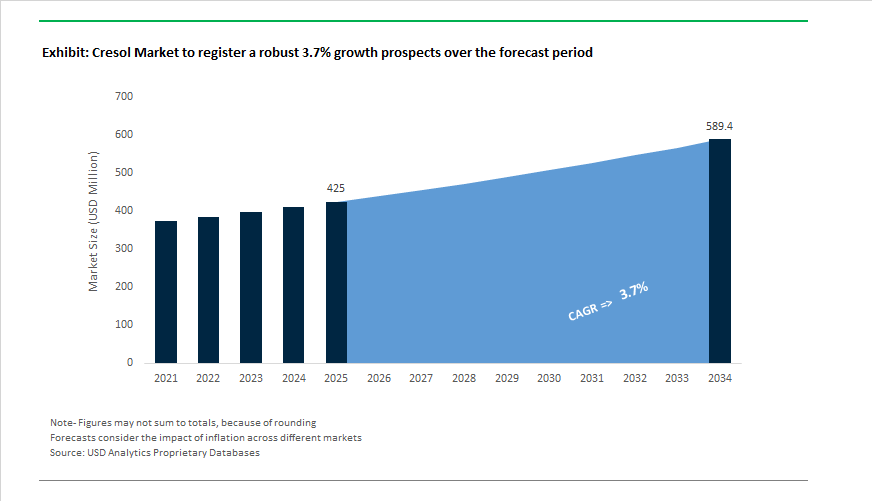

Cresol Market Outlook 2025–2034: $425 Million to $589.4 Million at 3.7% CAGR Driven by Specialty Intermediates, Vitamin E Demand, and Electronics Applications

The global Cresol Market is projected to expand from $425 Million in 2025 to $589.4 Million by 2034, registering a CAGR of 3.7%. Cresols including ortho-cresol, meta-cresol, and para-cresol remain critical phenolic intermediates used in agrochemicals, antioxidants, epoxy resins, polycarbonate modifiers, vitamin E synthesis, flavors and fragrances, and semiconductor-grade specialty chemicals. Market growth is influenced by restructuring within major petrochemical producers, increasing demand for synthetic Vitamin E in animal nutrition, expansion of high-purity cresol for electronics manufacturing, and gradual movement toward bio-based cresol derivatives for consumer-facing applications.

Supply chain optimization and production realignment defined 2024 and early 2025. In March 2024, Standard Industries and W. R. Grace & Co. launched a global AI chemical innovation challenge targeting more efficient synthesis pathways for para-cresol-based antioxidants and resin intermediates. In September 2024, Agilis partnered with Evonik to introduce the AI-driven Alchemist digital commerce suite, enhancing procurement transparency and technical data access for phenolic compounds such as cresols. During 2024, Atul Ltd. introduced bio-based cresol derivatives engineered for flavors, fragrances, and personal care markets, responding to demand for renewable phenolic ingredients. In late 2024, RÜTGERS Group shifted production focus toward ortho-cresol at European facilities to meet growing demand from synthetic Vitamin E manufacturers, a key driver in global feed additive and nutraceutical supply chains. In the same year, Nanjing Datang Chemical completed capacity expansion for high-purity cresol isomers targeting China’s semiconductor and photoresist manufacturing sector.

Corporate restructuring and operational volatility shaped 2025 market dynamics. In April 2025, LANXESS completed the divestment of its Urethane Systems business to UBE Corporation, reinforcing its strategy to prioritize Advanced Intermediates, including cresol and phenolic derivatives. In September 2025, Sasol reported operational challenges at its Secunda facility linked to coal quality issues, resulting in reduced output of cresylic acid feedstock and prompting stabilization measures within its chemicals segment. In October 2025, Sumitomo Chemical restructured its U.S. agro and life solutions operations to establish a Global Hub for Biorational Business, streamlining cresol-based agrochemical supply chains. LANXESS implemented its FORWARD! cost-saving plan throughout 2025, targeting €150 million in annual savings and announcing further network optimizations in November 2025 to address price pressure from Asian imports in the cresol intermediates market.

