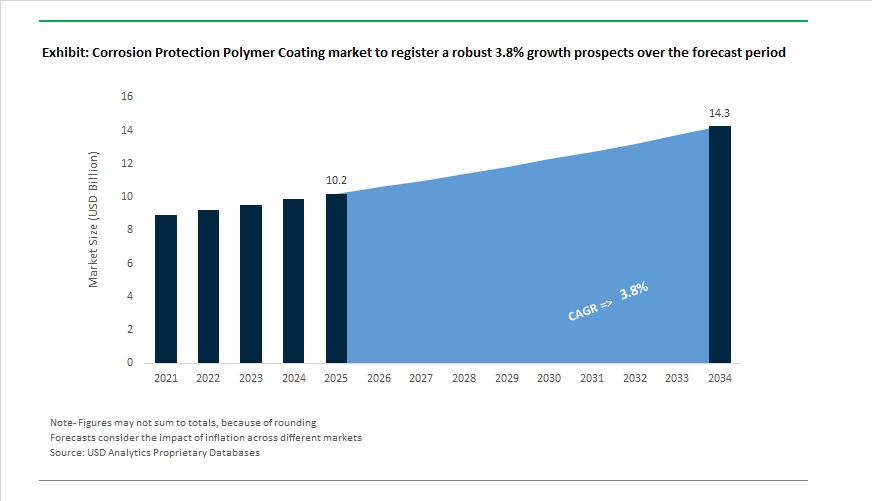

Corrosion Protection Polymer Coating Market Forecast 2025–2034: $10.2 Billion to $14.3 Billion at 3.8% CAGR Fueled by Offshore Wind, EV Batteries, and Sustainable Powder Technologies

The global Corrosion Protection Polymer Coating Market is projected to grow from $10.2 billion in 2025 to $14.3 billion by 2034, registering a CAGR of 3.8%. Market expansion is closely tied to long-life infrastructure coatings, offshore wind deployment, electric vehicle battery protection systems, aerospace chrome-free primers, and circular economy-driven powder coatings. High-performance epoxy primers, silicone fouling-release systems, fluoropolymer powders, zinc-rich protective coatings, and recycled polymer-based technologies are reshaping steel protection, marine coatings, coil coatings, and industrial corrosion prevention. Regulatory pressure around VOC reduction, PFAS elimination, chrome-free chemistry, and carbon footprint minimization is redefining formulation strategies across architectural, marine, energy, and transportation end markets.

Infrastructure repair and offshore wind applications gained momentum beginning in March 2024, when Sherwin-Williams launched Repacor™ SW-1000, engineered for wind turbine towers and offshore structures exposed to extreme humidity and salt spray. In January 2025, Hempel introduced Avantguard® 750 Pro, a zinc-rich epoxy primer featuring 76% solids and VOC levels of 244 g/L, engineered to deliver more than 35 years of structural corrosion protection for bridges, energy assets, and heavy industrial steel. In March 2025, Hempel strengthened its capital base by welcoming CVC Capital Partners as a strategic minority investor, channeling funding toward sustainable polymer technologies and energy infrastructure coatings. In April 2025, Sherwin-Williams Protective & Marine received the MP Corrosion Innovation of the Year Award for Heat-Flex® CUI-mitigation coatings designed to combat corrosion under insulation in refineries and petrochemical plants, addressing one of the most persistent industrial degradation modes.

Advanced powder coatings and EV battery polymer systems expanded technical boundaries in mid to late 2025. In June 2025, laboratory data confirmed that PPG Coraflon® Platinum FEVE fluoropolymer powder coatings demonstrated only 6% color loss after five years of extreme weathering, supporting their use as one-coat corrosion protection systems for architectural extrusions. During the same month, Jotun launched specialized powder coatings for electric vehicle battery packs, integrating electrical insulation, thermal management, and corrosion resistance to mitigate chemical degradation and thermal runaway risks in high-voltage systems. In September 2025, PPG introduced ENVIROLUXE™ powder coatings utilizing recycled industrial plastics in the polymer backbone, delivering PFAS-free circular corrosion protection solutions for appliances and transport sectors. Jotun also joined the EOLMED floating wind project in 2025, supplying marine-grade protective coatings engineered to withstand mechanical stress and severe salt-spray exposure on floating offshore wind foundations.

