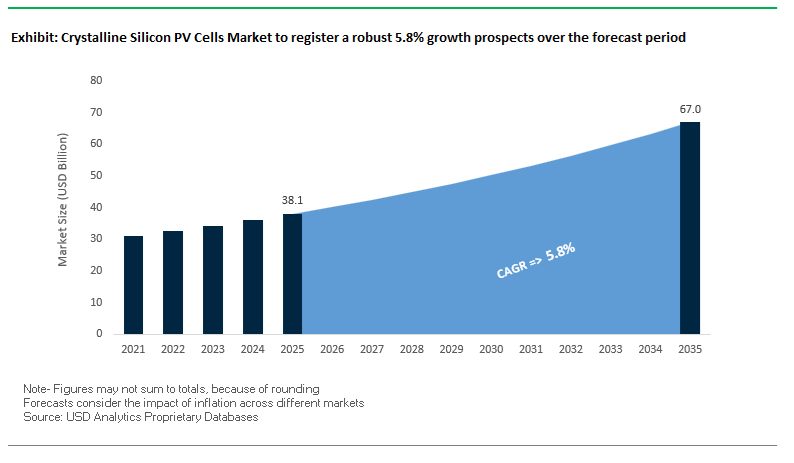

The crystalline silicon PV cells market is projected to rise from USD 38.1 billion in 2025 to around USD 67 billion by 2035, reflecting a solid CAGR of 5.8% (2025–2035). Growth is being driven less by incremental module volume and more by step-change gains in conversion efficiency, energy yield, and LCOE reduction, particularly through N-type TOPCon, HJT and back-contact (BC) cell architectures.

From late 2024 through 2025, the crystalline silicon PV cells market entered a new phase where R&D milestones are rapidly being converted into commercial product platforms. In November 2025, JinkoSolar set a 34.76% efficiency record for an N-type TOPCon-based perovskite tandem solar cell, signaling that crystalline silicon is not being displaced but rather upgraded through tandem integration with perovskites. In the same month, JinkoSolar also announced a 27.79% world-record N-type TOPCon cell efficiency, verified by ISFH, which effectively defines the TOPCon 2.0 performance ceiling for near-term mass production. These records confirm a multi-year roadmap where standard mono PERC has ceded leadership to N-type TOPCon, and where tandem structures will increasingly leverage the industrial base of crystalline silicon PV cells for higher efficiency and lower LCOE.

Module power classes and platform strategies are also shifting decisively toward large-format N-type and BC products. In October 2025, JA Solar began volume production and first shipments of DeepBlue 5.0 N-type TOPCon modules using Bycium+ 5.0 cells, delivering up to 650 W at 24.07% efficiency, directly targeting utility-scale solar projects looking to cut BOS costs with fewer strings and higher DC capacity per tracker. That same month, LONGi validated in a desert test that its Hi-MO 9 BC modules yield 2.45% more energy than comparable TOPCon, reinforcing developer interest in BC platforms where higher upfront CAPEX is offset by lower LCOE and higher IRR. In September 2025, Trina Solar strengthened Europe’s technology base by signing a TOPCon patent licensing deal with HoloSolis, enabling local European manufacturing of TOPCon-based PV cells and modules and supporting regional supply chain resilience.

Earlier in the year, the N-type momentum and technology diversity were further underlined by Trina Solar’s and Tongwei’s roadmaps. In July 2025, Trina launched its Vertex N i-TOPCon Ultra modules, pushing mass-produced module power to up to 740 W at 23.3% efficiency, providing a bankable solution for ultra-large utility plants while easing BOS and land-use constraints. On the upstream side, June 2025 saw Premier Energies and SAS announce a 2 GW wafer manufacturing joint venture in India, accelerating vertical integration into advanced silicon wafers outside China and diversifying the supply chain for global cell makers. In January 2025, Trina achieved a 27.08% world record for an N-type Cz-Si HJT solar cell, showing that HJT remains a parallel innovation track with superior temperature performance and bifaciality, even as TOPCon dominates near-term scale. Collectively, these developments indicate that the crystalline silicon PV cells market is evolving into a multi-platform N-type ecosystem (TOPCon, BC, HJT, tandems) with strong regional manufacturing footprints and relentless efficiency races.

