The dog food market is experiencing unprecedented growth and innovation, as global food giants and specialty brands vie to meet evolving consumer demands. In July 2025, WH Group made a significant move by acquiring Pupil Foods, a key Polish producer of wet and dry pet food, signaling WH Group’s determined entry into the European pet food landscape, especially for dogs. This expansion is part of a broader industry trend of strategic acquisitions, with The Nutriment Company a leading UK raw pet food manufacturer also acquiring Natural Instinct in July 2024, consolidating the raw pet food segment and increasing their footprint in natural and fresh dog food products.

Major brands are focusing on the booming fresh and minimally processed dog food segment. General Mills, through its Blue Buffalo brand, launched "Love Made Fresh" in late 2024, entering the fresh pet food space with options that combine the convenience of kibble with the appeal of human-grade, less processed ingredients. This commitment to quality and transparency is further highlighted by General Mills’ U.S. rollout of Edgard & Cooper, a European premium dog food brand acquired in 2024. With this exclusive PetSmart partnership, American pet owners now have access to a wider range of fresh, real-ingredient dog food options, including dry, wet, and treats. Meanwhile, Instinct Pet Food is catering to rising demand for convenient raw diets by introducing "FreshRaw Meals," making it easier for dog owners to provide minimally processed nutrition.

Sustainability, personalization, and dietary diversity are rapidly reshaping the global dog food market. Mars Petcare is partnering with Big Idea Ventures to support startups focused on sustainable pet food ingredients and eco-friendly production, while brands like Wild Earth and V-dog are expanding vegan and plant-based dog food lines for environmentally conscious and hypoallergenic alternatives. Companies such as WOOF are also investing in nutritionally tailored products and educational initiatives, helping owners make informed, personalized nutrition choices for their pets. These efforts collectively highlight how the dog food industry is evolving offering a broader spectrum of products, from raw and fresh to plant-based, and prioritizing sustainability and the individual health needs of dogs worldwide.

The dog food market is undergoing a major transformation with the rise of precision-microbiome formulations designed to address breed-specific health challenges. Unlike conventional diets, these scientifically advanced formulations focus on optimizing gut health through targeted prebiotic and probiotic blends tailored to the unique needs of different breeds. Clinical studies reveal that such formulations significantly reduce symptom recurrence in breeds prone to digestive issues, such as anal gland disorders, providing measurable improvements in overall health and well-being.

Breed genetics also play a critical role in shaping dietary requirements, reinforcing the demand for customized nutrition. For instance, German Shepherds often exhibit sensitivities to certain protein sources like poultry, making them more susceptible to digestive complications if fed standard diets. To address these concerns, leading pet nutrition companies are developing breed-specific recipes enriched with specialized fibers, alternative proteins, and microbiome-supportive ingredients to improve digestive function and nutrient absorption. This trend reflects a broader industry movement toward personalized nutrition solutions, driven by consumer awareness and advancements in genetic and microbiome research.

A significant growth opportunity in the dog food segment lies in the development of prescription renal diets tailored for dogs recovering from exposure to leptospirosis, a disease commonly associated with flood-prone regions. Even when clinical signs of leptospirosis subside, many affected dogs experience underlying kidney damage, increasing the risk of chronic kidney disease over time. Specialized low-phosphorus, kidney-supportive diets can play a vital role in managing this risk and promoting long-term renal health, yet current offerings in the veterinary nutrition market remain limited.

While general renal diets exist, there is a substantial gap in condition-specific formulations designed explicitly for dogs recovering from leptospirosis-related complications. Addressing this unmet need represents a compelling market opportunity for brands willing to invest in targeted nutritional innovations. By combining enhanced palatability, precise mineral balance, and tailored nutrient profiles, companies can create products that not only support recovery but also help veterinarians provide proactive care for at-risk canine populations. With the growing frequency of extreme weather events and related disease outbreaks, this niche is poised to become a high-demand segment within the premium veterinary nutrition market.

