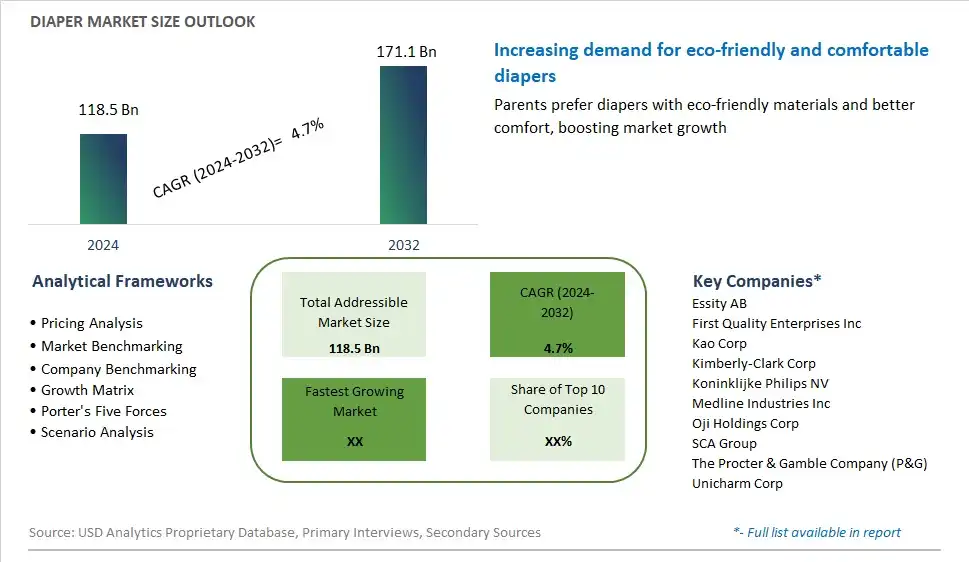

Global Diaper Market Size is valued at $118.5 Billion in 2024 and is forecast to register a growth rate (CAGR) of 4.7% to reach $171.1 Billion by 2032.

The global Diaper Market Comprehensive Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Type (Baby Diapers, Adult Diapers), By Distribution Channel (Supermarkets/ Hypermarkets, Pharmacy Stores, Online Channel), By End-User (Infant, Adult)

An Introduction to Diaper Market

The diaper market continues to expand in 2024, driven by factors such as rising birth rates, increasing urbanization, and growing awareness regarding hygiene and convenience. Modern diapers offer superior absorption, leakage protection, and comfort, making them indispensable for parents seeking reliable solutions for infant care. Moreover, innovations in materials and design have led to the development of eco-friendly and biodegradable diapers, catering to environmentally conscious consumers. Additionally, the adult diaper segment is witnessing significant growth due to demographic trends such as aging populations and a higher prevalence of conditions like incontinence. With manufacturers focusing on product enhancements such as breathable fabrics, stretchable waistbands, and wetness indicators, the diaper market is poised for continued expansion, both in developed and emerging economies. Furthermore, initiatives promoting diaper affordability and accessibility, particularly in underserved regions, are driving market penetration and fostering inclusive growth.

Diaper Competitive Landscape

The market report analyses the leading companies in the industry including Essity AB, First Quality Enterprises Inc, Kao Corp, Kimberly-Clark Corp, Koninklijke Philips NV, Medline Industries Inc, Oji Holdings Corp, SCA Group, The Procter & Gamble Company (P&G), Unicharm Corp, and Others.

Diaper Market Dynamics

Diaper Market Trend: Growing Demand for Eco-Friendly and Sustainable Diapers

A notable trend in the diaper market is the growing demand for eco-friendly and sustainable diaper options. With increasing environmental consciousness among consumers, there is a shift towards eco-friendly products that minimize environmental impact and promote sustainability. This trend is driven by concerns over the environmental footprint of traditional disposable diapers, which contribute to landfill waste and pollution due to their non-biodegradable materials. As a result, there is rising interest in biodegradable diapers made from renewable and compostable materials, as well as cloth diapering systems that can be reused multiple times, reducing waste and conserving resources. Manufacturers in the diaper market are responding to this trend by introducing eco-friendly diaper alternatives and incorporating sustainable practices into their production processes to appeal to environmentally conscious consumers.