Key technical and economic benchmarks define competitive advantage. LONGi’s Hybrid Interdigitated Back Contact (HIBC) cell reaching 27.81% efficiency in April 2025 resets expectations for commercializable BC technology, pushing beyond mainstream TOPCon limits and demonstrating real potential for next-generation premium modules. At the system level, BC modules including LONGi’s Hi-MO 9 can cut LCOE by 3–4.5% in high-irradiance desert sites because a 2.45% gain in field energy yield compounds across a 25–30 year asset life. In parallel, HJT modules deliver a superior temperature coefficient (around −0.25% to −0.27%/°C versus −0.29% to −0.32%/°C for N-type TOPCon), sustaining higher output in hot climates that dominate future solar build-out. Finally, aggressive wafer thinning of high-purity N-type mono silicon underpins an estimated 35% reduction in panel cost per watt over the five years to 2025, aligning efficiency gains with material savings and ensuring crystalline silicon remains the backbone of global PV deployment despite emerging tandem concepts.

- Record BC efficiency leadership: LONGi’s 27.81% HIBC efficiency (Apr 2025) demonstrates that BC architectures are surpassing mainstream TOPCon efficiency limits for industrial-sized cells.

- LCOE advantage through energy yield: Field data published in Oct 2025 show Hi-MO 9 BC modules deliver 2.45% higher energy yield than N-type TOPCon in desert conditions, translating into 3–4.5% LCOE reduction for utility-scale projects.

- Thermal resilience in hot climates: HJT modules maintain a better power temperature coefficient (−0.25% to −0.27%/°C) than mass-produced N-type TOPCon (−0.29% to −0.32%/°C), boosting output in high-temperature markets.

- Cost-down via wafer thinning: High-purity N-type mono wafers combined with advanced thinning have driven an estimated 35% decline in cost per watt over five years, primarily from lower silicon consumption per cell.

Efficiency Upgrades, Back-Contact Architectures, Ultra-Thin Silicon, and Perovskite-Silicon Tandems Define the Future of the Crystalline Silicon (c-Si) Photovoltaic Cells Market

Trend 1: Industry-Wide Migration from PERC to TOPCon Cells Across Utility-Scale and Premium Residential Solar Segments

The decline of PERC (Passivated Emitter and Rear Cell) technology reflects the industry’s pivot toward TOPCon (Tunnel Oxide Passivated Contact) cells, driven by significant efficiency enhancements, better field performance, and reduced first-year degradation. TOPCon has emerged as the scalable successor due to compatibility with existing PERC production lines and attractive cost-per-Watt metrics.

Key performance drivers include:

- Mass-production efficiencies reaching 25.2%, a significant step above standard PERC production efficiency (~23.2%). The widening gap solidifies TOPCon as the high-efficiency mainstream platform for utility and residential buyers.

- Superior power temperature coefficient of −0.30%/°C, outperforming PERC’s −0.34%/°C, delivering higher energy yields in hot climates and rooftop installations.

- Lower first-year degradation (≈1%) versus ~2% for PERC, ensuring more stable long-term performance and stronger lifecycle economics for commercial, industrial, and utility-scale investors.

- Bifaciality factor exceeding 80%, compared to PERC’s ~70%, enabling 5.69%–8.16% higher real-world energy yield in bifacial installations across ground-mounted utility projects.

- The rapid transition reflects the market’s emphasis on maximizing Levelized Cost of Electricity (LCOE) reduction, with TOPCon now emerging as the universal replacement for aging PERC technology.

Trend 2: Qualification of IBC and Back-Contact (BC) Technologies for High-Power-Density, Premium Distributed Generation

Premium residential and commercial projects-especially those with space constraints-are driving demand for Interdigitated Back Contact (IBC) and other back-contact technologies due to their exceptional power density and superior aesthetics. These architectures eliminate front-side metallization, enabling maximum light absorption and unmatched module efficiencies.

