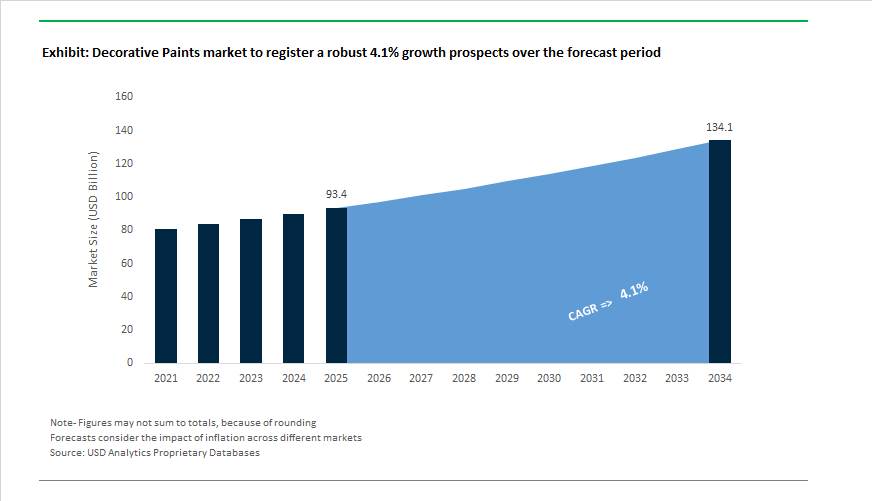

Decorative Paints Market to Reach $134.1 Billion by 2034 at 4.1% CAGR Amid Global Consolidation, Regulatory Transition, and Smart Coating Innovation

The Decorative Paints Market is projected to expand from $93.4 billion in 2025 to $134.1 billion by 2034, registering a CAGR of 4.1%. Market growth is being shaped by aggressive portfolio realignments, regional consolidation, premiumization of color offerings, and regulatory-driven reformulation toward PFAS-free and bisphenol-free decorative coatings. Demand fundamentals remain closely tied to residential renovation cycles, urban housing expansion, and commercial real estate refurbishment, particularly across Asia-Pacific and Latin America. Competitive positioning increasingly revolves around brand-led consumer engagement strategies, digital color ecosystems, and low-VOC architectural paint technologies aligned with tightening environmental mandates.

Structural consolidation intensified in late 2024, when PPG Industries finalized the sale of its U.S. and Canadian architectural coatings business to American Industrial Partners, leading to the rebranding of the unit as Pittsburgh Paints and sharpening PPG’s focus on industrial and aerospace coatings. In June 2025, AkzoNobel India divested its decorative paints business to the JSW Group for approximately €1.4 billion, enabling JSW to scale rapidly within the Indian architectural paints segment and directly challenge established leaders. Competitive pressures in India escalated further in July 2025, when the Competition Commission of India initiated a new antitrust probe into Asian Paints over alleged dealer exclusivity practices. Despite this scrutiny, Asian Paints reported 10.9% domestic decorative volume growth in November 2025, supported by festive season demand and housing recovery across rural and urban markets. Regional dominance shifted in October 2025, when Sherwin-Williams completed its $1.15 billion acquisition of BASF’s Suvinil business in Brazil, integrating two production facilities and approximately 1,000 employees into its Consumer Brands Group and strengthening its South American architectural paint footprint. The global competitive landscape was further reshaped in November 2025, when AkzoNobel and Axalta announced a merger of equals valued at roughly $25 billion, targeting $600 million in annual synergies upon expected closure in late 2026 or early 2027.