The global dog food market is highly competitive, dominated by multinational corporations leveraging advanced nutrition science, strong brand portfolios, and omni-channel distribution strategies. The competitive dynamics are shaped by rising demand for premium, natural, and functional dog food products, consumer preference for customized nutrition, and sustainability-driven innovation. Brands are differentiating themselves through veterinarian-recommended formulas, clean-label positioning, and fresh food offerings, while also focusing on eco-friendly packaging and alternative protein sources. Below is an analysis of the leading players driving growth and transformation in this sector.

Mars Petcare holds a dominant position in the dog food market with an extensive brand portfolio that caters to diverse consumer segments. Pedigree remains a household name in the mass market, offering affordable dry and wet food with complete and balanced nutrition for dogs of all life stages. For premium and specialized care, Royal Canin is the flagship brand, recognized globally for breed-specific and veterinary therapeutic diets developed in collaboration with veterinarians. Iams serves as a mid-tier offering, delivering protein-rich formulas that emphasize digestibility and functional benefits such as weight control and sensitive stomach support. Mars Petcare is setting benchmarks in sustainability, aiming for 100% recyclable packaging and a 25% reduction in virgin plastic usage by 2025, alongside switching to renewable energy across operations. The company also integrates AI-driven health innovations, including predictive tools for disease detection, and invests in pet well-being research through its Waltham Petcare Science Institute. These strategic moves reinforce Mars’ leadership in science-backed nutrition, environmental responsibility, and advanced pet healthcare solutions.

Nestlé Purina PetCare continues to be a formidable force in the dog food segment with its multi-tiered brand architecture. Purina Pro Plan stands at the premium end, offering high-performance and condition-specific diets supported by a team of over 500 scientists. This brand focuses on functional nutrition, such as allergen reduction, digestive support, and cognitive health, making it a trusted choice for pet owners seeking targeted solutions. Beneful serves the mid-tier market with wholesome, flavorful recipes featuring real meat and vegetables, while value-focused Friskies Dog ensures broad accessibility. Nestlé Purina is driving innovation through probiotics-enriched formulas and exploring alternative protein sources to reduce the environmental impact of pet food production. Sustainability remains a priority, with a commitment to 100% recyclable packaging by 2025 and initiatives to enhance ingredient transparency. With its emphasis on research-driven product development, functional health benefits, and eco-conscious practices, Nestlé Purina maintains its competitive edge in the evolving pet nutrition landscape.

Hill’s Pet Nutrition, under Colgate-Palmolive, is globally recognized for its science-led, vet-endorsed product lines, making it a dominant player in the clinical nutrition segment. Hill’s Science Diet provides precise, balanced nutrition for everyday wellness across various life stages and breed sizes, while Hill’s Prescription Diet remains a cornerstone of therapeutic care for managing chronic conditions such as renal disease, urinary issues, obesity, and food sensitivities. Hill’s continues to expand its capabilities through strategic investments, including a $700 million acquisition of three U.S. dry pet food manufacturing plants and the establishment of new canned food facilities to strengthen global supply. The brand also prioritizes sustainability, introducing recyclable packaging in Europe and working toward recycle-ready packaging in the U.S. Partnerships like the collaboration with The Street Dog Coalition further demonstrate Hill’s commitment to social responsibility. With advanced R&D infrastructure, such as the Small Paws Innovation Center, Hill’s sets industry standards for precision nutrition and veterinary integration.

Blue Buffalo has redefined premium dog food with its natural, grain-free, and holistic formulations, excluding corn, wheat, soy, and artificial additives. Its core lines, including BLUE Life Protection Formula, BLUE Wilderness, BLUE Basics, and BLUE Freedom, cater to consumers seeking high-quality protein, limited-ingredient diets, and grain-free options. The company is capitalizing on the fresh pet food trend with the launch of Love Made Fresh in 2025, reinforcing its position in the minimally processed, human-grade segment. Following the acquisition of Edgard & Cooper in 2024, Blue Buffalo expanded into the U.S. fresh pet food market, aligning with rising demand for natural and premium solutions. By embracing sustainable sourcing practices and responding to pet parents’ preference for humanized, clean-label products, Blue Buffalo continues to lead the natural and fresh dog food category, leveraging General Mills’ global distribution strength for accelerated growth.