Key data-backed performance attributes include:

- Commercial IBC modules achieving 25.0% certified efficiency, positioning them at the top of the crystalline silicon performance hierarchy.

- 3%–5% increase in short-circuit current (JSC) due to elimination of shading losses, improving performance in low-light or diffuse-light conditions.

- Temperature coefficient as low as −0.27%/°C, giving IBC modules a marginal but meaningful advantage over TOPCon and HJT alternatives.

- 40-year product and power warranties, enabled by robust hotspot mitigation and improved thermal stability.

These attributes position IBC as the preferred architecture for rooftops, BIPV systems, high-visibility residential arrays, and specialized commercial installations, where both efficiency and long-term durability are critical differentiators.

Opportunity 1: Commercialization of Ultra-Thin Silicon Wafers (<130 μm) to Reduce Material Cost and Lower Embodied Energy

With polysilicon representing a major share of module cost and carbon footprint, the industry is prioritizing wafer thinning to reduce material input while maintaining high electrical performance. This shift offers strong economic and sustainability benefits in the next phase of PV manufacturing.

Key drivers include:

- 28% reduction in module cost and 48% reduction in capital expenditure projected for innovative architectures using ~50 μm wafers, dramatically improving manufacturing economics.

- Lower embodied energy due to reduced purification and ingot growth requirements, directly supporting global net-zero manufacturing goals.

- Improved open-circuit voltage (VOC) demonstrated in heterojunction and advanced cell concepts as wafer thickness is reduced to 30 μm-defying historical assumptions about thinning losses.

- 21% efficiency achieved on <60 μm wafers in heterojunction designs, confirming that ultra-thin wafer pathways can sustain high-performance solar cells with drastically lower silicon consumption.

This opportunity is strategically aligned with global PV supply chain decarbonization goals, making ultra-thin-wafers a long-term economic and ESG-driven transformation.

Opportunity 2: Scaling Perovskite-Silicon Tandem Cell Integration for the Next Generation of Ultra-High-Efficiency PV Modules

Perovskite-silicon tandem cells represent the industry's most promising route to ultra-high efficiencies, surpassing the Shockley–Queisser limit of legacy single-junction silicon and delivering unprecedented voltage characteristics.

Key advancement indicators include:

- Certified tandem efficiencies reaching 33.5%, well above the single-junction limit of 29.4%, establishing tandem technology as the future of premium PV.

- VOC values up to 1.954 V, compared to <0.7 V for single-junction silicon cells, enabling superior power output under both direct and low-light conditions.

- TOPCon-compatible tandem designs achieving 31.3% efficiency, proving manufacturability and scalability on mainstream PV production lines.

- Major investments in pilot production, including a European manufacturer committing €20 million to develop tandem-capable fabrication lines targeting commercialization by 2026.

Tandem cells are expected to dominate premium rooftop, utility-scale, and distributed generation markets, especially where land availability and LCOE optimization drive engineering decisions.

Crystalline Silicon PV Cells Market Share Analysis

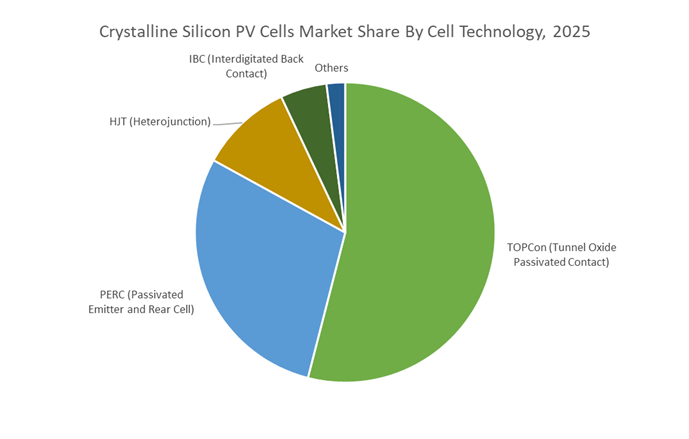

Market Share by Cell Technology: TOPCon Leads Through Higher Efficiency, Low Degradation, and Seamless Manufacturing Integration