Innovation and branding strategies remain central to differentiation within the decorative coatings sector. In September 2024, Jotun introduced its Nuances 2025 collection, featuring 30 curated shades developed through its Colour Tech Lab to enhance durability and interior depth. AkzoNobel unveiled its Rhythm of Blues 2026 palette in September 2025, rolling out indigo-led themes across Dulux and Sikkens brands to address consumer demand for calming residential aesthetics. PPG followed in October 2025 with its Secret Safari 2026 Color of the Year, positioning botanical yellow-green tones across residential and commercial spaces. Nippon Paint Thailand initiated its Inspired by You 2024–2026 strategy in January 2024, targeting 15 billion baht in revenue through green building collaborations and developer-focused marketing programs. Product technology advancements accelerated in February 2025, when several manufacturers piloted self-healing decorative paints utilizing microencapsulation systems designed to extend repainting cycles in high-traffic commercial interiors. Regulatory reformulation intensified as the industry prepared for compliance with EU Regulation 2024/3190, prompting major players in early 2026 to commercialize BPXni and PFAS-free decorative coatings ahead of the July 2026 ban affecting food-contact and residential applications. This regulatory pivot is reshaping resin selection, additive chemistry, and raw material sourcing across the global decorative paints value chain.

Trends and Opportunities in the Global Decorative Paints Market

Functional Wellness Claims and Air-Purifying Paint Systems

- Indoor air quality has emerged as a decisive purchase driver in the decorative paints market, transforming coatings into active contributors to healthier living environments. In May 2025, peer-reviewed studies confirmed that decorative paints formulated with titanium dioxide nanoparticles and plant-derived antioxidants such as green tea catechins can reduce indoor volatile organic compound concentrations by up to 50% on wood substrates and approximately 25% on paper surfaces within 60 minutes of ambient light exposure. This photocatalytic oxidation mechanism actively breaks down airborne pollutants rather than masking them, shifting decorative paints from passive low-VOC products to active air purification systems.

- The same light-activated chemistry is gaining traction in institutional environments. Hospitals, schools, and public infrastructure projects are increasingly specifying photocatalytic decorative coatings due to their ability to eliminate up to 95% of airborne pathogens and microbial contaminants. This has accelerated a move away from conventional biocide-based antimicrobial additives toward continuous, light-driven molecular degradation of pollutants. For paint manufacturers, wellness-oriented performance claims are becoming a core premiumization lever, particularly in urban residential and healthcare renovation markets.

Rapid Scale-Up of Circular and Bio-Based Decorative Paint Formulations

- Sustainability mandates and consumer eco-consciousness are accelerating the replacement of petroleum-derived binders with renewable and circular alternatives. In January 2024, AkzoNobel introduced a next-generation interior decorative paint range featuring more than 40% bio-based content and near-zero VOC emissions. This launch set a benchmark that has shaped the 2025 competitive landscape, with eco-premium decorative lines increasingly incorporating resins derived from soy, algae, and wood-based tall oil.

- Packaging circularity is advancing in parallel. By late 2025, AkzoNobel reported that post-consumer recycled plastic content across its European decorative paint packaging averaged 43 %, with selected product ranges reaching up to 90% recycled material. In the United Kingdom, coordinated recycling programs have already processed more than one million used paint cans, with targets to triple volumes by the end of 2025 through partnerships with waste management and recycling specialists. These initiatives are strengthening brand positioning while addressing regulatory and retailer-driven sustainability scorecards.

High-Impact Growth Opportunities in Performance and Smart Coatings

High-Reflectance Paints for Climate Resilience and Energy Efficiency

- The intensification of urban heat island effects and stricter building energy codes are creating strong demand for high-reflectance exterior decorative paints. Experimental evaluations published in February 2025 demonstrated that advanced cool roof coatings can lower roof surface temperatures by between 8.7 degrees Celsius and 34.2 degrees Celsius. Under peak solar exposure, this translates into surface heat reductions of up to 53.6 %, significantly limiting thermal transfer into building interiors.

- Regulatory alignment is accelerating adoption. Energy efficiency standards such as California’s Title 24 are positioning reflective decorative coatings as a primary compliance tool. In large commercial and mixed-use developments, these coatings can reduce peak summer air conditioning energy demand by an estimated 15 to 20 %, directly supporting Energy Star certification and operational cost reduction. As climate adaptation becomes a priority in urban planning, high-reflectance decorative paints are shifting from niche roofing solutions to mainstream exterior finishing systems.

