CVD Lab-Grown Diamonds Market Overview — Economics, Demand Re-Segmentation, and Industrial Pull Redefine the Industry Trajectory

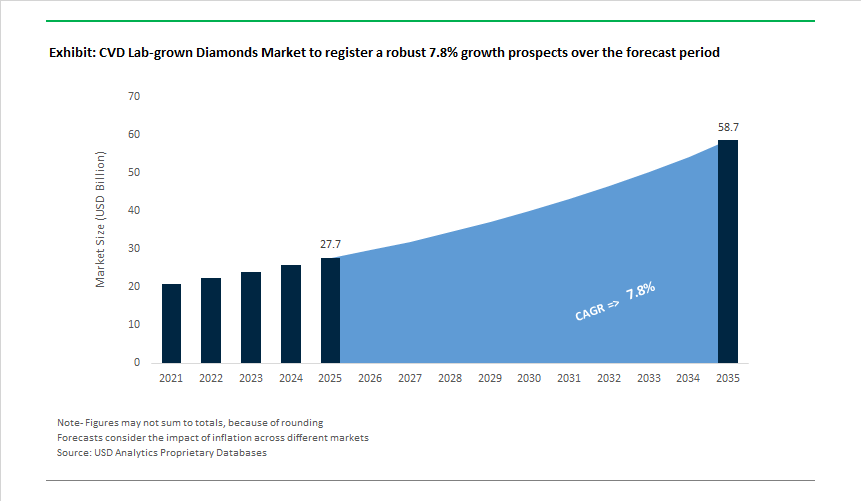

The CVD Lab-Grown Diamonds Market is valued at USD 27.7 Billion in 2025 and is projected to reach USD 58.7 Billion by 2035 at a 7.8% CAGR between 2025 and 2035.

The CVD lab-grown diamonds (LGD) market is undergoing a structural repositioning—from a cost-driven substitute for mined diamonds into a bifurcated materials market spanning accessible luxury and mission-critical industrial applications. Growth through 2035 is being shaped less by incremental capacity additions and more by shifts in production economics, pricing architecture, and end-market pull from electronics and advanced thermal management. As a result, competitive advantage is consolidating around players that can scale reactor productivity, guarantee consistency and purity, and integrate traceability into global supply chains.

At the upstream level, improvements in CVD reactor economics are redefining cost curves and capital efficiency. Shorter growth cycles and higher utilization rates are lowering unit costs and compressing payback periods, particularly in India and China, where scale and operational intensity increasingly determine margin leadership. This has transformed CVD diamonds from a speculative capacity-expansion play into a manufacturing-led industry where throughput discipline, yield optimization, and quality control dictate returns on invested capital.

Downstream, the market is being reshaped by a sustained price realignment relative to natural diamonds. CVD diamonds trading at a fraction of mined equivalents have structurally expanded the addressable consumer base, particularly in bridal and fashion jewelry, by shifting purchase decisions from exclusivity toward size, design flexibility, and ethical sourcing. This is not a temporary discount cycle; it represents a lasting reset in consumer value perception, enabling higher volumes and faster inventory turnover for retailers while compressing margins for undifferentiated producers.

Beyond jewelry, industrial demand is emerging as a strategically significant growth pillar. High-purity CVD diamonds are increasingly specified in thermal management and power-dense electronics, where performance—not price—drives procurement decisions. For semiconductor, defense, and communications OEMs, diamond substrates offer a clear system-level advantage in heat dissipation and reliability, supporting long-term supply agreements rather than spot purchasing. While volumes remain modest relative to jewelry, margins and switching costs are materially higher, making this segment disproportionately attractive for advanced producers.

Across both segments, traceability and compliance have become gating requirements rather than marketing features. Institutional buyers, global retailers, and industrial customers increasingly require verifiable origin, ESG alignment, and digital certification, raising barriers to entry and favoring organized, compliant supply chains. As regulation, certification, and trade scrutiny intensify, informal or opaque production models are losing relevance.