J.M. Smucker has streamlined its pet portfolio, divesting major dog food brands like Rachael Ray Nutrish in 2023 to sharpen its focus on dog snacks and cat food. Milk-Bone, a flagship brand, remains a dominant name in the treats segment, offering a wide range of crunchy and chewy options for dental health, training, and indulgence. Smucker continues to innovate with functional treats, incorporating flavors, textures, and health benefits that resonate with modern pet owners. By concentrating on snack innovation and brand strength while leveraging robust retail relationships, J.M. Smucker positions itself as a leader in companion pet snacking, aligning with the growing trend of treat-based bonding and functional rewards in pet care.

Dry Dog Food (Kibble) remains the largest product segment with 51.2% market share in 2025, owing to its affordability, convenience in storage, and long shelf life, making it the go-to choice for most pet owners globally. Wet Dog Food continues to maintain strong demand due to its high palatability and suitability for senior dogs. Dog Treats & Chews are witnessing rapid adoption, fueled by premiumization trends and the increasing popularity of functional treats designed for dental health and training. Among emerging categories, Raw Food and Dehydrated/Freeze-Dried Food are the fastest-growing segments, as pet parents shift toward biologically appropriate and minimally processed diets for improved canine health. Veterinary and therapeutic diets also show consistent growth as awareness of pet nutrition and condition-specific formulations expands. Other niche categories such as Frozen Food, Semi-Moist Food, and Powdered Diets remain small but serve specialized dietary needs and offer convenience-driven alternatives for urban pet owners.

Animal-Derived ingredients dominate the market, accounting for the largest share of 74.8% in 2025, supported by their essential amino acid profile and alignment with dogs’ natural dietary requirements. This category continues to anchor mainstream formulations, including premium and grain-free diets. Plant-Derived sources, including pea protein and lentil-based recipes, are steadily gaining traction with the rise of vegan pet food trends and eco-conscious consumers seeking sustainable options. Insect-Derived protein, though a niche today, is the fastest-growing source with an impressive CAGR of 6.9%, driven by sustainability initiatives and regulatory approvals for alternative protein sources such as black soldier fly larvae. These proteins not only offer a high-quality amino acid profile but also present an environmentally friendly solution amid global concerns over resource-intensive meat production.

.png)

The United States dog food market continues to dominate globally, driven by a robust culture of pet humanization and consumer willingness to invest in premium pet nutrition. In 2023, Americans spent $147 billion on pets, with projections reaching $150.6 billion by 2024 a testament to the country's prioritization of pet well-being. The market is seeing explosive growth in premium and human-grade dog food, as more pet owners treat their dogs as cherished family members. Companies like PawCo Foods exemplify the trend toward plant-based innovation with the 2024 launch of "InstaBites" and "LuxBites," leveraging proprietary ingredients and AI for optimal nutrition. JustFoodForDogs also expanded its fresh-frozen, minimally processed products to over 900 PetSmart stores, making fresh options more accessible to mainstream consumers seeking transparency and quality.

Functional dog food targeting specific health needs such as joint health, digestion, allergies, and dental hygiene continues to gain ground. Ingredients like glucosamine and probiotics are increasingly common in everyday formulations, as owners expect more from their dog's diet than basic nutrition. Sustainability is also shaping market evolution, with major players like Mars Petcare and Big Idea Ventures investing in alternative proteins and sustainable food startups to address environmental concerns. This intersection of premiumization, functionality, and responsible innovation ensures the U.S. remains a trendsetter and powerhouse in the global dog food industry.

China’s dog food market is expanding rapidly, buoyed by the urban pet boom and evolving consumer tastes. In 2024, the total pet market reached $41.9 billion, with dog food representing 52.8% of all pet-related spending. Urban households, in particular, are fueling demand for premium, natural, and grain-free dog foods that align with the growing trend of pet humanization. American brands continue to enjoy strong appeal, evidenced by a record $296.6 million in U.S. pet food exports to China in 2024, even as domestic imports as a whole decline underscoring Chinese consumers' trust in the safety and quality of foreign products.