Market Driver: Increasing Birth Rates and Urbanization

A significant driver behind the demand for diapers is the increasing birth rates and urbanization worldwide. With growing populations, particularly in urban areas where access to modern conveniences is prevalent, there is a steady demand for diapers as essential baby care products. Additionally, rising disposable incomes and changing lifestyles contribute to higher consumption of diapers, as parents prioritize convenience and hygiene for their infants and toddlers. Moreover, as more women enter the workforce and families opt for smaller living spaces, there is greater reliance on disposable diapers for their convenience and ease of use compared to cloth diapering. This demographic and lifestyle shift drives market growth and presents opportunities for diaper manufacturers to meet the evolving needs of families in urban settings.

Market Opportunity: Innovation in Diaper Design and Technology

An opportunity for the diaper market lies in innovation in diaper design and technology to improve performance and address consumer preferences. Manufacturers can explore opportunities to develop diapers with enhanced absorbency, leak protection, and comfort features to provide a better experience for both babies and caregivers. This includes innovations such as superabsorbent polymers, moisture-wicking liners, stretchable waistbands, and breathable materials that help prevent diaper rash and discomfort. Furthermore, advancements in smart diaper technology, such as sensors that monitor moisture levels and alert caregivers when a diaper change is needed, offer convenience and peace of mind to busy parents. By investing in research and development efforts to innovate and differentiate their products, diaper brands can maintain a competitive edge in the market and capitalize on opportunities for growth amidst changing consumer preferences and technological advancements.

Diaper Market Share Analysis: Baby Diapers held the dominant market share in 2024

Within the Diaper Market segmented by type, baby diapers emerge as the largest segment, commanding a substantial share of the market. This dominance can be attributed to several key factors. Firstly, the sheer size of the infant population globally fuels consistent demand for baby diapers, as newborns and infants require frequent diaper changes throughout the day. Additionally, factors such as increasing birth rates in emerging economies and the rising trend of nuclear families contribute to sustained growth in the baby diaper segment. Further, advancements in diaper technology, including enhanced absorbency, leakage protection, and skin-friendly materials, continue to attract parents seeking convenience and comfort for their babies. Furthermore, aggressive marketing strategies by leading diaper manufacturers, coupled with extensive distribution networks, ensure widespread availability and accessibility of baby diapers across various retail channels. As a result, the baby diaper segment maintains its position as the largest segment in the diaper market, poised for continued expansion in the foreseeable future.

Diaper Market Share Analysis: Online Channel market is poised to register the fastest growth rae over the forecast period to 2032

Among the distribution channels in the Diaper Market, the online channel is the fastest-growing segment, propelled by several compelling factors. Firstly, the increasing penetration of internet and smartphone usage globally has significantly augmented the e-commerce landscape, providing consumers with greater convenience and accessibility to purchase diapers online. This trend is particularly pronounced among tech-savvy parents who value the convenience of doorstep delivery and the ability to browse a wide range of diaper brands and variants online. Additionally, the COVID-19 pandemic has further accelerated the shift towards online shopping, as consumers prioritize safety and contactless transactions. Furthermore, aggressive marketing strategies and promotional campaigns by e-commerce platforms and diaper manufacturers have heightened consumer awareness and incentivized online purchases through discounts, subscription services, and bundle deals. Further, the online channel offers a platform for niche and emerging diaper brands to reach a wider audience, fostering competition and innovation in the market. As a result, the online channel stands out as the fastest-growing segment in the diaper market, poised to continue its upward trajectory amidst evolving consumer preferences and digital advancements.

