Dimethyl Sulfoxide Market to Reach $540.1 Million by 2034 at 6.5% CAGR Driven by Pharma-Grade Expansion and Electronics-Grade Demand

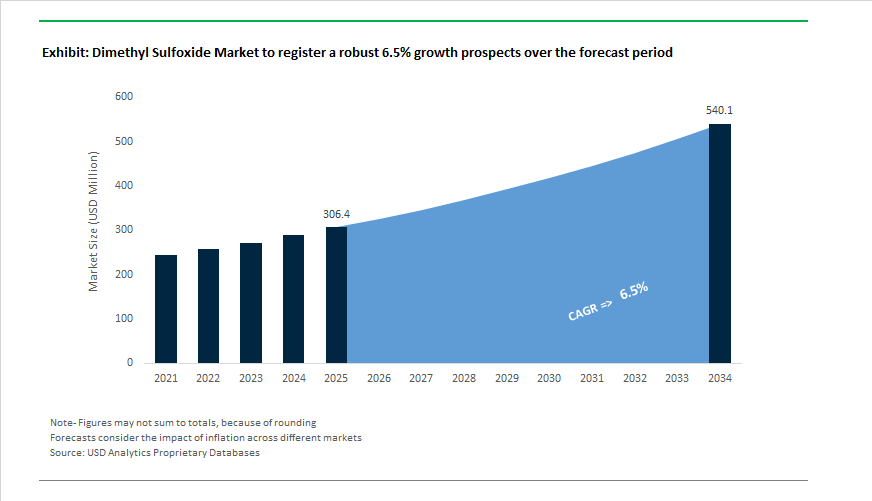

The Dimethyl Sulfoxide (DMSO) Market is projected to grow from $306.4 Million in 2025 to $540.1 Million by 2034, reflecting a CAGR of 6.5%. Growth is anchored in high-purity pharmaceutical solvents, electronic-grade DMSO for semiconductor fabrication, agrichemical formulations, and cryopreservation logistics for advanced biologics. The market has shifted decisively toward regulated, cGMP-compliant production and vertically integrated sulfur oxidation chains to ensure supply reliability and impurity control. Rising compliance standards in China and the European Union during late 2025 further accelerated investment in purification technologies, solvent recovery systems, and trace impurity monitoring to meet stricter environmental and hazard labeling frameworks.

A structural transformation unfolded between 2024 and 2025. In November 2024, gChem, formerly Gaylord Chemical Company, completed a major capacity expansion at its Tuscaloosa, Alabama facility to meet accelerating global demand for pharmaceutical- and electronics-grade DMSO. The expansion preserved the plant’s high automation and safety standards while strengthening global export capabilities. In 2024, gChem achieved back-integration with the commissioning of the world’s first dedicated Nitrogen Tetroxide (N2O4) facility at Tuscaloosa, eliminating reliance on imported oxidants and securing the upstream supply chain for high-grade DMSO synthesis. The company also deployed its AgXalt™ solvent series across regulated agrichemical markets during 2024 following EPA approvals, positioning DMSO as a safer alternative in pesticide and herbicide formulations. In April–May 2025, Gaylord Chemical formally rebranded to gChem, signaling its transition toward green chemistry innovation and pharmaceutical-grade specialization. During the same period, Hubei Xingfa Chemical Group released its 2024 annual performance results in April 2025, highlighting record output and a strategic pivot toward electronic-grade DMSO for China’s domestic semiconductor and display sectors.

Pharmaceutical and advanced therapy demand intensified through 2025. In October 2025, gChem expanded the validation profile of Procipient®, its cGMP-compliant DMSO manufactured under ICH Q7 conditions, targeting the high-growth Antibody-Drug Conjugate market where impurity control directly influences Drug-to-Antibody Ratio reproducibility. Throughout 2025, DMSO solidified its position as the standard cryoprotectant for Cell and Gene Therapy logistics, with Contract Research Organizations bundling cGMP-grade DMSO into formulation packages to streamline regulatory submissions. Arkema reinforced its sustainability roadmap through a 20-year renewable electricity agreement signed during 2024–2026, committing 20 GWh per year beginning in 2026 to power French operations, aligning solvent manufacturing with carbon-reduction mandates. In January 2026, Arkema brought a new transparent polyamide facility online in Singapore, strengthening its footprint in electronics and healthcare markets that rely heavily on high-purity solvent systems.