Strategic consolidation and digital curing ecosystems accelerated transformation in late 2025 and early 2026. In October 2025, AkzoNobel launched the IONOMY™ ecosystem to enable coil coaters to transition to renewable energy curing, addressing carbon reduction targets for corrosion-protected architectural metals in 2026 sustainability roadmaps. In December 2025, AkzoNobel and Axalta announced a merger of equals, combining marine, automotive, industrial polymer, and protective coatings expertise to prioritize sustainable corrosion protection R&D programs beginning in 2026. The same month, AkzoNobel expanded U.S. aerospace coatings production capacity, focusing on chrome-free primers and high-performance polymer topcoats designed for extreme atmospheric corrosion resistance and temperature cycling. In February 2026, Hempel completed the first round of Hempaguard NB silicone coating applications on new Maersk vessels, deploying low-friction hull protection technologies aimed at reducing biofouling, fuel consumption, and lifecycle corrosion from vessel commissioning onward.

Trends and Opportunities in the Global Corrosion Protection Polymer Coating Market

Accelerated Transition to 100% Solid and VOC-Compliant Coating Systems

- Regulatory mandates on volatile organic compound emissions and corporate sustainability commitments are rapidly accelerating the shift from solvent-borne coatings to 100% solid and solvent-free polymer systems. By mid-2025, industry assessments indicated that the transition to solvent-free polyurethane coatings alone could eliminate up to 775 metric tons of annual VOC emissions across major industrial manufacturing hubs. These next-generation polyurethane systems have closed the historical performance gap with solvent-based alternatives, achieving dry-to-touch times below 30 minutes while delivering higher film build per coat and improved edge retention.

- In parallel, epoxy resin innovation is increasingly focused on eliminating substances of very high concern and CMR-classified components without compromising mechanical strength or chemical resistance. Product launches showcased in 2025 highlighted CMR-free and SVHC-free epoxy systems formulated with bio-circular raw materials, enabling measurable reductions in carbon footprint while maintaining the high cross-link density required for primary containment, secondary bunds, and heavy-duty industrial flooring. For asset owners, these coatings reduce compliance risk, simplify worker safety protocols, and support ESG reporting without sacrificing corrosion protection performance.

Extreme-Resistance Coatings for Semiconductor and Battery Manufacturing Facilities

- The rapid build-out of semiconductor fabs and electric vehicle battery giga-factories is creating demand for polymer coatings capable of withstanding environments far more aggressive than conventional industrial settings. Exposure to ultra-pure chemical baths, acidic fumes, and high-humidity cleanroom conditions has rendered many standard coatings ineffective. By late 2025, PVDF-based fluoropolymer thermoplastic coatings had become the benchmark solution for fasteners and small components in these facilities. Their dip-spin application capability allows uniform coating of complex geometries while providing hydrophobic, chemically inert barriers resistant to corrosion from wet processing lines.

- In the electric vehicle battery sector, polymer-based dielectric coatings are gaining strategic importance as manufacturers seek to prevent galvanic corrosion between dissimilar metals within battery packs. Industry discussions in 2025 emphasized that these coatings must function simultaneously as corrosion barriers and electrical insulators, maintaining adhesion and dielectric strength under repeated thermal cycling associated with fast-charging regimes. This dual-performance requirement is reshaping material selection criteria and increasing the value of high-performance polymer formulations in advanced manufacturing ecosystems.

Specialized Polymer Linings for Hydrogen and CCUS Infrastructure

- The global hydrogen economy is emerging as a high-growth opportunity for corrosion protection polymer coatings due to hydrogen’s small molecular size, high diffusivity, and propensity to accelerate steel degradation mechanisms such as hydrogen-induced cold cracking. In response, pipeline operators are increasingly specifying multi-layer polymer coating systems engineered specifically for hydrogen and carbon capture service. Introduced in late 2025, dual-polymer white jacket systems combining polyethylene for corrosion resistance with polypropylene for mechanical robustness are designed to withstand the stresses of horizontal directional drilling while reducing hydrogen permeation and leakage risk.

- Hydrogen storage is reinforcing this trend. By mid-2025, Type 4 composite tanks rated up to 700 bar had become the preferred solution for heavy-duty fuel cell vehicles and aerospace applications. These tanks rely on internal polymer liners with ultra-low permeability to ensure long-term safety and compliance. Demand is rising for high-molecular-weight polymers that can maintain barrier integrity under extreme pressure and cyclic loading, creating a premium segment within the corrosion protection polymer coating market tied directly to hydrogen mobility and infrastructure investments.