Diaper Market Share Analysis: Infant held the dominant market share in 2024

Within the Diaper Market segmented by end-user, the infant segment stands as the largest, exerting significant influence and capturing a substantial share of the market. This dominance can be attributed to several pivotal factors. Firstly, the global birth rate continues to drive consistent demand for infant diapers, as newborns and infants require frequent diaper changes for proper hygiene and comfort. Additionally, societal norms and cultural practices prioritize the use of diapers for infants as an essential component of childcare routines. Further, the baby care industry's focus on product innovation, including advancements in diaper technology such as enhanced absorbency, leakage protection, and hypoallergenic materials, continues to attract parents seeking high-quality diaper solutions for their babies. Furthermore, extensive marketing efforts by leading diaper manufacturers, coupled with widespread availability through various retail channels, ensure the accessibility and affordability of infant diapers to a broad consumer base. As a result, the infant segment maintains its position as the largest segment in the diaper market, poised for sustained growth driven by demographic trends and evolving consumer preferences.

Diaper Market Segmentation

By Type

Baby Diapers

Adult Diapers

By Distribution Channel

Supermarkets/ Hypermarkets

Pharmacy Stores

Online Channel

By End-User

Infant

Adult

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Diaper Companies Profiled in the Study

Essity AB

First Quality Enterprises Inc

Kao Corp

Kimberly-Clark Corp

Koninklijke Philips NV

Medline Industries Inc

Oji Holdings Corp

SCA Group

The Procter & Gamble Company (P&G)

