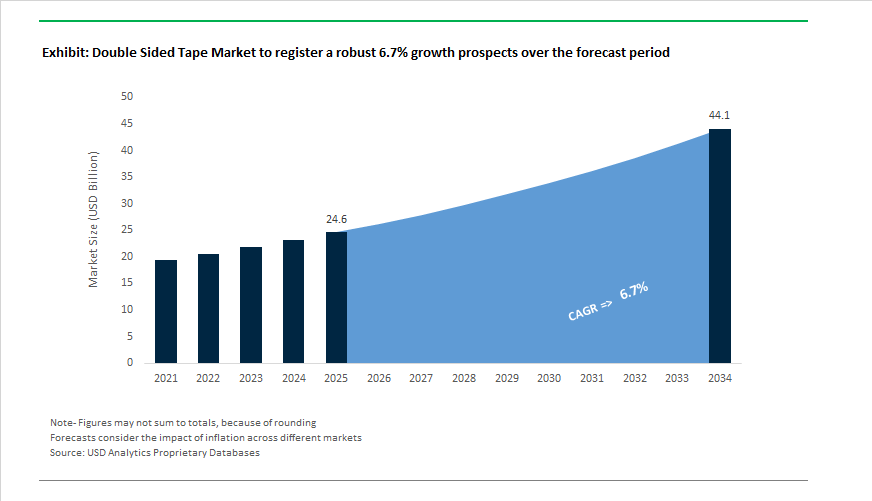

Double Sided Tape Market to Reach $44.1 Billion by 2034 at 6.7% CAGR Driven by EV Lightweighting and Sustainable PSA Innovation

The Double Sided Tape Market is projected to expand from $24.6 billion in 2025 to $44.1 billion by 2034, registering a CAGR of 6.7%. Growth is being propelled by structural shifts toward lightweight assembly, solvent-free pressure-sensitive adhesives (PSAs), and automated manufacturing in automotive, electronics, solar, and construction industries. In February 2024, Avery Dennison launched a portfolio of nearly 40 PSA tape solutions for appliances, engineered to enhance Noise, Vibration, and Harshness (NVH) damping while replacing mechanical fasteners in refrigerators and washing machines. This early move reflected the broader transition from screws and rivets to high-bond acrylic and rubber-based double sided tapes for cleaner aesthetics and reduced assembly time. In September 2024, LG Chem expanded its automotive adhesive unit in North America, focusing on thermally conductive double sided tapes for EV battery modules. With more than 180 patents in adhesive technologies, the company is positioning tapes as structural enablers of EV lightweighting and thermal management.

Sustainability and portfolio consolidation accelerated through 2025. In April 2025, Avery Dennison introduced UV-resistant double sided PSA tapes specifically designed for solar panel bonding, eliminating mechanical fasteners in photovoltaic module assembly and supporting the U.S. target of 30% domestic solar production by 2030. In May 2025, 3M outlined its medium-term growth strategy following the 2024 spinoff of Solventum, reaffirming focus on industrial tapes and adhesives while declaring a $0.73 quarterly dividend. The company simultaneously launched ScotchBlue™ PROSharp™ and advanced bio-based PSA R&D initiatives. Meanwhile, Lohmann was named Future Company 2025 in November 2025, recognizing its DuploCOLL® LE range, which leverages solvent-free TwinMelt® UV-acrylate technology to meet strict electric vehicle cabin air-quality standards. Sustainable material innovation extended to release liners; Avery Dennison rolled out rBG Pure recycled liners during 2024–2025, reducing the carbon footprint of tape carrier systems in European and North American markets.

Strategic acquisitions and capacity optimization intensified in 2026, reinforcing competitive realignment across the double sided tape industry. In January 2026, Henkel signed an agreement to acquire ATP Adhesive Systems, a Swiss specialist with 90% water-based, low-VOC tape solutions, strengthening Henkel’s position in environmentally compliant automotive, electronics, and medical bonding applications. Nitto Denko was recognized as a Clarivate Top 100 Global Innovator in January 2026, underscoring its leadership in precision electronics tapes and medical adhesive patches. The same month, Scapa Industrial introduced new sheathing tapes (Scapa 625/627/637) engineered for construction insulation in harsh environments. Consolidation continued with Shurtape Technologies’ acquisition of Pro Tapes & Specialties in late 2024, enhancing specialty production capacity for entertainment and industrial markets, while Silgan and other global packaging players expanded sustainable dispensing technologies that complement adhesive bonding systems. These developments highlight the sector’s evolution toward high-performance, low-emission, and digitally optimized bonding architectures across industrial verticals.

