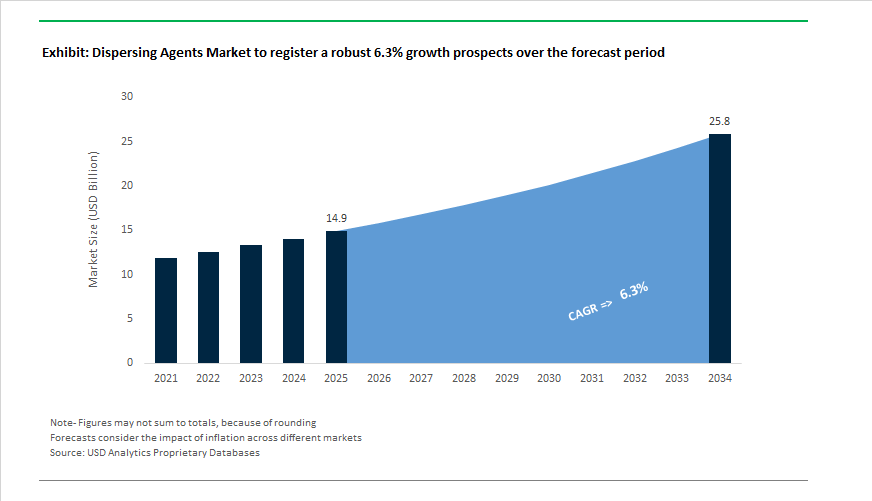

Dispersing Agents Market to Reach $25.8 Billion by 2034 at 6.3% CAGR Driven by CFRP Technology and Bio-Based Additives

The Dispersing Agents Market is projected to expand from $14.9 billion in 2025 to $25.8 billion by 2034, registering a CAGR of 6.3%. Growth is being propelled by rapid adoption of high-performance polymeric dispersants in automotive coatings, architectural paints, digital inks, battery materials, and agrochemicals. In July 2024, Arclin strengthened its North American footprint by acquiring RG Dispersants, enabling vertical integration of specialty dispersing technologies into its construction and industrial resin portfolio. In September 2024, Lubrizol doubled production capacity for its Solsperse™ hyperdispersants at Avon Lake, Ohio, responding to surging demand for high-efficiency pigment dispersion in water-based and 100% active ink systems. These expansions signal a decisive shift toward higher-solids, low-VOC formulations where dispersing efficiency directly impacts gloss development, viscosity control, and long-term stability.

Capacity investments accelerated in Asia through 2025. In early 2025, Borregaard expanded its lignin-based biopolymer output, reinforcing the transition toward renewable dispersing agents in agrochemical and construction markets. In November 2025, BASF commissioned a new high-performance dispersant production line in Nanjing utilizing Controlled Free Radical Polymerization (CFRP) technology. This advanced process enables precise molecular weight distribution and functional group control, producing dispersants optimized for automotive OEM coatings and high-solid industrial systems with a lower Product Carbon Footprint. Lubrizol followed its U.S. expansion with a new Singapore Innovation Center in July 2025 and expanded its Shanghai Innovation Center in February 2026, strengthening region-specific R&D capabilities for Asia-Pacific coatings and personal care markets. Meanwhile, BASF completed the divestment of its decorative paints business to Sherwin-Williams in October 2025, sharpening its focus on supplying dispersing agents and raw materials rather than competing in finished paint segments.

Strategic restructuring and distribution optimization are reshaping competitive dynamics entering 2026. Arkema proposed the divestment of its impact modifiers and processing aids business in December 2025, concentrating capital on higher-margin specialty surfactants and dispersing technologies under its Rheotech and Ethacryl brands. Clariant advanced its CHF 80 million savings initiative through 2025, including selective site closures to offset weaker European industrial demand and redirect resources toward EV and renewable-energy additives. In February 2026, BASF announced a new dispersions line in Mangalore to capture India’s accelerating architectural paints and paper market growth. Evonik streamlined its North American distribution network in February 2026, appointing Palmer Holland and Andicor Specialty Chemicals to enhance technical service and supply continuity for its TEGO Dispers portfolio. The company’s Tailor Made restructuring, implemented through 2026, aims to sustain cost competitiveness in performance additives. At major trade events in February 2026, Arkema showcased unified coating material solutions emphasizing avoided CO2 emissions methodologies, underscoring the structural migration toward waterborne, bio-based dispersing agents as regulatory and ESG pressures intensify across the global dispersing agents market.