Distribution consolidation and regulatory evolution further reshaped market dynamics. In October 2025, ChemPoint and Eastman expanded their North American distribution collaboration, reflecting a broader solvent logistics optimization trend to improve supply-chain resilience for high-performance reagents. In late 2025, China’s Ministry of Ecology and Environment and EU regulatory authorities introduced tighter chemical registration and labeling protocols, compelling DMSO manufacturers to invest in advanced distillation, impurity profiling, and closed-loop solvent management systems. These developments, combined with strategic capacity expansions and renewable energy integration, position high-purity and electronic-grade DMSO as central to pharmaceutical innovation, semiconductor manufacturing, and next-generation green solvent applications through 2034.

Trends and Opportunities Defining the Dimethyl Sulfoxide (DMSO) Market

Surging Demand for GMP-Grade DMSO in Cell and Gene Therapy Manufacturing

- The rapid expansion of the global Cell and Gene Therapy pipeline has made GMP-grade DMSO a non-discretionary input rather than a commodity solvent. DMSO remains the industry-standard cryoprotectant for Mesenchymal Stem Cells and other advanced cell therapies due to its proven ability to prevent intracellular ice formation during cryopreservation. Clinical datasets generated between 2024 and 2025 consistently show post-thaw cell viability levels above the 70% threshold required for patient infusion, a benchmark that competing cryoprotectants have struggled to match at scale.

- This demand shift is directly influencing upstream manufacturing investments. In April 2025, gChem announced capacity expansion dedicated to excipient-grade DMSO, targeting compliance with both USP and Ph. Eur. monographs. These upgrades focus on ultra-low endotoxin levels and trace impurity control, which are mandatory for sterile injectable applications. At the same time, Toray Fine Chemicals introduced its DMSO-StG sterilized grade, integrating sterility assurance directly into the manufacturing process. This innovation addresses a critical operational bottleneck for CGT manufacturers by reducing the need for downstream sterilization and supporting Animal-Origin-Free solvent requirements across regulated markets.

Emergence of Green Solvent Alternatives and EHS-Driven Substitution Pressure

- Despite its relatively favorable toxicological profile, DMSO’s high dermal penetration capability and characteristic metabolic odor are driving selective substitution in research, agrochemical, and early-stage discovery workflows. Environmental, health, and safety teams are increasingly cautious about operator exposure risks, particularly in high-throughput laboratory environments.

- Bio-based alternatives are gaining traction in this context. Industrial assessments published in 2025 highlight Cyrene, derived from waste cellulose, as a leading green solvent candidate in polymer processing and antimicrobial drug discovery. Unlike DMSO, Cyrene does not confer reactive oxygen species protection to microbial systems, making it more suitable for screening assays where DMSO can mask compound toxicity or antimicrobial efficacy. In parallel, regulatory alignment with the EU Green Deal is prompting agrochemical formulators to reassess long-term solvent strategies. Industry surveys conducted in early 2025 indicate that nearly 28% of agrochemical companies are actively testing bio-based solvent systems to hedge against future regulatory tightening on petroleum-derived solvents.

Penetration Enhancer for Transdermal and Topical Drug Delivery Systems

- DMSO’s unique ability to reversibly disrupt the lipid architecture of human skin continues to unlock growth in non-invasive drug delivery. Pharmaceutical developers are increasingly leveraging this property to improve systemic absorption of large or poorly soluble molecules that traditionally require injectable administration. Regulatory momentum is reinforcing this trend. During 2024 and 2025, the U.S. Food and Drug Administration approved several topical therapies utilizing penetration-enhancing mechanisms, signaling greater regulatory comfort with advanced transdermal technologies.

- Market intelligence suggests that approximately 46% of personalized medicine R&D programs are now evaluating DMSO-compatible delivery platforms. Clinical studies published in mid-2025 demonstrate that DMSO-based formulations can increase the bioavailability of certain NSAIDs and hormone therapies by up to 31%. This performance profile positions DMSO as a critical enabler within the transdermal patch and topical drug delivery market, which is valued at approximately USD 6 billion and continues to expand across chronic disease management.

Electrolyte Stabilizer in Next-Generation Battery Chemistries

- Beyond life sciences, DMSO is emerging as a functional co-solvent in advanced battery systems where high dielectric constant and chemical stability are essential. In lithium-sulfur batteries, studies published in March 2025 in Electrochimica Acta confirm that DMSO enhances the solubility of long-chain polysulfides. This directly mitigates the shuttle effect, enabling initial specific capacities of 1,093.4 mAh/g, substantially outperforming conventional carbonate electrolyte systems.

