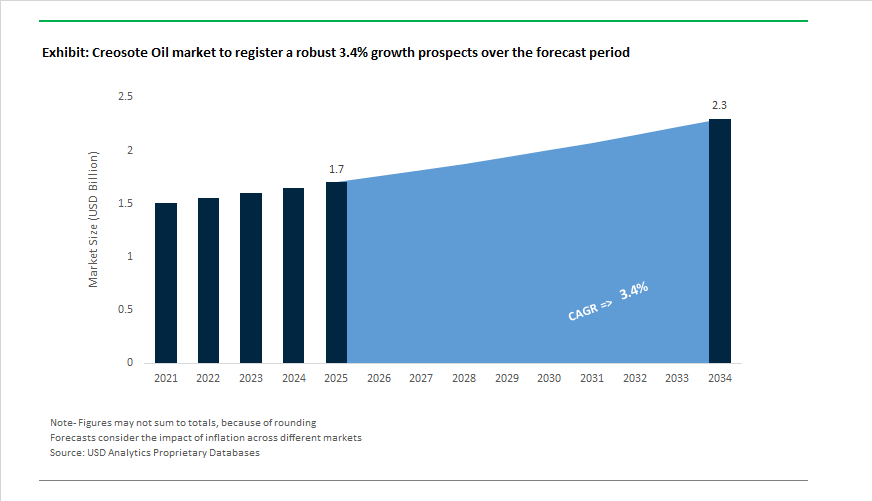

Creosote Oil Market Outlook 2025–2034: $1.7 Billion to $2.3 Billion at 3.4% CAGR Shaped by Utility Grid Expansion and Regulatory Transition

The global Creosote Oil Market is projected to expand from $1.7 billion in 2025 to $2.3 billion by 2034, registering a CAGR of 3.4%. Market performance remains closely linked to railway sleepers, utility poles, marine pilings, and industrial timber preservation, where coal-tar creosote remains a preferred wood preservative due to its deep penetration, long-term rot resistance, and performance under high-moisture conditions. Demand trends are increasingly influenced by regulatory scrutiny under biocidal product regulations, coal-tar feedstock price volatility, infrastructure grid modernization programs, and the emergence of bio-based wood creosote alternatives.

Operational efficiency and restructuring initiatives defined 2024 and early 2025. In May 2024, Koppers Inc. announced significant investment in automation across its creosote oil production and wood treatment facilities to improve distillation efficiency, maintain consistent tar fraction quality, and enhance worker safety through reduced exposure. During 2024, AI-based monitoring systems were implemented within creosote refining plants to optimize distillation curves in real time, reducing energy intensity in coal-tar processing. In September 2024, Arch Wood Protection partnered with a major North American railway operator to supply timber treated with advanced creosote formulations engineered to reduce environmental leaching while maintaining Class I rail performance standards. Stella-Jones reported record annual sales of $3.5 billion in 2024, though it noted shifts in competitive dynamics as certain railway customers moved tie-treatment operations in-house, affecting commercial treatment volumes entering 2025.

Regulatory adjustments and portfolio realignment influenced 2025 market dynamics. In February 2025, the UK Health and Safety Executive extended the approval expiry date for creosote (Product Type 8) under the GB Biocidal Products Regulation to March 31, 2026, providing a transition window for railway and utility stakeholders evaluating alternatives. In Q1 2025, Stella-Jones acquired Lockwell, marking entry into steel transmission structures and signaling strategic diversification beyond wood utility poles. In June 2025, Koppers discontinued phthalic anhydride production as part of its Catalyst transformation plan, reallocating resources toward refined tar, naphthalene, and creosote lines, which experienced volume growth in mid-2025. Throughout 2025, Koppers implemented global cost optimization measures under the Catalyst strategy, reducing its workforce by 11% between April 2024 and mid-2025 to offset rising coal-tar feedstock costs and stabilize profitability.

Infrastructure expansion and product evolution are shaping the 2026 outlook. Utility pole demand surged across North America during 2025–2026, with Stella-Jones projecting 15% growth in pole sales due to power grid modernization and large-scale replacement of aging wooden supports. Parallel to traditional infrastructure demand, pharmaceutical-grade wood-derived creosote saw increased research and niche adoption in 2024–2025 for antiseptic and expectorant applications. In January 2026, several manufacturers initiated pilot projects for bio-based wood tar-derived creosote alternatives designed to address toxicological concerns in residential and garden applications, reflecting mounting regulatory pressure on coal-tar derivatives. These developments highlight a market balancing legacy infrastructure reliance with operational efficiency improvements, regulatory transition management, and selective diversification into alternative materials and specialty derivatives.