Trends and Opportunities in the Double-Sided Tape Market

Material Science Innovation for Electrically Conductive Adhesive Tapes in Miniaturized Electronics

- Rapid miniaturization in 5G smartphones, wearables, and medical electronics has rendered mechanical fasteners and solder joints less viable due to space constraints, heat sensitivity, and signal interference risks. Double-sided electrically conductive adhesive tapes are emerging as multifunctional solutions that combine bonding, grounding, and EMI shielding in a single layer.

- In late 2024, 3M expanded its Electrically Conductive Adhesive Transfer Tape portfolio for grounding and EMI management in 5G smartphones. These tapes provide controlled conductivity across XY and Z axes, enabling OEMs to reduce device thickness by up to 0.5 mm while preserving high-frequency signal integrity. This form factor advantage is critical as flagship smartphones and wearables push toward sub-7 mm profiles.

- Advances in nanomaterial integration are accelerating adoption. The incorporation of graphene and carbon nanotubes into adhesive matrices has enabled volume resistivity levels below 0.05 ohm-centimeter, allowing double-sided tapes to function as both structural bonds and electrical pathways in flexible printed circuits. According to 2025 industrial deployment data from TE Connectivity, conductive tape-based grounding solutions in medical diagnostic equipment reduced assembly labor time by 22% by eliminating precision soldering on heat-sensitive sensor modules. This productivity gain is positioning conductive double-sided tapes as a default choice in automated electronics assembly lines.

Regulatory-Driven Shift Toward Solvent-Free and Low-VOC Adhesive Formulations

- Environmental regulation is forcing a rapid reformulation of pressure-sensitive adhesive systems used in double-sided tapes. Updates to EU REACH and new U.S. EPA VOC limits are accelerating the industry-wide transition toward water-based acrylics and hot-melt technologies.

- In December 2025, the U.S. Environmental Protection Agency finalized revisions to Maricopa County Rule 335, significantly tightening VOC emission thresholds for industrial coating and tape manufacturing. This action has accelerated the phase-out of toluene and xylene solvents across North American adhesive production.

- Major manufacturers are already responding at scale. Avery Dennison and Henkel have expanded water-based acrylic emulsion platforms, which represented more than 45% of their total adhesive production volume by late 2025. These formulations achieve approximately 99% lower VOC emissions compared with 1990 benchmarks while maintaining the shear strength required for industrial nameplates, electronics labels, and automotive trim bonding.

- Biodegradability is emerging as the next competitive frontier. In January 2025, Power Adhesives launched Tecbond 214B, the first certified fully biodegradable hot-melt adhesive containing 45% bio-based content. Such innovations are increasingly specified by electronics and consumer goods OEMs as part of their 2030 circular economy and net-zero roadmaps.

Enabling Automated Assembly and Lightweighting in Electric Vehicle Battery Systems

- Electric vehicle platform redesign is creating a structurally durable growth opportunity for high-performance double-sided tapes. The shift toward cell-to-pack battery architectures is reducing reliance on bolts and liquid adhesives, elevating tapes to structural and safety-critical components.

- In November 2025, Avery Dennison introduced specialized electrode fixing tapes for EV battery cells. These products are engineered to withstand electrolyte exposure while delivering thinner profiles than mechanical clips, supporting higher energy density and simplified assembly.

- Beyond battery packs, EV infrastructure is also tape-intensive. The U.S. Department of Energy estimates that 1.25 million public charging ports will be required by 2030, each utilizing dielectric double-sided tapes for internal component mounting to prevent electrical arcing and vibration-induced failures.

