Management platform to forecast corrosion digitally. A key strategic pillar is “what-if” scenario analysis, allowing refiners to simulate the corrosion impact of opportunity crudes before processing. Honeywell reports that customers using its real-time monitoring tools have avoided unit failure costs exceeding USD 60 million per incident through proactive alerts.

SGS strengthens asset integrity with microbial corrosion analytics and global field services

SGS leads the testing and forensic side of corrosion monitoring, combining on-site inspections with laboratory-grade diagnostics. In late 2025 and early 2026, SGS acquired MsMin and Cyanre Group to enhance industrial asset integrity and accelerate its digital transformation. A standout capability is Microbial Risk Assessment Services (MiRAS), where SGS applies qPCR and next-generation sequencing to detect Microbiologically Influenced Corrosion. With a vast global laboratory network, SGS also delivers Environmental Simulation Testing to replicate harsh marine conditions and predict material lifespan. Its integrated model independently validates biocide and inhibitor performance, supporting compliance-driven industries worldwide.

Cosasco sets the benchmark for intrusive corrosion probes in high-pressure environments

Cosasco is a pure-play corrosion monitoring specialist, widely regarded as the gold standard for intrusive measurement in extreme operating conditions. Its Microcor® electrical resistance probes detect corrosion in as little as 30 seconds, providing direct, high-resolution metal-loss data. Cosasco dominates high-pressure, high-temperature applications, offering retrieval systems that safely replace probes at pressures up to 10,000 psi without shutdown. Recent innovation includes the Cosasco Wireless System, which upgrades legacy mechanical monitoring points to automated remote transmission. The company’s core strength lies in deep expertise in corrosion physical chemistry, delivering the industry’s most direct and reliable measurement of active corrosion.

United States: Digital Twins and EV Standards Redefining Corrosion Intelligence

The United States corrosion monitoring industry is advancing rapidly as aging infrastructure, electric vehicle adoption, and environmental compliance converge. According to the U.S. Department of Transportation, more than 60% of pipeline and refinery assets had exceeded their original 30-year design life by 2025. This has materially increased demand for advanced corrosion monitoring architectures aligned with Organic Acid Technology environments, where continuous monitoring is essential to extend asset life without introducing heavy metals. The industry focus has shifted from periodic inspection toward continuous integrity assurance, particularly across energy, petrochemical, and municipal water systems.

Standards and digitalization are reinforcing this evolution. In late 2025, ASTM International Committee D15 progressed WK76375 and WK83561 toward final ballot, defining low-conductivity monitoring requirements for EV battery cooling systems. These standards are catalyzing adoption of high-sensitivity sensors capable of operating in electrically isolated thermal fluids. Laboratory automation is accelerating response times. POLARIS Laboratories advanced its Aurora AI platform through 2025, enabling operators to detect liner pitting and scale formation up to six months ahead of mechanical failure. At the asset level, Honeywell scaled its Predict-RT digital twin framework, integrating real-time corrosion sensor data with chemical dosing logic and delivering significantly faster corrosion rate prediction than manual sampling. Regulatory pressure is also reshaping hardware choices, as forthcoming Clean Water Act updates for 2026 have driven monitoring providers toward non-phosphorus sensor technologies. Market structure continues to consolidate, highlighted by SGS completing its acquisition of Applied Technical Services in July 2025, expanding third-party validation capacity for aerospace and defense corrosion monitoring.

India: ZLD Enforcement and Infrastructure-Led Sensor Deployment

India’s corrosion monitoring industry is scaling alongside stricter environmental regulation and large-scale public infrastructure investment. Under the PM JI-VAN Yojana, the government allocated targeted grants in late 2025 to second-generation bio-refineries, encouraging the development of domestically manufactured corrosion and antiscalant monitoring probes. This localization push is strengthening India’s supply chain resilience while aligning monitoring hardware with the chemical complexity of bio-based industrial processes.

Regulatory enforcement is a decisive growth catalyst. In 2025, the Central Pollution Control Board tightened Zero Liquid Discharge mandates for textile and pharmaceutical clusters, sharply increasing demand for monitoring systems that remain accurate under high-TDS and high-calcium conditions typical of evaporation units. Infrastructure projects are also embedding monitoring at the design stage. The Chennai Metro Rail Phase II project incorporated specialized Migrating Corrosion Inhibitor sensors across nearly 119 kilometers of track to achieve a targeted 100-year structural service life. Governance reform is reinforcing data standardization. On August 29, 2025, the Ministry of Environment, Forest and Climate Change notified the Environment Audit Rules 2025, mandating third-party verification and standardized digital corrosion data reporting, effectively formalizing corrosion monitoring as a compliance instrument rather than a discretionary maintenance tool.

Germany: Hydrogen Transition and Secure Data Ecosystems

Germany’s corrosion monitoring landscape is being reshaped by the hydrogen economy, advanced materials research, and stringent data governance. During 2025–2026, the German Federal Ministry of Research funded multiple programs addressing hydrogen embrittlement risks in repurposed natural gas pipelines. These initiatives require specialized monitoring techniques capable of tracking corrosion and material degradation in high-moisture electrolyzer-linked environments, elevating demand for electrochemical and in situ chemical sensors.