Smart Decorative Paints with Dynamic and Diagnostic Capabilities

- Advances in nanotechnology and embedded electronics are opening a new frontier for smart decorative paints that respond to environmental conditions or generate actionable data. Thermochromic formulations introduced in 2025 utilize leuco dye technology to reversibly change color in response to temperature fluctuations. In industrial and low-slope roofing applications, these coatings absorb heat during colder periods and reflect it during warmer conditions, delivering passive energy savings through crystalline phase transitions without mechanical intervention.

- At the same time, leading manufacturers such as Nippon Paint and PPG are exploring decorative paints embedded with passive RFID elements and conductive additives. These smart coatings enable touch-sensitive walls and IoT-enabled surfaces that integrate with building management and HVAC systems. By capturing wall-surface temperature and humidity data, such paints support real-time indoor climate optimization, positioning decorative coatings as active components within smart home and smart building ecosystems rather than static finishes.

Decorative Paints Market Share and Segmentation Insights

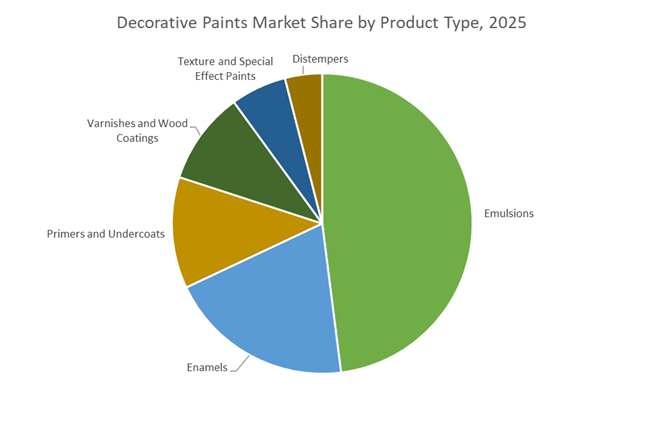

Product Type Distribution: Emulsions Lead Volume as Texture Paints Gain Design Momentum

Emulsion paints account for 48% of decorative paint demand in 2025, driven by water-based formulations offering low odor, fast drying, and ease of application for interior and exterior walls. Growing DIY activity and preference for washable matte finishes continue to propel this segment. Enamels maintain a strong presence for doors, trims, and metal surfaces, delivering high gloss and durability with improving adoption of waterborne technologies. Primers and undercoats remain essential for adhesion and stain blocking, reflecting professional emphasis on surface preparation. Varnishes and wood coatings support furniture and flooring markets, combining aesthetic enhancement with abrasion resistance. Texture and special-effect paints are gaining traction as consumers seek personalized interiors through metallic, chalkboard, and faux finishes. Distempers represent a declining segment in urban areas but retain relevance in cost-sensitive rural and developing markets.

Resin Type Breakdown: Acrylics Dominate as Polyurethane Serves Premium Finishes

Acrylic resins command 55% of decorative paint binder usage, supported by excellent UV stability, color retention, and flexibility that underpin modern waterborne emulsions for exterior durability. Alkyd resins remain important in enamels and varnishes, with newer high-solids and waterborne alkyds preserving traditional flow and leveling while reducing environmental impact. Vinyl resins serve cost-effective interior paints, often blended with acrylics to balance performance and price. Polyurethane resins occupy premium niches in wood coatings and high-traffic floor paints, delivering superior abrasion and chemical resistance. Epoxy resins remain specialized, primarily used in garage floors, basements, and wet-area wall systems requiring extreme durability and chemical protection.