Trends and Opportunities in the Global Creosote Oil Market

Regulatory-Driven Exit from Industrial Wood Preservation Applications

- Regulatory scrutiny around carcinogenicity and environmental persistence is rapidly accelerating the phase-out of creosote oil in industrial wood preservation. Under the REACH Annex XVII framework, rail and utility operators across the European Union are implementing mandatory transition timelines that restrict the continued use of creosote-treated wood. A notable milestone occurred in September 2025 when SNCF Réseau formally shifted production at its Bretenoux-Biars facility from creosote-treated sleepers to copper naphthenate-based alternatives, aligning with the EU objective to fully eliminate creosote-treated wood by 2029.

- Beyond regulatory compliance, the transition has delivered measurable operational benefits. The adoption of copper-based treatment oils reduced treatment temperatures from approximately 120 degrees Celsius to 60 degrees Celsius, resulting in a fourfold reduction in energy consumption and annual boiler water savings of roughly 3,000 cubic meters at the SNCF site. These metrics are now serving as benchmarks for other rail operators evaluating the total cost of ownership of alternative preservatives, reinforcing the long-term decline of creosote oil demand in traditional wood protection markets.

Repositioning Creosote Oil as a Critical Feedstock for Needle Coke and EV Anodes

- As legacy applications contract, creosote oil is being increasingly valorized as a high-aromatic feedstock for needle coke production, a critical material for ultra-high-power graphite electrodes and lithium-ion battery anodes. Coal tar streams rich in creosote fractions are gaining strategic importance as petroleum-based feedstocks face supply volatility and rising costs. In October 2025, POSCO Future M finalized a USD 470 million anode supply agreement, underpinned by vertically integrated coal tar distillation and synthetic graphite capacity exceeding 18,000 tons per year.

- Process optimization is further strengthening this trend. Technical studies published in August 2025 confirmed that polymer-modified needle coke derived from refined coal tar feedstocks can achieve full carbonization at approximately 1,200 degrees Celsius, compared with around 1,400 degrees Celsius for unmodified petroleum-based stocks. This reduction in calcination temperature materially lowers energy intensity, improving the economics of coal-derived carbon products at a time when industrial energy costs remain structurally elevated. As a result, creosote oil is increasingly viewed as a strategic input for energy transition materials rather than a declining by-product.

Feedstock Role in Sustainable Carbon Black and Circular Economy Models

- The global push toward sustainable materials is creating a new opportunity for creosote oil as a feedstock for recovered and low-emission carbon black. Tire manufacturers are actively reducing reliance on virgin fossil-based fillers as part of circular economy commitments. Leading producers such as Bridgestone and Michelin have publicly targeted the use of approximately 40% sustainable materials in tire production by 2030. Creosote oil, with polyaromatic content often exceeding 90 %, offers a consistent and high-performance feedstock for furnace carbon black processes requiring high tint strength and reinforcement, particularly for high-mileage electric vehicle tires.

- Strategic feedstock security is also shaping investment behavior. In September 2025, Epsilon Advanced Materials entered into a strategic agreement with Phillips 66 to secure needle coke and carbon-rich feedstocks. Such partnerships highlight a broader industry trend toward localized, high-purity aromatic supply chains that reduce exposure to crude oil price volatility and geopolitical risk.

High-Value Aromatic Monomers for Advanced Polymer and Specialty Chemical Synthesis

- Creosote oil’s complex polycyclic aromatic hydrocarbon composition is unlocking opportunities in specialty chemicals and advanced polymer synthesis. Fractions containing fluorene, acenaphthene, and naphthalene are increasingly used as precursors for heat-resistant resins and high-performance engineering plastics serving semiconductor, aerospace, and telecommunications applications. Reflecting this shift toward value-added aromatics, Reaxis announced the acquisition of TIB Chemicals AG in February 2025, aiming to expand capabilities in specialty metal salts and aromatic additives derived from coal tar streams.

- From an economic perspective, refining creosote oil into oxygen-containing aromatics such as dibenzofuran delivers a 20 to 30% cost advantage compared with fully synthetic petrochemical routes. These cost-efficient monomers are increasingly specified in high-performance polyimides and liquid crystal polymers required for 5G and emerging 6G infrastructure, where thermal stability and dielectric performance are non-negotiable. This positions creosote oil not as a sunset material, but as a transitional feedstock enabling advanced materials growth in regulated and technology-intensive markets.