Strategic portfolio shifts and sustainability initiatives intensified entering 2026. SABIC transitioned its Cartagena polycarbonate site to 100% renewable power during 2024, supporting the production of cresol-derived monomers within certified circular polymer programs. In January 2026, SABIC announced the divestment of its European Petrochemical business to AEQUITA, aligning with its focus on higher-value specialty and circular materials rather than base commodity chemicals. These developments reflect an evolving cresol market increasingly shaped by specialty chemical positioning, vitamin E precursor demand, high-purity electronics applications, bio-based derivative expansion, AI-enabled synthesis optimization, and portfolio rationalization among global producers.

Trends and Opportunities in the Global Cresol Market

Rising Strategic Importance of Para-Cresol in Polymer Antioxidant Systems

- Demand for para-cresol is accelerating as high-performance plastics consumption expands across electric vehicles, medical devices, and advanced packaging. Para-cresol is a key precursor for hindered phenolic antioxidants such as Butylated Hydroxytoluene, which are essential for preventing oxidative and thermal degradation in polyethylene and polypropylene during processing and long service lifetimes. Despite cyclical pressure across the broader chemical sector, stabilizer demand has remained structurally resilient due to its non-discretionary role in polymer integrity.

- In November 2025, LANXESS reported that its Consumer Protection segment maintained an EBITDA margin of 15.9 %, up from 13.6% year on year, underscoring the pricing power and demand stability of antioxidant-related product lines. This resilience is directly linked to para-cresol-derived stabilizers embedded in automotive-grade polymers and medical plastics where failure risks are unacceptable. Reflecting long-term confidence in these applications, SABIC confirmed in late 2025 its strategic objective to expand overall chemical production capacity by 70 %, with para-cresol derivatives playing a role in supporting AO-1135 and other advanced antioxidant formulations used across U.S. shale-linked manufacturing clusters and Asian polymer processing hubs.

Regulatory Contraction of Meta-Cresol in Agrochemical Synthesis

- In contrast to para-cresol, meta-cresol is facing a structural decline as regulatory scrutiny tightens around toxicological and environmental persistence risks. European agrochemical policy has become a decisive factor shaping cresol isomer demand. In May 2025, the European Commission issued Implementing Regulation (EU) 2025/910, reinforcing a regulatory environment that tolerates maximum residue levels as low as 0.01 milligrams per kilogram for substances with endocrine-disrupting potential. Although the regulation primarily targets specific herbicide actives, its downstream impact is accelerating the phase-out of meta-cresol-based synthesis routes for products such as MCPA.

- Regulatory pressure is not limited to Europe. In September 2025, the United States Environmental Protection Agency expanded its Aquatic Life Benchmarks program to cover 782 chemicals, intensifying risk assessments for phenolic intermediates. This has prompted agrochemical majors to reformulate portfolios toward newer herbicide and antimicrobial classes that do not rely on cresol intermediates. As a result, the traditional agrochemical demand base for meta-cresol is eroding, reinforcing a shift in capacity utilization toward higher-value cresol isomers.

Commercial Scale-Up of Bio-Based and Lignin-Derived Cresols

- One of the most transformative opportunities in the cresol market lies in the commercialization of bio-based production pathways that decouple aromatic chemicals from fossil and coal-tar feedstocks. In December 2025, UPM announced the start of operations at its €1.275 billion Leuna biorefinery in Germany. The facility is designed to produce 220,000 tonnes per year of biochemicals from sustainably sourced hardwood, including lignin-derived aromatic intermediates that can serve as renewable alternatives to conventional cresols.

- Scientific progress is reinforcing this industrial momentum. Research presented at the Lignin Workshop 2025 hosted by Åbo Akademi demonstrated that photoelectrochemical processes can selectively cleave carbon oxygen and carbon carbon bonds in lignin under mild reaction conditions. These advances enable higher-yield production of bio-phenolics, allowing downstream users to achieve carbon dioxide footprint reductions of up to 90% compared with coal-tar-based cresol production. For consumer-facing brands and electronics manufacturers facing Scope 3 emissions targets, bio-based cresols represent a strategic sourcing advantage rather than a niche sustainability play.

Premium Demand for High-Purity Ortho-Cresol in Electronic-Grade Resins

- The semiconductor and advanced electronics sectors are creating a premium, high-margin market for ultra-high-purity ortho-cresol used in cresol novolac epoxy and phenolic resins. These materials are essential for encapsulation, printed circuit board laminates, and wafer-level packaging where ionic contamination and residual phenol content can directly impact device reliability. In 2025, Shengquan Group published technical specifications for electronic-grade phenolic resins derived from high-purity ortho-cresol, highlighting residual phenol levels below 200 parts per million and extremely low sodium, potassium, and chloride ion concentrations.