- Performance benefits are quantifiable. Modern acrylic foam tapes used in EV batteries, including compressible architectures developed by 3M, accommodate expansion and contraction of pouch cells during charge cycles. This stress compensation has been shown to reduce mechanical load on cooling plates by up to 15 %, directly contributing to extended battery lifespan and improved thermal management reliability.

Facilitating Building-Applied Photovoltaics in Smart Construction

- The expansion of building-applied photovoltaic systems is opening a high-margin application space for UV-stable, long-life double-sided tapes. High-performance Very High Bond acrylic tapes are increasingly used to mount solar panels directly onto building skins without drilling, preserving water-tightness and eliminating thermal bridges.

- Across the European Union, where energy efficiency regulations accelerated BAPV adoption during 2024 and 2025, tape-based mounting systems reduced installation time on metal roofs by approximately 40% compared with traditional rail-based systems. This speed advantage is particularly attractive for retrofit projects in dense urban environments.

- With the global BAPV market projected to approach USD 18.5 billion by 2032, demand is rising for acrylic-based double-sided tapes capable of maintaining bond integrity for more than 20 years under continuous UV exposure, wind loading, and temperature cycling. These performance requirements are shifting procurement decisions away from commodity fastening solutions toward engineered adhesive systems, reinforcing the long-term growth trajectory of the double-sided tape market.

Double Sided Tape Market Share and Segmentation Insights

Foam-Backed Double Sided Tapes Lead Structural Bonding and Gap-Filling Applications

Foam-backed double sided tapes account for 38% of the global market share in 2025, reflecting their critical role in applications requiring conformability, vibration damping, and stress distribution. Acrylic and polyethylene foam tapes are extensively adopted in automotive exterior trim attachment, electronics assembly, and building and construction projects where bonding dissimilar substrates is essential. Their ability to compensate for surface irregularities and differential thermal expansion makes them a preferred alternative to mechanical fasteners and liquid adhesives. Film-backed double sided tapes hold a strong secondary position, offering high tensile strength, temperature resistance, and dimensional stability for electronics bonding, graphic mounting, and precision die-cut applications. Paper and tissue-backed tapes remain important in cost-sensitive industrial uses such as splicing, packaging, and light-duty mounting. Meanwhile, transfer tapes are gaining momentum, particularly in electronics and medical device assembly, due to their ultra-thin bond lines and precise thickness control.

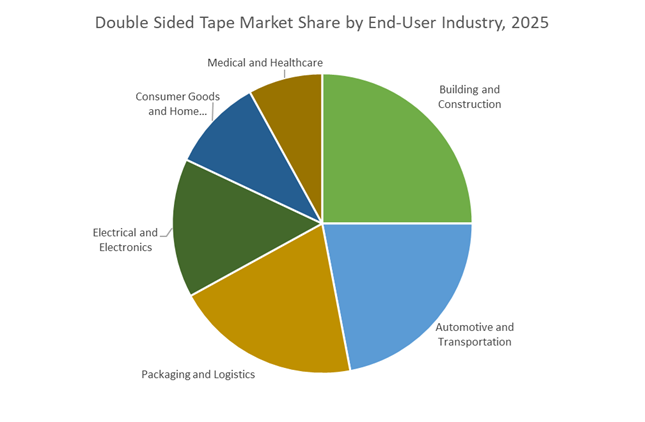

Building and Construction Drives Volume Demand Across Multiple Tape Formats

The building and construction sector represents 25% of total double sided tape consumption, making it the largest end-user industry in 2025. Demand is driven by widespread use in architectural cladding, window installation, signage, floor marking, and temporary fastening during construction activities. Foam-backed tapes are increasingly replacing screws and rivets, delivering improved aesthetics, reduced installation time, and enhanced load distribution. Automotive and transportation applications form a major secondary segment, utilizing double sided tapes for trim attachment, mirror bonding, emblem mounting, and interior assembly to reduce vehicle weight and eliminate corrosion risks. Packaging and logistics rely heavily on paper-backed and transfer tapes for carton sealing and pallet stabilization in high-volume operations. Electrical and electronics manufacturing continues to expand tape usage for display mounting and battery attachment, while medical and healthcare applications remain specialized, demanding biocompatibility, sterilization resistance, and regulatory compliance.