Smart Self-Healing and Inspection-Ready Functional Coatings

- Advances in nanotechnology are opening a new frontier in corrosion protection through self-healing and inspection-ready polymer coatings. In early 2025, validation studies confirmed that smart epoxy coatings incorporating carbon nanotube-based nanocarriers could dramatically reduce corrosion progression after mechanical damage. These systems release encapsulated corrosion inhibitors such as zinc and sodium gluconate when micro-cracks or scratches occur, cutting corrosion rates by approximately 86% in saline and marine environments.

- The marine and offshore sectors are among the earliest adopters of these technologies. By 2025, autonomous self-repairing anti-corrosion coatings were being deployed at scale on ship hulls and offshore platforms, with operators reporting meaningful extensions in recoating intervals. In economic terms, increasing the time between major maintenance cycles by up to 40% translates into substantial reductions in dry-docking, subsea intervention, and downtime costs. As inspection and maintenance budgets come under pressure, self-healing polymer coatings are emerging as a strategic lever for lifecycle cost optimization rather than a niche innovation.

Corrosion Protection Polymer Coating Market Share and Segmentation Insights

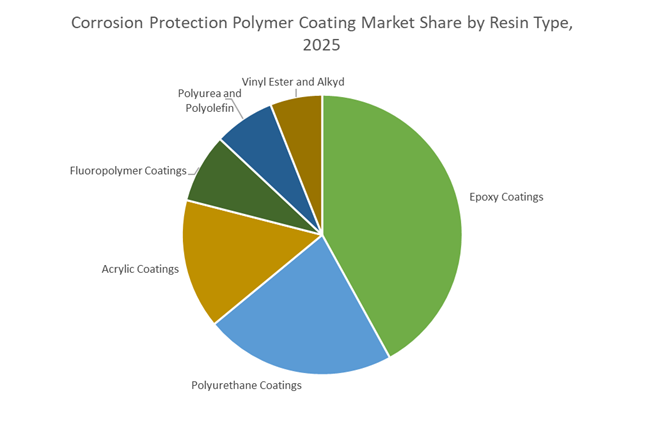

Resin Type Distribution: Epoxy Coatings Lead as High-Performance Systems Gain Share

Epoxy coatings command 42% market share in 2025, supported by exceptional adhesion, chemical resistance, and barrier performance in immersion service, buried pipelines, and industrial linings. They serve as the backbone of most corrosion protection systems, particularly as primers in multi-layer coating architectures. Polyurethane coatings form a major complementary segment, widely used as UV-resistant topcoats over epoxy to prevent chalking and color fade in exterior environments. Acrylic coatings provide cost-effective weatherability and fast drying for maintenance painting and moderate exposure conditions. Fluoropolymer coatings occupy a premium niche, offering outstanding chemical resistance and thermal stability for chemical processing equipment and architectural façades requiring decades-long color retention. Polyurea systems are gaining traction where rapid cure and fast return-to-service are critical, while vinyl ester and alkyd coatings address specialized chemical resistance and economical atmospheric protection needs across industrial facilities.

End-Use Industry Landscape: Oil and Gas Anchors Demand as Infrastructure Investment Expands

Oil and gas accounts for 32% of corrosion protection polymer coating consumption, driven by the need to safeguard pipelines, storage tanks, offshore platforms, and refineries against corrosive fluids, high temperatures, and marine exposure. Fusion-bonded epoxy and advanced multi-layer systems are widely specified for pipeline integrity. Infrastructure represents a growing segment, encompassing bridges, highways, water towers, and public utilities, where governments prioritize lifecycle extension and reduced maintenance costs. Marine applications demand robust coating stacks for hulls, ballast tanks, and offshore structures operating in continuous saltwater exposure. Industrial equipment manufacturers apply protective coatings to machinery, reactors, and material handling systems to ensure operational reliability. Automotive and transportation utilize coatings for chassis components and rail assets, balancing corrosion resistance with aesthetics. Aerospace and defense remain highly specialized, requiring rigorously qualified coating systems capable of withstanding extreme thermal cycles and operational stress.