CVD Lab-Grown Diamonds Market Analysis- Policy Signals, Technology Validation, and Demand Inflection Points

Market dynamics in 2025 reinforce the shift from experimentation to industrial maturity. Government policy interventions, technology validation by high-credibility buyers, and visible consumer acceptance events collectively strengthened demand visibility across the value chain.

Policy support has played a direct role in reinforcing India’s position as the global manufacturing hub for CVD diamonds. Trade facilitation measures reduced input friction, improved working capital efficiency, and supported higher reactor utilization, directly improving exporter competitiveness. At the same time, tightening disclosure and hallmarking frameworks clarified product differentiation at retail, reducing consumer confusion and enabling clearer pricing segmentation between mined and lab-grown stones.

Technology validation accelerated adoption beyond jewelry. Partnerships and programs involving defense, advanced computing, and power electronics signaled that CVD diamonds are being evaluated—and increasingly specified—as functional materials rather than experimental substitutes. Progress toward larger-diameter diamond wafers and defense-grade qualification further reduced perceived technical risk, strengthening the investment case for downstream integration and long-term supply contracts.

Consumer demand signals in 2025 demonstrated that acceptance of lab-grown diamonds has moved decisively into higher-value segments. High-visibility purchases and social validation effects translated into measurable spikes in interest for large-carat stones, confirming that price accessibility does not preclude premium positioning when combined with design and ethical narratives.

Trade friction, particularly around tariffs and import duties, has introduced new strategic considerations. Rather than constraining growth, these pressures are accelerating regionalization strategies, including “grow-to-retail” models in end markets, vertical integration, and localized finishing operations. This shift favors capitalized players capable of reconfiguring supply chains, while increasing exit pressure on smaller, export-dependent producers.

Scaling Multi-Reactor CVD Platforms for Large-Area Single-Crystal Diamond Substrates

The CVD lab-grown diamonds market is undergoing a decisive industrial shift from small, single-reactor R&D environments toward multi-reactor, factory-scale CVD platforms designed to deliver large-area, electronic-grade single-crystal diamond. This transition is being driven less by jewelry demand and more by semiconductor, RF, and thermal-management requirements, where substrate size, defect density, and reproducibility directly determine system-level performance.

In March 2025, Orbray reported the fabrication of the world’s largest self-standing (111) single-crystal diamond plates at 20 mm × 20 mm, a step-change from the legacy 3–5 mm formats that constrained device scaling. The breakthrough was achieved using proprietary step-flow growth techniques on sapphire templates, eliminating twin boundaries that historically limited electronic performance. Commercialization timelines now point to >2-inch class diamond wafers by 2026, aligning with roadmap needs for next-generation wide-bandgap devices.

On the equipment side, modular Microwave Plasma CVD (MPCVD) systems are becoming the dominant architecture. Suppliers such as Aixtron and Seki Diamond Systems are deploying pocket-holder reactor designs that support growth rates of 16–32 µm/hour while reducing etch-pit density by 1–3 orders of magnitude. By late 2024, more than 50% of new reactor installations in the U.S. and Japan were dedicated to semiconductor thermal-management applications, reflecting the market’s pivot from artisanal output toward repeatable, high-volume diamond manufacturing ecosystems.

Defect and Dopant Engineering of CVD Diamond for Quantum Information Systems

Beyond power electronics, CVD lab-grown diamonds are emerging as a platform material for quantum technologies, where atomic-scale control of defects determines commercial viability. Intensive R&D is now focused on Nitrogen-Vacancy (NV) center engineering, transforming diamond from a passive material into an active quantum sensing and communication medium.

In September 2025, joint research from Hebrew University of Jerusalem and Humboldt University achieved a record ~80% photon collection efficiency from NV centers operating at room temperature. By embedding nanodiamond emitters into precisely patterned nano-antenna structures, researchers overcame long-standing optical losses caused by internal reflection—removing a critical bottleneck for chip-scale quantum photonics.