Digital retail is king in China, with platforms like Tmall, Taobao, JD.com, and TikTok driving most dog food sales and offering consumers unprecedented convenience and variety. At the same time, there is a noticeable uptick in consumer confidence in domestic brands, which are rapidly improving product quality and targeting regional taste preferences. As more pet owners seek grain-free and natural formulations for their dogs, brands both international and local are diversifying their offerings to meet these demands and secure a larger share of this highly competitive, digitally enabled marketplace.

Germany’s dog food market stands out for its commitment to quality, sustainability, and nutritional innovation. The sector is seeing increased consolidation, as illustrated by VAFO Group’s acquisition of Allco Tiernahrung and the subsequent creation of VAFO.de in May 2024 demonstrating both local and international investment interest in Germany’s premium pet food industry. German consumers are renowned for their preference for natural, organic, and environmentally responsible products. This is further highlighted by partnerships like that of MicroHarvest and VEGDOG, who are pioneering microbial protein-based treats and emphasizing sustainable, animal-free alternatives.

The premiumization trend is strong in Germany, where 45% of households own at least one pet and seek specialized, high-quality formulations tailored to specific needs. Dog owners look for functional foods with targeted health benefits and are increasingly invested in the environmental impact of their choices. These factors paired with robust innovation in both ingredient sourcing and product development ensure that Germany remains a leader in shaping Europe’s future dog food landscape.

The United Kingdom’s dog food market is thriving thanks to high pet ownership rates 60% of households own pets, with dogs comprising a significant segment and an ongoing shift toward health-conscious, functional foods. The market is experiencing a surge in demand for functional dog treats, offering benefits like dental care, calming effects, and joint support, responding to proactive pet owner concerns about holistic well-being. UK brands are also prioritizing eco-friendly packaging and sustainable sourcing, as ethical and environmental awareness rises among consumers.

The rapid expansion of online retail has transformed how UK consumers access dog food, offering a broad array of specialized, premium, and health-focused products at the click of a button. E-commerce channels are especially important for niche and emerging brands aiming to reach discerning pet owners. These trends, coupled with innovation in product development and responsible business practices, position the UK as a mature and rapidly evolving dog food market.

India’s dog food market is experiencing dynamic transformation, propelled by rising disposable incomes, the humanization of pets, and increasing nutritional awareness among dog owners. Major brands like Godrej Pet Care are investing heavily in domestic market expansion, with a notable Rs 500 crore ($60 million USD) commitment through the launch of "Godrej Ninja" in 2025. Indian pet parents are increasingly seeking premium, grain-free, and protein-rich dog food options, paralleling trends seen in Western markets.

E-commerce has emerged as a vital channel for dog food distribution in India, providing consumers with access to a wide range of products and driving innovation through direct-to-consumer models. Specialized products addressing life-stage nutrition, allergies, digestive health, and breed-specific needs are seeing robust demand. Innovative launches, such as Dogsee Chew’s turmeric and coconut treats, highlight the market’s appetite for new flavors and functional ingredients. This shift toward premiumization, convenience, and evidence-based nutrition signals ongoing market expansion and sophistication.

Brazil’s dog food market is one of the largest and most rapidly growing in Latin America, with pet food accounting for over half of the country’s $12.5 billion pet industry in 2024. The opening of Adimax’s $140 million manufacturing plant in May 2025 has significantly boosted domestic production capacity, reflecting robust market optimism and growth. Pet humanization is exceptionally high in Brazil, with 92% of owners considering their dogs family members driving strong demand for premium and specialized foods tailored to life stage, breed, and health concerns.

Functional dog foods addressing digestion, immunity, skin, and coat health are increasingly popular, aligning with the Brazilian consumer’s focus on visible health outcomes and proactive care. Investments in local manufacturing, innovation, and brand-driven sustainability initiatives further reinforce Brazil’s dynamic market, ensuring continued growth and product diversification in the years ahead.