Trends and Opportunities Shaping the Dispersing Agents Market

Strategic Backward Integration by Formulators to Secure Supply and Drive Innovation

- Backward integration is accelerating as leading dispersing agent producers seek to insulate themselves from feedstock price volatility, logistics disruptions, and evolving regulatory constraints. Control over upstream raw materials is increasingly viewed as essential for maintaining formulation consistency and developing proprietary performance attributes in premium coatings and functional materials.

- A notable example is Evonik, which completed its fully integrated methionine production hub in Mobile, Alabama in January 2024. While methionine itself is not a dispersant, this investment signals a broader strategic shift toward vertically integrated specialty chemical platforms. The project is expected to reduce internal logistics complexity and lower annual CO₂ emissions by approximately 25,000 metric tons, underscoring how integration supports both cost control and sustainability objectives.

- From a strategic standpoint, backward integration enables companies to engineer next-generation dispersing agents with tightly controlled molecular architectures and reduced lifecycle emissions. Evonik’s 2025 corporate strategy targets more than 50% of total sales from sustainable and innovation-led solutions by 2030, illustrating how supply chain control has become a prerequisite for meeting long-term ESG, margin, and differentiation targets in the dispersing agents market.

Regulatory Push Accelerating Bio-Based and Low-VOC Dispersing Agent Adoption

- Global regulatory frameworks are rapidly shifting from voluntary sustainability guidelines to mandatory compliance regimes, particularly around VOC emissions and persistent substances such as PFAS. This regulatory tightening is forcing immediate reformulation across coatings, construction materials, and industrial formulations.

- In December 2025, the U.S. EPA finalized revisions to Maricopa County Air Quality Department Rule 335, tightening VOC thresholds for architectural coatings. In parallel, the European Chemicals Agency advanced its universal PFAS restriction proposal in August 2025, targeting more than 10,000 substances. These actions are being mirrored in emerging markets, with India’s Ministry of Environment and Urban Affairs releasing a draft mandate in May 2025 requiring all new residential and commercial projects to adopt low-VOC materials compliant with IS 15489 standards by 2026.

- This regulatory convergence is already reshaping supplier portfolios. BASF announced in August 2024 that it would transition exclusively to bio-based ethyl acrylate production from Q4 2024 onward, achieving an estimated 30% reduction in product carbon footprint versus fossil-based equivalents. For dispersing agents, these shifts are accelerating demand for bio-based polymers and low-VOC architectures that deliver equivalent or superior dispersion efficiency without regulatory risk.

Formulation Support for Next-Generation Battery Manufacturing

- As lithium-ion battery gigafactories scale globally, dispersing agents have emerged as a critical bottleneck in electrode slurry formulation. High-purity polymeric dispersants are essential for achieving homogeneous distribution of conductive carbon and active materials in both NMC and LFP chemistries, directly influencing energy density, cycle life, and manufacturing yield.

- A key commercial development came from Cargill, which introduced its Electrosperse™ 4000 series polymeric amide dispersants engineered for NMP-based slurry systems. These dispersants enable higher solids loading while maintaining manageable viscosity, reducing solvent consumption and lowering the energy intensity of electrode drying, one of the most cost-intensive steps in battery cell production.

- Industry analyses indicate that high-performance dispersing agents now account for roughly 60% of the total value within the battery slurry additive segment. Bio-based dispersants are projected to grow at approximately 15% annually through 2028, as battery manufacturers move away from fluorinated chemistries and align with sustainability-driven procurement policies.