Parallel advances in ion-implantation through nano-channels now allow deterministic placement of NV arrays with nanometer-scale accuracy. Studies released in 2025 demonstrate that precise nitrogen flow control enables spin coherence times (T₂) ranging from ~45 µs to over 540 µs, performance levels required for quantum magnetometry and biomedical imaging. Commercial intent is becoming evident: Germany’s €152 million investment in a quantum-enabled semiconductor inspection facility in Munich underscores how CVD diamond sensors are moving from laboratory curiosity to industrial metrology tools within advanced chip manufacturing.

Diamond Heat Spreaders as a Thermal Enabler for RF, AI, and Power Electronics

One of the most immediate commercial opportunities for CVD lab-grown diamonds lies in thermal management, where conventional materials have reached their physical limits. With intrinsic thermal conductivity exceeding 2,200 W/m·K—more than five times that of copper—CVD diamond has become the only viable heat-spreading solution for extreme heat-flux environments.

In RF electronics, technical data from Element Six shows that GaN-on-diamond RF devices can operate at six times higher frequencies than aluminum nitride-based alternatives before signal distortion occurs. Package-level integration of diamond substrates reduces thermal resistance by ~30%, enabling higher output power without compromising device lifetime—an essential requirement as 5G Advanced and early 6G architectures push into millimeter-wave and sub-THz regimes.

The opportunity extends into AI infrastructure. With rack densities now exceeding 50 kW, internal thermal bottlenecks are becoming a primary constraint on compute scaling. Industry evaluations in 2025 indicate that ~70% of AI-focused data center operators are actively assessing diamond-based heat spreaders, which can lower junction temperatures by up to 20°C versus advanced ceramic solutions. In automotive power electronics, diamond-based Cu-diamond composites are gaining traction in 800V EV architectures, where CTE matching and superior heat dissipation mitigate fatigue under aggressive power cycling.

Ultrapure CVD Diamond Windows for High-Energy Photon and Laser Systems

A second high-value opportunity is emerging in scientific infrastructure, where national investments in synchrotrons, free-electron lasers, and high-power beamlines are driving demand for ultrapure, radiation-hard diamond components. Traditional materials such as beryllium are increasingly unable to cope with the escalating power densities of modern facilities.

Between 2024 and 2025, next-generation beamlines reached radiation powers approaching 49 kW with power densities near 92 kW/mrad². Validation trials confirmed that 0.2 mm-thick CVD diamond windows can dissipate heat four times more effectively than state-of-the-art beryllium, maintaining structural integrity at localized temperatures above 370°C.

CVD diamond’s wide spectral transparency—from deep UV (~220 nm) to far-infrared (>100 µm)—further strengthens its position. Technical specifications from Torr Scientific indicate that a 250 µm diamond window exhibits <5% attenuation above 15 keV, preserving beam coherence for precision experiments. As global synchrotron facilities modernize to support higher-frequency, higher-brightness beams, demand is consolidating around ultra-high-purity (ppb-level) diamond windows, establishing a defensible niche for CVD producers capable of defect-free, large-area growth.

Market Share Analysis: CVD Lab-Grown Diamonds Market

Market Share by Product Type: Polished CVD Diamonds Capture the Value Pool

Polished diamonds account for approximately 85% of the global CVD Lab-Grown Diamonds Market, underscoring the reality that economic value in the diamond industry is realized almost entirely at the finished-gem stage rather than at the rough crystal level. This segment dominates because polishing transforms CVD-grown rough—an intermediate industrial output—into retail-ready gemstones that can be certified, branded, and sold at scale through jewelry channels. Market share is reinforced by the growing preference for environmentally certified, low-carbon diamonds, as leading CVD producers now operate reactors powered entirely by renewable energy, positioning polished lab-grown stones as a structurally sustainable alternative to mined diamonds. From a quality standpoint, polished CVD diamonds consistently achieve Type IIa purity, a category associated with exceptional optical clarity and historically rare in natural stones, enhancing their appeal among both consumers and jewelers. Advances in post-growth treatment have further strengthened this segment by enabling color correction into top-tier D–F grades, allowing a majority of polished CVD diamonds to meet “investment-grade” jewelry standards. Further, the optical properties of polished CVD stones—refractive index, brilliance, and fire—are physically indistinguishable from natural diamonds, eliminating perceptual trade-offs at the point of sale. These combined sustainability, quality, and retail-readiness advantages explain why polished diamonds dominate the CVD market’s value structure.