- This demand is being reinforced by the rise of artificial intelligence-driven microprocessors and high-density chip architectures. Research published in 2025 by MDPI confirmed that cresol novolac epoxy resins provide dielectric stability and thermal resistance exceeding 160 degrees Celsius, making them suitable for high-vacuum semiconductor environments operating above 105 degrees Celsius. For resin producers, electronic-grade ortho-cresol offers significantly higher margins than industrial phenolics, supported by strict REACH and RoHS compliance requirements and the semiconductor industry’s low tolerance for material failure.

Cresol Market Share and Segmentation Insights

Product Type Distribution: Meta-Cresol Leads Intermediates While Para and Ortho Support Specialty Chemistry

Meta-cresol commands 42% of cresol market share in 2025, driven by its central role in producing pyrethroid insecticides, vitamin E, antioxidants, and specialty resins where precise methyl positioning enables targeted synthesis. Para-cresol follows as the second-largest segment, supported by demand for butylated hydroxytoluene (BHT) used in fuels, rubber, and food preservation, alongside fragrance intermediates such as anisaldehyde and thymol. Ortho-cresol maintains steady consumption as a precursor for herbicide intermediates including MCPA and mecoprop, as well as phenolic resins used in foundry binders and wire enamels. Cresylic acid, a mixed-isomer stream, represents the smallest value segment but significant volume contributor, supplying lower-purity applications such as phosphate esters, ore flotation reagents, and industrial cleaning formulations where isomer specificity is not critical.

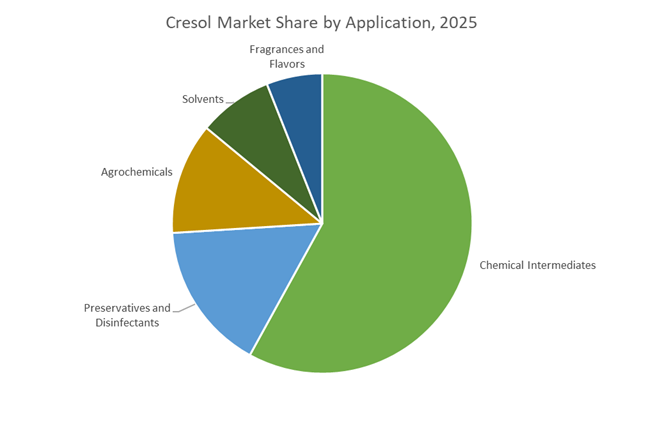

Application Segmentation: Chemical Intermediates Dominate While Agrochemicals and Disinfectants Sustain Volume

Chemical intermediates account for 58% of cresol demand, converting cresol isomers into antioxidants, vitamin E, epoxy resins, and polymer additives used across plastics, lubricants, rubber, and food packaging. Preservatives and disinfectants form a substantial secondary segment, leveraging cresol’s biocidal properties in industrial preservatives, metalworking fluids, and veterinary sanitation products. Agrochemicals remain strategically important, with cresols serving as core building blocks for phenoxy herbicides used in cereal crops and turf management. Solvent applications utilize cresols for dissolving resins and oils in paint stripping and industrial cleaning processes. Fragrances and flavors represent the smallest but highest-value segment, where high-purity cresol derivatives are transformed into aroma compounds such as thymol and carvacrol, supplying premium perfumery, food flavoring, and essential oil formulations.

Competitive Landscape of the Cresol Market

The Cresol Market is characterized by high integration across petrochemical, coal-tar, and specialty chemical value chains, with leading producers competing on isomer purity, downstream derivative integration, and sustainability performance in aroma chemicals, antioxidants, agrochemicals, and advanced electronics resins.

LANXESS strengthens European leadership with high-purity synthetic cresols

LANXESS AG holds an estimated 18% global cresol market share in 2026, positioning it as a dominant force in synthetic meta-cresol and ortho-cresol production. Its high-purity cresols serve as critical intermediates for flavorings, fragrances, vitamin E synthesis, and disinfectant formulations. In late 2025, LANXESS optimized its Consumer Protection segment to emphasize cresol-based preservatives aligned with tightening EU biocidal regulations. The company leverages its Leverkusen production hub, which underwent a digital upgrade in 2025, boosting output efficiency by 12%. With vertical integration into aroma chemicals and agrochemicals, LANXESS ensures stable internal demand while advancing its Climate Neutral 2040 decarbonization roadmap.