Unicharm Corp

*- List Not Exhaustive

Chapter 1. TABLE OF CONTENTS

Chapter 2. Introduction to Diaper Market

2.1. Market Overview

2.2. Key Statistics and Report Highlights

2.3. Scope of the Comprehensive Study

2.3.1. Market Definition

2.3.2 Countries and Regions Covered

2.3.3 Research Objective

2.3.4 Units, Currency, and Conversions

2.3.5 Industry Value Chain

2.4. Key Market Segments

2.5. Key Companies

2.6. Study Period

Chapter 3. Strategic Analysis Review

3.1. Diaper Pricing Analysis and Forecast

3.2. Porter’s Five Forces

3.3. Market Ecosystem

3.4. SWOT Analysis

3.5. Regulatory Scenario

3.3. Effects of Inflation, Russia-Ukraine War, moderating economic growth, and other macroeconomic factors

Chapter 4. Competitive Landscape

4.1. Market Share Analysis

4.1.1. Global Diaper Market Share by Company, 2023

4.1.2. Product Offerings of Leading Diaper Companies

4.2. Market Entropy

4.2.1. New Product Launches in the Industry

4.2.2. Mergers, Acquisitions, Joint ventures, and Partnerships

4.3. Key Strategies and Best Practices

Chapter 5. Global Market Projections: Best, Reference, and Low Case Scenarios

5.1. Growth Analysis- Case Scenario Definitions

5.2. Low Growth Case Scenario Forecasts

5.3. Reference Growth Case Scenario Forecasts

5.4. High Growth Case Scenario Forecasts

Chapter 6. Market Dynamics

6.1. Diaper Market Drivers

6.2. Diaper Market Challenges

6.6. Diaper Market Opportunities

6.4. Diaper Market Trends

Chapter 7. Global Diaper Market Outlook Trends

7.1. Global Diaper Revenue (USD Million) and CAGR (%) by Type (2021-2032)

7.2. Global Diaper Revenue (USD Million) and CAGR (%) by Application (2021-2032)

7.3. Global Diaper Revenue (USD Million) and CAGR (%) by Product (2021-2032)

By Type

Baby Diapers

Adult Diapers

By Distribution Channel

Supermarkets/ Hypermarkets

Pharmacy Stores

Online Channel

By End-User

Infant

Adult

Chapter 8. Global Diaper Regional Analysis and Outlook

8.1. Global Diaper Revenue (USD Million) By Regions (2021- 2032)

8.2. North America Diaper Revenue (USD Million) by Country (2021-2032)

8.2.1. United States Diaper Regional Analysis and Outlook

8.2.2. Canada Diaper Regional Analysis and Outlook

8.2.3. Mexico Diaper Regional Analysis and Outlook

8.3. Europe Diaper Revenue (USD Million), by Country (2021-2032)

8.3.1. Germany Diaper Regional Analysis and Outlook

8.3.2. France Diaper Regional Analysis and Outlook

8.3.3. United Kingdom Diaper Regional Analysis and Outlook

8.3.4. Spain Diaper Regional Analysis and Outlook

8.3.5. Italy Diaper Regional Analysis and Outlook

8.3.6. Russia Diaper Regional Analysis and Outlook

8.3.7. Rest of Europe Diaper Regional Analysis and Outlook

8.4. Asia Pacific Diaper Revenue (USD Million) by Country (2021-2032)

8.4.1. China Diaper Regional Analysis and Outlook

8.4.2. Japan Diaper Regional Analysis and Outlook

8.4.3. India Diaper Regional Analysis and Outlook

8.4.4. South Korea Diaper Regional Analysis and Outlook

8.4.5. Australia Diaper Regional Analysis and Outlook

8.4.6. South East Asia Diaper Regional Analysis and Outlook

8.4.7. Rest of Asia Pacific Diaper Regional Analysis and Outlook

8.5. South America Diaper Revenue (USD Million), by Country (2021-2032)

8.5.1. Brazil Diaper Regional Analysis and Outlook

8.5.2. Argentina Diaper Regional Analysis and Outlook

8.5.3. Rest of South America Diaper Regional Analysis and Outlook

8.6. Middle East and Africa Diaper Revenue (USD Million) by Country (2021-2032)

8.6.1. Middle East Diaper Regional Analysis and Outlook

8.6.2. Africa Diaper Regional Analysis and Outlook

Chapter 9. North America Diaper Analysis and Outlook

9.1. North America Diaper Revenue (USD Million) by Segments (2021-2032)

9.1.1. North America Diaper Revenue (USD Million) by Type (2021-2032)

9.1.2. North America Diaper Revenue (USD Million) by Application (2021-2032)

9.1.3. North America Diaper Revenue (USD Million) by Product (2021-2032)

By Type

Baby Diapers

Adult Diapers

By Distribution Channel

Supermarkets/ Hypermarkets

Pharmacy Stores

Online Channel

By End-User

Infant

Adult

Chapter 10. Europe Diaper Analysis and Outlook

10.1. Europe Diaper Revenue (USD Million), by Segments (USD Million) (2021-2032)

10.1.1. Europe Diaper Revenue (USD Million) by Type (2021-2032)

10.1.2. Europe Diaper Revenue (USD Million) by Application (2021-2032)

10.1.3. Europe Diaper Revenue (USD Million) by Product (2021-2032)

By Type

Baby Diapers

Adult Diapers

By Distribution Channel

Supermarkets/ Hypermarkets

Pharmacy Stores

Online Channel

By End-User

Infant

Adult