Competitive Landscape of the Double Sided Tape Market

The global double sided tape market in 2026 is defined by innovation in acrylic foam tapes, pressure-sensitive adhesives (PSA), EV assembly bonding, electronics miniaturization, and sustainable adhesive technologies, with competition centered on performance, automation readiness, and recyclability.

3M drives structural bonding leadership with VHB™ and sustainable PSA innovation

3M Company remains the undisputed leader in the double sided adhesive tape market, anchored by its iconic VHB™ (Very High Bond) acrylic foam series that replaces rivets and welds across construction, aerospace, and automotive manufacturing. In late 2024 to early 2025, 3M launched sustainable pressure-sensitive adhesives using recycled and bio-based content, aligning with 2026 Green Building mandates. Its 300LSE low surface energy tapes enable immediate handling strength in automated EV battery assembly lines, supporting lightweighting strategies. With unmatched application versatility, 3M supplies tapes for medical wearables, high-heat engine compartments, and industrial automation, backed by one of the world’s largest adhesive R&D infrastructures.

tesa SE strengthens Europe’s industrial tape ecosystem with ACXplus and solvent-free production

tesa SE, a subsidiary of Beiersdorf, dominates Europe’s specialty double sided tape market, particularly in automotive and electronics. Its tesa® ACXplus acrylic foam tapes deliver permanent outdoor mounting and thermal expansion compensation for architectural panels and vehicle trim. Under its Sustainability Agenda 2030, tesa is targeting 100% solvent-free production across European plants by end-2026. The company leads smartphone assembly, supplying ultra-thin tapes below 100 µm for bezel bonding and battery fixing in foldable devices. Strategic investments in Asia-Pacific manufacturing hubs position tesa to capture demand from regions representing 41.8% of global electronics production.

Nitto Denko accelerates EV and electronics growth through high-purity specialty tapes

Nitto Denko Corporation follows its “Global Niche Top” strategy, focusing on high-value double sided tapes for displays, semiconductors, and electric vehicles. Nitto is a primary supplier of electronics-grade bonding tapes for advanced display panels and chip processing. During 2025–2026, it expanded its HumanFlags portfolio, introducing breathable, residue-free medical tapes for diagnostics and skin-contact sensors. Deep integration into EV propulsion and battery cooling systems enables delivery of thermal-gap-filling adhesive tapes critical for next-generation thermal management. Its Sanshin philosophy, combining new products with new applications, continues to unlock premium demand across healthcare, electronics, and mobility.

Avery Dennison expands functional tape portfolio for construction and circular packaging

Avery Dennison Corporation leverages its expertise in pressure-sensitive materials to bridge bonding and labeling technologies. After integrating CCL Industries’ label and graphics business in early 2025, Avery strengthened its packaging and retail display presence. In 2026, its Performance Tapes division posted strong growth in modular and prefabricated housing, driven by high-tack construction tapes. The Core Series™ portfolio simplifies industrial tape selection by adhesive chemistry (acrylic, rubber, silicone). Avery also launched tension-release double sided tapes in 2026, enabling clean separation during recycling, supporting circular packaging initiatives and brand sustainability targets.

Henkel delivers system-level adhesive solutions for electronics, packaging, and medical wearables

Henkel AG & Co. KGaA competes through its vast Adhesive Technologies division, emphasizing integrated bonding systems rather than standalone tapes. At LOPEC 2026, Henkel introduced conductive double sided tapes that provide both adhesion and electrical pathways for printed electronics. Its TECHNOMELT® hotmelt and LOCTITE® acrylic tape ranges serve security packaging and high-speed e-commerce lines. Henkel’s Partner Ecosystems strategy delivers “Tape-on-Demand” automation for industrial customers. In healthcare, Henkel’s bio-compatible tapes play a vital role in medical wearables, including continuous glucose monitoring sensors requiring long-term skin adhesion.