At the innovation frontier, BASF Coatings disclosed at EUROCORR 2025 that machine learning models are being deployed to identify non-toxic, Cr(VI)-free inhibitor molecules. This data-driven chemistry discovery is closely linked with next-generation surface monitoring methods that validate inhibitor performance in real time. Data security has become equally critical. In late 2025, Intertek achieved TISAX Assessment Level 3 in Germany, enabling the secure handling of sensitive corrosion and materials performance data for automotive OEMs. This certification is increasingly a prerequisite as corrosion monitoring becomes embedded in proprietary vehicle platform design.

Saudi Arabia: Predictive Analytics for Energy and Desalination Assets

Saudi Arabia’s corrosion monitoring industry is advancing through targeted investment in predictive digital technologies and mandatory monitoring in water infrastructure. In 2025, Saudi Aramco Energy Ventures finalized a $5 million investment in CorrosionRADAR to scale predictive monitoring across upstream assets. The focus is on early detection of corrosion under insulation, a persistent challenge in high-temperature, high-humidity operating environments.

Water security initiatives are reinforcing monitoring demand. As desalination capacity expands, Saudi authorities have mandated the integration of Electrical Resistance and Linear Polarization Resistance monitoring systems in all new coastal desalination and cooling infrastructure by 2026. This requirement reflects the strategic importance of continuous corrosion intelligence in extending asset life under highly saline operating conditions.

China: Circular Materials and Industrial IoT Scaling

China’s corrosion monitoring industry is evolving in line with circular economy policies and large-scale industrial digitalization. In response to 2025 mandates requiring 20% recycled content in industrial assets, chemical hubs in Shanghai have pivoted toward producing VCI-integrated recycled resins embedded with corrosion sensors. This integration enables real-time monitoring while supporting recycled material adoption in storage, packaging, and structural components.

Digital infrastructure investment is accelerating deployment. Under the 2025 Industrial Digitalization Roadmap, the Ministry of Industry and Information Technology allocated more than $120 million to install IoT-enabled dosing and corrosion monitoring systems across the Yangtze River Delta manufacturing cluster. These systems are designed to reduce material degradation, minimize water blowdown, and improve lifecycle performance across heavy industry.

Comparative Snapshot: Country-Level Direction in the Corrosion Monitoring Industry

Corrosion Monitoring Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

Key Application Focus

|

Direction of Monitoring Evolution

|

|

United States

|

Aging infrastructure and EV standards

|

Pipelines, EV cooling, defense

|

AI-enabled, digital twin based monitoring

|

|

India

|

ZLD mandates and public infrastructure

|

Rail, textiles, pharmaceuticals

|

High-TDS stable, compliance-driven sensors

|

|

Germany

|

Hydrogen transition and data security

|

Pipelines, automotive systems

|

Hydrogen-compatible, secure data monitoring

|

|

Saudi Arabia

|

Energy asset protection and desalination

|

Upstream oil and water infrastructure

|

Predictive analytics and ER/LPR systems

|

|

China

|

Circular economy and industrial IoT

|

Manufacturing and industrial assets

|

Embedded sensors and large-scale IoT deployment

|

Corrosion Monitoring Market Report Scope

Corrosion Monitoring Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$917.5 Million

|

|

Market Size (2034)

|

$2253.5 Million

|

|

Market Growth Rate

|

10.5%

|

|

Segments

|

By Offering (Hardware, Software, Services), By Type (Intrusive Monitoring, Non-Intrusive Monitoring), By Technique (Corrosion Coupons, Electrical Resistance, Linear Polarization Resistance, Electrochemical Impedance Spectroscopy, Ultrasonic Thickness Measurement), By Application (Oil and Gas, Chemical and Petrochemical, Power Generation, Water and Wastewater Treatment, Infrastructure and Construction, Aerospace and Defense, Marine and Shipbuilding)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Emerson Electric Co., Baker Hughes Company, Honeywell International Inc., SGS S.A., Intertek Group plc, Cosasco Corporation, Bureau Veritas S.A., ALS Limited, Corrpro Companies Inc., Pepperl+Fuchs SE, Olympus Corporation, ClampOn AS, Rysco Corrosion Services, Mistras Group Inc., InduTech

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Corrosion Monitoring Market Segmentation

By Offering

- Hardware

- Software

- Services

By Type

- Intrusive Monitoring

- Non-Intrusive Monitoring

By Technique

- Corrosion Coupons

- Electrical Resistance

- Linear Polarization Resistance

- Electrochemical Impedance Spectroscopy

- Ultrasonic Thickness Measurement

By Application

- Oil and Gas

- Chemical and Petrochemical

- Power Generation

- Water and Wastewater Treatment

- Infrastructure and Construction

- Aerospace and Defense

- Marine and Shipbuilding

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Corrosion Monitoring Industry

- Emerson Electric Co.

- Baker Hughes Company

- Honeywell International Inc.

- SGS S.A.

- Intertek Group plc

- Cosasco Corporation

- Bureau Veritas S.A.

- ALS Limited

- Corrpro Companies Inc.

- Pepperl+Fuchs SE

- Olympus Corporation

- ClampOn AS

- Rysco Corrosion Services

- Mistras Group Inc.

- InduTech

*- List not Exhaustive