Competitive Landscape of the Corrosion Protection Polymer Coating Market

The Corrosion Protection Polymer Coating Market is shaped by ESG-driven innovation, low-energy curing technologies, and multi-layer protection systems, with global leaders competing on durability, offshore compliance, and carbon-reduction performance across marine, infrastructure, and heavy industry.

AkzoNobel accelerates low-energy powder coatings and marine margin growth

AkzoNobel leads the corrosion protection polymer coating market through its International® marine portfolio and rapidly expanding powder coating technologies. In late 2025, AkzoNobel and Axalta announced an all-stock merger of equals, creating a coatings giant with unmatched global R&D scale. The launch of Interpon Reduz™ in early 2026 marked a major milestone, enabling significantly lower curing temperatures and cutting industrial energy consumption by up to 20%. The company reported a strong year of execution in February 2026, driven by profit margin expansion in its high-performance marine division. Strategically, AkzoNobel is targeting Zero-Carbon Footprint operations by 2030, integrating functional aesthetics like its 2026 “Rhythm of Blues” industrial color program.

PPG advances edge-protection technology for extreme corrosion environments

PPG Industries remains a titan in industrial corrosion protection coatings, leveraging deep vertical integration across automotive, aerospace, and infrastructure markets. Its ENVIROCRON® powder primers and HI-TEMP® coatings are widely specified for high-heat and chemically aggressive environments. In November 2025, PPG introduced a new high-edge powder coating that delivers superior corrosion resistance on sharp metal edges, traditionally one of manufacturing’s weakest protection points. Under its “Layer Without Limits” strategy, PPG combines pretreatment, electrocoat, and liquid or powder topcoats into unified substrate protection systems. The company invested $18.1 million in sustainability initiatives during 2025, reinforcing its ESG-aligned roadmap for next-generation polymer coatings.

Sherwin-Williams standardizes global specifications for harsh-service coatings

Sherwin-Williams dominates North America while rapidly scaling its Global Core portfolio to deliver standardized corrosion protection chemistry worldwide. In late 2025, the company acquired Gross & Perthun GmbH and Powdertech Oy Ltd., strengthening its European powder coating and industrial footprint. Its Macropoxy® 2600 and related systems are engineered to meet ISO 12944:2018 and NORSOK M501, making them pre-approved for offshore platforms and wastewater infrastructure. Sherwin-Williams is showcasing its full 2026 portfolio at EXPO-SURFACE, emphasizing multi-layer bridge and highway protection systems. A major differentiator is identical formulations across regions, simplifying specification for multinational EPC firms and accelerating project deployment.

Jotun pioneers next-generation offshore barrier technologies

Jotun sets the global benchmark for deep-sea corrosion protection, serving offshore energy, shipping, and renewable infrastructure. In 2026, the company introduced Next Generation Barrier Technologies with upgraded zinc-rich polymer systems that extend maintenance cycles of offshore wind and oil assets by 15–20%. Jotun is also supporting France’s EOLMED floating wind project with specialized anti-corrosion and anti-fouling coatings. Its Clean Shipping Commitment integrates Hull Skating Solutions to proactively clean vessel hulls, reducing fuel consumption and emissions. Recently verified by DNV, Jotun’s updated 2026 avoided-CO2 metrics confirm the measurable sustainability impact of its high-performance marine polymer coatings.

RPM International strengthens infrastructure coatings across Southeast Asia

RPM International operates a decentralized model anchored by corrosion specialists like Carboline and Rust-Oleum, delivering polymer coating solutions for critical infrastructure and fireproofing applications. Under its MAP 2025/2026 program, RPM is implementing a $100 million annual cost-optimization strategy while reinvesting in high-growth construction and industrial projects. In late 2025, RPM acquired a new manufacturing facility in Malaysia to serve Southeast Asia’s expanding infrastructure market. The company also declared its 52nd consecutive year of dividend increases in January 2026, highlighting financial stability that supports long-term R&D. RPM’s core strength lies in high-performance building solutions, where Carboline remains an industry standard for corrosion and fire protection.