Sasol expands tar-derived cresol supply through Secunda output growth

Sasol Limited commands approximately 14% of the global cresol market, primarily supplying tar-derived cresols from its coal-to-liquids and gas-to-liquids complexes. In February 2026, Sasol reported a 10% production increase at its Secunda Operations, expanding cresol feedstock availability for export markets. A major supplier of para-cresol for BHT antioxidant manufacturing, Sasol plays a critical role in food stabilization and fuel preservation industries. In early 2026, the company secured 300 MW of renewable energy to power distillation units, enhancing the sustainability profile of its cresol portfolio. Its closed-loop integration maximizes feedstock value and strengthens global supply reliability.

SABIC integrates cresol chemistry into EV and specialty resin growth

SABIC leverages petrochemical scale to drive high-volume synthetic cresol production, tightly integrated with Saudi Aramco’s feedstock base. In February 2026, SABIC signed a raw material supply agreement supporting regional tire manufacturing, where cresol-derived resins function as rubber tackifiers. The company emphasizes ortho-cresol for polyphenylene oxide resins, essential for EV battery housings and electronics components. Under its Transformation 2024–2026 strategy, SABIC is shifting toward specialty chemicals, elevating cresol-based intermediates for medical and advanced material applications showcased at MD&M West 2026. Its low-cost feedstock access and global logistics infrastructure ensure stable cresol supply across Asia-Pacific and Europe.

Mitsui Chemicals advances ultra-pure cresols for ICT and LCP applications

Mitsui Chemicals, through its majority stake in Honshu Chemical Industry, dominates high-purity cresols for electronics and ICT markets. In early 2026, the group filed patents for advanced phenol compound crystallization techniques, enhancing cresol purity levels above 99.5% for liquid crystal polymers and specialty epoxy resins. These materials are vital for smartphone circuit boards and 5G infrastructure components. Mitsui’s Bio & Circular initiative, launched in January 2026, introduces bio-attributed cresols through mass-balance accounting. With strong technical expertise in isomeric separation, the company supports pharmaceutical-grade meta-cresol production for precision chemical synthesis.

Atul capitalizes on China Plus One strategy in aromatic derivatives

Atul Ltd. has emerged as a key cresol producer benefiting from global supply chain diversification. A leading manufacturer of para-cresol and derivatives such as para-cresidine and p-anisaldehyde, Atul supplies dyes, fragrances, and agrochemical intermediates worldwide. In 2025, its Aromatics division reported strong export-driven growth across Europe and North America. Strategically, the company is moving downstream into value-added cresol derivatives rather than competing solely in bulk markets. Supported by a cost-competitive manufacturing base and green chemistry-focused R&D, Atul is reducing effluent discharge while strengthening its role in pharmaceutical and crop protection supply chains.

Sumitomo Chemical integrates cresol intermediates into agro and semiconductor growth

Sumitomo Chemical utilizes cresols as essential precursors for agrochemicals and advanced semiconductor materials. In February 2026, the company revised its FY2025/2026 forecast upward, citing a 3.1% rise in core operating income driven by semiconductor material demand. Its ICT & Mobility Solutions segment was realigned in 2026 to prioritize cresol-based photoresist materials for advanced node chip manufacturing. Additionally, Sumitomo is a global agrochemical leader, incorporating cresol intermediates into proprietary herbicide and insecticide formulations. Deep integration from monomers to finished crop protection products enables strong R&D synergies across chemical and life science divisions.

South Africa: Feedstock Stability and Margin-Led Chemical Upgrading

South Africa remains structurally critical to the global cresol industry due to its coal-to-chemicals backbone. In August 2025, Sasol Limited confirmed that restoration initiatives at its Secunda Operations are progressing in line with expectations. Secunda is one of the world’s most important sources of coal-gasification-derived cresylic acids, and the stabilization of output is essential for balancing global supply, particularly for downstream meta-cresol and para-cresol consumers in pharmaceuticals, antioxidants, and resins. Any disruption at this node historically translates into global price volatility, making operational reliability a strategic rather than purely operational priority.