TOPCon (Tunnel Oxide Passivated Contact) commands a dominant 55% share of the Crystalline Silicon PV Cells Market, driven by its superior conversion efficiency, enhanced long-term stability, and low-cost scalability compared to legacy PERC technology. As the solar industry pushes toward higher module power output and lower Levelized Cost of Electricity (LCOE), TOPCon has emerged as the most commercially viable upgrade pathway because it requires minimal modification of existing PERC production lines. Manufacturers can adopt TOPCon using much of their current infrastructure—significantly reducing capex barriers while gaining an efficiency boost of 1 to 3 percentage points, enabling mass-production cell efficiencies between 23% and 25%. This efficiency uplift is primarily due to TOPCon’s ultra-thin tunnel oxide layer and polysilicon passivation stack, which drastically reduces recombination losses at the rear surface.

Further strengthening its leadership is TOPCon’s reliance on n-type silicon wafers, which exhibit inherently lower susceptibility to LID and LETID than traditional p-type substrates. This stability translates into lower annual degradation rates (≤0.4%/year), ensuring higher lifetime energy output—a critical metric for utility-scale developers and investors seeking long-term yield certainty. Additionally, TOPCon modules offer a superior temperature coefficient (~−0.30%/°C) compared to PERC, allowing better performance in hot climates where PV installations commonly experience output losses during peak solar hours. The combination of high efficiency, excellent thermal behavior, and proven long-term durability positions TOPCon as the most strategically advantageous technology for PV manufacturers transitioning to next-generation solar architectures.

Market Share by Application/Product Form: Bifacial Solar Cells Dominate Through Superior Energy Yield and Lowest LCOE in Utility-Scale Installations

Bifacial solar cells hold an overwhelming 75% share of the market because they deliver the strongest economic and performance advantages across commercial and utility-scale solar projects, where every marginal gain in energy generation substantially improves project economics. By harvesting solar irradiance from both the front and rear sides, bifacial modules capture 5% to 30% more energy annually depending on site-specific albedo, installation height, and array configuration. This bifacial gain significantly reduces LCOE, making bifacial technology the preferred choice for developers targeting maximum output per unit area—especially in high-reflectivity environments such as snow-covered regions, deserts, white membrane rooftops, or sites engineered with reflective ground treatments.

The widespread adoption of bifacial cells is further reinforced by the dual-glass module design commonly used in this product category. The use of glass on both sides improves mechanical strength, enhances resistance to moisture ingress, and mitigates micro-cracking—key factors that extend module reliability and support performance warranties up to 30 years. These durability enhancements reduce long-term operational costs and increase investor confidence in large-scale solar assets. Given that utility-scale installations now dominate global solar capacity additions, the ability of bifacial modules to optimize irradiance capture and maximize annual energy yield has cemented their position as the leading product form in the crystalline silicon PV ecosystem.

Country Analysis: Global Crystalline Silicon PV Cell Manufacturing Hubs

China – N-Type TOPCon Dominance and Record-Breaking Efficiency Strengthen Its Command of the Global c-Si PV Cell Supply Chain

China maintains an unchallenged leadership position in the global Crystalline Silicon PV Cells Market, driven by massive N-Type technology adoption, unparalleled manufacturing scale, and continuous breakthroughs in high-efficiency cell architectures. By the end of 2024, the majority of newly added Chinese capacity transitioned toward N-Type TOPCon solar cell manufacturing, rapidly phasing out legacy PERC lines in favor of high-efficiency, high-lifetime architectures. The acceleration of N-Type production has redefined China’s competitiveness by enabling higher module wattage, longer operational lifetimes, and better performance in low-irradiance conditions—critical requirements for utility-scale installations across Asia, Europe, and the Middle East.