Chapter 11. Asia Pacific Diaper Analysis and Outlook

11.1. Asia Pacific Diaper Revenue (USD Million), and Revenue (USD Million) by Segments (2021-2032)

11.1.1. Asia Pacific Diaper Revenue (USD Million) by Type (2021-2032)

11.1.2. Asia Pacific Diaper Revenue (USD Million) by Application (2021-2032)

11.1.3. Asia Pacific Diaper Revenue (USD Million) by Product (2021-2032)

By Type

Baby Diapers

Adult Diapers

By Distribution Channel

Supermarkets/ Hypermarkets

Pharmacy Stores

Online Channel

By End-User

Infant

Adult

Chapter 12. South America Diaper Analysis and Outlook

12.1. South America Diaper Revenue (USD Million), by Segments (2021-2032)

12.1.1. South America Diaper Revenue (USD Million) by Type (2021-2032)

12.1.2. South America Diaper Revenue (USD Million) by Application (2021-2032)

12.1.3. South America Diaper Revenue (USD Million) by Product (2021-2032)

By Type

Baby Diapers

Adult Diapers

By Distribution Channel

Supermarkets/ Hypermarkets

Pharmacy Stores

Online Channel

By End-User

Infant

Adult

Chapter 13. Middle East and Africa Diaper Analysis and Outlook

13.1. Middle East and Africa Diaper Revenue (USD Million), by Segments (2021-2032)

13.1.1. Middle East and Africa Diaper Revenue (USD Million) by Type (2021-2032)

13.1.2. Middle East and Africa Diaper Revenue (USD Million) by Application (2021-2032)

13.1.3. Middle East and Africa Diaper Revenue (USD Million) by Product (2021-2032)

By Type

Baby Diapers

Adult Diapers

By Distribution Channel

Supermarkets/ Hypermarkets

Pharmacy Stores

Online Channel

By End-User

Infant

Adult

Chapter 14. Diaper Company Profiles

14.1 Business Overview

14.2 Product Profiles

14.3 SWOT Profiles

14.5 Recent Developments

14.6 Financial Profile

List of Companies

Essity AB

First Quality Enterprises Inc

Kao Corp

Kimberly-Clark Corp

Koninklijke Philips NV

Medline Industries Inc

Oji Holdings Corp

SCA Group

The Procter & Gamble Company (P&G)

Unicharm Corp

15. Methodology and Data Sources

15.1 Customization Offerings

15.2 Subscription Services

15.3 Related Reports

15.4 Publisher Expertise

LIST OF TABLES

Table 1 Market Segmentation Analysis

Table 2 Global Diaper Market Share of Leading Companies, 2023

Table 3 Product Offerings of Leading Companies

Table 4 Low Growth Scenario Forecasts

Table 5 Reference Case Growth Scenario

Table 6 High Growth Case Scenario

Table 7 Global Diaper Revenue (USD Million) And CAGR (%) By Type (2021-2032)

Table 8 Global Diaper Revenue (USD Million) And CAGR (%) By Application (2021-2032)

Table 9 Global Diaper Revenue (USD Million) And CAGR (%) By Product (2021-2032)

Table 10 Global Diaper Market Revenue (USD Million) By Regions (2021-2032)

Table 11 Global Diaper Market Share (%) By Regions (2021-2032)

Table 12 North America Diaper Revenue (USD Million) By Country (2021-2032)

Table 13 Europe Diaper Revenue (USD Million) By Country (2021-2032)

Table 14 Asia Pacific Diaper Revenue (USD Million) By Country (2021-2032)

Table 15 South America Diaper Revenue (USD Million) By Country (2021-2032)

Table 16 Middle East and Africa Diaper Revenue (USD Million) By Region (2021-2032)

Table 17 North America Diaper Revenue (USD Million) By Type (2021-2032)

Table 18 North America Diaper Revenue (USD Million) By Application (2021-2032)

Table 19 North America Diaper Revenue (USD Million) By Product (2021-2032)

Table 20 Europe Diaper Revenue (USD Million) By Type (2021-2032)

Table 21 Europe Diaper Revenue (USD Million) By Application (2021-2032)

Table 22 Europe Diaper Revenue (USD Million) By Product (2021-2032)

Table 23 Asia Pacific Diaper Revenue (USD Million) By Type (2021-2032)

Table 24 Asia Pacific Diaper Revenue (USD Million) By Application (2021-2032)

Table 25 Asia Pacific Diaper Revenue (USD Million) By Product (2021-2032)

Table 26 South America Diaper Revenue (USD Million) By Type (2021-2032)

Table 27 South America Diaper Revenue (USD Million) By Application (2021-2032)

Table 28 South America Diaper Revenue (USD Million) By Product (2021-2032)

Table 29 Middle East and Africa Diaper Revenue (USD Million) By Type (2021-2032)

Table 30 Middle East and Africa Diaper Revenue (USD Million) By Application (2021-2032)

Table 31 Middle East and Africa Diaper Revenue (USD Million) By Product (2021-2032)

LIST OF FIGURES

Figure 1. Market Scope

Figure 2. Pricing Forecasts Per Unit, 2023- 2032

Figure 3. Porter’s Five Forces

Figure 4. Global Diaper Market Revenue (USD Million) By Regions (2021-2032)

Figure 5. Global Diaper Market Share (%) By Regions (2023)

Figure 6. North America Diaper Revenue (USD Million) By Country (2021-2032)