Creosote Oil Market Share and Segmentation Insights

Type-Based Segmentation: Coal Tar Creosote Dominates While Heavy Fractions Support Industrial Longevity

Coal tar creosote accounts for 78% of global creosote oil consumption in 2025, reinforcing its position as the industry standard for industrial wood preservation. Derived from coal tar distillation, it offers powerful biocidal performance at relatively low cost, making it indispensable for railway sleepers, utility poles, and marine timbers. Heavy creosote oil represents a smaller but strategically important segment, favored for pressure-treated wood in harsh outdoor environments due to its higher boiling point, lower volatility, and long-term stability. Light creosote oil holds limited share, primarily serving as a processing intermediate or chemical recovery feedstock rather than a final preservative. Wood tar creosote remains a niche category, confined largely to pharmaceutical and traditional medicine applications where coal tar derivatives face restrictions. Despite increasing regulatory scrutiny in Europe and North America over PAH content, coal tar creosote continues to dominate critical infrastructure markets, supported by ongoing performance advantages.

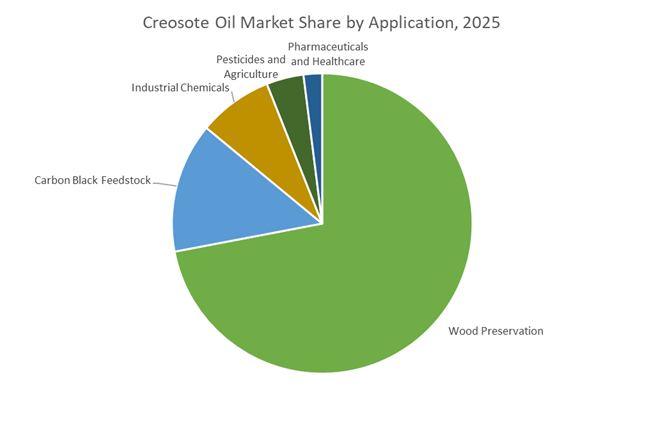

Application Landscape: Wood Preservation Anchors Demand as Carbon Black Feedstock Gains Importance

Wood preservation drives 72% of creosote oil demand, reflecting widespread use in extending the service life of railway ties, bridge timbers, marine pilings, and utility poles from years to decades by preventing fungal decay, insect attack, and marine borer damage. Carbon black feedstock represents the second-largest application, utilizing heavy creosote fractions as raw material for tire reinforcement, rubber goods, and printing inks. Industrial chemicals form another key segment, extracting aromatics such as naphthalene, anthracene, and phenanthrene for downstream plastics, dyes, and specialty chemical synthesis. Pesticides and agricultural applications continue to decline amid environmental regulation, while pharmaceuticals and healthcare remain the smallest segment, largely limited to wood tar creosote used in regional traditional medicine markets.

Competitive Landscape of the Creosote Oil Market

The Creosote Oil Market is highly consolidated and vertically integrated, driven by coal tar distillation capacity, railroad infrastructure demand, and long-term utility pole preservation contracts, with profitability closely tied to carbon materials pricing and regulatory compliance in wood preservation.

Koppers anchors the creosote oil value chain through coal tar distillation integration

Koppers Holdings Inc. is the dominant global leader in creosote oil production, operating a uniquely vertical model from coal tar distillation to pressure-treated railroad ties and utility poles. As one of the few producers that distills its own coal tar, Koppers converts output directly into high-purity creosote oil for in-house wood treatment, serving major Class I railroads. Its creosote-borate dual treatments extend tie lifespan in high-decay climates such as the Southeastern US. In late 2025 and early 2026, the company optimized its Carbon Materials and Chemicals segment, increasing refined tar and creosote volumes to offset carbon pitch volatility, targeting adjusted EBITDA of $250M–$270M.

Stella-Jones dominates North American railway tie distribution and utility pole markets

Stella-Jones Inc. operates as the largest North American pressure-treated wood provider and a major downstream consumer of creosote oil. With a strategic goal of achieving approximately $4 billion in annual sales by 2028, the company is focused on modernizing aging railway networks and the electrical grid between 2026 and 2028. Stella-Jones aims to maintain EBITDA margins of 17.5%–18.5%, supported by mid-single-digit growth in utility poles and railway ties. Implementation of a full-scale ERP system by end-2025 enhances treated wood inventory control and environmental compliance tracking. Its long-term contracts with major transit agencies secure a significant majority share of creosote-treated railway ties.