Competitive Landscape of the Decorative Paints Market

The Decorative Paints Market is highly consolidated, led by multinational coating majors leveraging color leadership, sustainability-driven formulations, and deep contractor networks. Competition is intensifying around low-VOC architectural paints, bio-based resins, digital color ecosystems, and premium exterior durability, as players race to capture growth from urbanization, renovation cycles, and emerging-market housing demand.

AkzoNobel drives consolidation and color innovation in global decorative coatings

AkzoNobel continues to shape the decorative paints landscape through aggressive consolidation and trend-led product development. In late 2025, the company prioritized a proposed merger with Axalta, aiming to create the world’s largest coatings entity with unmatched R&D scale across decorative and industrial segments. Holding an estimated 15–20% global market share in early 2026, AkzoNobel also launched its “Rhythm of Blues” 2026 Color of the Year collection, blending aesthetics with emotional wellness. Backed by a strong 2025 execution year and margin expansion, the company’s “Space and Pace” strategy targets zero-carbon operations by 2040, emphasizing bio-based resins and recyclable, command-removal coatings for circular renovation cycles.

Sherwin-Williams strengthens professional dominance and Latin American presence

Sherwin-Williams remains the benchmark for professional-grade architectural coatings, dominating North America while accelerating expansion in high-growth regions. The late-2025 acquisition of BASF’s Brazilian decorative paints business significantly strengthened its Latin American footprint. For 2026, Sherwin-Williams is promoting “Strength in Simplicity” across its Color of the Year portfolio, aligning durability with adaptable design. The company is consistently ranked a preferred brand among professional painters due to its contractor-centric product lines and streamlined procurement systems. Strategically, Sherwin-Williams is prioritizing lifecycle ROI, developing high-performance finishes that extend repaint intervals for commercial properties, multifamily housing, and high-traffic interiors, reinforcing its leadership in premium architectural coatings.

Asian Paints dominates India through scale, services, and hyper-localization

Asian Paints is the undisputed leader in India’s decorative paints sector, commanding over 50% market share and delivering 10.9% volume growth in late 2025, far above global averages. Beyond paints, the company has built a powerful home décor ecosystem spanning modular kitchens, wardrobes, and professional painting services via its Beautiful Homes platform. In 2026, Asian Paints intensified its regionalization strategy, rolling out state-specific packaging and localized marketing to penetrate Tier-2 and Tier-3 cities. Its core competitive advantage lies in scale: 65,000+ dealers and over 100,000 retail touchpoints, enabling unmatched last-mile reach across South Asia’s fast-growing residential renovation market.

PPG advances biophilic design and AI-enabled color customization

PPG leverages technical performance and design-forward innovation to maintain a strong global decorative coatings position, holding an estimated 12–16% market share in 2026. Its 2026 Color of the Year, “Secret Safari,” reflects rising demand for biophilic, nature-inspired interiors, supported by the broader “Parallels” palette of 36 curated shades addressing climate and social themes. PPG is heavily investing in digital color ecosystems and AI visualization tools, allowing architects and homeowners to preview complex palettes in real time. The company also continues expanding eco-friendly architectural paints and antimicrobial wall finishes, positioning itself at the intersection of sustainability, wellness-driven interiors, and advanced coatings performance.

Nippon Paint accelerates Asia growth with functional decorative technologies

Nippon Paint operates an “Asset Assembler” model, acquiring regional leaders to build a decentralized global footprint, with Asia as its primary growth engine. In 2026, the company launched an “India-First” strategy under a unified operating model, targeting 8–9% revenue growth and 10–12% EPS growth, driven largely by India and China. Nippon Paint leads in advanced functionality, offering anti-viral, heat-shielding, and self-cleaning exterior coatings tailored for tropical and high-pollution climates. Its NIPSEA Group R&D backbone delivers low-VOC, weather-resistant formulations, giving Nippon a competitive edge in emerging markets where durability, energy efficiency, and regulatory compliance are increasingly decisive.