- Similarly, in lithium-air battery research, work published in August 2025 highlights the role of DMSO in stabilizing reactive intermediates through the formation of solvated Li(DMSO)₄⁺ ion pairs. This mechanism supports more reversible electrochemical reactions and addresses one of the core technical barriers to commercializing lithium-air batteries. As automotive and grid-scale energy storage developers push toward higher energy density chemistries, DMSO’s role as a specialty electrolyte component represents a high-margin, technology-driven opportunity rather than a volume-led expansion.

Dimethyl Sulfoxide (DMSO) Market Share and Segmentation Insights

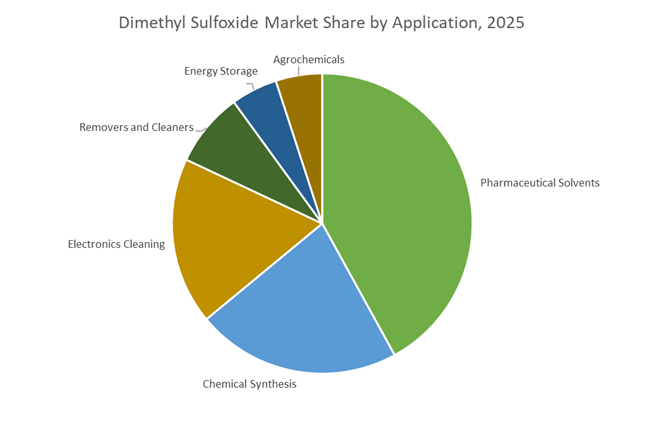

DMSO Market Share by Application : Pharmaceutical Solvents Anchor Demand as Electronics and Energy Storage Expand

Pharmaceutical solvents dominate the dimethyl sulfoxide market in 2025 with 42% share, reflecting DMSO’s unmatched ability to dissolve both polar and non-polar compounds while enhancing transdermal and parenteral drug delivery. Chemical synthesis represents a significant segment, leveraging DMSO as a polar aprotic solvent for nucleophilic substitutions, oxidations, and high-temperature reactions. Electronics cleaning is one of the fastest-growing applications, driven by semiconductor fabrication needs such as photoresist stripping, flux removal, and precision MEMS cleaning. Removers and cleaners also account for meaningful demand, replacing chlorinated solvents in paint stripping and industrial degreasing. Energy storage is emerging as a high-potential niche, with DMSO used in lithium battery electrolytes and materials processing. Agrochemicals remain limited due to cost sensitivity, although specialty formulations increasingly adopt DMSO for enhanced penetration and solvency.

DMSO Market Share by End-User Industry : Pharma and Semiconductors Lead High-Purity Consumption

Pharmaceuticals and biotechnology account for 48% of global DMSO demand, driven by its role in API synthesis, formulation development, cryopreservation, and regenerative medicine cell banking. Electronics and semiconductors form a rapidly growing segment, requiring ultra-high-purity DMSO for wafer cleaning, residue-free processing, and advanced lithography workflows. Research and academia maintain a strong presence, using DMSO extensively in organic synthesis, biological assays, and cell-based studies due to its exceptional solvency and membrane permeability. Automotive and polymer processing contribute steady volume through polymer synthesis and specialty materials manufacturing, where DMSO’s thermal stability is critical. Agrochemicals remain a smaller end-user, primarily confined to premium formulations and R&D applications. Looking ahead, tightening solvent regulations and expanding semiconductor capacity are expected to further strengthen DMSO’s position across high-value industrial ecosystems.

Competitive Landscape of the Dimethyl Sulfoxide (DMSO) Market

The Dimethyl Sulfoxide Market in 2026 is defined by rapid growth in pharmaceutical excipients, cryopreservation media, semiconductor cleaning solvents, battery electrolytes, and agrochemical penetrants. Competitive intensity is rising as suppliers differentiate through ultra-high purity grades, vertical feedstock integration, sustainable solvent platforms, and specialty life-science formulations, with North America, APAC, and Europe acting as the primary demand hubs.

Gaylord Chemical Company leads specialty-grade DMSO through pharma purity and battery innovation

Rebranding to gChem in 2026, Gaylord Chemical Company is the only dedicated DMSO manufacturer in the Western Hemisphere and commands nearly 47% of the global specialty-grade DMSO segment. Its flagship PROCIPIENT® USP and Ph. Eur. DMSO remains the gold standard for drug delivery, cryopreservation, and life-science formulations. In February 2026, gChem announced a strategic collaboration with Hyundai Motor Group to develop DMSO-based electrolyte systems for next-generation solid-state batteries. Under its “Chemistry With a Conscience” strategy, the company launched Miracule, a low-odor medical DMSO platform that improves patient compliance in topical therapies. gChem’s core advantage lies in high-purity manufacturing and human-safe formulations for biotech and advanced energy markets.