Figure 7. United States Diaper Revenue (USD Million) By Country (2021-2032)

Figure 8. Canada Diaper Revenue (USD Million) By Country (2021-2032)

Figure 9. Mexico Diaper Revenue (USD Million) By Country (2021-2032)

Figure 10. Europe Diaper Revenue (USD Million) By Country (2021-2032)

Figure 11. Germany Diaper Revenue (USD Million) By Country (2021-2032)

Figure 12. France Diaper Revenue (USD Million) By Country (2021-2032)

Figure 13. United Kingdom Diaper Revenue (USD Million) By Country (2021-2032)

Figure 14. Spain Diaper Revenue (USD Million) By Country (2021-2032)

Figure 15. Italy Diaper Revenue (USD Million) By Country (2021-2032)

Figure 16. Russia Diaper Revenue (USD Million) By Country (2021-2032)

Figure 17. Rest of Europe Diaper Revenue (USD Million) By Country (2021-2032)

Figure 11. Asia Pacific Diaper Revenue (USD Million) By Country (2021-2032)

Figure 12. China Diaper Revenue (USD Million) By Country (2021-2032)

Figure 13. Japan Diaper Revenue (USD Million) By Country (2021-2032)

Figure 14. India Diaper Revenue (USD Million) By Country (2021-2032)

Figure 15. South Korea Diaper Revenue (USD Million) By Country (2021-2032)

Figure 16. Australia Diaper Revenue (USD Million) By Country (2021-2032)

Figure 17. South East Asia Diaper Revenue (USD Million) By Country (2021-2032)

Figure 18. South America Diaper Revenue (USD Million) By Country (2021-2032)

Figure 19. Brazil Diaper Revenue (USD Million) By Country (2021-2032)

Figure 20. Argentina Diaper Revenue (USD Million) By Country (2021-2032)

Figure 21. Rest of Asia Pacific Diaper Revenue (USD Million) By Country (2021-2032)

Figure 22. Middle East and Africa Diaper Revenue (USD Million) By Region (2021-2032)

Figure 23. Saudi Arabia Diaper Revenue (USD Million) By Region (2021-2032)

Figure 24. The UAE Diaper Revenue (USD Million) By Region (2021-2032)

Figure 25. Rest of Middle East Diaper Revenue (USD Million) By Region (2021-2032)

Figure 26. South Africa Diaper Revenue (USD Million) By Region (2021-2032)

Figure 27. Africa Diaper Revenue (USD Million) By Region (2021-2032)

Figure 28. North America Diaper Revenue (USD Million) By Type (2021-2032)

Figure 29. North America Diaper Revenue (USD Million) By Application (2021-2032)

Figure 30. North America Diaper Revenue (USD Million) By Product (2021-2032)

Figure 31. Europe Diaper Revenue (USD Million) By Type (2021-2032)

Figure 32. Europe Diaper Revenue (USD Million) By Application (2021-2032)

Figure 33. Europe Diaper Revenue (USD Million) By Product (2021-2032)

Figure 34. Asia Pacific Diaper Revenue (USD Million) By Type (2021-2032)

Figure 35. Asia Pacific Diaper Revenue (USD Million) By Application (2021-2032)

Figure 36. Asia Pacific Diaper Revenue (USD Million) By Product (2021-2032)

Figure 37. South America Diaper Revenue (USD Million) By Type (2021-2032)

Figure 38. South America Diaper Revenue (USD Million) By Application (2021-2032)

Figure 39. South America Diaper Revenue (USD Million) By Product (2021-2032)

Figure 40. Middle East and Africa Diaper Revenue (USD Million) By Type (2021-2032)

Figure 41. Middle East and Africa Diaper Revenue (USD Million) By Application (2021-2032)

Figure 42. Middle East and Africa Diaper Revenue (USD Million) By Product (2021-2032)

By Type

Baby Diapers

Adult Diapers

By Distribution Channel

Supermarkets/ Hypermarkets

Pharmacy Stores

Online Channel

By End-User

Infant

Adult

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)