Rain Carbon leverages world-scale distillation for global carbon derivatives supply

Rain Carbon Inc. is one of the largest coal tar distillers globally, converting steel industry by-products into high-value creosote oils and carbon materials. The company produces heavy creosote oil and specialized impregnation oils used in graphite and refractory manufacturing, while serving as a primary supplier of Carbon Black Oil feedstock to tire manufacturers. Rain Carbon operates the world’s largest single-line coal tar distillation plant in Castrop-Rauxel, Germany, reinforcing its global supply hub status. Its Resourceful Waste-Heat Recovery innovation significantly lowers process carbon intensity, strengthening competitiveness in an increasingly sustainability-driven creosote oil market.

Himadri scales coal tar distillation to fund EV-focused new energy expansion

Himadri Speciality Chemical Ltd. has evolved from a domestic tar distiller into a global specialty chemicals and new energy materials player. Reporting a consolidated PAT of ₹192.20 crore in Q3 FY26, Himadri demonstrates strong operational momentum across creosote oil, pitch, and carbon black segments. The company is commissioning expanded coal tar pitch distillation capacity by Q1 FY27 through phased debottlenecking to meet India’s infrastructure surge. Strategically, it is reinvesting cash flows from creosote and carbon products into India’s first commercial LFP cathode plant, aligning with the EV revolution. Its EcoVadis Platinum Medal underscores rare sustainability leadership in coal tar chemistry.

Epsilon Carbon expands multistage distillation with energy-independent operations

Epsilon Carbon is emerging as a competitive challenger in the global creosote oil market through its multistage distillation expertise. Its proprietary EPSOTETM blend of wash oil and dense creosote oil claims wood preservation durability of up to 100 years, appealing to long-life infrastructure projects. The company plans to invest ₹2,000 crores through 2030 in specialty carbon initiatives, including the 300,000 MTPA Ashoka Project coal tar distillation facility in Odisha. Epsilon is also developing a 45 MW captive power plant using tail gas from carbon black operations, positioning its Vijayanagar complex as nearly energy independent by 2026, strengthening cost competitiveness.

United States: Infrastructure-Led Stability and Carbon Feedstock Reorientation

The United States creosote oil industry in 2025 is characterized by operational consolidation, regulatory tightening, and sustained infrastructure-linked demand. Koppers Inc., under its parent Koppers Holdings Inc., advanced its multi-year Catalyst transformation program in late 2025. The initiative targets more than $40 million in operational benefits by 2026 through plant rationalization, procurement optimization, and improved yield efficiency in coal tar distillates used for creosote blending. This restructuring reflects a shift away from volume-driven growth toward margin stability and disciplined asset utilization in a mature preservatives market.

Downstream consolidation is reinforcing long-term demand visibility. In September 2025, Stella-Jones Inc. acquired Brooks Manufacturing Co. for approximately $140 million, securing backward integration in creosote-treated utility poles and reinforcing its strategic position in North American power transmission infrastructure. Railway maintenance cycles remain a core demand anchor. Class I railroads reported stable consumption of creosote-treated crossties through 2025, with consistent maintenance-of-way capital expenditure despite broader macroeconomic moderation. Regulatory oversight has intensified in parallel. The U.S. Environmental Protection Agency issued multiple Clean Water Act consent agreements in July 2025, enforcing stricter Spill Prevention, Control, and Countermeasure compliance for creosote storage and handling facilities. Standards governance has also evolved, with the American Wood Protection Association updating P1 and P13 specifications in 2025 to introduce more rigorous PAH testing aligned with state-level environmental scrutiny. Strategically, U.S. producers are reallocating R&D budgets toward high-purity carbon pitch and refined tar, positioning creosote oil as a critical intermediate feedstock for aluminum smelting and graphite electrode applications.

India: Export Momentum and Integrated Carbon Value Chains

India’s creosote oil industry is transitioning from domestic infrastructure reliance toward export-oriented carbon materials integration. In December 2025, Himadri Speciality Chemical Ltd. completed a landmark export of 3,600 tonnes of liquid coal tar pitch and specialty oils to the Middle East. This shipment marked a strategic inflection point, signaling India’s growing role as a supplier of creosote-derived intermediates to global industrial hubs. Capacity expansion is reinforcing this trajectory. Epsilon Carbon commissioned the second phase of its Vijayanagar facility in June 2025, adding 100,000 tpa of capacity that integrates creosote-derived feedstocks to produce advanced N134 grade carbon black for high-performance tire applications.