Enabling Industrial-Scale Additive Manufacturing and Advanced Ceramics

- The expansion of additive manufacturing from prototyping into serial production is creating a structurally attractive opportunity for dispersing agents capable of stabilizing high-solids powder-in-liquid systems. In metal and ceramic 3D printing processes such as vat photopolymerization and binder jetting, dispersing agents are essential for preventing particle agglomeration, ensuring dimensional accuracy, and achieving high final part density.

- In December 2023, Lithoz GmbH partnered with the Oak Ridge National Laboratory to advance additive manufacturing of non-oxide ceramics. These applications rely heavily on advanced dispersing agents to maintain suspension stability in ceramic-loaded resins, which directly impacts resolution, surface finish, and mechanical performance.

- Parallel investments reinforce the scale of this opportunity. GE committed more than $450 million in 2023 to expand its manufacturing footprint, with a significant share allocated to additive manufacturing technologies. As aerospace, defense, and healthcare applications demand lightweight, high-strength, and defect-free components, dispersing agents are becoming indispensable for achieving the porosity control and material uniformity required for flight-critical and implant-grade parts.

Dispersing Agents Market Share and Segmentation Insights

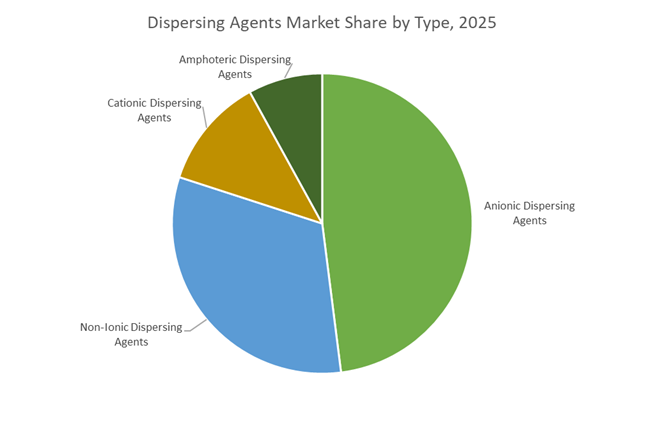

Market Share by Type: Anionic Dispersing Agents Lead Aqueous Systems While Non-Ionic Grades Expand High-Compatibility Formulations

The dispersing agents market by type in 2025 is dominated by anionic dispersing agents, capturing 48% market share, driven by their strong electrostatic stabilization performance in aqueous formulations. These products are widely adopted across paints and coatings, construction materials, and agrochemical formulations, where effective pigment and filler dispersion prevents agglomeration and settling. Non-ionic dispersing agents hold a significant share, valued for steric stabilization and consistent performance across broad pH ranges, making them essential in pharmaceuticals, textiles, and high-performance coatings requiring electrolyte tolerance and formulation compatibility. Cationic dispersing agents remain niche, serving asphalt emulsions, mineral processing, and fabric softeners where positively charged chemistry is required for substrate adhesion. Amphoteric dispersing agents represent a specialty segment, offering dual-charge functionality for personal care and specialty coatings, although higher costs limit large-scale adoption. Growing demand for low-VOC coatings, sustainable dispersants, and advanced formulation stability continues to reshape product development across all chemistry types.

Market Share by Application: Paints and Coatings Dominate as Construction and Agriculture Drive Volume Growth

The dispersing agents market by application is led by paints and coatings, accounting for 35% of global demand in 2025, supported by rising consumption of architectural, industrial, and protective coatings. Dispersing agents play a critical role in pigment stabilization, gloss development, color strength, and long-term storage stability in both waterborne and solvent-based systems. Construction represents a major segment, utilizing dispersants in concrete admixtures, gypsum boards, and tile adhesives to enhance workability, reduce water demand, and improve filler dispersion. Agriculture continues to expand steadily, with dispersing agents ensuring uniform suspension of crop protection actives in pesticide and fertilizer formulations. Oil and gas applications rely on dispersants for drilling fluids and cementing slurries under high-temperature, high-pressure conditions. Textiles show growing adoption for dye uniformity, while pharmaceuticals remain a high-value niche supporting suspension stability and dosage consistency in regulated formulations.