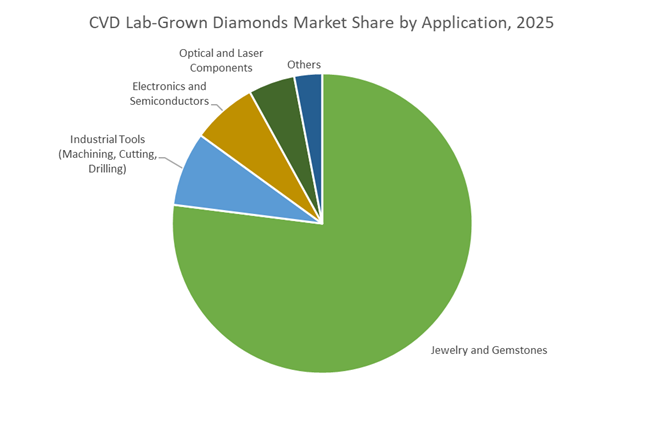

Market Share by Application: Jewelry and Gemstones Drive Volume-Led Adoption

Jewelry and gemstone applications represent approximately 80% of total demand in the CVD Lab-Grown Diamonds Market, making this segment the unequivocal demand anchor. This dominance reflects a structural shift in consumer behavior, where lab-grown diamonds are transitioning from niche ethical alternatives to mainstream luxury and fashion products. A dramatic wholesale price correction over the past several years has repositioned CVD diamonds into a predictable, cost-plus retail model, enabling brands to offer larger stones at a fraction of the price of mined equivalents. Market share is further amplified by changing consumer preferences toward larger carat sizes, as improved reactor yields and lower production costs have made 2–4 carat stones commercially viable for mass-market jewelry. Standardized per-carat pricing has reduced volatility and inventory risk for retailers, encouraging broader adoption across omnichannel jewelry platforms. In addition, the predictable geometry of CVD-grown rough allows for superior cut consistency, resulting in a higher proportion of stones achieving top-tier cut grades—a critical determinant of visual appeal and consumer confidence. As accessibility, size, and design flexibility increasingly define purchasing decisions, jewelry applications remain the primary growth engine sustaining CVD diamonds’ market dominance.

India - Reactor Indigenization and a Duty-Free LGD Manufacturing Ecosystem

India has decisively repositioned itself from being primarily a cutting-and-polishing hub to a vertically integrated CVD lab-grown diamond manufacturing powerhouse. The operationalization of the ₹242.96 crore InCent-LGD grant at IIT Madras in 2025 marks a structural inflection point, as the program directly targets indigenous CVD reactor design, plasma recipes, and high-purity seed development. This significantly reduces dependence on imported reactors and proprietary foreign growth technologies, improving cost control and long-term technological sovereignty. Parallel policy actions-most notably the abolition of customs duties on LGD seeds and the launch of the Diamond Imprest Authorization (DIA) Scheme-have streamlined working capital cycles for MSME exporters and reinforced India’s competitiveness across both luxury and industrial LGD segments.

At an industry level, 100% FDI allowance has catalyzed the formation of large-scale “green luxury” manufacturing clusters in Surat and Mumbai, integrating growth, polishing, grading, and branding under one roof. This ecosystem-level integration is enabling India to protect and expand its ~25.8% global trade share, while simultaneously shifting into higher-margin fancy-color diamonds and electronic-grade CVD plates. India’s strategy is increasingly export-led but technology-anchored, positioning the country as both a volume leader and a future IP owner in CVD diamond growth systems.