Australia’s dog food market is shaped by a highly health-conscious and engaged consumer base. Pet owners are increasingly investing in high-quality, specialized nutrition including organic, grain-free, hypoallergenic, and raw diets. Tuckers Natural’s raw food line, introduced in December 2023, and the launch of plant-based dog food by Natural Pet Food Co. in March 2024, exemplify Australian brands’ responsiveness to global trends and environmental concerns.

With pet obesity rates on the rise, brands like Hill’s Science Diet are launching new weight management formulas, addressing specific health issues and catering to informed consumer demand. The combination of raw and fresh options, functional formulas, and growing interest in sustainable sourcing and eco-friendly packaging reflects Australia’s position as a forward-thinking and evolving dog food market.

Japan’s dog food market is uniquely shaped by demographic and cultural trends, most notably its significant aging dog population. This has fueled strong demand for senior-specific dog foods formulated to address joint health, kidney function, and cognitive support. Premium and health-focused ingredients are prioritized by Japanese dog owners, with a strong preference for natural, highly palatable, and texture-varied products including wet and semi-moist foods.

With a large proportion of small dog breeds, Japanese manufacturers focus on appropriate kibble size, digestibility, and tailored nutrition. The market’s attention to quality, palatability, and specific health benefits reflects the meticulous approach of Japanese consumers, making Japan a leader in customized, functional, and premium dog food products in Asia.

|

Parameter |

Details |

|

Market Size (2025) |

$61.6 Billion |

|

Market Size (2034) |

$102.3 Billion |

|

Market Growth Rate |

5.8% |

|

Segments |

By Product (Dry Dog Food (Kibble), Wet Dog Food, Dog Treats & Chews, Dehydrated Food, Freeze-Dried Food, Frozen Food, Raw Food, Semi-Moist Food, Powder, Veterinary Diets/Therapeutic Diets), By Nature (Organic, Natural, Conventional, Monoprotein, Limited Ingredient Diets (LID), Hypoallergenic), By Source (Animal-Derived, Plant-Derived, Insect-Derived), By Application (Puppy, Adult, Senior), By Distribution Channel (Supermarkets & Hypermarkets, Specialty Pet Stores, Veterinary Clinics & Pharmacies, Independent Retailers, E-commerce Platforms, Subscription Box Services) |

|

Study Period |

2019- 2024 and 2025-2034 |

|

Units |

Revenue (USD) |

|

Qualitative Analysis |

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking |

|

Companies |

Mars Petcare Inc., Nestlé Purina PetCare, Hill's Pet Nutrition, Blue Buffalo Company, Ltd., The J.M. Smucker Company, Diamond Pet Foods, WellPet LLC, Canidae, Farmina Pet Foods, Arden Grange, Orijen / Acana (Champion Petfoods - owned By Mars), Simmons Pet Food, Affinity Petcare S.A., Heristo AG, Unicharm Corporation |

|

Countries |

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa |

* List Not Exhaustive

The Dog Food Market report by USDAnalytics offers a comprehensive analysis of market sizing, CAGR, and value projections, presenting critical insights into the drivers, restraints, and evolving trends that define the industry. The study incorporates recent developments such as WH Group’s acquisition of Pupil Foods, Nutriment Company’s consolidation of the raw pet food segment, and high-profile product launches like Blue Buffalo’s "Love Made Fresh" and Instinct Pet Food’s "FreshRaw Meals." Emphasis is placed on emerging dynamics including fresh and human-grade dog food, sustainable packaging, personalized nutrition, plant-based innovation, and breed-specific formulations.

Segment coverage includes product types (dry dog food, grain-free/traditional kibble, wet food, treats & chews, raw/freeze-dried/dehydrated/frozen/semi-moist foods, powders, veterinary and therapeutic diets), nature (organic, natural, conventional, monoprotein, limited ingredient diets, hypoallergenic), source (animal-derived, plant-derived, insect-derived), application (puppy, adult, senior), and distribution channels (supermarkets, specialty pet stores, veterinary clinics, independent retailers, e-commerce, subscription box services).