China’s innovation edge is reinforced by world-leading efficiency advances. In November 2025, LONGi achieved a certified world record of 33.4% efficiency on a flexible perovskite-silicon tandem cell, signaling the beginning of commercially viable tandem integration within crystalline silicon frameworks. LONGi also initiated mass production of its HIBC (Hybrid Interdigitated Back Contact) solar cell technology in June 2025, reaching 27.3% cell efficiency and module efficiencies above 25%, setting a new benchmark for industrial-scale crystalline silicon manufacturing. Export momentum remains strong: in H1 2025, China’s exports of solar cells surged 76% and wafers rose 26%, with solar wafers and cells representing over 40% of total solar product exports. This shift underscores China’s evolving strategy of dominating upstream PV cell and wafer supply for emerging manufacturing hubs such as India, Southeast Asia, and the Middle East.

United States – IRA Incentives Trigger a Nationwide Reshoring Wave for Crystalline Silicon PV Cells and Domestic Wafer Production

The United States is experiencing the most significant reshoring movement in its solar industry history, catalyzed by the Inflation Reduction Act (IRA). Since August 2022, IRA-linked tax credits and manufacturing incentives have generated over $100 billion of private-sector solar investments, marking a structural realignment of the U.S. Crystalline Silicon PV Cells Market. These investments target the creation of a fully domestic PV supply chain, from polysilicon to wafers, cells, and modules. As part of this reshoring wave, newly announced solar manufacturing facilities include 43 GW of crystalline silicon cell capacity and 20 GW of silicon ingot and wafer capacity, projected to meaningfully reduce U.S. dependence on imports by 2026.

The U.S. policy framework is deeply advantageous for crystalline silicon PV cell manufacturers. The Domestic Content Bonus under the IRA—an additional 10% Investment Tax Credit and a 0.3¢/kWh Production Tax Credit—directly rewards solar developers for using U.S.-made crystalline silicon cells and wafers, creating assured offtake for domestic producers. Meanwhile, the revival of the U.S. polysilicon industry is restoring supply-chain security for ultra-high-purity feedstock required for N-Type ingots. Together, these developments position the U.S. to evolve from a heavily import-dependent market into a resilient manufacturing hub capable of producing high-efficiency TOPCon, HJT, and future tandem crystalline silicon cells.

India – PLI-Backed Gigafactories and N-Type TOPCon Adoption Accelerate its Emergence as a Global PV Cell Manufacturing Powerhouse

India’s Crystalline Silicon PV Cells Market is being transformed by the large-scale industrialization enabled by the government’s Production Linked Incentive (PLI) Scheme, which is catalyzing downstream and upstream integration across the solar value chain. Under the flagship PLI initiative, the government has approved 48.3 GW of fully or partially integrated solar module manufacturing capacity, backed by an investment outlay of ₹24,000 crore (~$2.9 billion). These Gigafactory-scale commitments enable India to rapidly scale domestic manufacturing of wafers, cells, and modules, positioning the country to become a major global exporter of high-efficiency crystalline silicon PV products by 2026 and beyond.

India is also emerging as a fast adopter of N-Type TOPCon solar cell technology. During H1 2025, TOPCon accounted for 41.5% of India’s total crystalline silicon cell capacity additions, illustrating a technological leap that allows India to align itself with advanced global standards without the legacy burden of PERC phase-out. The PLI scheme has already created 43,000 new jobs across nine states, with Gujarat leading capacity expansions through investments from Adani New Industries and Reliance Industries. As of November 2025, India’s total installed module manufacturing capacity reached 121.68 GW, validating its ambition to emerge as one of the world’s largest producers of high-efficiency crystalline silicon solar cells and modules.

Europe (France/Germany) – Net Zero Industry Act Fuels TOPCon Cell Gigafactories and Regional Photovoltaic Sovereignty

Europe’s Crystalline Silicon PV Cells Market is undergoing a strategic revival powered by the EU’s Net Zero Industry Act (NZIA), which aims to localize critical PV manufacturing and reduce dependency on Asian imports. A landmark development is the HoloSolis Gigafactory, which secured more than €220 million in public and private funding in November 2025. This 5 GW facility in France will be one of Europe’s largest solar manufacturing sites, dedicated exclusively to TOPCon crystalline silicon cell production, and is set to begin commercial operations in 2026.