Energy resilience has emerged as a parallel competitiveness lever. Sasol’s Damlaagte solar PV plant, commissioned in August 2025 with 97.5 MW capacity, marks a tangible step toward its 2 GW renewable energy target by 2030. This transition directly lowers the carbon intensity of energy-intensive cresol distillation and separation processes. From a profitability standpoint, Sasol’s May 2025 Capital Markets Day outlined a focused roadmap to lift margins in its International Chemicals segment by 2028 through a pivot toward higher-value cresol derivatives rather than commoditized fractions. The reported FY25 adjusted EBITDA uplift of more than $120 million in international chemicals strengthens funding visibility for 2026 investments in high-purity m-cresol and p-cresol separation technologies, reinforcing South Africa’s role as a global upstream anchor rather than a volume-only supplier.

India: Pharmaceutical Pull and Sustainability Certification Momentum

India’s cresol industry is increasingly shaped by specialty demand and downstream integration. Atul Ltd continued to scale the benefits of its para-cresol expansion through 2025, leveraging an integrated supply chain to serve fragrance-grade and pharmaceutical-grade requirements. Domestic demand is being structurally reinforced by India’s growing role in global pharmaceutical synthesis, where cresol purity and supply consistency are critical.

A key structural driver is India’s emergence as a consumption hub for m-cresol in synthetic Vitamin E production. Global players such as Zhejiang Medicine and DSM increasingly rely on Indian-sourced intermediates for the 2,4,6-Trimethylphenol route, embedding India deeper into global nutraceutical value chains. Policy support is reinforcing this trajectory. The 2025–2026 Make in India chemical initiatives have accelerated localized agrochemical manufacturing, boosting cresol derivative usage in low-toxicity pyrethroid insecticides. Sustainability credentials are becoming a market qualifier. In August 2025, Himadri Speciality Chemical secured ISCC PLUS certification, signaling a broader domestic push to certify coal-tar-derived intermediates, including cresylic acids, for export-facing and regulated end markets.

China: Capacity Rationalization and Export Quality Shift

China’s cresol market in 2025 reflects a dual dynamic of protectionism and structural overcapacity. The Ministry of Commerce of China continued anti-dumping oversight on cresol imports from the U.S., EU, and Japan, maintaining duties to shield domestic producers such as Anhui Haihua Chemical Technology Group, which operates at approximately 8,000 tpa capacity. This policy stance has preserved domestic utilization rates but has not fully offset broader demand softness.

Downstream integration is emerging as a partial counterbalance. In November 2025, SABIC confirmed that its Fujian Petrochemical Complex remains on schedule, integrating high-performance polymer units that consume cresol-based antioxidants and resin intermediates. However, persistent overcapacity has weighed on pricing. Reports from September 2025 indicate a declining O-cresol price index within China, prompting producers to pivot toward higher-purity m/p-cresol exports rather than competing in saturated domestic segments. Regulatory pressure is also reshaping production economics. China’s 2025 Industrial Digitalization Roadmap mandates AI-optimized molecular design and process control, targeting a 10% reduction in environmental footprint at cresol distillation facilities by 2030. This effectively favors technologically advanced producers and accelerates consolidation.

United States: Rubber Additives and Cost-Driven Volatility

The U.S. cresol market is being reshaped by downstream specialization and macro-driven cost pressures. In September 2025, LANXESS announced the expansion of its Bushy Park facility in South Carolina, introducing domestic production of cresol-based rubber processing promoters such as Aktiplast®. This move strengthens supply security for the North American tire and industrial rubber sector while reducing reliance on imports.

At the same time, pricing dynamics remain sensitive to broader chemical inflation. During Q3 2025, the U.S. O-cresol price index rose in response to a 3.0% CPI increase and higher phenol and methanol feedstock costs linked to refinery turnarounds and regional supply tightness. Beyond rubber, microbial control applications are gaining prominence. Following its acquisition of IFF’s microbial control business, LANXESS expanded U.S. production of cresol-based biocides in 2025, targeting industrial water treatment and consumer hygiene formulations. This diversification supports demand resilience even as cyclical sectors fluctuate.

Germany: Cost Discipline and Low-Carbon Intermediate Leadership

Germany’s cresol industry is increasingly defined by cost optimization and regulatory alignment. LANXESS advanced its FORWARD! action plan through 2025, targeting permanent annual savings of €150 million by year-end, with an additional €100 million of optimization measures scheduled for early 2026. These initiatives are directly linked to its Advanced Intermediates segment, where cresol economics are sensitive to energy and compliance costs.