Arkema integrates DMSO into polymers, recycling, and advanced battery materials

Arkema Group embeds DMSO across its high-performance polymers, thiochemicals, and recycling technologies, reinforcing its role in premium industrial applications. In early 2026, Arkema tripled global capacity for Rilsan® Clear transparent polyamides, a process heavily dependent on DMSO as a reaction solvent. The company also signed an MoU with Senior plc to advance DMSO-processed electrode coatings for battery separators. Arkema is expanding high-purity solvent and transparent polyamide production in Singapore, targeting Asia’s semiconductor corridor. Its leadership in thermoplastics recycling uses DMSO as a key extraction agent, while industrial cleaning and digital ink stabilization further diversify demand across electronics, polymers, and sustainable materials.

Toray Fine Chemicals dominates electronics-grade DMSO for advanced semiconductor nodes

Toray Fine Chemicals, part of the Toray Group, holds approximately 31.4% of the global high-purity DMSO market, supplying South Korean and Japanese electronics leaders. In 2026, its analytical-grade DMSO became essential for 3nm and 5nm semiconductor fabrication, particularly in precision wafer cleaning. Under Toray’s “Sustainability Innovation” program, DMSO is promoted as a nature-positive alternative to chlorinated solvents in carbon fiber manufacturing. Fully aligned with Toray Sustainability Vision 2050, production integrates with water-treatment membranes and carbon-neutral supply chains. Strategic pricing adjustments in 2025–2026 reflect the premium value of ultra-low metallic content, reinforcing Toray’s leadership in electronics, composites, and high-spec solvent markets.

Hubei Xingfa Chemicals Group scales industrial DMSO through low-cost feedstock integration

Hubei Xingfa Chemicals Group is the global volume leader, expanding total DMSO capacity to 60,000 tons per year in early 2026, positioning itself among the world’s largest single-site producers. Backed by China’s phosphorus and sulfur resources, Xingfa benefits from internal precursor production, insulating margins from global price volatility. The company dominates pesticide and herbicide formulations, where DMSO enhances soil penetration and active efficacy. Its industrial-grade DMSO is widely used in polymers, coatings, and chemical processing due to high solvency and elevated flash point. During 2025–2026, Xingfa transitioned toward “Green Industrial Parks,” deploying advanced wastewater treatment to strengthen sustainability credentials across sulfur-based chemical lines.

Merck KGaA anchors pharmaceutical and research-grade DMSO through global lab infrastructure

Merck KGaA operates as the world’s laboratory backbone for ultra-pure DMSO, supporting cryopreservation, vaccine production, and medicinal chemistry. Its Supelco® analytical and pharma-grade DMSO meets ACS, USP, and Ph. Eur. standards with ≥99.9% purity, making it the most widely used cryoprotectant for stem cells and bone marrow. In early 2026, Merck launched Green Reagent kits, pairing DMSO with bio-based inputs to replace NMP in peptide synthesis. Expansion of its Darmstadt life-science hub now supports rising demand for sterile-filtered DMSO. Integrated with the M-Shop platform, Merck delivers lot-level compliance data for biotech, diagnostics, and pharmaceutical R&D worldwide.

United States: Integrated Supply Security and High-Specification End Use Expansion

The United States dimethyl sulfoxide market has entered a phase of structural reinforcement driven by domestic supply integration and tightening end-use specifications. In 2024–2025, Gaylord Chemical, now operating under the gChem brand, completed optimization of its Tuscaloosa, Alabama complex to achieve fully integrated production of dimethyl sulfide and DMSO. This eliminated reliance on imported intermediates and stabilized domestic availability for 2026, a critical advantage as pharmaceutical, semiconductor, and regulated agricultural applications demand uninterrupted, traceable supply chains. Pricing dynamics also shifted in January 2025, when North American producers implemented a $0.05 per pound increase on technical-grade DMSO, reflecting a 19% rise in sulfur feedstock costs and elevated Gulf Coast logistics expenses.