United States: EV Thermal Protection, PFAS Exit, and Smart Infrastructure Scale-Up

The United States corrosion protection polymer coating industry is being reshaped by electrification, infrastructure renewal, and regulatory transition away from legacy chemistries. In September 2025, AkzoNobel introduced a high-heat-resistant polymer coating engineered specifically for eVTOL platforms and electric vehicle battery systems. This launch reflects the growing requirement for coatings that deliver both electrical insulation and thermal stability in compact, high-energy-density environments, particularly within urban air mobility and advanced EV architectures. At the macro level, infrastructure renewal is acting as a sustained demand engine. According to late-2025 updates from the U.S. Department of Transportation, global infrastructure spending is approaching $9 trillion annually, with the United States channeling significant capital toward transit corridors, water utilities, and asset-heavy public systems under the Infrastructure Investment and Jobs Act. These programs favor long-life polymer coatings capable of reducing maintenance cycles and lifecycle corrosion risk.

Regulatory and technology shifts are reinforcing formulation change. At FABTECH 2025, PPG debuted its ENVIROLUXE powder coatings, a PFAS-free polymer line incorporating recycled PET feedstock to align with the 2026 transition away from forever chemicals. Performance-driven innovation remains a differentiator. Sherwin-Williams received the 2025 MP Corrosion Innovation of the Year Award for its Heat-Flex CUI-mitigation coatings, which address corrosion under insulation in high-temperature industrial assets. Policy timing is also shaping market behavior. The U.S. Environmental Protection Agency extended national VOC compliance deadlines to January 2027, providing a critical window for accelerated adoption of waterborne and high-solids polymer systems. Workforce modernization is emerging as a parallel theme, highlighted by Mankiewicz inaugurating a U.S. training center in August 2025 dedicated to robotic coating application, targeting consistency gains and reduced overspray losses.

China: Offshore Energy, Battery Storage, and Municipal Water Protection

China’s corrosion protection polymer coating market is expanding through offshore wind deployment, energy storage infrastructure, and mandated municipal upgrades. In September 2025, Shanghai Electric launched two Ulstein-designed Service Operation Vessels for offshore wind farms, specifying advanced epoxy-polymer coatings to withstand C5-M marine corrosion exposure. Offshore oil and gas assets are also driving material innovation. In April 2025, PETRONAS commercialized ProShield+, a graphene-enhanced polymer coating developed with Chinese research partners to address persistent corrosion challenges in harsh offshore environments.

Battery storage expansion is creating a new application layer. Jotun finalized a 2025 partnership with leading Chinese battery manufacturers to supply powder coatings for large-scale Energy Storage Systems, emphasizing dielectric insulation and corrosion resistance for grid-scale renewable integration. Regulatory mandates are reinforcing polymer adoption in civil infrastructure. Under 2025 guidelines issued by the National Development and Reform Commission, all municipal wastewater upgrades must incorporate advanced polymer liners to prevent chemical erosion of concrete assets.

Germany: Ultra-Durability, Smart Polymers, and Circular Certification

Germany’s corrosion protection polymer coating industry is anchored in durability engineering, smart materials, and certified sustainability. In January 2025, Hempel introduced Avantguard 750 Pro, a zinc-rich polymer primer engineered to extend steel structure durability beyond 35 years. This product directly supports Germany’s bridge rehabilitation and transport asset renewal programs, where extended service life is a core procurement criterion. Innovation is also moving toward functional intelligence. Bayer highlighted advances in polyurethane-based self-healing coatings during 2025, enabling automated repair of micro-scratches in automotive surfaces and reducing the initiation points for sub-surface corrosion.

Sustainability verification is becoming a competitive requirement. In December 2025, PPG achieved REDCert² certification at its German production sites, validating the use of bio-based and sustainably sourced raw materials in industrial polymer coating lines. This certification strengthens alignment with Germany’s circular economy objectives and EU-level procurement standards, positioning certified polymer coatings as preferred solutions for public and industrial projects.

Norway and the Nordic Region: Biocide-Free Marine Efficiency and Rapid-Cure Topcoats

The Nordic corrosion protection polymer coating market is defined by marine efficiency and environmental performance. In mid-2025, Hempel launched Hempaguard Ultima, a biocide-free silicone-polymer system that delivers measurable fuel savings for cruise ships by minimizing biofouling drag while maintaining corrosion resistance. This technology aligns with stricter regional marine environmental standards and rising fuel efficiency targets. Complementing this, Jotun announced the global rollout of Hardtop XP II in September 2025, a polyester-based topcoat offering faster curing and higher initial hardness. Reduced downtime and accelerated maintenance cycles are key value drivers for offshore platforms and marine operators across the Nordic region.