Scapa (Mativ) targets niche healthcare and industrial bonding with customized tape systems

Scapa Group, now part of Mativ Holdings, operates as a specialty double sided tape provider for healthcare and demanding industrial applications. Scapa offers transfer tapes and unsupported adhesive constructions delivering ultra-low-profile finishes for luxury electronics and technical goods. Known as a niche market specialist, the company excels in customized solutions for cable wrapping and aerospace insulation. In early 2026, Scapa released an updated Double Sided Product Guide, highlighting new silicone-based systems for low surface energy substrates like silicone rubber. Leveraging Mativ’s global footprint, Scapa is expanding medical-grade tape distribution across Latin America.

United States: Solar Manufacturing Pull and EV-Grade Adhesive Engineering

The United States double sided tape market in 2025–2026 is being reshaped by federal clean energy priorities, electric vehicle lightweighting, and a decisive shift toward solvent-free adhesive technologies. In April 2025, Avery Dennison introduced a dedicated Solar Panel Bonding Portfolio engineered to replace mechanical fasteners in photovoltaic modules. This launch directly aligns with national objectives to achieve 30% domestic solar panel production by 2030 and has elevated demand for pressure-sensitive adhesive tapes that deliver long-term UV stability, creep resistance, and rapid assembly. Parallel to this, tesa committed a $36 million investment to expand its Sparta, Michigan facility in 2025, integrating eco-efficient production technologies to support automotive and construction demand across North America.

Technology differentiation is accelerating. 3M has advanced its proprietary solvent-free adhesive coating process for the GPT-020 and VHB Extrudable Tape families, materially reducing CO2 equivalents per square meter while improving energy efficiency. These ultra-high-bond tapes are now central to EV assembly lines, enabling immediate handling strength and reliable bonding of dissimilar substrates such as aluminum and composites. On the regulatory front, updated TSCA Section 8(d) requirements mandating health and safety data submissions by May 22, 2026 are pushing U.S. manufacturers toward higher-transparency, electronics-grade, and medical-grade adhesive systems.

China: NEV Localization and Ultra-Thin Electronics Tapes

China’s double sided tape industry is moving rapidly up the value chain, driven by New Energy Vehicle localization and consumer electronics miniaturization. In 2025, the Ministry of Industry and Information Technology prioritized domestic production of high-performance tapes for NEV battery packs. Manufacturers are scaling flame-retardant double sided tapes that combine electrical insulation with thermal management, a critical requirement as battery energy densities increase. This policy-driven demand has strengthened domestic capabilities in acrylic and modified rubber adhesive chemistries tailored for automotive safety standards.

Simultaneously, China’s dominance in foldable smartphones and compact consumer devices is reshaping tape specifications. Tape converters have commercialized ultra-thin PET-based tapes in the 0.01 mm to 0.03 mm range to support fingerprint-proof shielding and LCD module fastening for 2025–2026 device cycles. Sustainability regulations are reinforcing this transition. The 2025 Green Packaging Regime has accelerated the phase-out of non-recyclable carriers, resulting in a marked capacity expansion for paper-based and bio-based adhesive carriers, particularly within Zhejiang’s industrial clusters.

India: Manufacturing Localization and Infrastructure-Led Demand

India is emerging as a structurally important growth market for double sided tapes, supported by localization incentives and strong downstream demand. In late 2024, tesa inaugurated strategic hubs in Mumbai and Bengaluru to serve electronics and automotive corridors, while its Chennai facility transitioned to self-sufficient solar power operations. This reflects a broader shift toward sustainable manufacturing practices among global tape suppliers operating in India.

Policy support is equally influential. The Production Linked Incentive scheme for specialty chemicals has mobilized over ₹1.5 lakh crore into domestic value chains through 2025, enabling Indian manufacturers to scale high-tack acrylic double sided tapes for e-commerce packaging and logistics automation. Infrastructure expansion adds another demand pillar. With construction activity growing at roughly 9% through 2025, structural glazing tapes and double sided foam tapes are increasingly specified in modular and prefabricated building systems, where speed of installation and load distribution are critical.

Germany: Bio-Based Adhesives and Automated Bonding Systems

Germany’s double sided tape market is shaped by sustainability regulation and advanced industrial automation. Lohmann has launched the DuploCOLL ECO range featuring bio-based, solvent-free adhesives designed for automotive interiors. These products align with the EU’s 2026 Packaging and Packaging Waste Regulation and reflect a broader industry pivot toward low-emission bonding solutions without compromising performance.