Demand-side evolution is increasingly application led. In late 2024 and early 2025, the U.S. Environmental Protection Agency approved the AgXalt™ solvent series for regulated agrochemical formulations, explicitly leveraging DMSO’s exceptional solvency and penetration enhancement to improve active ingredient uptake. Pharmaceutical requirements remain even more stringent. Gaylord continues to be the sole producer of PROCIPIENT® DMSO USP and PhEur grades, and in 2025 the company introduced enhanced GC-MS protocols to meet tighter FDA expectations for sterile injectable manufacturing solvents. Beyond life sciences, electronics is emerging as a fast-growing pillar. By 2026, semiconductor manufacturers in Arizona’s Silicon Desert cluster transitioned to DMSO-based photoresist strippers to comply with state-level VOC mandates, accelerating substitution away from N-Methyl-2-pyrrolidone systems and reinforcing DMSO’s role as a regulatory-compliant, high-performance solvent.

China: Circular Sulfur Integration and Electronics-Driven Volume Leadership

China remains the global center of gravity for industrial-grade dimethyl sulfoxide consumption, underpinned by scale, circular chemistry, and electronics manufacturing dominance. Hubei Xingfa Chemicals Group, the world’s largest DMSO producer, reported in its 2024 Annual Report that it has fully operationalized a closed-loop sulfur recovery system at its Yichang fine chemicals park. By-product sulfur from glyphosate production is now recaptured and converted into DMSO, sharply reducing waste and feedstock costs for the 2025–2026 cycle while aligning with China’s circular economy priorities. This integration gives leading producers a structural cost and sustainability advantage that smaller, less efficient plants struggle to replicate.

Regulatory consolidation has reinforced this trend. The enforcement of GB/T 21395-2024 in late 2024 introduced tighter national quality standards for DMSO, accelerating the shutdown of high-emission, sub-scale facilities and concentrating production among large players such as Xingfa and Zhejiang Haibang. Demand growth is increasingly technology driven. In August 2025, Chinese researchers disclosed a DMSO and 1,3-dioxolane electrolyte system for Li/CFx batteries that delivered a 12% energy density improvement over conventional PC/DME blends, positioning high-purity DMSO as a strategic input for next-generation energy storage. At the same time, China accounted for roughly 48% of global industrial-grade DMSO consumption in 2025, largely tied to TFT-LCD flat panel display manufacturing and semiconductor precision cleaning, reinforcing its role as the largest single demand hub worldwide.

France: Specialty Materials Growth Anchored in Decarbonization Finance

France’s DMSO market trajectory is closely tied to specialty materials and decarbonization strategies. Arkema reported in November 2025 that its specialty materials segment, which includes DMSO, achieved approximately 20% year-over-year sales growth in high-technology markets such as advanced batteries and electronics. This performance reflects a deliberate pivot away from commodity exposure toward applications where solvent purity, performance consistency, and regulatory compliance are decisive purchasing factors.

Capital allocation is reinforcing this shift. In the third quarter of 2025, Arkema issued a €500 million green bond to finance decarbonization across its specialty chemical portfolio. Part of this funding is directed toward bio-based feedstock research and energy optimization within the DMSO value chain, supporting compliance with EU Green Deal targets ahead of 2026. Operational discipline is also a core theme. Arkema announced a €100 million cost-saving target for 2025–2026 through optimization of energy-intensive DMSO distillation units at European sites, signaling that efficiency gains and sustainability investments are being pursued in parallel rather than as trade-offs.

India: Regulatory Standardization and Pharmaceutical Supply Chain Resilience

India’s dimethyl sulfoxide market is characterized by policy-driven localization and pharmaceutical supply chain risk management. In 2025, the Department of Chemicals and Petrochemicals included DMSO intermediates within its Production Linked Incentive outreach, aiming to reduce the country’s roughly 35% import dependence for pharmaceutical solvents used in domestic API manufacturing. This initiative reflects a broader strategic push to strengthen self-reliance in critical chemical inputs while supporting India’s position as a global bulk drug supplier.

Regulatory enforcement has tightened accordingly. In early 2025, the Ministry of Chemicals finalized Quality Control Orders for DMSO, mandating Bureau of Indian Standards certification for all imports to ensure suitability for medical and pharmaceutical applications. This has raised compliance thresholds for foreign suppliers while improving confidence among downstream drug manufacturers. Supply chain resilience emerged as a practical driver in 2025 as well. Bulk drug producers in Hyderabad expanded localized storage of pharmaceutical-grade DMSO by 18% to hedge against logistics disruptions linked to Red Sea shipping constraints, underscoring the solvent’s strategic importance in uninterrupted API production.