Brazil: Food-Contact Safety and Bisphenol-Free Packaging Coatings

Brazil’s corrosion protection polymer coating industry is seeing targeted growth in food-contact and packaging applications. At Abralatas 2025 in São Paulo, AkzoNobel unveiled its Accelshield range, a BPAni polymer coating for beverage cans. This bisphenol-free formulation addresses anticipated 2026 regulatory shifts toward safer internal can coatings, particularly for acidic and carbonated beverages. Brazil’s role as a major beverage packaging hub positions such polymer innovations as strategically important for export-oriented can manufacturers seeking regulatory alignment across global markets.

Comparative Snapshot: Country-Level Strategic Positioning in the Corrosion Protection Polymer Coating Industry

Corrosion Protection Polymer Coating Market County Level Snapshot

|

Country / Region

|

Primary Strategic Driver

|

Key Application Focus

|

Direction of Polymer Coating Innovation

|

|

United States

|

Infrastructure renewal and electrification

|

EV batteries, transit, industrial assets

|

PFAS-free, CUI-resistant, automated application

|

|

China

|

Offshore wind and municipal upgrades

|

Offshore energy, ESS, wastewater

|

Graphene-enhanced, high-durability polymers

|

|

Germany

|

Asset longevity and circular economy

|

Bridges, automotive, steel structures

|

Ultra-durable, self-healing, certified coatings

|

|

Nordic Region

|

Marine efficiency and environmental rules

|

Shipping and offshore platforms

|

Biocide-free, fast-curing silicone systems

|

|

Brazil

|

Food safety regulation

|

Beverage packaging

|

Bisphenol-free internal polymer coatings

|

Corrosion Protection Polymer Coating Market Report Scope

Corrosion Protection Polymer Coating market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$10.2 Billion

|

|

Market Size (2034)

|

$14.3 Billion

|

|

Market Growth Rate

|

3.8%

|

|

Segments

|

By Resin Type (Epoxy Coatings, Polyurethane Coatings, Acrylic Coatings, Fluoropolymer Coatings, Polyurea and Polyolefin, Vinyl Ester and Alkyd), By Technology (Water-Borne, Solvent-Borne, Powder Coatings, High-Solids and UV-Curable), By Application Method (Electrostatic Spraying, Airless and Conventional Spray, Dip Coating and Autophoresis, Brush and Roller), By End-Use Industry (Oil and Gas, Marine, Infrastructure, Automotive and Transportation, Aerospace and Defense, Industrial Equipment)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

AkzoNobel N.V., PPG Industries Inc., The Sherwin-Williams Company, Jotun A.S., Hempel A.S., BASF SE, Axalta Coating Systems Ltd., Kansai Paint Co. Ltd., Nippon Paint Holdings Co. Ltd., RPM International Inc., Tnemec Company Inc., Mankiewicz Gebr. & Co., Indutron S.A., Berger Paints India Limited, Carboline Company

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Corrosion Protection Polymer Coating Market Segmentation

By Resin Type

- Epoxy Coatings

- Polyurethane Coatings

- Acrylic Coatings

- Fluoropolymer Coatings

- Polyurea and Polyolefin

- Vinyl Ester and Alkyd

By Technology

- Water-Borne

- Solvent-Borne

- Powder Coatings

- High-Solids and UV-Curable

By Application Method

- Electrostatic Spraying

- Airless and Conventional Spray

- Dip Coating and Autophoresis

- Brush and Roller

By End-Use Industry

- Oil and Gas

- Marine

- Infrastructure

- Automotive and Transportation

- Aerospace and Defense

- Industrial Equipment

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Corrosion Protection Polymer Coating Industry

- AkzoNobel N.V.

- PPG Industries Inc.

- The Sherwin-Williams Company

- Jotun A.S.

- Hempel A.S.

- BASF SE

- Axalta Coating Systems Ltd.

- Kansai Paint Co. Ltd.

- Nippon Paint Holdings Co. Ltd.

- RPM International Inc.

- Tnemec Company Inc.

- Mankiewicz Gebr. & Co.

- Indutron S.A.

- Berger Paints India Limited

- Carboline Company

*- List not Exhaustive