Parallel to efficiency measures, low-carbon positioning is becoming a competitive differentiator. In 2025, BASF ramped up production of low-carbon chemical intermediates, offering cresol-based solutions aligned with the EU’s 2026 environmental auditing and lifecycle reporting requirements. Germany’s approach reflects a broader European trend of preserving cresol’s role in high-value applications while systematically reducing its environmental footprint.

South Korea: Polyurethane-Driven Demand Upswing

South Korea’s relevance to the cresol market is increasingly downstream-led. In December 2025, Kumho Mitsui Chemicals announced plans to expand MDI capacity by 100,000 tpa, reaching 710,000 tpa, with construction commencing in February 2026. This expansion directly drives demand for cresol-based specialty additives used in polyurethane stabilization and performance enhancement. As South Korea continues to scale high-end polymers for construction, automotive, and insulation, cresol demand is expected to remain structurally linked to MDI and derivative value chains rather than commodity applications.

Comparative Summary: Strategic Positioning of the Cresol Industry by Country

Cresol Market County Level Snapshot

|

Country / Region

|

Primary Demand Driver

|

Strategic Industry Shift

|

Role in Global Cresol Value Chain

|

|

South Africa

|

Coal-based feedstock security

|

Margin uplift via specialty derivatives

|

Global upstream stabilizer

|

|

India

|

Pharma, Vitamin E, agrochemicals

|

Specialty expansion and sustainability certification

|

Fast-growing downstream hub

|

|

China

|

Domestic protection and polymers

|

Export shift to high-purity grades

|

Volume leader under rationalization

|

|

United States

|

Rubber additives and biocides

|

Downstream specialization

|

High-value application market

|

|

Germany

|

Regulatory compliance

|

Low-carbon intermediates

|

Premium regulated supplier

|

|

South Korea

|

Polyurethanes and MDI

|

Capacity-led additive demand

|

Demand-driven downstream consumer

|

Cresol Market Report Scope

Cresol Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$425 Million

|

|

Market Size (2034)

|

$589.4 Million

|

|

Market Growth Rate

|

3.7%

|

|

Segments

|

By Product Type (Ortho-Cresol, Meta-Cresol, Para-Cresol, Cresylic Acid), By Source (Chemical Synthesis, Coal Tar Distillation), By Application (Chemical Intermediates, Solvents, Preservatives and Disinfectants, Agrochemicals, Fragrances and Flavors), By End-Use Industry (Pharmaceuticals and Healthcare, Agriculture, Automotive, Electronics and Electrical, Construction)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sasol Limited, LANXESS AG, Anhui Haihua Chemical Technology Group Co., Ltd., Atul Ltd., Mitsui Chemicals, Inc., SABIC, Sumitomo Chemical Co., Ltd., Hexion Inc., Honshu Chemical Industry Co., Ltd., Konan Chemical Manufacturing Co., Ltd., Nanjing Datang Chemical Co., Ltd., Dakota Gasification Company, Rain Carbon Inc., Samyoung Innovation Corp., Merisol USA LLC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Cresol Market Segmentation

By Product Type

- Ortho-Cresol

- Meta-Cresol

- Para-Cresol

- Cresylic Acid

By Source

- Chemical Synthesis

- Coal Tar Distillation

By Application

- Chemical Intermediates

- Solvents

- Preservatives and Disinfectants

- Agrochemicals

- Fragrances and Flavors

By End-Use Industry

- Pharmaceuticals and Healthcare

- Agriculture

- Automotive

- Electronics and Electrical

- Construction

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Cresol Industry

- Sasol Limited

- LANXESS AG

- Anhui Haihua Chemical Technology Group Co., Ltd.

- Atul Ltd.

- Mitsui Chemicals, Inc.

- SABIC

- Sumitomo Chemical Co., Ltd.

- Hexion Inc.

- Honshu Chemical Industry Co., Ltd.

- Konan Chemical Manufacturing Co., Ltd.

- Nanjing Datang Chemical Co., Ltd.

- Dakota Gasification Company

- Rain Carbon Inc.

- Samyoung Innovation Corp.

- Merisol USA LLC

*- List not Exhaustive