Germany and the European Union: Compliance Costs and Substitution-Led Demand

In Germany, the DMSO market is being reshaped by regulatory cost pressures and solvent substitution mandates. The European Chemicals Agency confirmed a 19.5% increase in REACH registration fees effective April 1, 2025, materially raising compliance expenses for distributors handling high-volume solvents such as DMSO. This has encouraged consolidation among distributors and favored players with diversified, high-purity solvent portfolios capable of absorbing higher administrative costs.

At the same time, policy direction is creating new demand vectors. Under the progressing One Substance, One Assessment framework targeted for 2026, German industrial cleaning and processing firms are accelerating the replacement of chlorinated solvents with DMSO-based blends to meet stricter EU workplace exposure limits. Distribution networks are expanding to capture this shift. In 2025, OQEMA Group and Merck KGaA strengthened their high-purity solvent logistics capabilities to serve fast-growing cell therapy and cryopreservation clusters in Munich and Berlin. This positions DMSO as a compliance-aligned solvent of choice in advanced biomedical and industrial applications across the EU.

Dimethyl Sulfoxide Market: Country-Level Strategic Snapshot

Dimethyl Sulfoxide (DMSO) Market County Level Snapshot

|

Region

|

Strategic Emphasis

|

Primary Driver

|

Market Implication

|

|

United States

|

Integrated domestic supply

|

FDA, EPA VOC mandates

|

Stable pharma and semiconductor demand with pricing firmness

|

|

China

|

Circular sulfur utilization

|

Electronics and battery manufacturing

|

Volume leadership with cost and sustainability advantages

|

|

France

|

Specialty materials and decarbonization

|

Green bond financing

|

High-margin growth in advanced electronics and batteries

|

|

India

|

Localization and quality enforcement

|

PLI and BIS standards

|

Reduced import reliance and pharma supply security

|

|

Germany / EU

|

Compliance-led substitution

|

REACH and exposure limits

|

Shift toward DMSO as a chlorinated solvent alternative

|

Dimethyl Sulfoxide (DMSO) Market Report Scope

Dimethyl Sulfoxide Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$306.4 Million

|

|

Market Size (2034)

|

$540.1 Million

|

|

Market Growth Rate

|

6.5%

|

|

Segments

|

By Purity Grade (Pharmaceutical Grade, Electronics Grade, Industrial Grade, Battery Grade), By Application (Pharmaceutical Solvents, Electronics Cleaning, Chemical Synthesis, Removers and Cleaners, Agrochemicals, Energy Storage), By End-User Industry (Pharmaceuticals and Biotechnology, Electronics and Semiconductors, Agrochemicals, Automotive and Polymer Processing, Research and Academia)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Hubei Xingfa Chemical Group Co., Ltd., Gaylord Chemical Company, LLC, Arkema S.A., Toray Industries, Inc., Zhejiang Haibang Chemical Co., Ltd., Xingfa Chemicals Co., Ltd., Yanbian Longzheng Chemical Development Co., Ltd., Mitsubishi Gas Chemical Company, Inc., Merck KGaA, Solvay S.A., Hubei Xingrui Chemical Co., Ltd., Zibo Qixiang Tengda Chemical Co., Ltd., Balaji Amines Limited, Tokyo Chemical Industry Co., Ltd., Thermo Fisher Scientific Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Dimethyl Sulfoxide Market Segmentation

By Purity Grade

- Pharmaceutical Grade

- Electronics Grade

- Industrial Grade

- Battery Grade

By Application

- Pharmaceutical Solvents

- Electronics Cleaning

- Chemical Synthesis

- Removers and Cleaners

- Agrochemicals

- Energy Storage

By End-User Industry

- Pharmaceuticals and Biotechnology

- Electronics and Semiconductors

- Agrochemicals

- Automotive and Polymer Processing

- Research and Academia

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Dimethyl Sulfoxide Industry

- Hubei Xingfa Chemical Group Co., Ltd.

- Gaylord Chemical Company, LLC

- Arkema S.A.

- Toray Industries, Inc.

- Zhejiang Haibang Chemical Co., Ltd.

- Xingfa Chemicals Co., Ltd.

- Yanbian Longzheng Chemical Development Co., Ltd.

- Mitsubishi Gas Chemical Company, Inc.

- Merck KGaA

- Solvay S.A.

- Hubei Xingrui Chemical Co., Ltd.

- Zibo Qixiang Tengda Chemical Co., Ltd.

- Balaji Amines Limited

- Tokyo Chemical Industry Co., Ltd.

- Thermo Fisher Scientific Inc.

*- List not Exhaustive