Competitive Landscape of the Dispersing Agents Market

The global dispersing agents market is highly consolidated around innovation-led majors competing on polymeric dispersants, bio-based additives, pigment stabilization efficiency, and regulatory-compliant formulations for coatings, inks, agriculture, ceramics, and electronics. Market leadership in 2026 is defined by R&D depth, sustainability credentials, controlled polymer architectures, and global technical service networks.

BASF SE leads dispersing agents with CFRP polymer design and PCF-transparent portfolios

BASF SE remains the dominant force in the dispersing agents market, leveraging its Verbund integration to control both upstream precursors and downstream specialty additives. Its Efka® and Dispex® brands anchor global demand, with Efka® PX 4360 emerging in 2026 as a benchmark aromatic-free, tin-free solution for solvent-based industrial coatings. BASF now commands an estimated 32% market share in North America, supported by unmatched expertise in Controlled Free Radical Polymerization (CFRP) that enables comb-shaped polymers for ultra-low viscosity pigment stabilization. The company has transitioned its entire European portfolio to Product Carbon Footprint (PCF) transparency while launching bio-ready waterborne dispersants using plant-based feedstocks, reinforcing leadership in sustainable coatings additives.

BYK Additives accelerates premium coatings performance with AI-guided dispersant selection

BYK Additives, part of Altana AG, is one of the most recognized names in polymeric dispersants for automotive, electronics, and high-end coatings. Its flagship DISPERBYK® series remains the industry standard for stabilizing carbon blacks and organic pigments in demanding formulations. During 2025 to 2026, BYK expanded its Digital Additive Consultation, deploying AI tools to help formulators match dispersants with next-generation nano-pigments. The company’s strategy centers on 100% VOC-free additives that enhance gloss and scratch resistance without sacrificing sustainability. With strong penetration across China and South Korea, BYK benefits from rising demand for weather-resistant automotive coatings and advanced electronic finishes.

Clariant strengthens agrochemical and coatings dispersants through biocompatible innovation

Clariant AG continues to expand its footprint in dispersing polymers and surfactant-based additives, serving paints, coatings, and agriculture. Its Dispersogen® and Hostapon® ranges anchor performance, with Dispersogen® PSL 100 in high demand for stable suspension concentrates at low dosage. In late 2025, Clariant reorganized its Adsorbents & Additives division, streamlining its 2026 supply chain and lifting EBITDA margins despite industrial headwinds. The company also introduced a Formulator Toolbox for biological crop protection, featuring biocompatible dispersants that stabilize live microorganisms. Showcased at CAC 2026, Clariant’s expanded Care Chemicals portfolio targets the fast-growing bio-pesticide and sustainable agriculture additives market.

Lubrizol dominates digital inks and ceramics with Solsperse hyperdispersant technology

Lubrizol Corporation, owned by Berkshire Hathaway, is a powerhouse in high-performance dispersing agents for digital printing, ceramics, and advanced materials. Its Solsperse™ Hyperdispersants are widely regarded as best-in-class for achieving low viscosity and high color intensity, particularly in inkjet systems using sub-micron particles. The 2025 to 2026 launch of Solsperse™ AC specifically addresses advanced ceramics applications such as semiconductors, medical implants, and aerospace components. Lubrizol’s deep surface chemistry expertise, including tailored anchor groups for alumina and zirconia, differentiates its portfolio. Strategically, the company is advancing 100% solids and UV-curable dispersant platforms to eliminate solvents.

Evonik advances green dispersing agents with TEGO and renewable biosurfactant platforms

Evonik Industries AG plays a pivotal role in the specialty dispersing agents market, serving waterborne, solvent-borne, and radiation-curable systems through its TEGO® Dispers portfolio. In early 2026, Evonik introduced TEGO® Wet Terra, a renewable biosurfactant line supporting the coatings industry’s green transformation. The company also announced a streamlined U.S. and Canada distribution network effective May 2026, enhancing supply security and technical support. Evonik’s Custom Solutions capability enables tailor-made dispersants for electronics and pharmaceutical applications, while its leadership in silica technology delivers unique matting and dispersion effects. Sustainability-driven innovation and application-specific engineering underpin Evonik’s strong positioning in next-generation coatings additives.