The Gigafactory directly supports the NZIA mandate for 40% of deployed solar PV in Europe to be EU-made, enhancing regional energy sovereignty. Germany and France are prioritizing low-carbon solar technologies, placing strong emphasis on lifecycle sustainability, embodied carbon reduction, and advanced crystalline silicon cell designs optimized for European climatic conditions. With EU-backed financing, cutting-edge equipment imports, and an increasing commitment to N-Type TOPCon manufacturing, Europe is building the foundations of a competitive, long-term regional supply chain capable of producing premium-efficiency crystalline silicon PV cells for utility-scale and rooftop markets.

Competitive Landscape: N-Type TOPCon, HJT and Back-Contact Leaders in Crystalline Silicon PV

The crystalline silicon PV cells market is dominated by a small group of vertically integrated Tier-1 manufacturers that combine upstream wafer and cell manufacturing with downstream module supply and project support. Competitive differentiation is increasingly defined by cell efficiency roadmaps, N-type technology breadth (TOPCon, HJT, BC), global manufacturing footprints, and proven LCOE gains in real-world field data. LONGi is positioning itself as the BC and LCOE champion, JinkoSolar as the TOPCon and tandem efficiency frontrunner, Tongwei as the cell volume and dual N-type specialist, while Trina and JA Solar leverage large-format modules, scenario-based product lines and global project pipelines. For buyers, bankability means not only financial robustness, but also evidence that suppliers can execute rapid technology transitions without compromising reliability, degradation, or supply security.

LONGi is driving the back-contact (BC) transformation in crystalline silicon PV cells, supported by one of the industry’s largest R&D budgets. In 2024, the company reported CNY 5.014 billion (around EUR 605 million) in R&D expenditure, underscoring its commitment to fundamental cell architecture innovation. In April 2025, LONGi achieved a 27.81% certified efficiency for an industrial-size Hybrid Interdigitated Back Contact (HIBC) cell, creating a new benchmark beyond mainstream TOPCon. Its Hi-MO 9 BC modules are already validated in desert test beds to deliver 2.45% higher energy yield than TOPCon and 3–4.5% LCOE reduction, positioning LONGi as a preferred supplier for developers optimizing long-term project economics in high-irradiance regions.

JinkoSolar has emerged as the N-type TOPCon performance and tandem R&D leader in the crystalline silicon PV cells market. In November 2025, it set a 27.79% world record for N-type TOPCon cell efficiency, verified by ISFH, effectively pushing state-of-the-art mass-production efficiency into the high-20s. In parallel, the company reached a 34.76% efficiency record for a perovskite/TOPCon tandem solar cell, making it one of the most advanced contenders for future hybrid crystalline silicon platforms. On the product side, Jinko’s Tiger Neo 3.0 N-type module family, with up to 670 W output and 24.8% module efficiency, is optimised for high-power-density commercial and utility deployments, reinforcing its role as a global top-tier supplier for large-scale PV cell and module solutions.

Tongwei Solar leverages deep vertical integration “from silicon to module” and scale leadership to shape price and technology trends in crystalline silicon PV cells. The company shipped around 100 GW of modules in the three-and-a-half years to H1 2025, confirming its position as one of the highest-volume cell producers globally. Strategically, Tongwei is investing in both N-type TOPCon and HJT technologies, with TOPCon cell efficiencies around 25.2% and HJT pushing 26.5% in Q3 2024. In Q1 2025, Tongwei announced plans for a new 25 GW module base including 5 GW of HJT capacity, ensuring it can respond to regional requirements for hotter climates, bifacial projects and premium rooftop segments. The dual-track N-type roadmap allows Tongwei to serve both cost-optimized and performance-maximized use cases.