China - High-Volume Scaling and Industrial CVD Diversification

China continues to dominate global CVD lab-grown diamond output through industrial-scale manufacturing concentrated in Henan Province. The commissioning of SF Diamond’s 700,000-carat CVD facility has reinforced China’s leadership in industrial-grade and mid-market LGDs, particularly for precision tooling, abrasives, and affordable luxury jewelry. By late 2024, China accounted for ~46% of global LGD production, with export growth exceeding 78% YoY, underscoring its unmatched scale advantage.

Strategically, Chinese manufacturers are accelerating vertical integration into fancy-color diamonds, leveraging in-situ doping during the CVD growth phase to produce stable pink and blue stones without post-growth irradiation. This not only improves yield consistency but also reduces processing complexity. While China remains price-competitive, its 2025 strategy reflects a clear pivot toward differentiation-combining scale economics with product engineering to capture more value per carat across jewelry and industrial markets.

United States - Regulatory Clarity and High-Tech Diamond Applications

The United States remains the world’s largest demand center for CVD lab-grown diamonds, while simultaneously emerging as a high-value innovation hub for diamond-enabled advanced technologies. The GIA’s 2025 grading simplification, formally classifying LGDs into “Premium” and “Standard” categories, has removed long-standing consumer ambiguity and accelerated mainstream adoption. By the end of 2025, over 50% of engagement rings sold in the U.S. featured lab-grown diamonds, cementing LGDs as a normalized luxury product.

Beyond jewelry, federal funding under the CHIPS and Science Act is channeling investment into diamond-on-silicon heat spreaders for AI data centers, 5G/6G infrastructure, and quantum computing. With thermal conductivity roughly 5× higher than silicon, CVD diamond substrates are increasingly viewed as mission-critical materials for next-generation electronics. The U.S. market is therefore bifurcating into two high-value verticals-consumer luxury and deep-tech infrastructure-both of which reinforce long-term demand stability.

South Korea - Disruptive Liquid-Metal Diamond Growth

South Korea has emerged as a technological wildcard in the global CVD LGD landscape. The IBS–UNIST breakthrough, demonstrating diamond growth in 15 minutes at atmospheric pressure using liquid metal alloys, represents a potentially disruptive alternative to conventional vacuum-based CVD systems. While still pre-commercial, this approach could dramatically reduce capex intensity and energy consumption if scaled successfully, reshaping the economics of diamond synthesis.

Commercially, South Korea is also witnessing early luxury market traction, with domestic brands entering the LGD jewelry segment. At the policy level, LGDs are increasingly framed as strategic “super-materials” under the MPE 2030 Roadmap, particularly for diamond-based semiconductors and power electronics. South Korea’s role is therefore less about volume today and more about process innovation with long-term systemic impact.

Singapore - Precision Monocrystalline Diamond and B2B Platforms

Singapore occupies a specialized, high-margin niche in the global CVD LGD market, centered on monocrystalline diamond plates for scientific, optical, and industrial applications. Companies such as IIa Technologies continue to expand production using proprietary processes capable of delivering large-area, ultra-pure diamond windows for high-energy lasers and X-ray systems. These applications are structurally insulated from jewelry price cycles and prioritize material performance over cost.

In parallel, Singapore’s role as a financial and logistics hub is enabling the rise of “Diamond-as-a-Service” platforms, combining blockchain traceability, AI-based grading analytics, and cross-border B2B marketplaces. This positions the country as a control and verification node within the global LGD value chain, rather than a volume producer.

Germany - Sustainability-Led “Green Diamond” Innovation

Germany leads Europe’s CVD lab-grown diamond strategy through a strong emphasis on sustainability, optics, and precision engineering. German R&D clusters are deeply involved in developing CVD diamond optical components for large-scale research infrastructure such as the European XFEL. These applications demand extreme purity, dimensional stability, and radiation resistance-attributes where German producers excel.