China: CFRP Localization and Scale-Driven Automotive Integration

China’s dispersing agents market is entering a structurally advanced phase, shaped by localization of high-end chemistries and scale expansion in downstream industries. In November 2025, BASF commissioned a high-performance dispersant production line at the Jiangbei New Material Technology Park in Nanjing, leveraging Controlled Free Radical Polymerization technology. This move significantly reduces China’s reliance on imported European dispersants, while improving consistency and molecular weight control required for electronics, coatings, and composite applications. The commissioning aligns closely with the final phase of the Made in China 2025 agenda, under which the Ministry of Industry and Information Technology is incentivizing National Champion chemical firms to achieve 70% domestic content for core specialty additives, including high-purity dispersing agents used in NEVs and advanced electronics.

Automotive and textile demand continue to provide volume stability. With domestic vehicle production projected to reach 35 million units by late 2025, consumption of organic dispersants in engine lubricants has risen sharply, supporting sludge control and fuel efficiency targets. In parallel, China’s leadership in textile dyeing remains a critical anchor. Zhejiang Longsheng Group maintains a dominant regional position in Dispersing Agent MF, supported by vertically integrated production that serves China’s export-oriented textile base. This dual pull from mobility and textiles positions China as both a technology upgrader and a scale stabilizer in the global dispersing agents landscape.

United States: Regulatory Timelines and Low-VOC Reformulation

The United States dispersing agents market in 2025–2026 is being reshaped by regulatory recalibration rather than abrupt restriction. The U.S. Environmental Protection Agency issued an interim final action extending the transition period for the National Contingency Plan Product Schedule to June 10, 2026. This extension affects the conditional listing of chemical dispersants used in oil spill response and gives manufacturers additional time to meet revised toxicity and effectiveness benchmarks. In parallel, TSCA Section 8(d) reporting extensions announced in June 2025 have eased near-term compliance pressure for producers using aromatic intermediates in dispersant formulations, allowing more orderly data submission and reformulation planning.

From a demand perspective, public spending and sustainability targets are reinforcing dispersant adoption. The FY 2025 EPA budget allocation of $100 million for the Diesel Emission Reduction program is driving demand for high-performance dispersants in low-emission engine oils and federally funded construction coatings. At the same time, U.S. producers are accelerating the shift toward low-VOC and bio-based polymeric dispersants to align with the EPA Strategic Plan for 2022–2026. These trends collectively favor multifunctional dispersing agents that deliver performance while meeting tightening air toxics and sustainability expectations.

Germany: REACH-Led Chemistry Shifts and Digital Printing Uptake

Germany’s dispersing agents market is being transformed by regulatory substitution and digital manufacturing trends across the European Union. The adoption of Regulation (EU) 2025/1731 in August 2025 added 16 new CMR substances to REACH Annex XVII, effective September 1, 2025. This regulatory shift has accelerated the replacement of legacy chemistries with safer, polymer-based dispersing agents across coatings, fibers, and inks. The impact is particularly pronounced in applications where solvent stability under alternative, REACH-compliant systems has become a prerequisite.

Innovation in digital printing further strengthens demand. In May 2025, Evonik launched a new range of AERODISP dispersions in Essen, designed specifically for waterborne inkjet receptive coatings. These dispersions enhance dot sharpness and resolution, supporting Europe’s rapid transition from analog to digital printing in packaging and textiles.

India: PLI-Backed Capacity and Infrastructure Pull

India’s dispersing agents market is expanding on the back of domestic capacity creation and strong downstream fundamentals. By 2025, the Production Linked Incentive scheme for specialty chemicals had mobilized investments exceeding ₹1.76 lakh crore, enabling local manufacturers to scale wetting and dispersing agent production for pharmaceutical and agrochemical value chains. This localization effort is reducing dependence on imports while improving formulation control for regulated end uses.