Operational efficiency is another defining theme. German manufacturers are integrating automated bonding systems from 3M and Nordson into assembly lines. This hybrid approach combines double sided tape application with precision liquid dispensing, reducing manual labor requirements by an estimated 15% and improving consistency in high-throughput manufacturing environments.

Japan: Electronics-Grade Precision and Halal-Compliant Expansion

Japan continues to lead in electronics-grade double sided tapes, with a strong emphasis on purity, thermal management, and niche compliance standards. Nitto Denko has concentrated 2025 R&D on sebum-resistant and high-thermal-conductivity tapes such as the TR-5310EX series, engineered to dissipate heat from dense circuit boards in 5G infrastructure and wearable electronics. These requirements are elevating performance thresholds for Japanese suppliers relative to global peers.

In parallel, Japanese firms are tailoring products for export growth in Southeast Asia. The introduction of Halal-certified double sided tapes, including dedicated HL-series products, ensures the absence of animal-derived components in both adhesives and carriers. This compliance-driven innovation is strengthening Japan’s competitive position in Muslim-majority markets where regulatory and cultural conformity directly influences procurement decisions.

Double Sided Tape Market: Country-Level Strategic Snapshot

Double Sided Tape Market County Level Snapshot

|

Country

|

Primary Growth Driver

|

Key Applications

|

Strategic Direction

|

|

United States

|

Solar manufacturing and EV assembly

|

Solar modules, EV lightweighting, medical electronics

|

Solvent-free, high-transparency adhesives

|

|

China

|

NEV localization and electronics miniaturization

|

Battery packs, foldable devices

|

Ultra-thin, flame-retardant, recyclable tapes

|

|

India

|

PLI-driven localization and infrastructure build

|

E-commerce, construction glazing

|

Capacity scaling and cost-efficient acrylics

|

|

Germany

|

Sustainability regulation and automation

|

Automotive interiors, industrial assembly

|

Bio-based tapes and automated bonding

|

|

Japan

|

High-purity electronics and export compliance

|

5G, wearables, specialty exports

|

Thermal management and Halal-certified products

|

Double Sided Tape Market Report Scope

Double Sided Tape Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$24.6 Billion

|

|

Market Size (2034)

|

$44.1 Billion

|

|

Market Growth Rate

|

6.7%

|

|

Segments

|

By Resin Type (Acrylic, Rubber, Silicone), By Backing Material (Foam-Backed, Film-Backed, Paper and Tissue, Transfer Tape), By Technology (Solvent-Based, Water-Based, Hot-Melt, UV-Curable), By End-User Industry (Automotive and Transportation, Electrical and Electronics, Building and Construction, Packaging and Logistics, Medical and Healthcare, Consumer Goods and Home Appliances)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M Company, Nitto Denko Corporation, tesa SE, Avery Dennison Corporation, Lintec Corporation, Intertape Polymer Group, Lohmann GmbH & Co. KG, Scapa Group Ltd, Berry Global, Inc., Orafol Europe GmbH, Nichiban Co., Ltd., Adchem Corporation, Shurtape Technologies, LLC, DIC Corporation, Yem Chio Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Double Sided Tape Market Segmentation

By Resin Type

By Backing Material

- Foam-Backed

- Film-Backed

- Paper and Tissue

- Transfer Tape

By Technology

- Solvent-Based

- Water-Based

- Hot-Melt

- UV-Curable

By End-User Industry

- Automotive and Transportation

- Electrical and Electronics

- Building and Construction

- Packaging and Logistics

- Medical and Healthcare

- Consumer Goods and Home Appliances

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Double Sided Tape Industry

- 3M Company

- Nitto Denko Corporation

- tesa SE

- Avery Dennison Corporation

- Lintec Corporation

- Intertape Polymer Group

- Lohmann GmbH & Co. KG

- Scapa Group Ltd

- Berry Global, Inc.

- Orafol Europe GmbH

- Nichiban Co., Ltd.

- Adchem Corporation

- Shurtape Technologies, LLC

- DIC Corporation

- Yem Chio Co., Ltd.

*- List not Exhaustive