Jotun builds premium decorative leadership through durability and sustainability

Jotun Group has carved out a strong premium decorative paints position, particularly in the Middle East and Scandinavia, reporting a record start to 2025–2026 despite global volatility. Renowned for extreme weather-resistant coatings, Jotun protects villas, high-rise buildings, and coastal properties using marine-grade decorative technologies. Its 2026 strategy centers on “Sustainability at Jotun,” prioritizing lower-carbon manufacturing and reduced solvent content across its global portfolio. High brand loyalty among architects is reinforced through Jotun’s Global Color Trends research, which consistently influences upscale residential and commercial projects, positioning the company as a leader in long-life exterior protection and premium architectural finishes.

India: Infrastructure-Led Demand and Rapid Competitive Reordering

India’s decorative paints market is being structurally reshaped by public capital expenditure, private capacity creation, and unprecedented competitive churn. In the 2025–2026 interim budget, the Government of India raised infrastructure capital outlay by 11.1% to USD 133.86 billion, directly translating into sustained demand for architectural coatings across highways, metro corridors, smart cities, and public housing projects. This policy-led demand is reinforcing paint consumption beyond cyclical real estate activity, anchoring growth in repainting and first-time application across Tier II and Tier III cities.

On the supply side, Asian Paints announced a ₹2,000 crore investment in late 2025 to commission a 400,000 KL per annum manufacturing facility in Madhya Pradesh, explicitly aligned with the Housing for All initiative. Competitive dynamics have intensified sharply following the 2024 entry of Birla Opus under Aditya Birla Group, which scaled to a high single-digit share by October 2025, one of the fastest ramps by a new entrant in the segment’s history. Consolidation has further altered market structure, with the Competition Commission of India approving JSW Paints’ acquisition of a 75% stake in AkzoNobel India in September 2025. Regulatory tightening is also reshaping formulations, as revised BIS norms cap lead content at 90 ppm and VOCs at 50 g/L, accelerating the shift toward compliant plastic emulsions. India’s role is simultaneously globalizing, with Berger Paints Emirates committing ₹340 crore to an Abu Dhabi plant to position India-linked manufacturing as an export hub for the Middle East.

China: Renovation Demand and Green Formulation Mandates

China’s decorative paints market is transitioning from new-build dependency toward renovation-driven stability, supported by policy intervention and sustainability mandates. The 2025 Petrochemical Steady Growth Plan targets a 5% annual increase in value addition, with explicit emphasis on refurbishing aging urban residential stock. This has created consistent demand for interior and exterior repainting, particularly in first- and second-tier cities where building lifecycles are entering major maintenance phases.

Sustainability is becoming a binding requirement rather than a brand differentiator. In March 2025, Nippon Paint China entered a strategic alliance with Evonik to co-develop zero-VOC decorative solutions for the APAC region. This collaboration anticipates national standards taking effect in 2026 that require 70% of urban buildings in major provinces to use bio-based or waterborne exterior coatings, aligned with China’s 2030 carbon peak commitments. As a result, supplier competitiveness is increasingly determined by formulation chemistry and additive innovation rather than pricing alone.

United States: Portfolio Rationalization and Digitalized Consumption

The U.S. decorative paints market in 2025 is characterized by regulatory convergence, corporate portfolio reshaping, and digitally enabled purchasing behavior. Following EPA updates on vapor pressure and carbon atom content, manufacturers have converted roughly 85% of premium interior paint lines to near-zero-VOC waterborne formulations, making regulatory compliance a baseline rather than a premium feature. This has compressed differentiation at the formulation level while raising barriers for smaller regional brands.

Strategically, PPG Industries exited the North American architectural coatings business in late 2024 through a USD 550 million sale to American Industrial Partners, signaling a decisive pivot toward industrial and performance coatings. At the retail and contractor interface, players like Sherwin-Williams are embedding smart-home and AI visualization tools into the buying process, allowing consumers and professionals to test palettes digitally before purchase. E-commerce penetration is rising fastest in the professional channel, with major home improvement retailers reporting double-digit growth in digital sales for contractor-grade decorative paints during 2025.