Textiles and construction remain the principal demand engines. With the Indian textile and apparel industry on track to reach $190 billion by 2026, demand for dispersing agents in digital textile printing and uniform dyeing is growing at an estimated 9% annually. Simultaneously, government-led housing initiatives are expected to lift affordable housing availability by 70% through 2026, driving sustained consumption of dispersing agents used in high-workability concrete and cementitious systems. These dual demand streams anchor India’s market in volume growth with increasing quality expectations.

Norway: Bio-Based Dispersants and Battery Materials

Norway occupies a differentiated position in the dispersing agents market through its focus on bio-based chemistries. In early 2025, Borregaard announced a significant capacity expansion for advanced lignin-based biopolymers. These sustainable dispersing agents are increasingly targeted at high-performance applications such as battery electrode slurries, agrochemicals, and construction materials. As Europe intensifies its transition toward circular and low-carbon material systems, Norway’s lignin-derived dispersants are gaining relevance well beyond traditional applications.

Dispersing Agents Market: Country-Level Strategic Snapshot

Dispersing Agents Market County Level Snapshot

|

Country

|

Primary Policy or Market Driver

|

Key Demand Anchors

|

Structural Direction

|

|

China

|

Made in China 2025 localization

|

Automotive lubricants, textile dyeing, NEVs

|

CFRP-based, high-purity domestic supply

|

|

United States

|

EPA and TSCA timeline adjustments

|

Low-emission engines, infrastructure coatings

|

Low-VOC, regulatory-aligned reformulation

|

|

Germany

|

REACH Annex XVII expansion

|

Digital printing, man-made fibers

|

Polymer-based substitution and inkjet growth

|

|

India

|

PLI-led capacity build-out

|

Textiles, housing and infrastructure

|

Import replacement with volume expansion

|

|

Norway

|

Bio-based material innovation

|

Batteries, agrochemicals, construction

|

Lignin-derived, circular dispersants

|

Dispersing Agents Market Report Scope

Dispersing Agents Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$14.9 Billion

|

|

Market Size (2034)

|

$25.8 Billion

|

|

Market Growth Rate

|

6.3%

|

|

Segments

|

By Type (Anionic Dispersing Agents, Non-Ionic Dispersing Agents, Cationic Dispersing Agents, Amphoteric Dispersing Agents), By Structure (Polymer-Based Dispersants, Surfactant-Based Dispersants, Bio-Based Dispersants), By Application (Paints and Coatings, Construction, Agriculture, Oil and Gas, Textiles, Pharmaceuticals, Other Applications), By Form (Liquid, Powder and Granules)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Arkema S.A., Evonik Industries AG, Clariant AG, Altana AG, Dow Inc., The Lubrizol Corporation, Croda International Plc, Solvay S.A., Ashland Inc., Borregaard ASA, Zhejiang Longsheng Group Co., Ltd., Elementis PLC, Kao Corporation, Manali Petrochemicals Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Dispersing Agents Market Segmentation

By Type

- Anionic Dispersing Agents

- Non-Ionic Dispersing Agents

- Cationic Dispersing Agents

- Amphoteric Dispersing Agents

By Structure

- Polymer-Based Dispersants

- Surfactant-Based Dispersants

- Bio-Based Dispersants

By Application

- Paints and Coatings

- Construction

- Agriculture

- Oil and Gas

- Textiles

- Pharmaceuticals

- Other Applications

By Form

- Liquid

- Powder and Granules

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Dispersing Agents Industry

- BASF SE

- Arkema S.A.

- Evonik Industries AG

- Clariant AG

- Altana AG

- Dow Inc.

- The Lubrizol Corporation

- Croda International Plc

- Solvay S.A.

- Ashland Inc.

- Borregaard ASA

- Zhejiang Longsheng Group Co., Ltd.

- Elementis PLC

- Kao Corporation

- Manali Petrochemicals Limited

*- List not Exhaustive