Trina Solar remains a pioneer of 210 mm large-format wafers and high-power utility-scale modules, combining advanced i-TOPCon cell technology with system integration expertise. By Q1 2025, Trina’s cumulative module shipments exceeded 275 GW, evidencing long-term field reliability and global bankability. The company’s Vertex N i-TOPCon Ultra modules deliver up to 760 W output and 24.5% module efficiency, driving BOS cost reductions and higher DC capacity per tracker row in large plants. Trina continues to win “Top Performer” status from PVEL—11 consecutive years by 2025—reinforcing its reputation for durability and low degradation. Coupled with PV+storage offerings and a strong IP portfolio (including TOPCon licensing to HoloSolis in Europe in Sept 2025), Trina is a central player in utility-scale crystalline silicon PV cell deployment.

JA Solar is positioning itself as a scenario-driven crystalline silicon PV supplier, emphasizing N-type TOPCon performance and reliability in harsh environments. In Q1 2025, the firm’s mass-produced N-type Bycium+ cells reached 27% efficiency, demonstrating rapid industrialization of its N-type architecture. JA Solar’s product portfolio includes DeepBlue 5.0 N-type TOPCon modules delivering up to 650 W and 24.07% efficiency, launched into volume production in October 2025 to address global utility-scale demand. For extreme sites, its DesertBlue module line is specifically engineered for sandy and high-temperature conditions, using patented Anti-Dust frames and low-degradation encapsulants (in collaboration with DuPont). Major wins like the 485 MW wind + PV + desert rehabilitation project in Inner Mongolia (Q1 2025) further cement JA Solar as a key N-type crystalline silicon PV cells supplier for complex, climate-challenged deployments.

Crystalline Silicon PV Cells Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$38.1 Billion

|

|

Market Size (2035)

|

$67 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Cell Technology (PERC, TOPCon, HJT, IBC, Back Contact Cells), By Crystalline Structure (Monocrystalline Silicon, Polycrystalline Silicon), By Value Chain Stage (Polysilicon, Ingot/Brick, Wafer, Cell, Module), By Application/Product Form (Standard Solar Cells, Bifacial Solar Cells, Flexible Crystalline Cells, Half-Cut Cells), By Conductor Material (Silver Paste, Copper Plating)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

LONGi Green Energy Technology Co. Ltd., JinkoSolar Holding Co. Ltd., Trina Solar Co. Ltd., JA Solar Technology Co. Ltd., Tongwei Solar, Canadian Solar Inc., Adani Solar, First Solar Inc., Meyer Burger Technology AG, Waaree Energies Ltd., REC Solar Holdings AS, Risen Energy Co. Ltd., Huasun Energy

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Crystalline Silicon PV Cells Market Segmentation

By Cell Technology

- PERC (Passivated Emitter and Rear Cell)

- TOPCon (Tunnel Oxide Passivated Contact)

- HJT (Heterojunction)

- IBC (Interdigitated Back Contact)

- Back Contact Cells

By Crystalline Structure

- Monocrystalline Silicon (Mono-Si)

- Polycrystalline Silicon (Poly-Si)

By Value Chain Stage

- Polysilicon (Feedstock)

- Ingot/Brick (Crystallization)

- Wafer (Slicing)

- Cell (Doping/Passivation/Metallization)

- Module (Assembly/Encapsulation)

By Application/Product Form

- Standard Solar Cells

- Bifacial Solar Cells

- Flexible Crystalline Cells

- Half-Cut Cells

By Conductor Material

- Silver Paste

- Copper Plating

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies: Key Crystalline Silicon PV Cell Manufacturers

- LONGi Green Energy Technology Co., Ltd.

- JinkoSolar Holding Co., Ltd.

- Trina Solar Co., Ltd.

- JA Solar Technology Co., Ltd.

- Tongwei Solar (Tongwei Co., Ltd.)

- Canadian Solar Inc.

- Adani Solar (Adani New Industries)

- First Solar, Inc.

- Meyer Burger Technology AG

- Waaree Energies Ltd.

- REC Solar Holdings AS

- Risen Energy Co., Ltd.

- Huasun Energy

*- List not Exhaustive