Sustainability and policy alignment are becoming central to competitiveness. In August 2025, Himadri Speciality Chemical Ltd. secured ISCC PLUS certification, validating its transition toward circular economy principles in coal tar distillation and derivative processing. Regulatory modernization is stabilizing upstream feedstock access. The Oilfields Regulation and Development Amendment Act, 2025 streamlined licensing for coal bed methane and mineral oils, indirectly supporting consistent raw material availability for coal tar distillers. Infrastructure-linked demand remains resilient. The Ministry of Railways’ 2025–2026 budget increased allocations for wooden sleeper replacement in heavy-haul corridors, where creosote-treated timber continues to outperform concrete alternatives due to superior vibration damping and lifecycle economics.

European Union: Controlled Authorization and Chemical Value Uplift

The European creosote oil market in 2025 reflects a tightly regulated equilibrium between restriction and essential-use preservation. Following evaluation under the EU Biocidal Products Regulation, creosote CAS 8001-58-9 received renewed authorization for Product Type 8 wood preservatives until October 31, 2029. This decision provides regulatory certainty for critical applications while reinforcing the EU’s precautionary stance. Effective mid-2025, the Union implemented stricter prohibitions on non-critical uses such as agricultural stakes and equestrian fencing, while explicitly safeguarding creosote use in railway sleepers and utility poles where no technically equivalent alternatives exist at scale.

Germany is emerging as a focal point for feedstock repositioning. In 2025, R&D initiatives led by BASF and Rütgers explored the conversion of coal tar distillates into higher-value specialty chemicals aligned with hydrogen economy applications. These projects aim to reduce the volume of creosote burned as low-value fuel and instead channel it into advanced chemical intermediates, improving carbon efficiency and regulatory acceptability. Northern European markets are therefore redefining creosote oil not as a declining preservative commodity, but as a strategically managed carbon resource within a constrained yet stable regulatory envelope.

Comparative Summary: Country-Level Strategic Positioning in the Creosote Oil Industry

Creosote Oil Market County Level Snapshot

|

Country

|

Primary Demand Anchor

|

Regulatory Direction

|

Strategic Industry Focus

|

|

United States

|

Railways and utility poles

|

Stricter CWA and PAH oversight

|

Operational consolidation and carbon feedstocks

|

|

India

|

Rail infrastructure and exports

|

Liberalized feedstock licensing

|

Integrated carbon materials and global exports

|

|

European Union

|

Essential-use wood preservation

|

Restricted but renewed authorization

|

Specialty chemical valorization of coal tar

|

Creosote Oil Market Report Scope

Creosote Oil market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.7 Billion

|

|

Market Size (2034)

|

$2.3 Billion

|

|

Market Growth Rate

|

3.4%

|

|

Segments

|

By Type (Light Creosote Oil, Heavy Creosote Oil, Coal Tar Creosote, Wood Tar Creosote), By Source (Coal Tar Distillation, Wood Pyrolysis, Synthetic Tar), By Application (Wood Preservation, Carbon Black Feedstock, Industrial Chemicals, Pharmaceuticals and Healthcare, Pesticides and Agriculture), By End-Use Industry (Transportation, Utilities, Construction and Infrastructure, Manufacturing, Healthcare and Life Sciences)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Koppers Holdings Inc., Stella-Jones Inc., Himadri Speciality Chemical Ltd., Epsilon Carbon Pvt. Ltd., Rain Carbon Inc., SGL Carbon SE, ArcelorMittal S.A., JFE Chemical Corporation, Baowu Carbon Technology Co., Ltd., Konark Tar Products Pvt. Ltd., Bilbaína de Alquitranes, S.A., Sandvik AB, Cooper Creek Chemical Corporation, AVH Polychem Pvt. Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Creosote Oil Market Segmentation

By Type

- Light Creosote Oil

- Heavy Creosote Oil

- Coal Tar Creosote

- Wood Tar Creosote

By Source

- Coal Tar Distillation

- Wood Pyrolysis

- Synthetic Tar

By Application

- Wood Preservation

- Carbon Black Feedstock

- Industrial Chemicals

- Pharmaceuticals and Healthcare

- Pesticides and Agriculture

By End-Use Industry

- Transportation

- Utilities

- Construction and Infrastructure

- Manufacturing

- Healthcare and Life Sciences

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Creosote Oil Industry

- Koppers Holdings Inc.

- Stella-Jones Inc.

- Himadri Speciality Chemical Ltd.

- Epsilon Carbon Pvt. Ltd.

- Rain Carbon Inc.

- SGL Carbon SE

- ArcelorMittal S.A.

- JFE Chemical Corporation

- Baowu Carbon Technology Co., Ltd.

- Konark Tar Products Pvt. Ltd.

- Bilbaína de Alquitranes, S.A.

- Sandvik AB

- Cooper Creek Chemical Corporation

- AVH Polychem Pvt. Ltd.

*- List not Exhaustive