The report profiles leading companies such as Mars Petcare, Nestlé Purina PetCare, Hill’s Pet Nutrition, Blue Buffalo, J.M. Smucker, Diamond Pet Foods, WellPet LLC, and more. It covers historical data from 2021–2024 and provides forecasts from 2025–2034, enabling actionable insights for strategic decision-making.

Geographic analysis spans North America (US, Canada, Mexico), Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia), South America (Brazil, Argentina), and Middle East & Africa (Saudi Arabia, UAE, South Africa, Egypt, and others). The report is tailored for industry professionals, delivering detailed market intelligence on competitive landscape, innovations, market segmentation, and future outlook in the global dog food industry.

Table of Contents: Dog Food Market

1. Executive Summary

2. Dog Food Market Landscape & Outlook (2025–2034)

3. Innovations Driving Growth in the Dog Food Market

4. Competitive Landscape: Dog Food Market

5. Market Share and Segmentation Insights: Dog Food Market

6. Country Analysis and Outlook of Dog Food Market

7. Dog Food Market Size Outlook by Region (2025-2034)

8. Company Profiles: Leading Players in the Dog Food Market

9. Methodology

10. Appendix

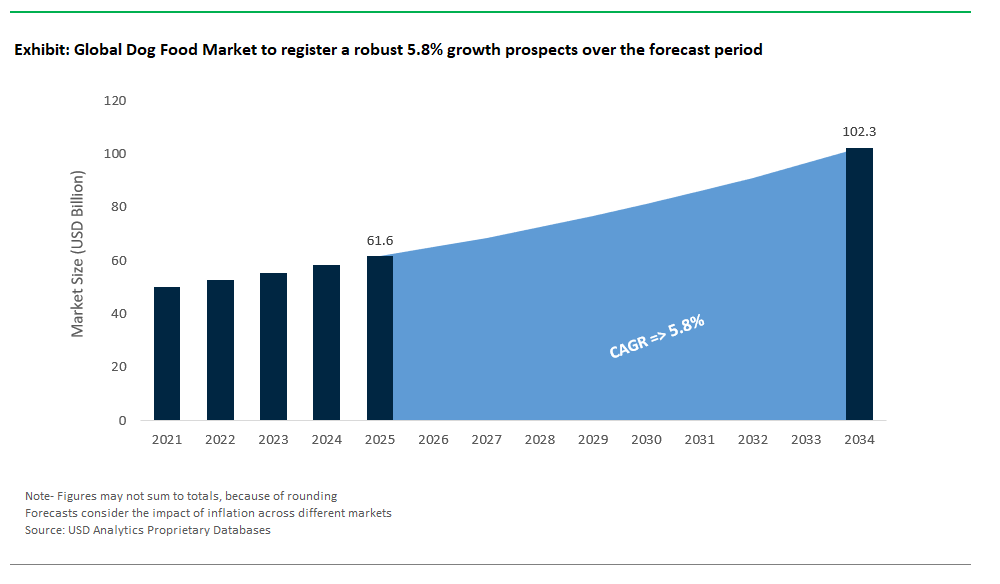

The global dog food market is valued at $61.6 billion in 2025 and is projected to reach $102.3 billion by 2034, growing at a CAGR of 5.8% during the forecast period.

Key trends include the rise of fresh and minimally processed dog foods, personalized and breed-specific nutrition, sustainable and plant-based ingredients, and increased adoption of digital retail channels.

Dry dog food (kibble) maintains the largest share due to its convenience and affordability, while raw, freeze-dried, and functional treats are experiencing rapid growth among health-conscious pet owners.

North America and Europe dominate with established brands and premiumization, while China, India, and Brazil are seeing the fastest growth driven by urbanization, e-commerce, and rising pet ownership.

Top companies include Mars Petcare, Nestlé Purina PetCare, Hill’s Pet Nutrition, Blue Buffalo (General Mills), The J.M. Smucker Company, Diamond Pet Foods, WellPet LLC, and others, all actively shaping innovation and global expansion.