Regulatory pressure from EU REACH and RoHS 2025 updates has also forced unprecedented transparency around LGD carbon intensity. In response, German manufacturers are deploying renewable-powered plasma reactors, achieving reported carbon intensities as low as 17 kg CO₂ per carat. This positions Germany as the reference market for “green diamonds”, a differentiation lever that is increasingly relevant for European luxury brands and institutional buyers.

Strategic Comparison: CVD Lab-Grown Diamonds Market (2025)

CVD Lab-Grown Diamonds Market Matrix

|

Country

|

Strategic Focus Area

|

Key 2025 Policy / Event

|

Structural Advantage

|

|

India

|

Reactor & seed indigenization

|

InCent-LGD + DIA Scheme

|

Full vertical integration

|

|

China

|

Mass CVD scaling

|

700k-carat Henan facility

|

Lowest cost per carat

|

|

United States

|

Luxury normalization & AI cooling

|

GIA grading reform + CHIPS funding

|

Dual demand engines

|

|

South Korea

|

Disruptive growth technology

|

Liquid-metal diamond synthesis

|

Process innovation

|

|

Singapore

|

Monocrystalline optics & B2B platforms

|

Iris process expansion

|

Precision leadership

|

|

Germany

|

Sustainable “green diamond” optics

|

EU carbon disclosure mandates

|

Lowest CO₂ intensity

|

CVD Lab-grown Diamonds Market Report Scope

CVD Lab-grown Diamonds Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$27.7 Billion

|

|

Market Size (2035)

|

$58.7 Billion

|

|

Market Growth Rate

|

7.8%

|

|

Segments

|

By Manufacturing Method (CVD, HPHT), By Type (Rough Diamonds, Polished Diamonds), By Nature & Color (Colorless, Colored), By Size (Below 2 Carat, 2–4 Carat, Above 4 Carat), By Application (Jewelry & Gemstones, Industrial Tools, Electronics & Semiconductors, Optical & Laser Components, Healthcare), By End-User Industry (Consumer Goods, Semiconductor & Electronics, Construction & Mining, Healthcare & Life Sciences, Aerospace & Defense)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

De Beers Group (Element Six), Sumitomo Electric Industries Ltd., Diamond Foundry Inc., IIa Technologies Pte Ltd., EDP Corporation, Swarovski AG, Brilliant Earth Group Inc., Signet Jewelers Limited, VRAI, Henan Huanghe Whirlwind Co., Ltd., Zhengzhou Sino-Crystal Diamond Co., Ltd., ALTR Created Diamonds, Pure Grown Diamonds LLC, Scio Diamond Technology Corporation, JSC New Diamond Technology

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

CVD Lab-Grown Diamonds Market Segmentation

By Manufacturing Method

- Chemical Vapor Deposition (CVD)

- High-Pressure High-Temperature (HPHT)

By Type

- Rough Diamonds

- Polished Diamonds

By Nature & Color

- Colorless

- Colored (Blue, Pink, Yellow, Fancy Hues)

By Size

- Below 2 Carat

- 2 – 4 Carat

- Above 4 Carat

By Application

- Jewelry and Gemstones

- Industrial Tools

- Electronics and Semiconductors

- Optical and Laser Components

- Healthcare

By End-User Industry

- Consumer Goods

- Semiconductor and Electronics

- Construction and Mining

- Healthcare and Life Sciences

- Aerospace and Defense

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in CVD Lab-Grown Diamonds Market

- De Beers Group (Element Six)

- Sumitomo Electric Industries, Ltd.

- Diamond Foundry Inc.

- IIa Technologies Pte Ltd

- EDP Corporation

- Swarovski AG

- Brilliant Earth Group, Inc.

- Signet Jewelers Limited

- VRAI

- Henan Huanghe Whirlwind Co., Ltd.

- Zhengzhou Sino-Crystal Diamond Co., Ltd.

- ALTR Created Diamonds

- Pure Grown Diamonds, LLC

- Scio Diamond Technology Corporation

- JSC New Diamond Technology

*- List not Exhaustive