European Union (Germany and Netherlands): Scale, Sustainability, and Structural Consolidation

The European decorative paints landscape is increasingly defined by sustainability economics and consolidation-led resilience. AkzoNobel reported in Q3 2025 that decorative paint volumes were supported by a shift toward mass-balanced bio-circular raw materials, part of a longer-term objective to cut the carbon footprint of its Dulux portfolio by 50% by 2030. This approach allows compliance with tightening EU environmental frameworks without disrupting supply continuity.

Industry structure changed materially in November 2025, when AkzoNobel and Axalta announced an all-stock merger, creating a combined global coatings entity valued at USD 25 billion. Parallel internal restructuring through AkzoNobel’s Industrial Excellence program delivered cost savings ahead of schedule in 2025, preserving profitability despite macroeconomic volatility in Germany and the Netherlands. In Europe, competitive advantage in decorative paints is increasingly tied to balance sheet strength, supply chain efficiency, and credible decarbonization pathways.

Comparative Snapshot: Decorative Paints Market by Country

Decorative Paints Market County Level Snapshot

|

Region

|

Primary Demand Driver

|

Competitive Dynamic

|

Structural Direction

|

|

India

|

Infrastructure spending and housing

|

Rapid new entry and consolidation

|

High-growth, export-capable hub

|

|

China

|

Urban renovation and green mandates

|

Chemistry-led differentiation

|

Sustainability-driven repaint cycle

|

|

United States

|

Regulatory reform and digital retail

|

Portfolio rationalization

|

Premiumization with digital tools

|

|

EU (Germany & Netherlands)

|

Carbon reduction and scale efficiency

|

Mega-mergers and cost restructuring

|

Consolidated, sustainability-led market

|

Decorative Paints Market Report Scope

Decorative Paints market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$93.4 Billion

|

|

Market Size (2034)

|

$134.1 Billion

|

|

Market Growth Rate

|

4.1%

|

|

Segments

|

By Product Type (Emulsions, Enamels, Distempers, Primers and Undercoats, Varnishes and Wood Coatings, Texture and Special Effect Paints), By Technology (Water-Based Coatings, Solvent-Based Coatings, Powder Coatings, UV-Curable Coatings), By Application (Residential, Non-Residential), By Resin Type (Acrylic, Alkyd, Polyurethane, Epoxy, Vinyl), By User Category (Professional, Do-It-Yourself)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sherwin-Williams Company, Akzo Nobel N.V., PPG Industries, Inc., Nippon Paint Holdings Co., Ltd., Asian Paints Limited, Kansai Paint Co., Ltd., Jotun A.S., Masco Corporation, RPM International Inc., Berger Paints India Limited, Hempel A.S., Axalta Coating Systems Ltd., DAW SE, Tikkurila Oyj, JSW Paints Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Decorative Paints Market Segmentation

By Product Type

- Emulsions

- Enamels

- Distempers

- Primers and Undercoats

- Varnishes and Wood Coatings

- Texture and Special Effect Paints

By Technology

- Water-Based Coatings

- Solvent-Based Coatings

- Powder Coatings

- UV-Curable Coatings

By Application

- Residential

- Non-Residential

By Resin Type

- Acrylic

- Alkyd

- Polyurethane

- Epoxy

- Vinyl

By User Category

- Professional

- Do-It-Yourself

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Decorative Paints Industry

- Sherwin-Williams Company

- Akzo Nobel N.V.

- PPG Industries, Inc.

- Nippon Paint Holdings Co., Ltd.

- Asian Paints Limited

- Kansai Paint Co., Ltd.

- Jotun A.S.

- Masco Corporation

- RPM International Inc.

- Berger Paints India Limited

- Hempel A.S.

- Axalta Coating Systems Ltd.

- DAW SE

- Tikkurila Oyj

- JSW Paints Limited

*- List not Exhaustive